Biofuels denote any energy commodity directly sourced from plants or animals. Examples that have featured in our research include ethanol, bio-diesel from agricultural oils, renewable diesel from waste oils, landfill gas, biogas, woody biomass and BECCS. We can consider 10GTpa of global food production in this category as well as a type of biofuel.

A general finding in our biofuels research is high variability. Capturing waste materials can be most economical and often has the best carbon credentials. Especially when these waste materials would otherwise have degraded; and the processing is simple, with low thermodynamic losses from upgrading and conversion.

Another general finding in our biofuels research is that opportunity costs matter. For example, there are examples of some biofuels crops where the same land could capture or store more carbon, via nature-based CO2 removals.

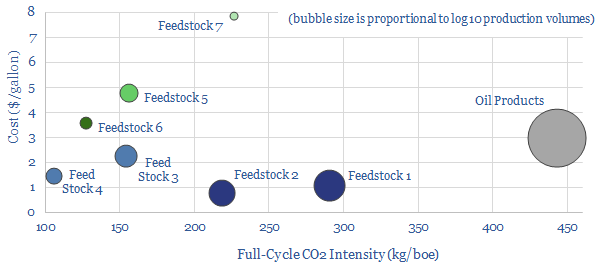

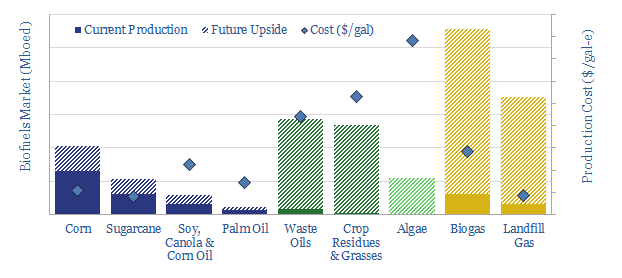

This data-file provides an overview of the 3.5Mbpd global biofuels industry, across its main components: corn ethanol, sugarcane ethanol, vegetable oils, palm oil, waste oils (renewable diesel), cellulosic biomass, algal biofuels, biogas and landfill gas.

For each biofuel technology, we describe the production process, advantages and drawbacks; plus we quantify the market size, typical costs, CO2 intensities and yields per acre.

While biofuels can be lower carbonthan fossil fuels, they are not zero-carbon, hence continued progress is needed to improve both their economics and their process-efficiencies.

Our long-term estimateis that the total biofuels market could reach 20Mboed (chart below), however this would require another 100M acres of land and oil prices would need to rise to $125/bbl to justify this switch.

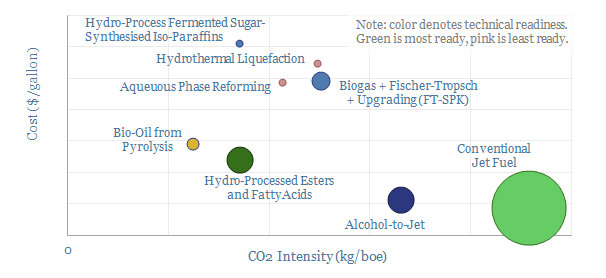

The data-file also contains an overviewof sustainable aviation fuels, summarizing the opportunity set, then estimating the costs and CO2 intensities of different options.

