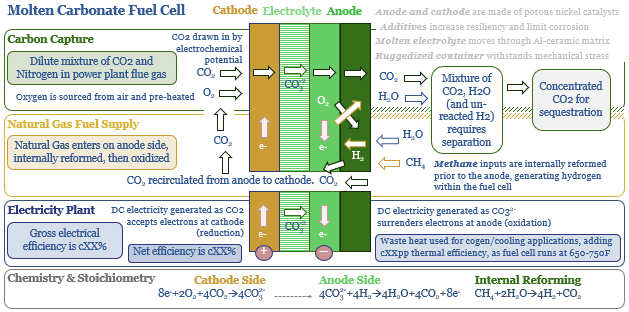

Molten carbonate fuel cells (MCFCs) could be a game-changer for CCS and fossil fuels. They are electrochemical reactors with the unique capability to capture CO2 from the exhaust pipes of combustion facilities; while at the same time, efficiently generating electricity from natural gas. The first pilot plant was due to be tested in 1Q20, by ExxonMobil and FuelCell Energy, but was deferred. Economics range from passable to phenomenal. The opportunity is outlined in our 27-page report.

Pages 2-4 outline the market opportunity for more efficient carbon separation technologies, which can be retrofitted to 4TW of pre-existing power plants, without adding $50/T of cost and 15-30% of energy penalties per traditional CCS.

Pages 5-13 outline how MCFCs work, including their operation, development history, how recent patents promise to overcome reliability problems, and their emergent adaptation to carbon capture.

Pages 14-18 assess the economics, both in absolute terms, and by comparison to new gas plants and hydrogen fuel cells. CCS-MCFC economics range from passable to phenomenal, at recent power prices.

Pages 19-23 suggest who might benefit. Fuel Cell Energy has received $60M investment from ExxonMobil, hence both companies’ prospects are explored.

Appendix I is an overview of incumbent CCS technologies, and their limitations.

Appendix II is an overview of six different fuel cell types, comparing and contrasting MCFCs.

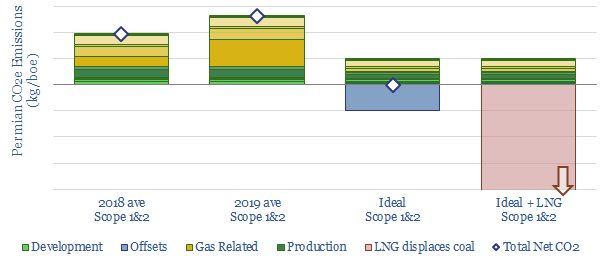

Shale growth has been slowing due to fears over the energy transition, as Permian upstream CO2 emissions reached a new high in 2019. We have disaggregated the CO2 across 14 causes. It could be eliminated by improved technologies and operations, making Permian production carbon neutral: uplifting NPVs by c$4-7/boe, re-attracting a vast wave of capital and growth. This 26-page note identifies the best opportunities.

Pages 2-5 show how fears over the energy transition have slowed down shale growth in 2019.

Pages 6-10 disaggregate the CO2 intensity of the Permian, by source and by operator, based on over a dozen models we have constructed.

Pages 11-15 argue why increased LNG development is the single greatest operational opportunity to reduce Permian CO2 intensity.

Pages 16-18 summarise advances in methane mitigation technologies and their impacts.

Pages 19-23 outline and quantify the best opportunities to lower CO2 from digital initiatives, renewables, lifting and logistics.

Pages 24-25 quantifies the sequestration potential from CO2-EOR, which could offset the remaining CO2 left after all the other initiatives above.

Our conclusion is to identify three top initiatives that companies and investors should favor. Industry leading companies are also suggested based on the patents and technical literature we have reviewed.

