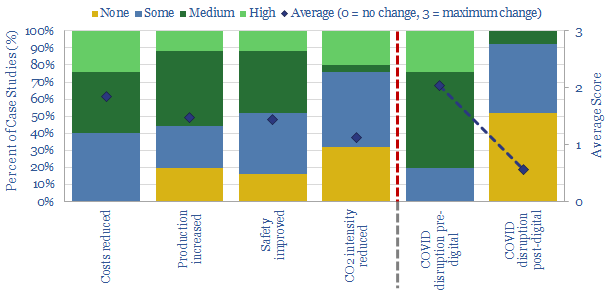

Digitization offers superior economics and CO2 credentials. But now it will structurally accelerate due to higher resiliency: Just 8% of digitized industrial processes will be materially disrupted due to COVID-19, compared to 80% of non-digitized processes. In this 22-page research report, we have constructed a database of digitization case studies around the energy industry: to quantify the benefits, screen the most digital operators and identify longer-term winners from the supply chain.

Pages 2 outlines our database of case studies into digitization around the energy industry.

Page 3 quantifies the percentage of the case studies that reduce costs, increase production, improve safety and lower CO2.

Pages 4-6 show how digitization will improve resiliency by 10x during the COVID-crisis, stoking further ascent of energy industry digitization.

Page 7 generalizes to other industries, arguing digitization will accelerate the theme of remote working, esepcially in physical manufacturing sectors.

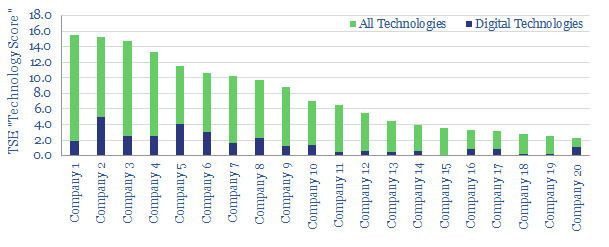

Pages 8-9 screen for digital leaders among the 25 largest energy companies in the world, based on our assessment of their patents, technical papers and public disclosures.

Pages 10-11 identify leading companies from the supply chain, which may benefit from the acceleration of industrial digitization; again based on patents and technical papers.

Pages 12-22 present the full details of the digitization case studies that featured in our database, highlighting the best examples, key numbers and leading companies; plus links to delve deeper, via our other research, data and models.

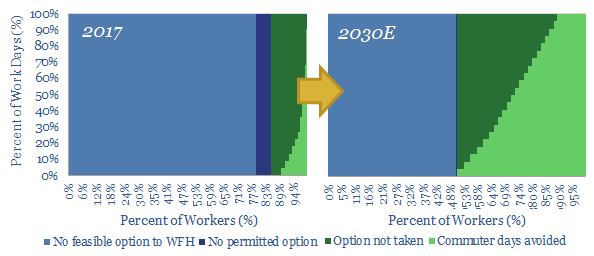

The COVID-19 crisis will structurally accelerate remote working. The opportunity is explored in our 21-page report. It can save 30% of commuter journeys by 2030, avoiding 1bn tons of CO2 per year, for a net economic benefit of $5-16k per employee. This makes remote work a materially more impactful opportunity than electric vehicles in the energy transition.

Remote work currently saves c3% of all US commuter miles, which comprise 33% of developed world gasoline demand (pages 2-4).

Remote work could save 30% of all commuter miles by 2030, structurally accelerating as the COVID-19 crisis changes habits (page 5).

Remote work, thus screens as more impactful than electric vehicles, as an economic opportunity in the energy transition (page 6).

Ecconomic benefits are $5-16k pp pa. Our numbers are conservative. They under-reflect productivity and wellbeing improvements in the technical literature (pages 7-8).

We stress test our numbers, looking profession-by-profession across the entire US labor force, and considering new technologies (pages 9-13).

Direct energy impacts save 1bn tons of annual CO2. Impacts on oil, gas and electricity demand are quantified, including evidence from the COVID crisis (pages 14-17).

