Direct Lithium Extraction from brines could help lithium scale 30x in the Energy Transition; with costs and CO2 intensities 30-70% below mined lithium; while avoiding the 1-2 year time-lags of evaporative salars. This 15-page note reviews the top ten challenges that decision-makers need to de-risk, in order to get excited within the fast-evolving DLE landscape.

The need to ramp lithium 30x in the energy transition is re-capped on pages 2-3, including why this is one of the most explosive trajectories of any material we have tracked, and becoming a painful bottleneck in 2022-23.

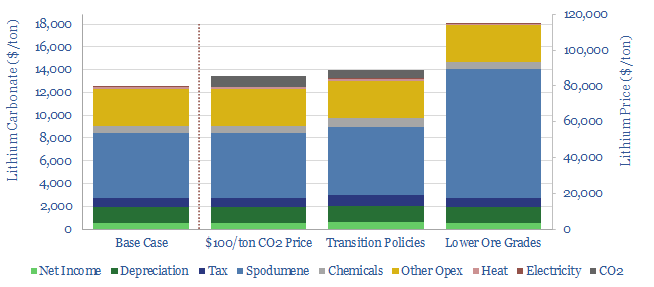

Today’s production is dominated by mining (page 4) and evaporative salars (pages 5-6). Each of these has drawbacks, which are covered in the note.

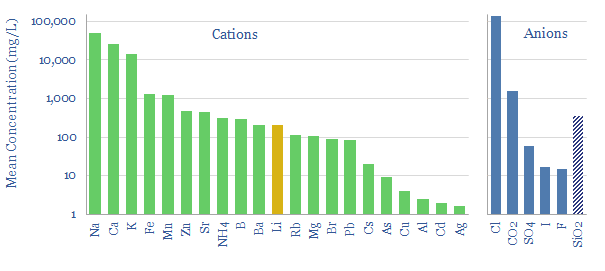

Direct lithium extraction is a kind of holy grail for the lithium industry, a magic process that can separate all and only the lithium ions from the complex ionic soup, even at challenging geothermal brines (example charted above). However, there are ten challenges that need to be overcome before a DLE technology gets truly exciting. They are laid out on pages 8-12.

The extent of these challenges may benefit incumbents in the lithium industry (shown on page 13), as their era of excess returns persists for longer.

Promising DLE leaders are summarized on pages 14-15, along with each company’s recent progress, and the challenges we would focus upon.

For an outlook on mined lithium supply chain, please see our article here.