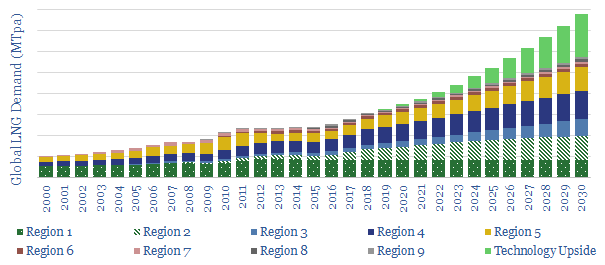

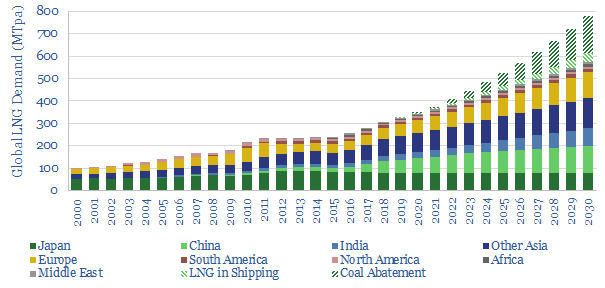

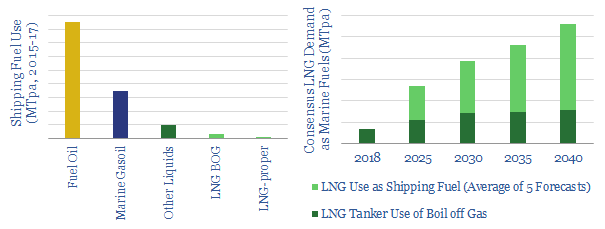

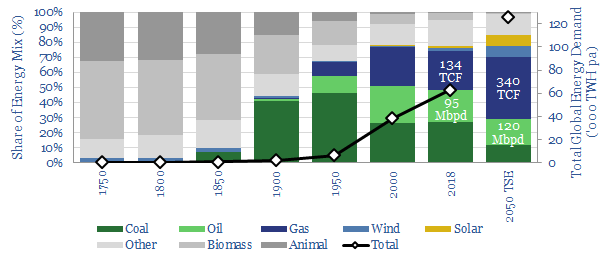

Gas demand could treble by 2050, gaining traction not just as the world’s cleanest fossil fuel, but also the most economical. The ascent would be driven by technology. Hence this note outlines 200MTpa of potential upside to consensus LNG demand, via de-carbonised power and shipping fuels. LNG demand could thus compound at 8% pa to 800MTpa by 2030, justifying greater investment in unsanctioned LNG projects.

[restrict]

Consensus LNG demand?

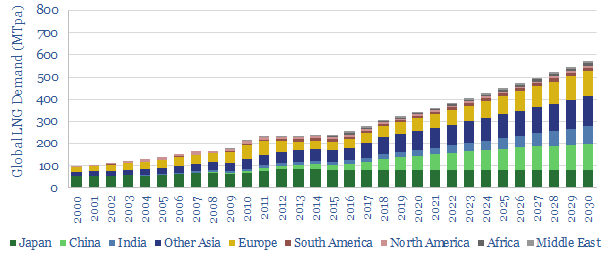

A simple model of global LNG demand is shown below (and downloadable here). It is created by extrapolating recent trends in key LNG-consuming regions. The total market grew at 5.7% pa in 2013-18. At a 5.4% forward CAGR, it would reach c570MTpa by 2030. These numbers are not far from other LNG forecasters’, and thus serve as a reasonable consensus.

What excites us is the potential for technology to accelerate LNG demand. Markets are slow to reflect technological breakthroughs. Hence these new demand sources likely do not feature in consensus forecasts yet. In our view, this makes them worthy of attention.

Upside from De-Carbonised Power Generation?