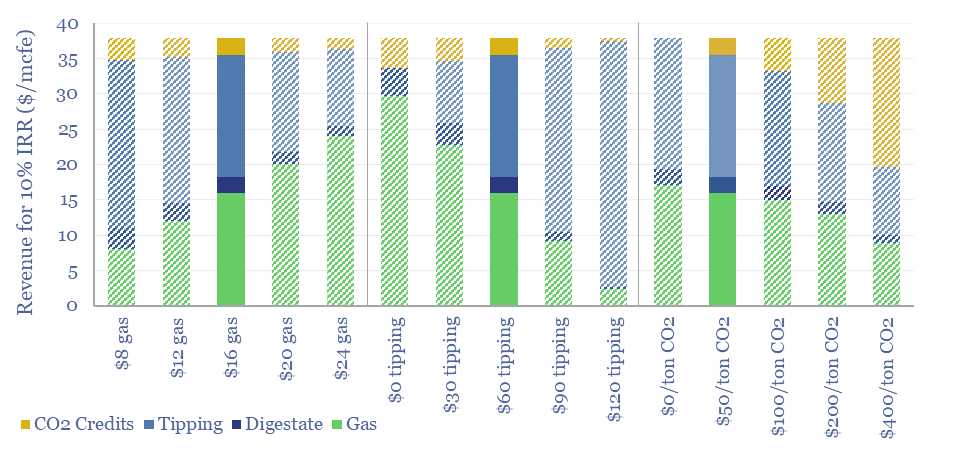

Biogas costs are broken down in this economic model, generating a 10% IRR off $180M/kboed capex, via a mixture of $16/mcfe gas sales, $60/ton waste disposal fees and $50/ton CO2 prices. High gas prices and landfill taxes can make biogas economical in select geographies. Although diseconomies of scale reward smaller projects?

Biogas is a mixture of 50-70% methane and 30-50% CO2, produced from the anaerobic digestion of organic matter, such as manure, sewage or crop residues, or other organic waste. Archaea notes that 72% of US renewable natural gas comes from landfills, 20% from livestock, 5% from organic waste and 3% from wastewater.

This economic model captures the costs of biogas production, informed by 20 case studies, covering yields, capex, opex, IRRs and sensitivities.

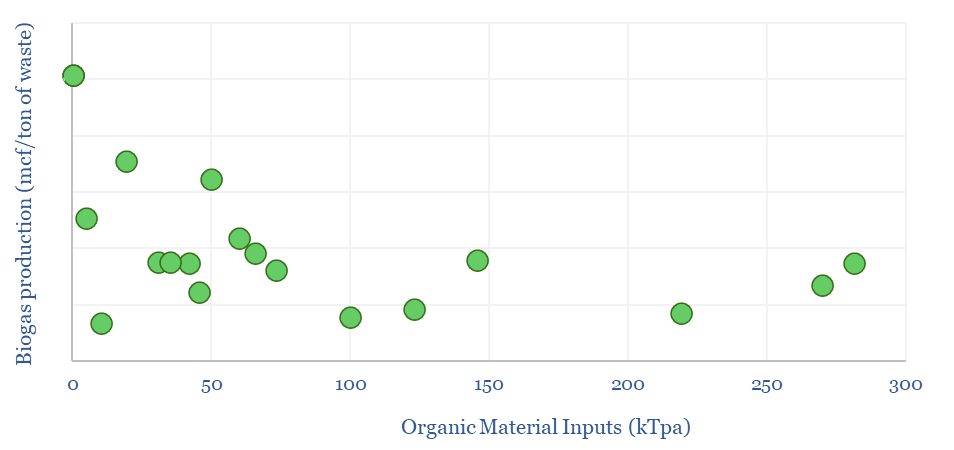

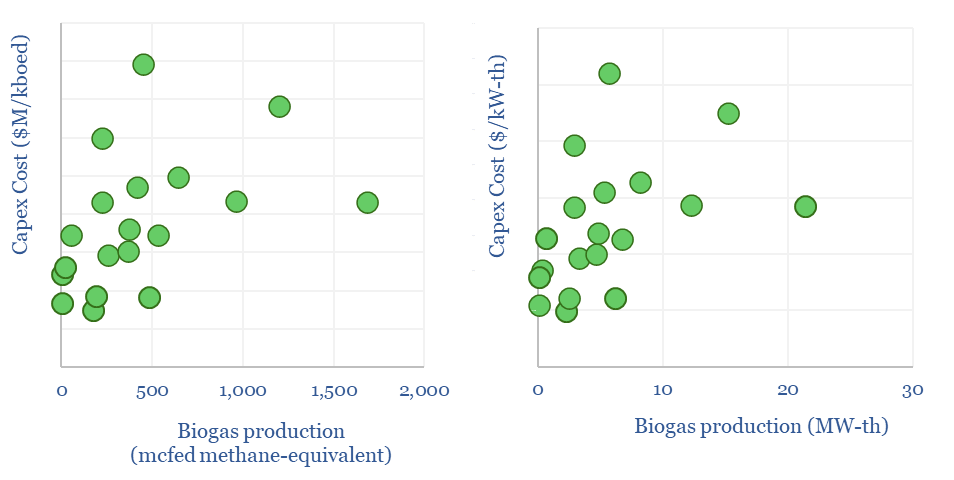

Biogas yields average around 4 mcf per ton of input material, although smaller plants may find it easier to source high-quality feedstocks, with greater quantities of volatile organic matter, and greater conversion of that matter into biogas (chart below).