Hidden consequences are more nuanced: reshaping mobility, urbanization and online retail habits (pages 18-21).

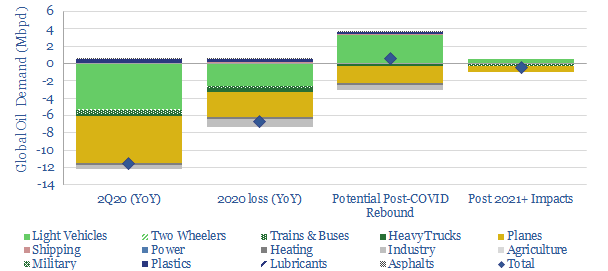

This 15-page note outlines our top three conclusions about COVID-19, which the oil markets may have missed. First, global oil demand likely declines by -11.5Mbpd YoY in 2Q20 due to COVID-19. This is over 15x worse than the global financial crisis of 2008-9, and too large for any coordinated production cuts to offset. Second, once the worst of the crisis is over, new driving behaviours could actually increase gasoline demand, causing a very sharp oil recovery. Finally, over the longer-term, structural changes will take hold, transforming the way consumers commute, shop and travel. (Please note, our oil supply-demand numbers have subsequently been updated here).

Pages 2-7 outline our new models of global oil demand and US gasoline demand, underpinning a scenario where oil demand likely falls -11.5Mbpd in 2Q20, and -6.5Mbpd YoY in 2020. In a more extreme downside case, declines of -20Mbpd in 2Q20 and 10Mbpd in FY20 are possible.

Pages 8-10 illustrate how gasoline demand could actually increase in the aftermath of the COVID crisis, once businesses re-open and travel resumes. The largest cause is a c25% potential degradation in developed world fuel economy per passenger, as lingering fears over COVID lower the use of mass transit and vehicle load factors.

Pages 11-15 outline our top three structural trends post-COVID, which will persist for years, transforming retail, commuting, leisure travel and the airline/auto industries.

Please don’t hesitate to contact us, if you have any questions or comments…

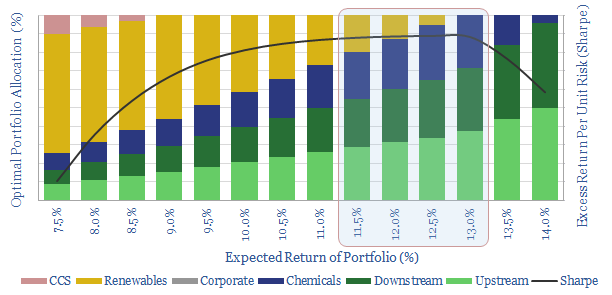

It is often said that Oil Majors should become Energy Majors by transitioning to renewables. But what is the best balance based on portfolio theory? Our 7-page note answers this question, by constructing a mean-variance optimisation model. We find a c0-20% weighting to renewables maximises risk-adjusted returns. The best balance is 5-13%. But beyond a c35% allocation, both returns and risk-adjusted returns decline rapidly.

Pages 2-3 outline our methodology for assessing the optimal risk-adjusted returns of a Major energy company’s portfolio, including the risk, return and correlations of traditional investment options: upstream, downstream and chemicals.

Page 4 quantifies the lower returns that are likely to be achieved on renewable investment options, such as wind, solar and CCS, based on our recent modeling.

Pages 5-6 present an “efficient frontier” of portfolio allocations, balanced between traditional investment options and renewables, with different risk and return profiles.

Pages 6-7 draw conclusions about the optimal portfolios, showing how to maximise returns, minimise risk and maximise risk-adjusted returns (Sharpe ratio).

The work suggests oil companies should primarily remain oil companies, working hard to improve the efficiency and lower the CO2-intensities of their base businesses.