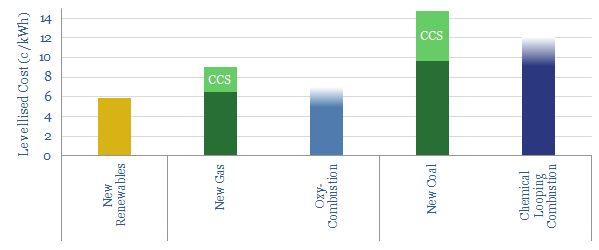

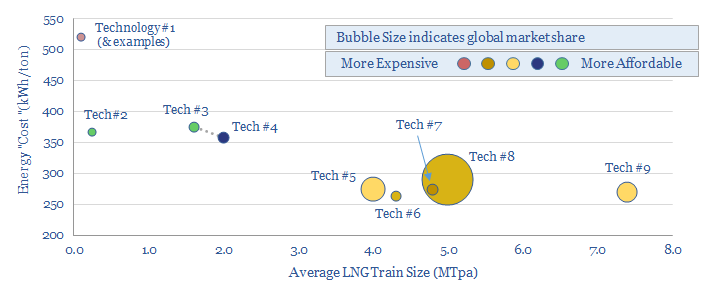

The first opportunity is in de-carbonised power generation, as we have discussed in our deep-dive report, ‘de-carbonising carbon‘. We think novel technologies are reaching maturity, which can generate cost-competitive electricity (chart below) alongside an exhaust stream of pure CO2, for use in industry or for immediate sequestration. The full details are in our report.

Let us now make some approximate calculations: The world consumes 7.7bn tons of coal per annum. In energy terms, this is equivalent to c165TCF of gas, or 3,300MTpa of LNG. We believe it would be economic, and achievable, to convert c5% of this coal power to gas by 2030. Converting it to decarbonised gas could save c1bn tons of CO2 emissions per annum. In turn, this could be achieved by 200GW of de-carbonised gas-power, in 500 x 400MW power plants, each burning c50mmcfd of input gas, fed by 165MTpa of LNG. This is the first area where technology can greatly accelerate LNG demand.

Upside in Shipping?

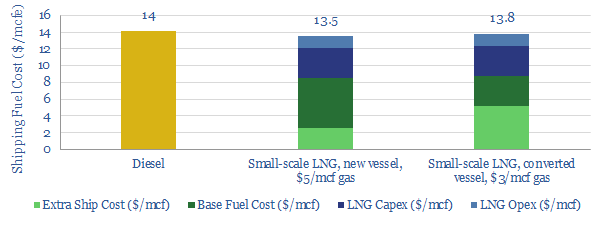

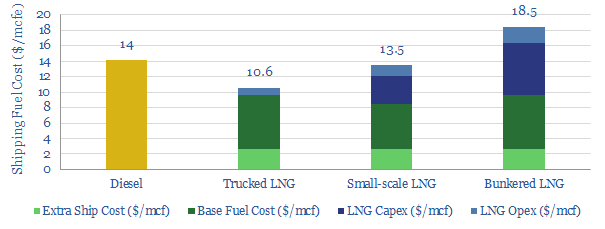

The second opportunity is in LNG as a shipping fuel, which will become increasingly economical after IMO 2020 sulphur regulations re-shape the marine sector. The economics are shown below and modelled here.

New technologies in small-scale LNG will accelerate adoption in smaller ports, moving beyond the large port-sizes required for bunkering. The technologies and economics are explored in detail, in our deep-dive note, LNG in Transport. The economics are modeled here. To assist, Shell is also pioneering new solutions for LNG in transport.

The upshot could be 40MTpa of incremental LNG demand in the maritime industry by 2030. This is the second area where technology can greatly accelerate LNG demand.

Less positive on trucking

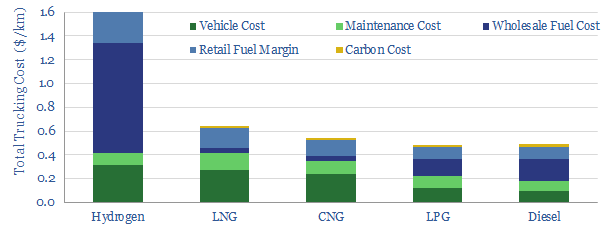

Is there further upside? One might expect, in an overview of LNG technologies, to find incremental upside in road vehicles: either directly in LNG-fired trucks, in gas-fired vehicles, or to produce hydrogen for fuel-cells. None of these opportunities are yet captured in our models.