The capex costs of biogas plants are also tabulated from the 20 case studies in this data-file. Costs vary. But good rules of thumb might be $200/Tpa of feedstocks. In energy industry terms, this is equivalent to around $180M/kboed, or around 6x the costs of offshore hydrocarbons, or around $2,500/kW-th, which again is around 2x higher than the per kW-e costs of solar or onshore wind.

Biogas production facilities need to earn around $35-40/mcfe of methane-equivalent production in order to generate a 10% IRR on their up-front capex. There are four main revenue streams: gas, waste disposal fees, CO2 prices or incentives, and the value of residual digestate, which can be used as fertilizer or bedding in agriculture.

Our base case biogas cost model sees a 10% IRR from a combination of $16/mcf methane, $60/ton disposal fees and a $50/ton CO2 incentive. However, $120/ton landfill taxes can take the methane-equivalent price down to as little as $2.5/mcf. Hence the economics depend on landfill taxes and gas prices in different countries.

Biogas production in Europe currently comprises around 1-2% of the total gas grid, although some studies have estimated that total biogas production could reach 10-20% of total, or around 50-100bcm pa in Europe, via a “huge scale-up”.

One interesting observation from the charts above is that unlike other economic models in our library, biogas facilities may not benefit from economies of scale. Smaller facilities seem to cost less in capex terms and achieve higher yields. This suggests an opportunity for middle-markets private equity and companies with many small facilities?

Please download the data-file to stress-test biogas production costs. We are also constructive on some of the economic opportunities in landfill gas and biochar.

Verbio is a bio-energy company, founded in 2006, listed in Germany, producing bio-diesel, bioethanol, biogas and fertilizers. The company has stated “we want to be in a position to convert anything that agriculture can deliver to energy”. Our Verbio technology review is based on its patents. We find some fascinating innovations in cold mash ethanol, integrated with biogas production, and making biogas from lignocellulosic feedstock.

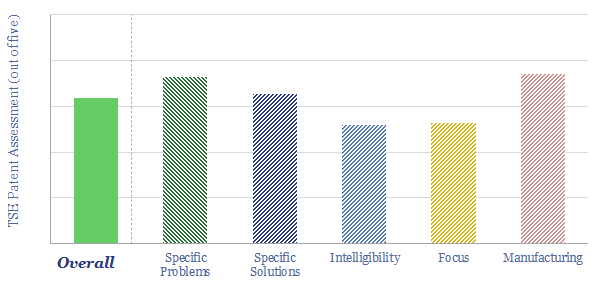

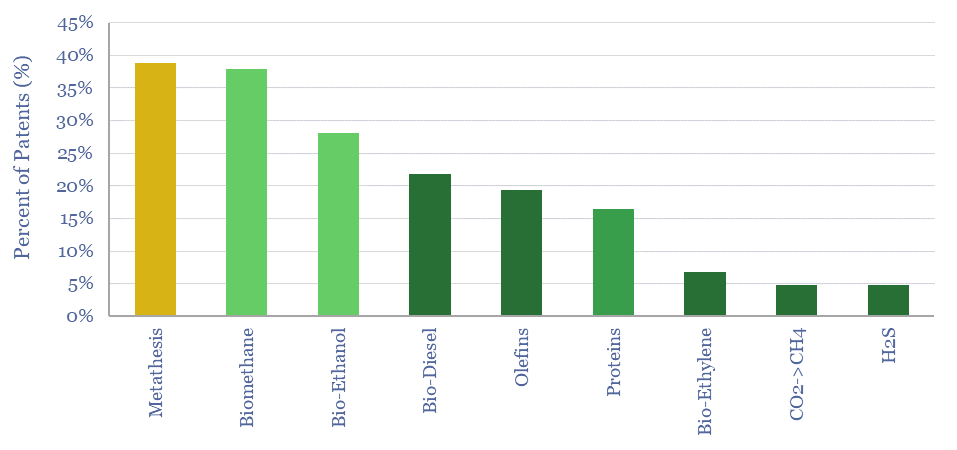

50-60% of Verbio’s EBITDA has recently come from its bio-diesel. We think bio-diesel will see increasing competition for feedstocks and possibly also due to food shortages. Numerically, the largest focus in Verbio’s patents was into metathesis catalysts (chart above), which is the rupturing and re-forming of C-C or C=C bonds, to ‘swap’ the hydrocarbon tails, and produce a more varied range of outputs, especially in bio-diesel. But we found these patents to be disjunctive, and hard to de-risk.