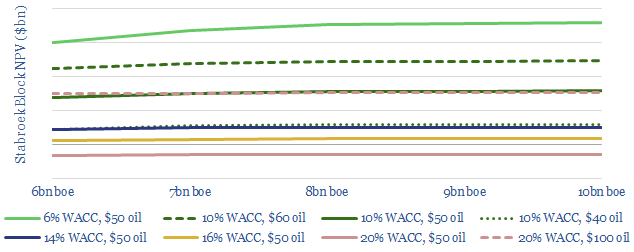

Prioritising low carbon barrels will matter increasingly to investors, as they can reduce total oil industry CO2 by 25%. Hence, these barrels should attract lower WACCs, whereas fears over the energy transition are elevating hurdle rates elsewhere and denting valuations. In Guyana’s case, the upshot could add $8-15bn of NAV, with a total CO2 intensity that could be c50% below the industry average.

Pages 2-3 introduce our framework for decarbonisation of the global energy system. Within oil, this requires prioritising lower carbon over higher carbon oil barrels.

Pages 3-6 outline the economic value in Guyana, which is now at the point where it is hard to move the needle with further resource discoveries.

Pages 7-8 show how lower WACCs can be trasnformative to resource value, even more material than increasing oil prices to $100/bbl.

Pages 9-17 outline the top technologies that should minimise Guyana’s CO2 emissions per barrel, including flaring policies, refining quality, midstream proximity, proprietary gas turbine technologies from ExxonMobil’s patents and leading digital technologies around the industry.

Our conclusion is that leading companies must deepen their efforts to minimise CO2 intensities and articulate these initiatives to the market.

Key points on Guyana carbon credentials and oil capital costs are spelled out in the article sent out to our distribution list.

Precision-engineered proteins are on the cusp of disrupting the meat industry, according to an exceptional, 75-page report, published recently by RethinkX. The science is rapidly improving, to create foods with vastly superior nutrition, superior taste and superior costs, by the early-2020s.

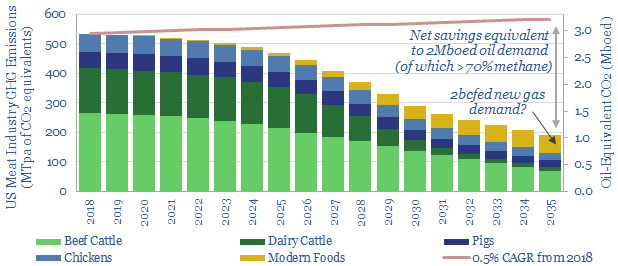

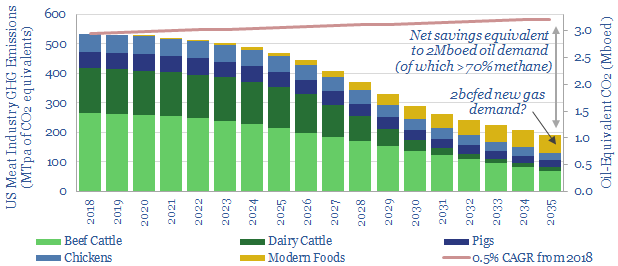

The energy opportunities are most exciting to us, after reading the report. If RethinkX’s scenarios play out, we estimate: direct CO2 savings of 400MTpa, enough to offset 10% of US oil demand; 2bcfd of upside to US gas demand; and enough land would be freed up to decarbonise all of US oil demand, or increase US biofuels production by 6x to c6Mbpd.

[restrict]

RethinkX Re-Thinks Food and Agriculture

ReThinkX argues “we are on the cusp of the deepest, fastest, most consequential disruption in food and agricultural production since the first domestication of plants and animals ten thousand years ago”. The disruption is producing proteins via precision fermentation (PF), which programs microorganisms to produce complex organic molecules in a fermenter.

It is a classic “tech disruption”. Individual molecules are now being engineered by scientists and uploaded to databases. Constant iteration is improving the process. Hence as Impossible Foods’ CEO has said: “unlike the cow, we get better at making meat every single day”. Eventually this will result in a superior product at a far lower cost than today’s cow-based meat industry.