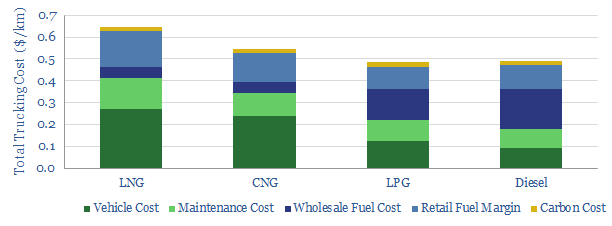

The reason is economics. Compared to diesel-powered trucks, we find compressed natural gas to be c10% more expensive, LNG to be 30% more expensive and hydrogen to be around 4x more expensive (model here, chart below). We also find hydrogen to be 85% costlier than gasoline, to powers cars in Europe (model here). In most cases, electrification is the better option, as superior vehicle concepts emerge.

Our numbers do not include any incremental LNG demand in the road-transportation sector. However, it is noteworthy that replacing 1Mbpd, or c2% of the world’s road fuels with LNG would consume an incremental 50MTpa of LNG. This could cushion delays or shortfalls in decarbonised gas-power.

Potential supplies can meet the challenge.

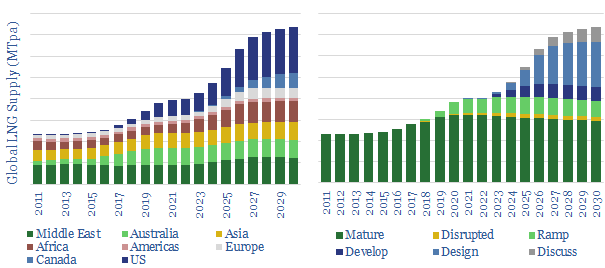

It is only possible for the world to consume 800MT of LNG in 2030 if it is also possible to supply 800MT. While our risked forecasts are for c600MT of LNG supply in 2030 (chart below), our numbers are including just c60% of the 230MTpa of LNG capacity that is currently in the design phase, and just 15% of the 180MTpa that is currently in the discussion phase. In a generous scenario, our forecasts rise close to the 800MTpa level that is required. Please download our risked, LNG supply model to see our scenarios, and the LNG projects included.

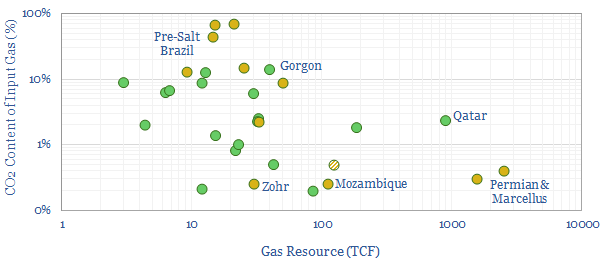

LNG technology could thus unlock incremental LNG facilities. We are most positive on low-cost, low-CO2 sources of gas, particularly in stable and low-tax countries. To help assess the potential, we have therefore compiled a data-file of the world’s great gas resources and their CO2 content, downloadable here. Our positive outlook on US LNG is further underpinned by our positive outlook on US shale.

Conclusions: path dependency?

The numbers above are not hard forecasts. We do not believe hard forecasts are possible in a market that is shaped by unpredictable geopolitics, technologies, weather and its own price-reflexivity. However, we have argued that new technologies may unlock materially more LNG demand than is currently embedded in consensus expectations. Leading companies with leading LNG projects may benefit.

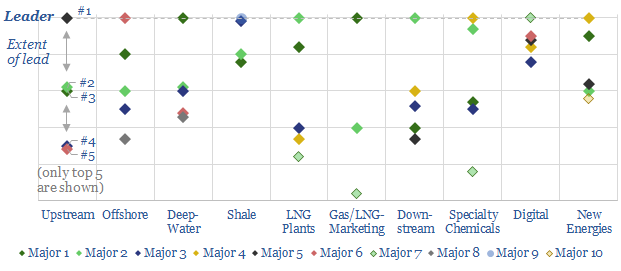

Technology leadership is crucial in energy. It drives costs, returns and future resiliency. Hence, we have reviewed 3,000 recent patent filings, across the 25 largest energy companies, in order to quantify our “Top Ten” patent leaders in energy.

