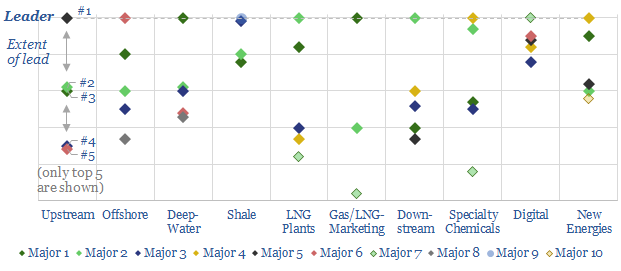

Technology leadership is crucial in energy. It drives costs, returns and future resiliency. Hence, we have reviewed 3,000 recent patent filings, across the 25 largest energy companies, in order to quantify our “Top Ten” patent leaders in energy.

This 34-page note ranks the industry’s “Top 10 technology-leaders”: in upstream, offshore, deep-water, shale, LNG, gas-marketing, downstream, chemicals, digital and renewables.

For each topic, we profile the leading company, its edge and the proximity of the competition.

Companies covered by the analysis include Aramco, BP, Chevron, Conoco, Devon, Eni, EOG, Equinor, ExxonMobil, Occidental, Petrobras, Repsol, Shell, Suncor and TOTAL.

Upstream technology leaders have been discussed in greater depth in our April-2020 update, linked here.

More information? Please do not hesitate to contact us, if you would like more information about accessing this document, or taking out a TSE subscription.

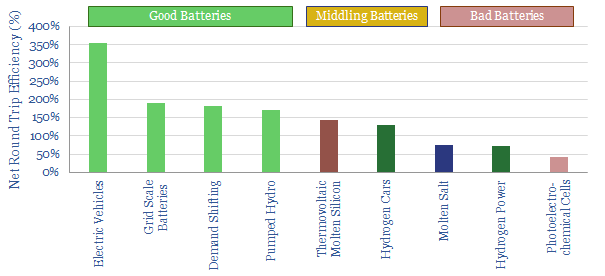

We define a “good battery” as one that enhances the efficiency of the total energy system. Conversely, a “bad battery” diminishes it. This distinction matters and must not be overlooked in the world’s quest for cleaner energy. Electric Vehicles are most favoured, while grid-scale hydrogen is questioned.

[restrict]

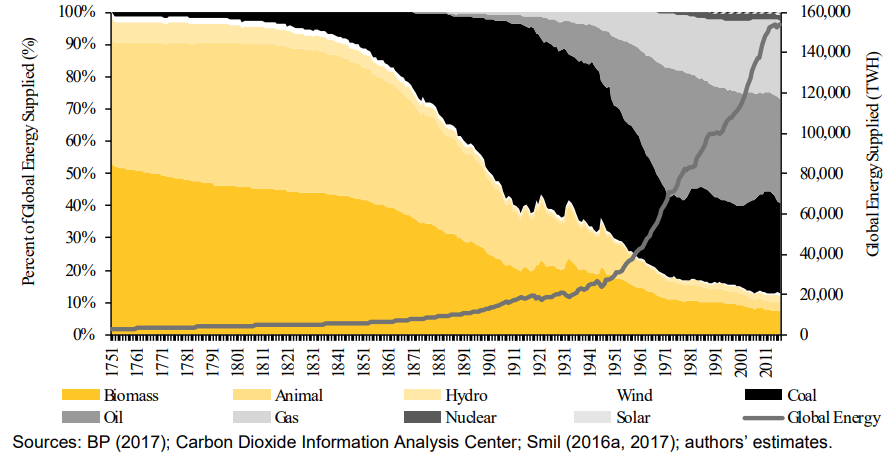

As renewable energy ramps up into the global energy mix (chart below, model here), the energy system will grow increasingly intermittent. This is unavoidable, because sunshine and wind speeds vary, and these variations are correlated over wide geographic areas.

Hence, batteries will be needed, to store up excess renewable generation for when the sun is not shining and the wind is not blowing. Most commentary on batteries focuses on their costs. But there is also an enormous opportunity in their efficiency…

Designed correctly, batteries can improve the efficiency of the global energy system, and accelerate the energy transition by lowering the total amount of energy that needs to be generated. Designed incorrectly, however, these variables are all worsened. The distinction is the topic of today’s note.