Precision engineered proteins “will be superior in every key attribute – more nutritious, healthier, better tasting, and more convenient, with almost unimaginable variety”. Every aspect can be optimised, in a way impossible with animal-based meat, to yield better taste, more nutrients, higher purity, yet less salt, fat and no need for antibiotics. You could even, in principle, replicate meat proteins from extinct animals, if you want to eat mammoth or giant moa burgers.

The cost of producing PF molecules is deflating: from $1M/kg in 2000 to $100/kg today, on course to hit $10/kg in 2025. The descent matches genome sequencing, which now takes a few days and costs c$1,000, compared with 13-years and $1bn in 2000; and it matches computing, which now costs $60 per teraflop, down from $50M per teraflop in 2000.

The cost of producing meat. Today, animal beef costs c$4.5/kg. PF beef costs $7/kg. RethinkX expects cost parity in 2021, $2/kg pricing in 2024 and $1/kg pricing in 2030. The same trend holds for milk, where just 3.3% of the content is protein, the rest water and sugar. PF production times are also likely to be 100x faster than rearing animals.

More recent context. The number of new US food products with added protein doubled from 2013 to 2017. Protein-enriched milk is becoming popular with baristas as it’s easier to froth. Halo Top was the most popular new consumer product in 2017, an ice cream with 2x more protein than normal. Soylent’s breakfast-replacement costs $3.25 and has the equivalent of a grande latte’s caffeine, three eggs’ protein, 6 Oz tuna’s omega-3s and all 26 essential nutrients. $17bn has been invested in plant-based foods in 2013-18. Disrupting agriculture is already on the ascent.

The consequences. It is argued that “product after product that we extract from the cow will be replaced by superior, cheaper, modern alternatives, triggering a death spiral of increasing prices [for the cattle farming industry], decreasing demand, and reversing economies of scale”. RethinkX’s report explores potential savings of $100bn for families across the USA by 2030; and potential downside for the $1.25 trn per annum US livestock industry. We recommend the report. It is linked here.

Thunder Said Energy Re-Thinks Food and Agriculture Energy

PF energy economics are transformative. The rumen of cow is a 40-50 gallon reactor, with c4% feedstock efficiency, responsible for 70-120kg pa of methane emissions per year, which is in turn, a 23-36x more potent greenhouse gas than CO2. However, an industrial fermenter is a 50-10 thousand gallon reactor, with 40-80% feedstock efficiency and no methane emissions.

Implication 1. 400MTpa of Direct Decarbonisation. The US currently contains 93M cattle, which in turn account for 530MTpa of CO2-equivalent emissions, or c8% of total US greenhouse emissions. RethinkX sees cow numbers reducing 50% by 2030, as the US needs 70% fewer cow products (90% less dairy, 70% less ground beef, 30% less steak); rising to 80-90% by 2035. By 2035, the data imply 400MTpa of CO2-equivalents could be saved, which is equivalent to offsetting c2Mboed of oil consumption.

Implication 2. Incremental Gas Demand of 2bcfd? Although fermentation reactors are c10-20x more thermally efficient than cows, they will still require incremental energy. We believe natural gas is emerging as best placed to provide heating and electric energy for industrial processes. Modern foods in the US could require c2bcfed of incremental gas consumption, 2.5% upside on current US demand, and stoking our expectations for the long-run rise of gas.