This 34-page note ranks the industry’s “Top 10 technology-leaders”: in upstream, offshore, deep-water, shale, LNG, gas-marketing, downstream, chemicals, digital and renewables.

For each topic, we profile the leading company, its edge and the proximity of the competition.

Companies covered by the analysis include Aramco, BP, Chevron, Conoco, Devon, Eni, EOG, Equinor, ExxonMobil, Occidental, Petrobras, Repsol, Shell, Suncor and TOTAL.

Upstream technology leaders have been discussed in greater depth in our April-2020 update, linked here.

More information? Please do not hesitate to contact us, if you would like more information about accessing this document, or taking out a TSE subscription.

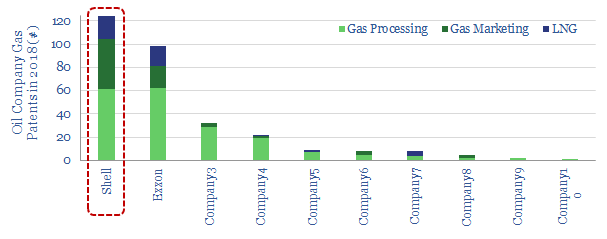

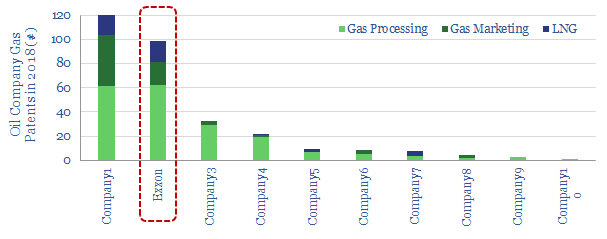

Shell is the leading Major in driving new LNG demand, based on patent filings (chart above). As an example, we highlight a leading new technology to promote LNG demand in transportation, by mitigating the problem of boil-off.

[restrict]

What is limiting LNG in transport?

LNG’s potential upside in transportationis exciting, particularly in shipping, as technologies improve and new sulphur regulation sweeps through the maritime industry (chart below, for full details see our deep-dive note, LNG in Transport: Scaling Up by Scaling Down). But challenges must also be acknowledged.

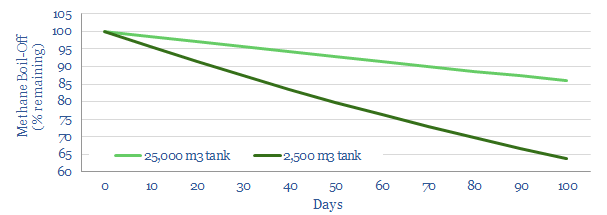

Most prominent is boil-off of LNG, which inhibits its storage over long time-frames. Boil-off typically runs at 0.15% per day, in a large, 25,000m3 tank, which means that c15% of the cargo would be lost over a 100-day period. For smaller-scale LNG, the rate is steeper, averaging c0.45% per day for a 2,500m3 tank, which in turn would cost c35% of the cargo over a 100-day period (chart below). In extremis, 1% per day boil-off is not unheard of.

Managing boil-off requires a vapor management system. Otherwise, as liquid evaporates into gas, the pressure exerted gradually rises, and eventually there is risk of exceeding the tank’s design pressure. This one one reason for the additional costs of converting a vessel to run on LNG, which can reach $17-35M for the largest tankers.