40-45% of Verbio’s EBITDA has recently come from bio-ethanol and bio-methane. And we found the patents here particularly interesting and high-quality. Verbio is using a cold-mash process, which results in 80% lower CO2/energy use than gasoline, and perhaps as much as 50% lower than US corn ethanol using hot mash processes. The patents explain how this is being achieved, including by combining bio-ethanol plants and bio-methane plants, then recirculating the stillage. Some nice flow diagrams are copied in our data-file. But most interestingly, halving the heat use on a bio-ethanol facility, and holding all else equal, would uplift its IRR by 3%, or conversely, lower its total production cost by 5%.

Converting lignocellulosic crop wastes into bio-methane is also covered in the patent library and by the company. This is likely to harness a particularly low-value feedstock (straw), and yield what will be, for the foreseeable future in European gas markets, a high-value product. The patents seem to overcome challenges in the breakdown of waxy coatings, ‘floating layers’, and yields. These patents include some clear and simple details.

Overall our Verbio technology review yielded a mixed score, but this was due to a mix effect. Low carbon bio-ethanol production and forming biogas from lignocellulosic feedstocks seemed most interesting, and also appears to be the focus for new investment in the company’s EUR 300M capex plans.

Is there value in bio-energy technology? We see persistent shortages of hydrocarbons in the 2020s (model here). Energy Majors have also been acquiring biofuels companies in 2022, such as Chevron buying Renewable Energy Group ($3.2bn), BP buying Archaea ($3.3bn) and Shell buying Nature Energy ($2bn).

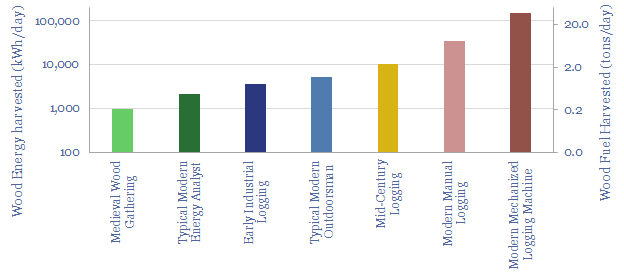

This data-file estimates how much wood can be cut in a day, using back-of-the-envelope calculations, across 500-years of industrial history. In medieval times, a manorial tenant might have gathered 250kg of fallen branches in a good day, containing 1,000 kWh of thermal energy. A modern feller-buncher is 150x more productive. But a modern energy analyst is little better than a medieval peasant. Harvesting wood as a heating fuel is expensive, inconvenient and prone to risks.

Wood as a heating fuel: volume, mass and energy?

Wood fuel quantities are most commonly measured in cords. One cord is defined as 128 cubic feet of wood, which can be visualized as a 4′ tall pile, over an 8′ x 4′ area. Mass and energy content will vary. But as an approximation, 1 cord of wood weighs 1.4 tons, and 1 ton of wood contains 4,000 kWh of thermal energy, which is materially less than other fuels.

500-years: how much wood can be cut in a day?

Wood was the dominant heating fuel of the medieval energy system. We think that a manorial tenant could have gathered 250kg of fallen branches on a good day, limited by the ability to carry only 20-25 kg on a single trip, and secondarily by an absence of comfortable footwear.

Mechanization offered a 2-4x productivity gain by the early industrial era, using handheld saws, axes, and horses to pull felled trees towards water-courses, where they could be floated downstream and processed (painting below from the 1890s).

By the mid-20th century, chainsaws and trucks offered 2-4x further productivity gains, so a professional logging crew could harvest 10,000 kWh of energy per person per day. About the same as 1.5 tons of a typical coal grade. Although debatably, it is less harmful to nature to burn a tree that has already been dead for 400M years than cut down a living one.

Today the logging industry is another 15x more productive again, using slightly terrifying machines such as feller-bunchers to fell, pluck and de-limb entire trees, before cutting them to length, and stacking them for transport. Specialist manufacturers include Tigercat, John Deere, Caterpillar. We are increasingly doing more work on sustainable forestry and screening nature-based CO2 removal projects.

Energy crisis: stocking up on heating fuel?