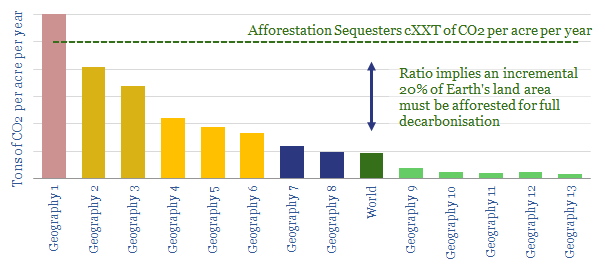

Implication 3. Decarbonising US Oil? We recently analysed seven major themes, which could eliminate 45Mbpd of global oil demand by 2050 (note here). But even on this aggressive scenario, we foresee US oil demand at 16Mbpd in 2035 and 11Mbpd in 2050. How can we decarbonise this oil? One solution is provided by re-purposing the 835M of land acres currently associated with US livestock farming: 655M for grazing, and 180M to grow crops. 60% will be freed for other uses by 2035, equivalent to 485M acres, or the entire Louisiana Purchase of 1803. If all of this land could be repurposed to grow forests, at a yield of c5.4T CO2 sequestation per acre, then we estimate enough CO2 could be absorbed to decarbonise 14Mbpd of oil demand. It is unlikely that all of this land can be repurposed in practice, but CO2 offsets could nevertheless be very large.

Implication 4. 5Mbpd of incremental biofuels. Another possibility is that some of the liberated land could be diverted into producing biofuels: Let us assume 250M acres can be devoted to growing corn, at a yield of c120 bushels per acre, and 2.8 gallons of ethanol per bushel. Multiply through and the total ethanol production would be 80 bn gallons per annum, equivalent to c5Mbpd of oil: 5x larger than current US biofuels production. Here is a positive opportunity for the energy industry, including the companies with the leading biofuels technologies.

Implication 5. Venture Opportunies? Finally, we have noted leading Energy Majors’ diversification into new energy technologies in their recent venture investments (chart below). Natural partnerships may emerge in PF companies. Indeed, we already saw BP deploy $30M investing in Calysta in June-2019, an alternative protein producer, for the aquaculture industry. Companies in the space are numerous: Beyond Meat went public in 1Q19. Impossible Foods is private, but valued at $2bn, having sold 13M units since 2016, and Burger King is introducing an Impossible Whopper in 2019, initially costing $1 more than the conventional Whopper. In March 2019, Geltor announced HumaColl21, the first human collagen created for cosmetics. We will tabulate other companies in a future screen.

Tubb, C. & Seba, T. (2019). Rethinking Food and Agriculture 2020-2030. RethinkX Sector Disruption Report. Full report linked here.

[/restrict]

We would be delighted to introduce clients of Thunder Said Energy to the reports’ authors, Catherine Tubb and Tony Seba. Please contact us if this is useful.