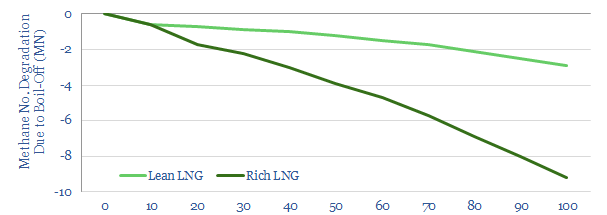

Gas Weathering is another challenge, less well-known, but crucially important. LNG is a mixture of hydrocarbon gases, all with different boiling points. Lower boiling-point components vaporize more readily. Hence over time, the higher boiling point constituents become more concentrated in the fuel tank, lowering the “methane number” of the fuel (chart below). This causes challenges. Most engine makers specify methane must comprise >80% of the fuel in a gas-fired engine. Below this level, the engine performs sub-optimally, knocking, misfiring, over-heating and potentially damaging components such as piston crowns and exhaust valves.

Shell’s improvements: a sub-cooler

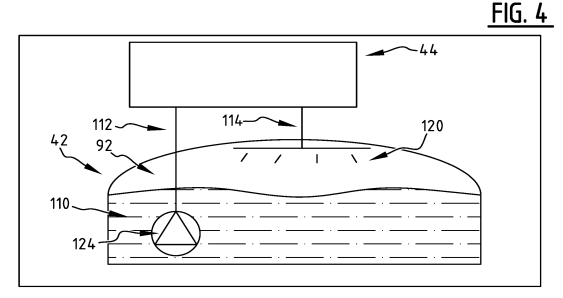

To support LNG’s ascent in transportation, Shell has been the most active Major in developing new technologies. We will be elaborate further, in our upcoming research. But in 2019, one patent stands out, as the company has developed a new ‘sub-cooler’ (pictured below), to met the challenges described above.

The sub-cooler (44) is fluidly connected to the LNG storage tank (42) on a LNG-powered vessel. The tank’s temperature is continually monitored. When it exceeds a predetermined upper threshold, by say 0.25C, a small volume of LNG is pumped out (through 112) , sub-cooled (in 44) then sprayed back into the tank’s vapor space (via 114), until the tank is cooled back below a lower threshold, say, 1C below methane’s boiling point.

The invention’s equipment includes a compressor, a turbine, two heat-exchangers and use of the Brayton Cycle, most likely Air Liquide’s Turbo-Brayton refrigeration cycle using Nitrogen and/or Helium. Its advantage is reliability and low maintenance, which matter for long voyages.

Eight Advantages are Cited

Storage capacity is increased by providing constant and continuous vapor management, using the sub-cooling system.

Weathering is prevented, by sub-cooling and recycling liquefied gas, thus preserving the composition of the liquefied gas.

Fuel economy is thus maximised by avoiding the sub-optimal fuel-consumption caused by weathering. Shell states “Utilization of this system on gas fueled vessels will also allow for greenhouse gas emissions to be optimized”.

Longer journeys are thereby made more feasible.

Capex is saved. By employing Shell’s sub-cooler, no auxiliary consumer is required, lowering the cost of the system, potentially elminating GVU units, control valves, double wall piping, and labor and installation costs.

Opex may improve, due to better fuel economy, and as a larger range of input fuels can be used,

Safety is improved during transfer of LNG from a discharging tank to a receiving tank, providing the ability to lower temperature to 0.5-3C below the gas’s boiling temperature and “thereby limit flashing in the receiving tank during transfer”.

Versatility. The system can be installed in new LNG-powered vessels, new conversion of diesel vessels or retro-fitted onto existing LNG vessels. It can also be deployed in a broad range of LNG-transportation concepts (the patent mentions cruise ships, tankers, container vessels, ferries, barges, tugs… and more exotically, rail, truck, car and even planes!).

Economic Impacts to spur the ascent of gas?

The improvements above may stoke the ascent of LNG for shipping, where we are most positive with 40-60MTpa of upside seen to LNG demand after 2040 (see LNG in Transport: Scaling Up by Scaling Down).

Small-scale liquefaction for shipping is already going to be highly economical after IMO 2020, while bunkered LNG can be rendered as economic if it can harness economies of scale (model here).

