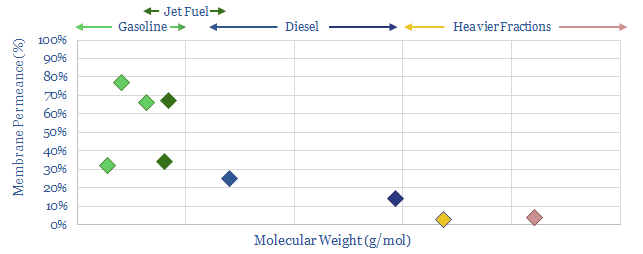

Almost 1% of global CO2 comes from distillation to separate crude oil fractions at refineries. An alternative is to separate these fractions using precisely engineered polymer membranes, eliminating 50-80% of the costs and 97% of the CO2. We reviewed 1,000 patents, including a major breakthrough in 2020, which takes the technology to TRL5. Refinery membranes also comprise the bottom of the hydrogen cost curve. This 14-page note presents the opportunity and leading companies.

The CO2 intensity of refining and the need for economic decarbonization of the sector are quantified on pages 2-4. The discussion focuses upon the CO2 intensity of distillation, including the thermodynamics and costs.

The opportunity to use membranes in lieu of conventional distillation is presented on pages 5-6. We draw on economic models to present respective costs and CO2 intensities of membrane processes.

Hence we screened 1,000 patents to identify leading companies exploring refinery membranes. The findings are presented on pages 7-8. There are three key reasons why the technology has been slow to gain traction.

The most active patent filer in refinery membranes is profiled on page 9, a publicly listed conglomerate with headquarters in the US.

ExxonMobil has made a breakthrough in 2020, deriving permeate streams from a synthetic polymer membrane that resemble the output from a distillation column. We have reviewed the technical disclosures on pages 10-13, highlighting the commercial opportunity and remaining challenges.

Membranes can also unlock the lowest cost hydrogen in the world, recovering hydrogen that is currently wasted or purged in the effluent streams from refinery units. An industry leading example of this technology is explored on page 14.

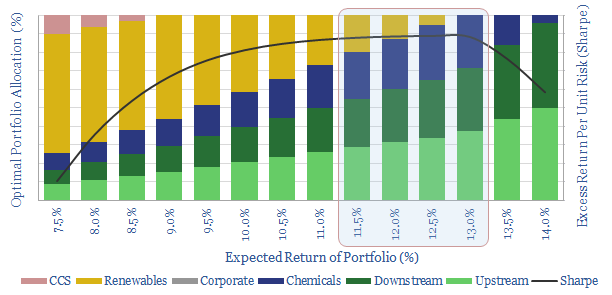

It is often said that Oil Majors should become Energy Majors by transitioning to renewables. But what is the best balance based on portfolio theory? Our 7-page note answers this question, by constructing a mean-variance optimisation model. We find a c0-20% weighting to renewables maximises risk-adjusted returns. The best balance is 5-13%. But beyond a c35% allocation, both returns and risk-adjusted returns decline rapidly.

Pages 2-3 outline our methodology for assessing the optimal risk-adjusted returns of a Major energy company’s portfolio, including the risk, return and correlations of traditional investment options: upstream, downstream and chemicals.

Page 4 quantifies the lower returns that are likely to be achieved on renewable investment options, such as wind, solar and CCS, based on our recent modeling.

Pages 5-6 present an “efficient frontier” of portfolio allocations, balanced between traditional investment options and renewables, with different risk and return profiles.

Pages 6-7 draw conclusions about the optimal portfolios, showing how to maximise returns, minimise risk and maximise risk-adjusted returns (Sharpe ratio).

The work suggests oil companies should primarily remain oil companies, working hard to improve the efficiency and lower the CO2-intensities of their base businesses.

