…by ramping up short-cycle shale, instead of another offshore cycle? We answer this pushback on pages 10-11. Is another offshore cycle compatible with the energy transition and global decarbonization? We…

…eventual under-supply in conventional oil and gas markets (pages 10-13). (5) Shale productivity is likely to disappoint during the recovery, albeit temporarily (pages 14-15). (6) Project FIDs will need to…

…output. Out to 2025, $60-70/bbl oil should suffice to balance oil markets, while higher prices could draw in 3Mbpd more shale and 1Mbpd more Saudi oil, plus a buffer of…

…+1.6Mbpd pa of shale growth. But generally we expect greater under-supply ahead in other commodities linked to the energy transition. The full modelling behind this 4-page note is available here….

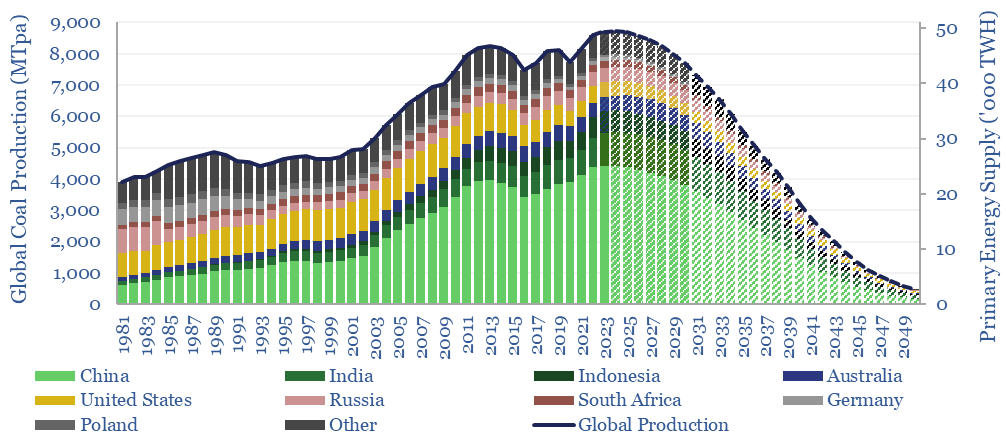

…the Emerging World. Coal-to-gas switching economics are profiled here. Some encouraging precedent come from the US, where coal production peaked at 1GTpa in the 2010s, before shale gas ramped to…

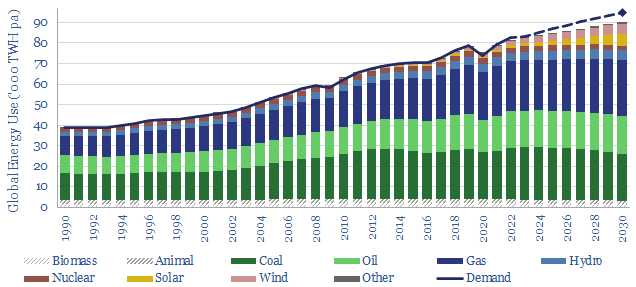

…2030 (model here). It includes oil demand, rising to 102Mbpd in 2024 (data here), then plateauing (model here) as OPEC and US shale (model here) offset the decline rate impacts…

…ones. Increasing energy supplies will be determined by what can actually increase. The largest option is coal, then short-cycle shale, as quantified on pages 6-8. Doubling down on new energies…

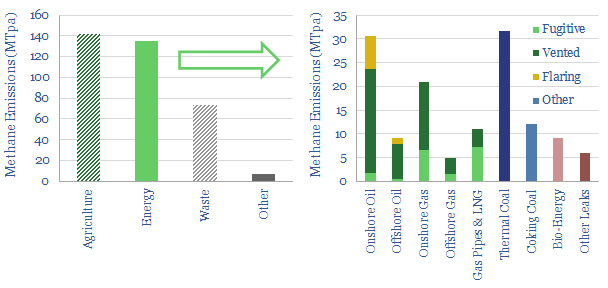

…pure environmental downside. At least coal mines produce coal. Second, there are companies working hard to lower their methane emissions, especially in US shale. For example, they are replacing the…

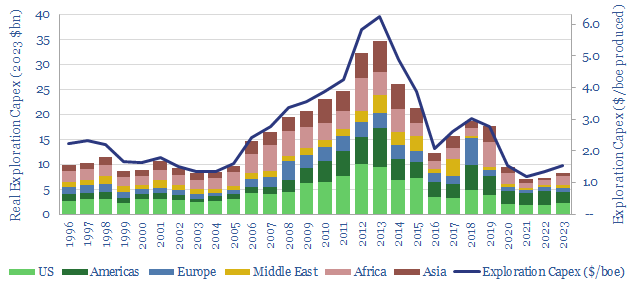

…Mexico) and increasingly for short-cycle shale. During the last oil and gas cycle, the largest increases in exploration investment occurred in Africa, other Americas, Australasia; and to a lesser extent…

…under-investment in conventional energy or in US shale. The larger “pull” on prices is likely to come from the rapid scale-up of solar. The EVA market is relatively small, around…