Somewhere in between the productivity of a medieval peasant and the modern forestry industry, a typical person today can likely collect 0.5-2.5 tons of firewood in an 8-hour day, containing about 2,000-10,000 kWh of useful energy. The precise number depends on the use of modern power tools, the type of wood, and the experience of the person.

Here I am illustrating the point below, after a stint working at a forest plot in Estonia. We cleared out some thicket from this land last year, and have now started the gruelling task of planting proper trees in the gaps. Last weekend, it took about 1.5-hours to gather these thinned branches, drag them across to the road-side, then chop them up using shears and an axe.

Energy metrics: can I do better than a medieval peasant?

(1) Energy quantities. In 1.5 hours, I gathered almost 100kg of wood, which might contain 400kWh of thermal energy. For comparison, a typical bath consumes 4kWh of thermal energy, so this is about “100 baths”. Overall, a typical household consumes 40-60kWh of heat energy per day in the winter. So if I wanted to meet my household’s heating needs by gathering firewood, trips like the one above would need to be a weekly occurrence.

(2) Energy return on energy investment of harvesting this woody debris is actually quite good. My fitness tracking app tells me I burned about 350 kilocalories while doing this back-breaking labor. Which translates into an EROEI of 100x, if the result is 400kWh of wood fuel. Although the EROEI falls to around 10x if we also include the gasoline consumed in driving out to my forest-plot and back (for comparisons, please see our EROEI datafile).

(3) Cost. Unfortunately, if a typical person values their weekend time at $35/hour, and manages to generate 300 kWh of net fuel per hour, then their implied energy cost from gathering firewood comes out to about 12 c/kWh. This is equivalent to paying $35/mcf for natural gas. This is not much cheaper than European natural gas in the 2020s. And debatably, you may also need to add the costs of buying forest land, garden equipment, a woodshed and obligatory Patagonia outdoor wear.

(4) Carbon credentials. The carbon credentials of different wood uses are evaluated in our note here. In this case, I am going to argue that the wood I gathered would simply be decomposing if it were not used up. However, there is clearly a limit to how much fallen debris or thinned material you can collect from a woodland before you are chopping-down older growth trees and contributing to deforestation (the largest single CO2 emissions source on the planet, and more than all the world’s passenger cars).

(5) Other drawbacks. A final conclusion from this exercise is that it is quite inconvenient to have to cut, transport and dry your own fuel; then kindle a fire; then clean up the ashes and air out the smell of smoke from the living room. Out in the forest, there were some slightly hair-raising moments involving the axe, which could have greatly impaired my beloved Excel keyboard shortcuts. And my wife was also quite cross about the state of the car.

Conclusions: better to use modern energy?

How much wood can be cut in a day? The data-file linked below contains our calculations for the tonnage and energy content that can be harvested across different forestry practices over the past 500-years. It is a reminder of the virtues of the modern energy system, if only we could get back to an energy surplus.

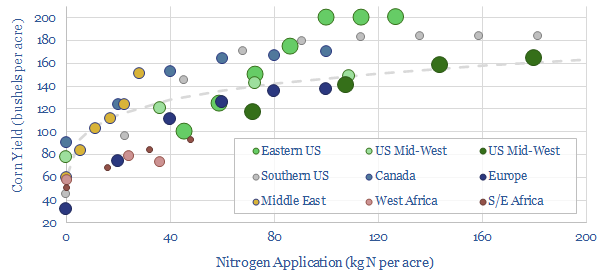

How much does fertilizer increase crop yields? To answer this question, we tabulated data from technical papers. Aggregating all of the global data, a good rule of thumb is that up to 200kg of nitrogen can be applied per acre, increasing corn crop yields from 60 bushels per acre (with no fertilizer) to 160 bushels per acre (at 200 kg/acre).

The relationship is almost logarithmic. The first 40 kg/acre of nitrogen application doubles crop yields, from 60 bushels per acre to around 130 kg/bushel. The next 20 kg/acre adds another 5% to crop yields. The next 20kg/acre adds 4%. The next 20kg/acre adds 3%. And so on. Ever greater fertilizer applications have diminishing returns.

In 2022-23, many decision-makers and ESG investors are asking whether energy shortages will translate into fertilizer shortages, which in turn translate into food shortages. The answer depends. A 10kg/acre cut in nitrogen fertilizer may have a negligible 0-2% impact on yields in the most intensive developed world farming. Whereas it may have a disastrous, >10% impact in the developed world, on the “left hand side” of our logarithmic curves.