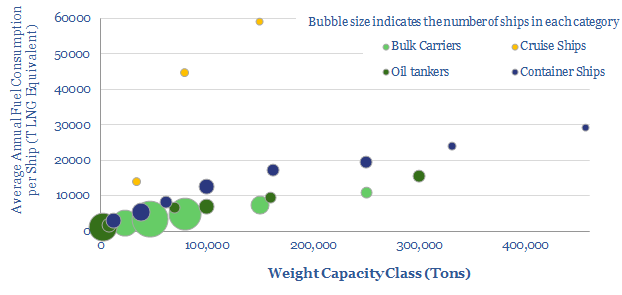

The most attractive vessels to convert to run on LNG are cruisers and large container ships (data-file here).

Economics are currently more challenging for LNG trucks (model here). However, this is due to 2.5x higher vehicle costs and 2x higher maintenance costs per mile. But technical progress such as Shell’s will help.

Source: Hutchins, W. R. & Hartman, S. J. S. (2019). Liquid Fuel Gas System and Method. Royal Dutch Shell Patent US2019024847

For large-scale capital projects in a commodity industry, harnessing better technologies tends to unlock better returns. Hence in this 7-page note we evaluate ExxonMobil greenfield LNG plant construction technology, particularly in remote geographies.

Its technical leadership is clear in our analysis of 3,000 patents across the industry. This matters as Exxon progresses new LNG investments in Mozambique, PNG and the US.

Opportunities should arisefor investors in Exxon’s LNG projects, and for its partners, resource-owners and other stakeholders to maximise value.

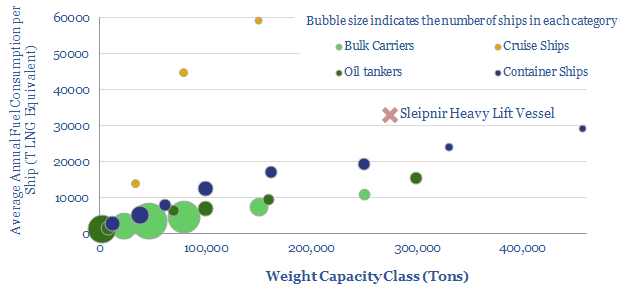

Multiple records have just been broken for an LNG-powered ship, as construction completed at Heerema’s “Sleipnir” heavy-lift vessel (charted above). It substantiates our recent deep-dive note, which sees 40-60MTpa upside to LT LNG demand, from large, fuel-intensive ships, after IMO 2020.

Sleipnir is a record-setting crane-lift vessel, with capacity to pick up 20,000T. This eclipses the prior records in offshore oil and gas, which were around 12,000T, set by the Heerema Thialf and the Saipem 7000. Hence Sleipnir has already lined up 18 contracts, starting with the 15,800T topsides for Israel’s Leviathan gas field, and progressing on to Johan Sverdrup Phase II.

Sleipnir is a record-setting LNG vessel, burning gas as its primary fuel (although it can also burn diesel). With a displacement of 273,700T, we estimate it is the heaviest LNG-powered vessel ever built (eclipsing the largest such container ships, at 220,000T). With a cost of $1.5bn, we estimate it is also the most expensive LNG-powered ship ever built (eclipsing Carnival’s $1.1bn AidaNova cruise ship). It has the world’s first Type-C LNG tank in an enclosed column. Numbers are updated in our data-file here.

There is upside to LNG demandin large, fuel-intensive ships, especially cruise- and container ships, after IMO 2020. Small-scale LNG may offer an economic “bridge”, while bunkering becomes increasingly attractive as volumes per port scale past c80kTpa. Forward-thinking Majors are already investing to capture the future market.

Finally, for a video of the construction vessel being constructed…

Next-generation technology in small-scale LNG has potential to reshape the global shipping-fuels industry. Especially after IMO 2020 sulphur regulations, LNG should compete with diesel. Opportunities in trucking and shale are less clear-cut.