To make our distinction clearer, we have created a new data-file estimating the “net round trip efficiency” of different battery types. The calculation has two steps:

First, we measure the energy efficiency of an energy storage system (kWh given out divided by kWh put in).

Second, the storage system’s energy efficiency is compared with the most likely energy source that storage system will displace.

Interpretation. A score over 100% indicates a “good battery”. It is more efficient than the energy source displaced. A score below 100% indicates a “bad battery”. It is less efficient than the energy source displaced.

Examples to illustrate good vs bad batteries

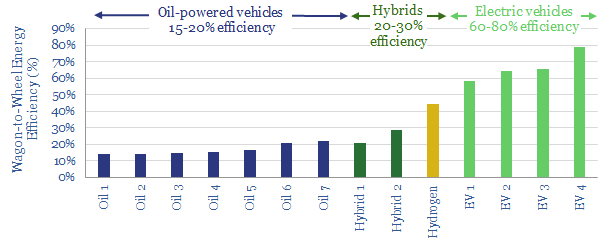

Electric cars are our top example of a “good battery”, with potential to uplift energy efficiency by 3.5x. This is because electric vehicles achieve c60-80% energy efficiencies. An electric vehicle, in turn, is most likely to displace an internal combustion engine, which typically achieves 15-20% energy efficiency (chart below, model here). Mop up c100 units of excess renewable energy with an electric vehicle battery, and it therefore displaces the equivalent of 350 units of oil-energy.

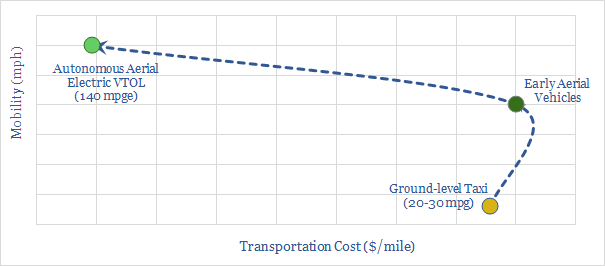

The same 3.5x uplift applies to the battery in an ‘aerial vehicle‘, as we recently reviewed in depth, with flying cars set to achieve the equivalent of 140mpg (chart below).

Grid-scale batteries can also achieve impressive uplifts in efficiency, when inefficient fuel use is displaced. As a general rule of thumb, a power plant might be c50% efficient, hence replacing the power plant with renewables plus batteries can achieve a c2x efficiency uplift.

Additional opportunities are emerging to uplift system efficiency using batteries. One recent example was described by ConocoPhillips, at the Darwin LNG plant, where the gas turbines have a “sweet spot” of maximum efficiency. Battery storage allows Conoco to avoid low-efficiency turbine usage, which will will cut emissions by 20%.

Demand shifting, in the middle of our chart, deserves special mention because it is practically free and can also arguably uplift efficiency by 1-2x. It constitutes moving demand to the times when electricity is flowing abundantly into the grid. Examples range from backups at data-centers to washer-driers in homes. The practice can be encouraged by variable electricity prices, incentivising consumption when electricity supply is abundant and disincentivising consumption at times when it is scarce.

Now we arrive at the right-hand-side of our graph, where we are more cautious. Many commentators have proposed using hydrogen, molten salt or photo-electro-chemical cells as storage mechanisms, to absorb excess renewable power, for later usage…

We calculate that these “batteries” have c35-40% round-trip efficiencies: i.e., one third of the energy is lost to “charge” the battery (e.g., hydrolysing water) and another third is lost discharging it (e.g., burning hydrogen). Mop up 100 units of of renewable energy with one of these “bad batteries” and only c35-40 units can be recovered later. This means the world’s installed renewable capacity achieves less decarbonisation.

Decision-makers may wish to consider system efficiency in these terms, to maximise the impacts of both their renewable and battery investments. Efficiency and economics tend to overlap in all the models we have built.

There is only one way to decarbonise the energy system: leading companies must find economic opportunities in better technologies. No other route can source sufficient capital to re-shape such a vast industry that spends c$2trn per annum. We outline seven game-changing opportunities. Leading energy Majors are already pursuing them in their portfolios, patents and venturing. Others must follow suit.