The scatter is broad, and shows that corn yields are a complex function of climate, weather, crop rotations, soil types, irrigation, other soil nutrients; and the nuances of how/when fertilizers are applied in the growing cycle. Nitrogen that is applied in the form of ammonia, ammonium nitrate, urea or NPK is always prone to denitrification, leaching, volatilization, and being uptaken by non-crop plants.

Moreover, while this data-file evaluates corn, the world’s most important crop by energy output, the relationship may be different for other crops. Corn is particularly demanding of nitrogen in its reproductive stages of growth. This ridiculously prolific crop will have 55% of its entire biomass invested in its ‘ears’ by the time of maturity. These ears contain so much nitrogen than around 70% is sourced by remobilizing nitrogen out of leaves and stems.

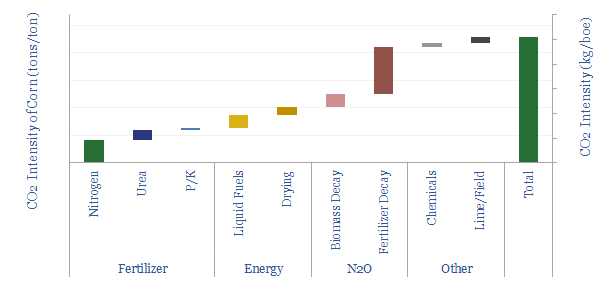

How much does fertilizer increase crop yields? For economic reasons. And to minimize the CO2 intensity of crop production. As a rule of thumb, the CO2 intensity of corn crop production is 75kg/boe, of which 50kg/boe is due to nitrogen fertilizer.

A constructive conclusion is that the first c40-80 kg/acre of nitrogen application does not increase CO2 intensity, or may even decrease it due to much greater yields. Best-fit formulae are derived in this data-file, using the data. So are our notes from technical papers, of which our favorite and most helpful was this paper from PennState.

The CO2 intensity of crop production is broken down in this datafile. We have focused our numbers on corn production, as it is the world’s largest crop, with production of around 1.2 GTpa, or c5,500 TWH of primary energy. (Amazingly, corn thus comprises about 25% of all human food-energy production; and 3% of all total human energy production, 2x more than all wind and solar energy in 2021 combined).

The CO2 intensity of producing corn averages 0.23 tons/ton, or 75kg/boe. This is relatively low, compared to industrial commodities, that tend to range from 0.5 – 150 tons/ton CO2 intensity, across our economic models.

The largest component of crop’s CO2 intensity, at c50% of the total, is N2O emissions, as c0.3-3.0% of all nitrogen fertilizers break down into N2O (per the IPCC). N2O is a greenhouse gas with 298x higher global warming potential than CO2, which explains around 7% of total US greenhouse gas emissions (per the EPA).

Another 30% of the total emissions footprint for producing crops is from producing fertilizers themselves, such as ammonia and urea.

Another 10% is liquid fuels, mainly diesel, used in farm machinery, for tillage, sewing seeds, harvesting crops and transporting them to a processing/storage facility.

The energy return on energy invested for crop production is around 12x on this model. Or in other words, for each 1 kWh of energy in the corn crop, around 0.09 kWh must be supplied, of which c6pp is in the form of natural gas and 3pp is in the form of oil products, mainly diesel. It is sometimes said that the modern agricultural system can be described as the conversion of fossil energy into food energy. Or numbers would suggest this statement is about 9% true!

Implications for biofuels. Making 1 boe of bio-ethanol requires around 2 boe of corn, plus additional gas, electricity and the re-release of CO2 from fermentation. Thus we can compile a total look-through CO2 footprint for corn ethanol, including data from actual bio-ethanol plants and our corn ethanol economic model. We think the Scope 1-3 CO2 of corn ethanol is 240kg/boe, or around 50% below conventional oil products. Although this does not include opportunity costs of biofuels, for example, the potential to re-forest croplands growing corn for ethanol, which could abate over 5 tons of CO2 per acre per year.

All of our numbers can be stress-tested in the data-file. The numbers can vary markedly, from 0.1 – 0.4 tons CO2/ton of corn; or in other words, from 40kg/boe to 160kg/boe. Agricultural improvements remain an important part of the energy transition.