This note outlines the technologies, economics and opportunities for LNG as a transport fuel, following a three-month investigation.

Why technology matters. Pages 2-4 of the note describe incumbent technologies in small-scale LNG, and the need for superior solutions.

The cutting edge . Pages 5-7 draw on patents and technical papers to describe next-generation technologies, at the cutting edge of small-scale LNG. We model that they are economic. They can can provide LNG to the market at $10/mcf.

Potential to transform shipping-fuels. Pages 9-13 find strong economic upside for novel LNG technologies in the shipping industry, with potential to create 40-60MTpa of incremental LNG demand, looking across the global shipping fleet.

Less positive on LNG as a trucking fuel. Pages 14-15 explain why the economics are more challenging for LNG use in land-transportation, i.e., trucking.

Less positive on LNG use in shale. Page 16 explains, similarly, why LNG is less advantageous in the shale patch than converting rigs and frac spreads to piped gas.

Other technologies. Page 17 notes other companies with interesting offerings in small-scale LNG liquefaction, including advances by Exxon and Shell.

Have further questions? Please contact us and we’ll be happy to help: contact@thundersaidenergy.com

It would be unwise to under-estimate the complexity of creating a new LNG province, with a 50MTpa prize on the table in Mozambique. After the first two trains are in motion, the longer-term opportunity is potentially “another Qatar”. But only if Mozambique can compete for capital with US greenfields and brownfield expansions.

Hence we have reviewed 200 of Chevron’s patents from 2018. The company’s ability to develop a new, deep-water LNG province is notable. Ten examples are tabulated below.

It was interesting how many of the patents were filed in Australia and may have derived from learnings at Gorgon and Wheatstone.

For a primer on different LNG process technologies, please see our data-file (here).

Find this work interesting? If so, please sign up for our distribution list.

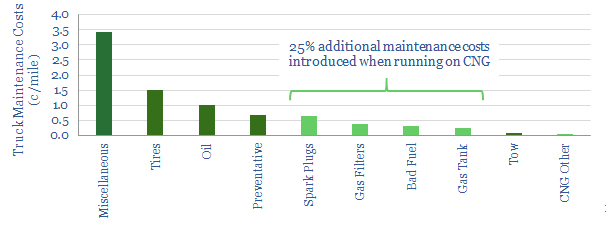

We have assessed whether gas is a competitive trucking fuel, comparing LNG and CNG head-to-head against diesel, across 35 different metrics (from the environmental to the economic). Total costs per km are still 10-30% higher for natural gas, even based on $3/mcf Henry Hub, which is 5x cheaper than US diesel. The data-file can be downloaded here.

The challenges are logistical. Based on real-world data, we think maintenance costs will be 20-100% higher for gas trucks (below). Gas-fired spark plugs need replacing every 60,000 miles. Re-fuelling LNG trucks requires extra safety equipment.

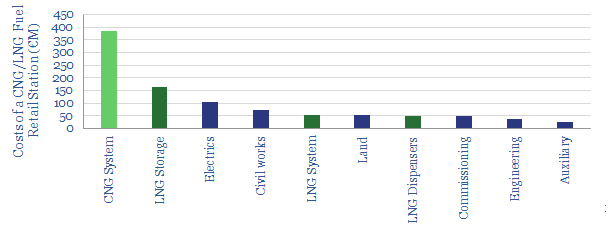

Specially designed service stations also elevate fuel-retail costs by $6-10/mcf. Particularly for LNG, a service station effectively ends up being a €1M regasification plant (or around $250/tpa, costs below).

We remain constructive on the ascent of gas (below), but road vehicles may not be the best option.

To flex our input assumptions, please download our data-model, comparing LNG, CNG and other trucking fuels across 35 different metrics .

Cookies?

This website uses necessary cookies. Our cookies are simply to improve your experience. We do not undertake any advertising or targeting via our cookies. By clicking 'accept' or continuing to use the website, you consent to our use of cookies.AcceptRead More

Privacy & Cookies Policy

Privacy Overview

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.