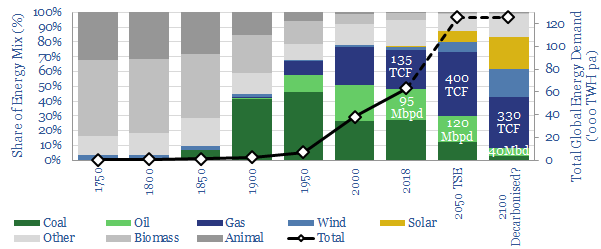

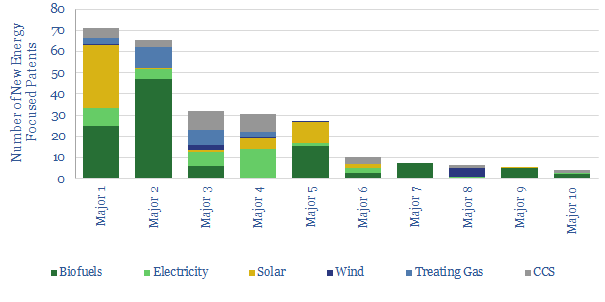

What will happen to oil refineries during the energy transition? On our numbers, liquid oil products will be needed past 2100, long after demand plateaus in the 2020s. Cleaner, more efficient technologies are therefore required in the downstream sector. This note considers whether refineries could increasingly be converted to bio-refineries.

Our evidence comes from the patent literature, as we have reviewed 3,000 patents from the leading 25 Energy Majors. 8% are focused on new energies (chart below, full details in our deep-dive note). Eni screens as the leader for converting refineries to bio-refineries, hence this note summarises its relevant patents on the topic.

Historical Context. Use of vegetable oils in diesel engines goes back to Rudolf Diesel, who, in 1900, ran an engine on peanut oil. Palm oil and peanut oil were both used as military diesel in Africa in WWII. However, vegetable fuels were abandoned due to high costs and inconsistent quality, compared with petroleum fuels.

Today’s vegetable oil fuel-blending components primarily contain Fatty Acid Methyl Esters (FAME). However, they cannot be blended beyond c7% without causing problems in auto engines. For example, FAME has a low energy content (38kJ/kg vs diesel at 45kJ/kg), a -5 – 15C cloud point, causes pollution in tanks, polymerises to form rubbers, causes fouling, dirties filters and contaminates lubricants.

Regulation is nevertheless stoking demand for more dio-diesel, going beyond the 7% threshold. Europe Directive 2009/28/C mandates 10% renewable material in diesel by 2020, up from 5% in 2014.

Eni is therefore converting refineries to bio-refineries, to upgrade renewable materials into “green diesel”. A 0.36MTpa facility started up at Porto Marghera, Venice in 2014. A larger, 0.7MTpa facility started at Gela in 2019. Both convert vegetable oils into diesel.

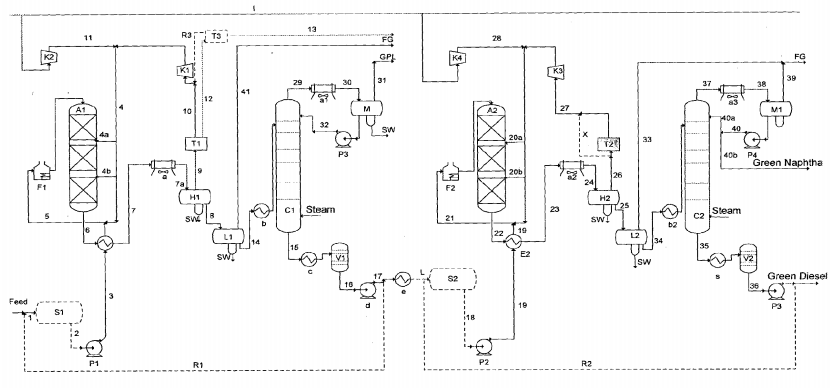

Patents indicate how they work. The starting point is a conventional oil refinery, with two sequential hydro-desulfurization units. For the conversion into a bio-refinery. these units are re-vamped into a hydrodeoxygenation reactor (HDO) and a subsequent hydro-isomerization reactor (ISO), shown in the schematic below.

HDO occurs in the presence of hydrogen, a sulfided hydrogenation catalyst from Group VIII or VIB metals, at 25-70 bar and 240-450C.

ISO occurs at 250-450C, 25-70bar and a Metal (Pt, Pd, Ni) Acid catalyst on an alumino-silica zeolite framework.

Upstream modifications. Pre-treatment processes, surge drums and heat-exchangers are installed upstream of each reactor.

Downstream modifications. The output products from the reactors will contain 1-5% H2S, which is removed in an acid gas treatment unit, and then a Claus unit for sulphur recovery; both reached via new connection lines.