Bio-coke is a source of carbon and energy for steel-making, and other smelting operations where metal oxides need to be reduced to pure metals.

Bio-coke differs from conventional coal-coke or petcoke in that it is derived from biomass, ideally waste biomass, which would otherwise have decomposed. This lowers emissions.

Specifically, input materials are treated at high temperatures and pressure (sometimes around 1,000ºC) to drive off non-carbon materials as gases and ashes.

Bio-coke energy economics. Costs of bio-coke production will most likely run at $450/ton, in order to earn a 10% IRR on a greenfield facility, per the calculations in this model. This is c50% more than the typical price of $300/ton for coal-coke, in normal times. But the higher cost may be economically justified…

Total CO2 intensity of producing bio-coke is calculated at 1 – 1.5 tons/ton, as quantified from technical papers and our own estimates in this data-file. Hence it would save around 2 – 3 tons/ton of CO2 compared with coal-coke. CO2 abatement costs are therefore implied to run at $70/ton, which is competitive on our roadmap to net zero.

However, bio-cokes are not directly comparable with coal-cokes. For example, bio-cokes might have an energy density above 5,000 kWh/ton and “fixed carbon” of 25-85%, a broad range depending on processing parameters. By contrast, traditional coke is closer to 7,000-8,000 kWh/ton, and always above 80% carbon. In addition, bio-cokes can be 50-75% softer and more reactive in some furnace designs than traditional coke. This requires plant modifications, additives and binders, which are still being de-risked.

There are also challenges for scaling. Near-term bio-coke production facilities are likely operating with scales of tens of kTpa. One of the larger operations today, situated in Brazil, makes 600kTpa of ‘zero carbon’ steel, which itself requires 50,000 hectares of planted eucalyptus. However, the total global steel industry produces 2GTpa of output, and replacing all of its coal and coke with biomass could require 2GTpa of biomass inputs, equivalent to the world’s total global timber harvest.

Overall, we conclude that there are good opportunities for bio-coke to contribute to decarbonization of metals and materials, as one out of many concurrent opportunities. Although we might still prefer adjacent opportunities in biochar. You can stress test broad-ranging input variables for bio-coke energy economics in this model.

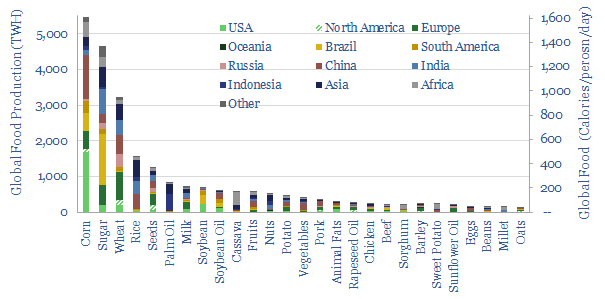

This-data file is a breakdown of world food energy production, by crop, and by major country-region. The source is the excellent and open-source data from the Food and Agriculture Organization. But more importantly, from our perspective as energy analysts, we have converted the numbers from tons to calories and TWH of primary energy equivalents.

World food output is 10bn tons per year, in tonnage terms, of which around 1GTpa comprises corn, vegetables, sugar products, milk, wheat, fruits and rice; while smaller categories include 360MTpa of potatoes, 360MTpa of meats, 350MTpa of soybeans and 250MTpa of vegetable oils (which are also broken down by component and region in the data-file).

Energy density varies sharply, however. 1 kg of vegetable oil might contain 10kWh/kg of energy, while this declines to 5kWh/kg for sugars, 3-4kWh/kg for cereal crops, 2kWh/kg for meats and 0.5kWh/kg for fruits and vegetables.

Food energy production, therefore, stands at 20 trn calories per year, equivalent to 25,000 TWH of primary energy. For perspective, the primary energy in total global gas production is around 40,000 TWH, in total global coal it is 40,000 TWH and in total global oil production it is 50,000 TWH. Food from the world’s 4bn acres of cropland is no less an energy source than conventional energy.