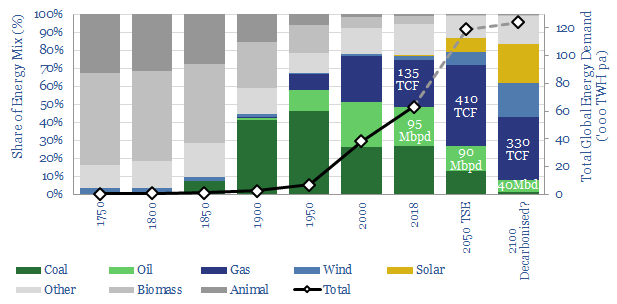

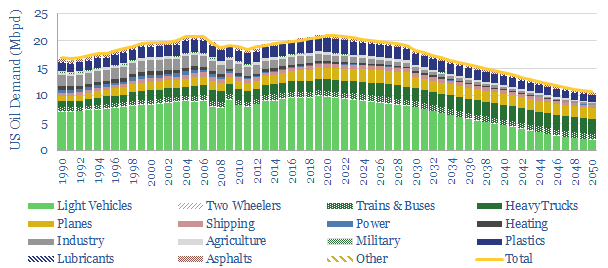

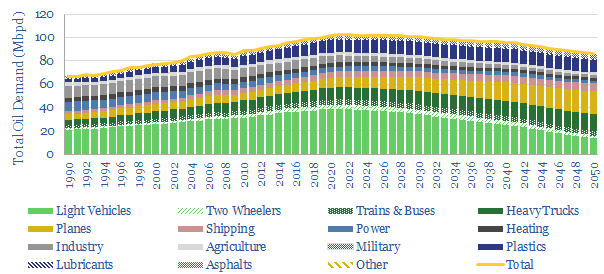

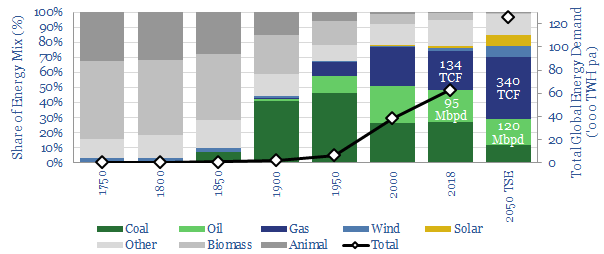

Many commentators fear long-run oil demand is on the cusp of a steep contraction, leaving oil and gas assets stranded. We are more concerned about the opposite problem. Projecting out the current trends, global oil demand is on course to keep rising to over 130Mbpd by 2050, undermining attempts to decarbonise the world’s energy system.

Our new, 20-page note reviews seven technology themes that can save 45Mbpd of long-term oil demand. We therefore find oil demand would plateau at 103Mbpd in the 2020s, before declining gradually to 87Mbpd in 2050. This is still an enormous market, equivalent to 1,000 bbls of oil being consumed every second.

Opportunities abound in the transition, in order to deliver our seven themes, improve mobility, substitute oil for gas, reconfigure refineries for changing product mixes, and to ensure that the world’s remaining oil needs are supplied as cleanly and efficiently as possible. Leading companies will seize these opportunities, driving the transition and earning strong returns in the process.

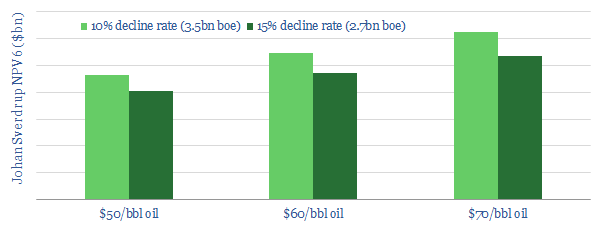

Equinor is deploying three world-class technologies to mitigate Johan Sverdrup’s decline rates, based on reviewing c115 of the company’s patents and dozens of technical papers. Our new 15-page note outlines how its efforts may unlock an incremental $3-5bn of value from the field, as production surprises to the upside.

Pages 2-3 provide the context of the Johan Sverdrup field, its implied decline rates and how their variability will determine the field’s ultimate value.

Page 4 re-caps the concept of decline rates and how they should be measured.

Pages 5-7 recount the history of Digital Twin technologies, the cutting edge of their application offshore Norway and evidence for Equinor’s edge, as it deploys the technology at Sverdrup.

Pages 8-11 illustrate the upside in Permanent Reservoir Monitoring, comparing Equinor’s plans versus prior achievements deploying the technology off Norway.

Page 12-14 show the cutting-edge technology that excites us most: combining two areas where Equinor has established a leading edge. This opportunity can improve well-level production rates by c1.5x.

Page 15 ends by touching upon other technologies that will be applied at Sverdrup, quantifying Equinor’s offshore patent filings versus other listed Majors’.

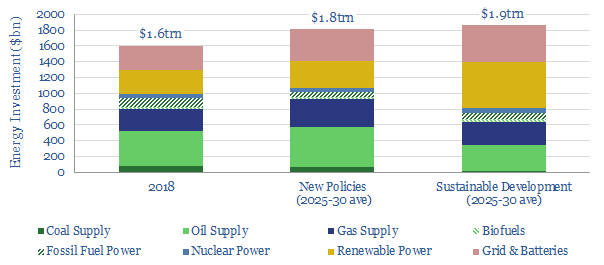

Global energy investment will need to rise by c$220-270bn per annum by 2025-30, according to the latest data from the IEA, which issued its ‘World Energy Investment’ report this week. We think the way to achieve this is via better energy technologies.