The main advantage of this process is cost, which is said to be 80% lower than constructing a new facility. For example, the Porto Marghera project was budgeted at €200M. In its patents, Eni states: “This method is of particular interest within the current economic context which envisages a reduction in the demand for oil products and refinery margins”.

Further advantages are that the produced diesel has excellent properties, including a high octane index, optimum cold properties, high calorific value and a further by-product stream of commercial LPGs. Moreover, the efficiency of the converted facility is seen to be similar to one constructed anew.

The disadvantage is that blending of free fatty acids is limited to c20%. This is why the bio-refineries so far intake 80% palm oil (which contain <0.1% free fatty acids). Eni states: “The reactor used for effecting the HDO step, deriving, through the method of the present invention, from a pre-existing hydrodesulfurization unit, may not have a metallurgy suitable for guaranteeing its use in the presence of high concentrations of free fatty acids in the feedstock consisting of a mixture of vegetable oils. The reactors of the HDO/ISO units specifically constructed for this purpose, are in fact made of stainless steel (316 SS, 317 SS), to allow them to treat contents of free fatty acids of up to 20% by weight of the feedstock”. Processing a broader range of vegetable oils and other waste oils would require a more costly refinery re-vamp.

Further challenges are that the production of hydrogen and other industrial above will be energy intensive. Moreover, Eni’s 1MTpa of green diesel production capacity is only equivalent to c20kbpd of fuel. It will be challenging to source sufficient feedstocks to scale bio-refineries up to meet larger portions of the world’s overall fuel needs.

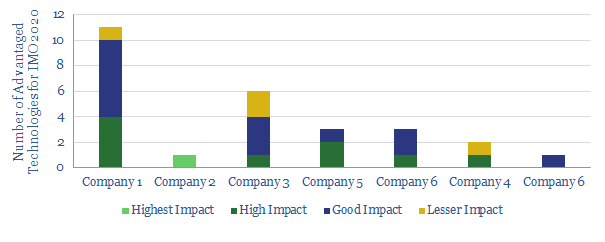

Our conclusion is therefore that bio-refineries have potential when re-purposing existing downstream facilities, preserving value in the very long-term future of the industry. However, further technological improvements are required before these facilities can scale up or deliver material, and truly decarbonised hydrocarbons. Out of Eni’s other refining patents, we are most positive on Eni Slurry Technology, which is a leading technology for IMO2020 (chart below). For details of other technology leaders in energy, please see our note, Patent Leaders.

Source: Rispoli, G., F. & Prati, C. (2018). Method for Re-Vamping a Conventional Mineral Oils Refinery to a Bio-Refinery. US Patent US2018079967.

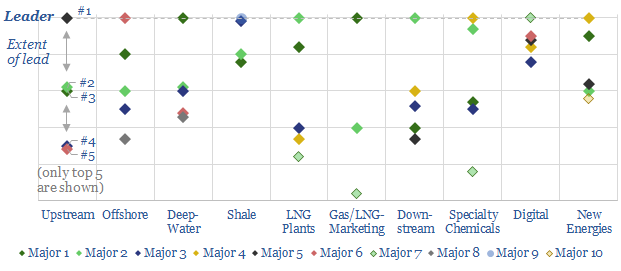

Technology leadership is crucial in energy. It drives costs, returns and future resiliency. Hence, we have reviewed 3,000 recent patent filings, across the 25 largest energy companies, in order to quantify our “Top Ten” patent leaders in energy.

This 34-page note ranks the industry’s “Top 10 technology-leaders”: in upstream, offshore, deep-water, shale, LNG, gas-marketing, downstream, chemicals, digital and renewables.

For each topic, we profile the leading company, its edge and the proximity of the competition.

Companies covered by the analysis include Aramco, BP, Chevron, Conoco, Devon, Eni, EOG, Equinor, ExxonMobil, Occidental, Petrobras, Repsol, Shell, Suncor and TOTAL.

Upstream technology leaders have been discussed in greater depth in our April-2020 update, linked here.

More information? Please do not hesitate to contact us, if you would like more information about accessing this document, or taking out a TSE subscription.

Cookies?

This website uses necessary cookies. Our cookies are simply to improve your experience. We do not undertake any advertising or targeting via our cookies. By clicking 'accept' or continuing to use the website, you consent to our use of cookies.AcceptRead More

Privacy & Cookies Policy

Privacy Overview

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.