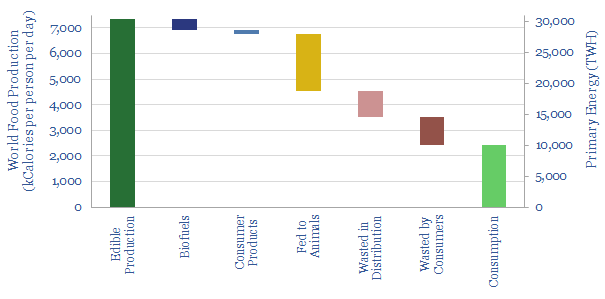

Global food consumption (by humans) only runs at 30% of total food production, or 2,500 calories per person per year, according to our bridging overleaf. c30% of total food production is wasted. Another c30% is fed to animals, which must consume an average of 8 calories to produce 1 calorie of meat. Another c5% is converted into energy as a biofuel. And another c2% is used in consumer products.

Food shortages are an increasing fear for 2022-25. The data also show a wide spread by country-region. Brazil produces 4x its own calorific needs. The US produces 3x. Europe produces 1.1x. But emerging Asia is only 0.7x. Africa is only 0.5x. Alleviating food shortages may result in changing biofuels strategies from developed world (note here) and changing consumption habits (note here).

The data-file contains all of the numbers behind the ideas above, plus a ‘cleaned’ and useful reference, as a breakdown of world food energy production by crop by country and region. For running mass balances, energy balances or biofuels considerations around the world food system.

To read moreabout world food energy production, please see our article here.

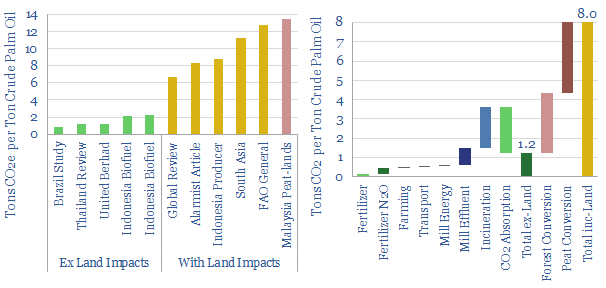

Global palm oil production is running at 80MTpa in 2022, for use in food products, HPC products and bio-fuels. CO2 intensity of palm oil is assessed in this short note and data-file.

Palm oil is controversial, as it is linked to destruction of virgin rainforests, c40% of recent production has been associated with deforestation and c20% has been associated with peatland degradation.

The purpose of this data-file is to estimate the CO2 intensity of palm oil production, in tons of CO2e per ton of crude palm oil. We have aggregated data from 12 technical papers, and also constructed our own bottom up estimates.

Excluding land use impacts, we think palm oil production most likely has a CO2 intensity of 1.2 tons per ton, which is also an OK baseline estimate for responsible palm oil producers.

On a global average basis, including land use changes, we think CO2 intensity is around 8 tons per ton, assuming 40% of the land was deforested and 20% peat-degraded. The worst case scenario is a CO2 intensity of 20 tons/ton.

All of this matters for biofuels. Biodiesel sourced from the world’s average palm oil (8 tons/ton) is going to have 2.5x more emissions than burning conventional diesel. Likewise, if renewable diesel is produced from 65% used cooking oil, 35% palm oil, then again, it will have a higher CO2 impact than conventional diesel (model here).

To read more, please see our article here. Our main conclusion is that bio- and renewable diesel expansion plans may be stymied by tighter feedstock constraints and regulations (note here).

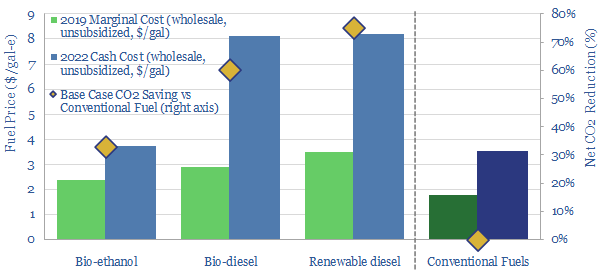

How will food and energy shortages re-shape liquid biofuels? This 11-page note explores four questions. Could the US re-consider its ethanol blending to help world food security? Could rising cash costs of bio-diesel inflate global diesel prices to $6-8/gal? Will renewable diesel expansion ambitions be dialed back? What outlook for each liquid biofuel in the energy transition?

Cookies?

This website uses necessary cookies. Our cookies are simply to improve your experience. We do not undertake any advertising or targeting via our cookies. By clicking 'accept' or continuing to use the website, you consent to our use of cookies.AcceptRead More

Privacy & Cookies Policy

Privacy Overview

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.