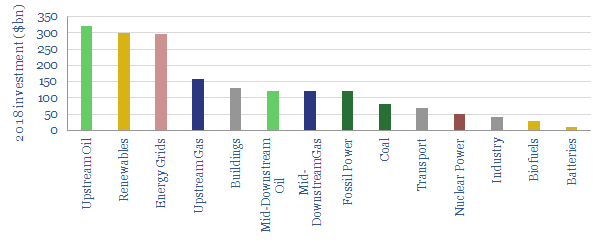

Specifically, the world invested $1.6bn in new energy supplies in 2018, which must be closer to $1.8-1.9bn, to meet future demand in 2025-30– whether emissions are tackled or not. The need for oil investment is most uncertain. More gas investment is needed in any scenario. And renewables investment must rise by 15-100%.

Note: data above includes $1.6trn investment in energy supplies and c$250bn in energy efficiency measures

Hence the report strikes a cautious tone:“Current market and policy signals are not incentivising the major reallocation of capital to low-carbon power and efficiency that would align with a sustainable energy future. In the absence of such a shift, there is a growing possibility that investment in fuel supply will also fall short of what is needed to satisfy growing demand”.

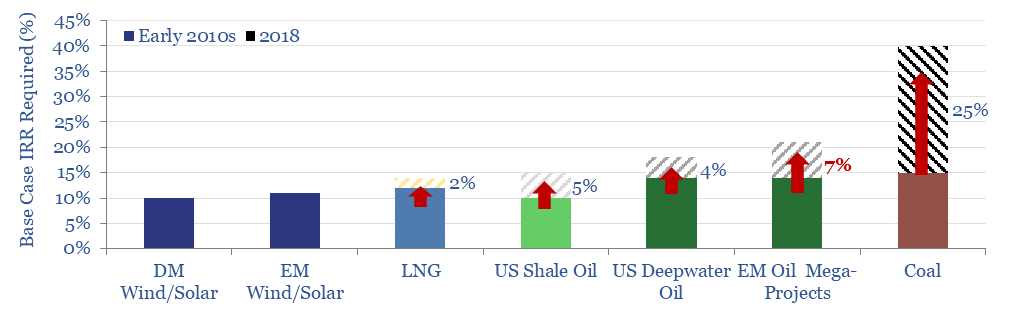

We do not think the conclusions are surprising. Our work surveying 50 investors last year found that fears over the energy transition are elevating capital costs for conventional energy investments (below).

Meanwhile, low returns make it challenging to invest at scale in renewables.

We argue better energy technologies are the antidote to attracting capital back into the industry. That is why Thunder Said Energy focuses on the opportunities arising from energy technologies. Please see further details in our recent note, ‘What the Thunder Said’. For all our ‘Top Technologies’ in energy, please see here.

References

IEA (2019). World Energy Investment. International Energy Agency.

Energy transition is underway. Or more specifically, five energy transitions are underway at the same time. They include the rise of renewables, shale oil, digital technologies, environmental improvements and new forms of energy demand. This is our rationale for establishing a new research consultancy, Thunder Said Energy, at the nexus of energy-technology and energy-economics.

This 8-page report outlines the ‘four goals’ of Thunder Said Energy; and how we hope we can help your process…

Pages 2-5 show how disruptive energy technologies are re-shaping the world: We see potential for >20Mbpd of Permian production, for natural gas to treble, for ‘digital’ to double Oil Major FCF, and for the emergence of new, multi-billion dollar companies and sub-industries amidst the energy transition.

Page 6 shows how we are ‘scoring’ companies: to see who is embracing new technology most effectively, by analysing >1,000 patents and >400 technical papers so far.

Page 7 compiles quotes from around the industry, calling for a greater focus on technology.

Page 8 explains our research process, and upcoming publication plans.

Cookies?

This website uses necessary cookies. Our cookies are simply to improve your experience. We do not undertake any advertising or targeting via our cookies. By clicking 'accept' or continuing to use the website, you consent to our use of cookies.AcceptRead More

Privacy & Cookies Policy

Privacy Overview

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.