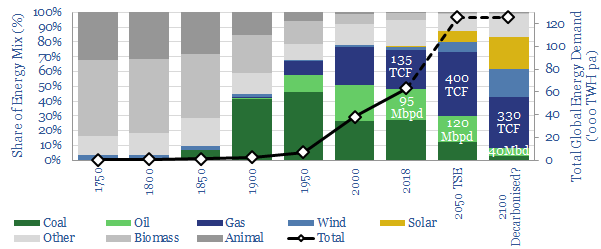

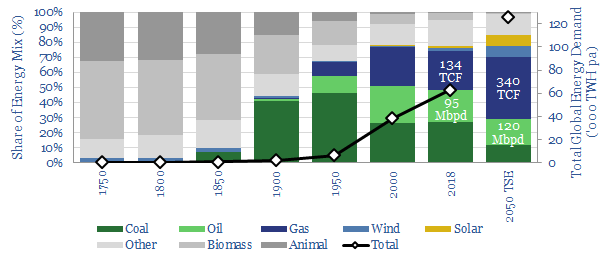

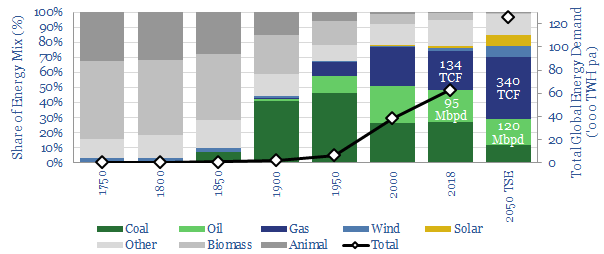

Pages 2-3 show that today’s technologies are not sufficient to decarbonise the global energy system, which will surpass 100,000TWH pa by 2050. Better technologies are needed.

Pages 4-6 show how Oil Majors are starting to accelerate the transition, by developing these game-changing technologies. The work draws on analysis of 3,000 patents, 200 venture investments and other portfolio tilts.

Pages 7-13 profile seven game-changing themes, which can deliver both the energy transition and vast economic opportunities in the evolving energy system. These prospects cover electric mobility, gas, digital, plastics, wind, solar and CCS. In each case, we find leading Oil companies among the front-runners.

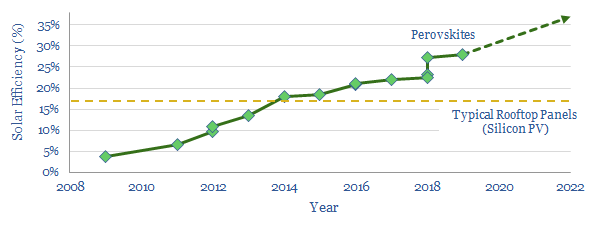

Perovskites are the fastest-improving solar innovation. The best test-cells hit a new record of 28% efficiency last year, with line-of-sight to the mid-30s, i.e., 2x more efficient than today’s silicon photovoltaics. A Major is at the cutting edge.

[restrict]

Today’s renewable technologies are not sufficient to deliver a rapid energy transition. On our numbers, the world will still need 120Mbpd of oil by 2050, while the need for gas will treble, even with $300bn pa invested in wind and solar (chart below, model here) .

What can accelerate the transition is next-generation technology, delivering more energy at a lower cost.

In the solar space, the most exciting opportunity we have reviewed so far is Perovskites. Their efficiency has improved faster than any other solar cells, since the first examples were tested in 2009. There is now line-of-sight to reach 2x higher efficiency than today’s solar cells (c17%), for lower costs.

Five Facts about Perovskites

(1) Perovskites are a mineral class (named after a 19th Century Russian Count). They exhibit exceptional optoelectronic properties: A low band gap means it is easy for incoming photons to dislodge electricity (electrons). Low thermalization losses mean that these liberated electrons are effectively conducted to electrodes, without their energy being dissipated.

(2) The most common cell designs sandwich a layer of MethylAmmonium Lead Iodide (band gap of 1.55 eV) in between an ‘electron carrier’ and a ‘hole carrier’, which are in turn sandwiched between a gold cathode and a fluorided tin oxide anode. A 400nm film of this material can absorb almost all photons in visible light.

(3) Costs should in principle be lower than today’s photovoltaics, due to eliminating the intricate and energy-intensive processing of silicon. Instead, Perovskites crystallise out of a solution onto a substrate. c35% of the cost is the “hole transport layer” and c20% is the gold cathode, both of which are being improved.

(4) Constant innovation is taking place in the technical literature. Mixing perovskites with different cations or silicon can improve the stability of the cells, and liberate more electrons. Efficiency is hindered when liberated electrons recombine at the boundaries of Perovskite “grains”, hence these grain boundaries can be “passivated”. Finally, efficiency can also be improved with better transport materials, electrodes and at the interfaces between materials.

(5) Not there yet. We have classified Perovskites at TRL5. So far, most Perovskites degrade within 500-1,000 hours, due to moisture, oxygen and ultra-violet light, while achieving c200-days’ lifespan is documented as remarkable. Outdoor applications have not been proven. The test cells developed in the lab typically cover 1cm x 1cm. And most use lead, which is toxic.

In conclusion, the technology is exciting, and improving rapidly, but it is also long-dated. It requires committed investors who understand the long-term potential…

Driving the Transition

Reviewing patents and technical papers around the energy industry, what has surprised us most is the Oil Majors’ involvement at the cutting edge of next-generation renewables technology. Leading Majors want to drive the transition: strengthening their societal license to operate and capitalising on vast new opportunities in the future energy system.

It is no different in solar. In 2017, Equinor participated in the £31M Series D funding of Oxford PV, the company at the forefront of Perovskite research, and holding the most recent records for Perovskite cell efficiency. Equinor’s involvement will support Oxford PV gear up to a more commercial phase.

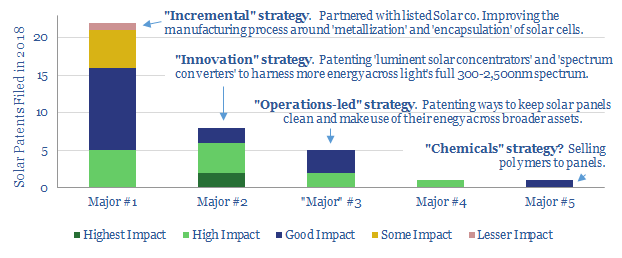

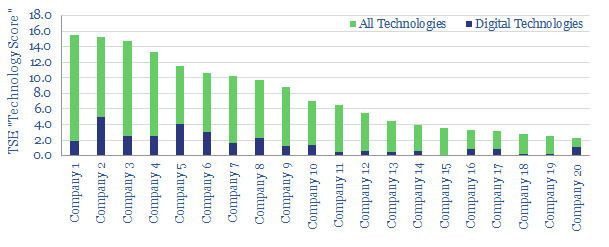

This adds to the other Majors’ efforts at the forefront of solar. We have reviewed 37 patents across the group, and have characterised the leading companies’ efforts here (chart below).

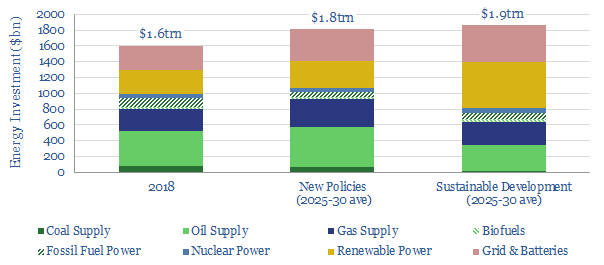

Global energy investment will need to rise by c$220-270bn per annum by 2025-30, according to the latest data from the IEA, which issued its ‘World Energy Investment’ report this week. We think the way to achieve this is via better energy technologies.

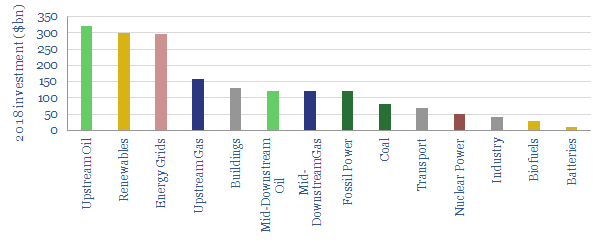

Specifically, the world invested $1.6bn in new energy supplies in 2018, which must be closer to $1.8-1.9bn, to meet future demand in 2025-30– whether emissions are tackled or not. The need for oil investment is most uncertain. More gas investment is needed in any scenario. And renewables investment must rise by 15-100%.

Note: data above includes $1.6trn investment in energy supplies and c$250bn in energy efficiency measures

Hence the report strikes a cautious tone:“Current market and policy signals are not incentivising the major reallocation of capital to low-carbon power and efficiency that would align with a sustainable energy future. In the absence of such a shift, there is a growing possibility that investment in fuel supply will also fall short of what is needed to satisfy growing demand”.

We do not think the conclusions are surprising. Our work surveying 50 investors last year found that fears over the energy transition are elevating capital costs for conventional energy investments (below).

Meanwhile, low returns make it challenging to invest at scale in renewables.

We argue better energy technologies are the antidote to attracting capital back into the industry. That is why Thunder Said Energy focuses on the opportunities arising from energy technologies. Please see further details in our recent note, ‘What the Thunder Said’. For all our ‘Top Technologies’ in energy, please see here.

References

IEA (2019). World Energy Investment. International Energy Agency.

Energy transition is underway. Or more specifically, five energy transitions are underway at the same time. They include the rise of renewables, shale oil, digital technologies, environmental improvements and new forms of energy demand. This is our rationale for establishing a new research consultancy, Thunder Said Energy, at the nexus of energy-technology and energy-economics.

This 8-page report outlines the ‘four goals’ of Thunder Said Energy; and how we hope we can help your process…

Pages 2-5 show how disruptive energy technologies are re-shaping the world: We see potential for >20Mbpd of Permian production, for natural gas to treble, for ‘digital’ to double Oil Major FCF, and for the emergence of new, multi-billion dollar companies and sub-industries amidst the energy transition.

Page 6 shows how we are ‘scoring’ companies: to see who is embracing new technology most effectively, by analysing >1,000 patents and >400 technical papers so far.

Page 7 compiles quotes from around the industry, calling for a greater focus on technology.

Page 8 explains our research process, and upcoming publication plans.

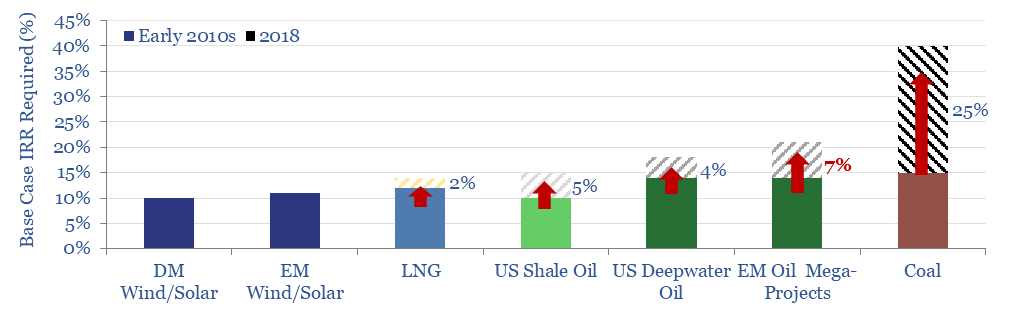

Fears over the energy transition are now restricting investment in fossil fuels, based on our new paper, published in conjunction with the Oxford Institute for Energy Studies, linked here.

They have elevated capital costs by 4-7% for oil and by c25% for coal, compared with the early 2010s.

One consequence will be to concentrate capital into renewables, gas, and shorter-cycle oil projects (i.e., shale).

But there will also be negative consequences, risking long-run supply shortages of oil and coal.

Companies are also being pressured to ‘harvest’ their existing assets, rather than maximising potential value in the 2020s, which may impact valuations.

For further details please see the full paper, linked here, or contact us.

In 2018, we reviewed 250-years of energy transitions, arguing that another great energy transition is now on hand.

It will occur over the next century. Thus for another hundred years, today’s energy industry will remain vitally important. In addition, new sources of supply will create unimaginable new sources of energy demand.

This website uses necessary cookies. Our cookies are simply to improve your experience. We do not undertake any advertising or targeting via our cookies. By clicking 'accept' or continuing to use the website, you consent to our use of cookies.AcceptRead More

Privacy & Cookies Policy

Privacy Overview

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.