Metals

-

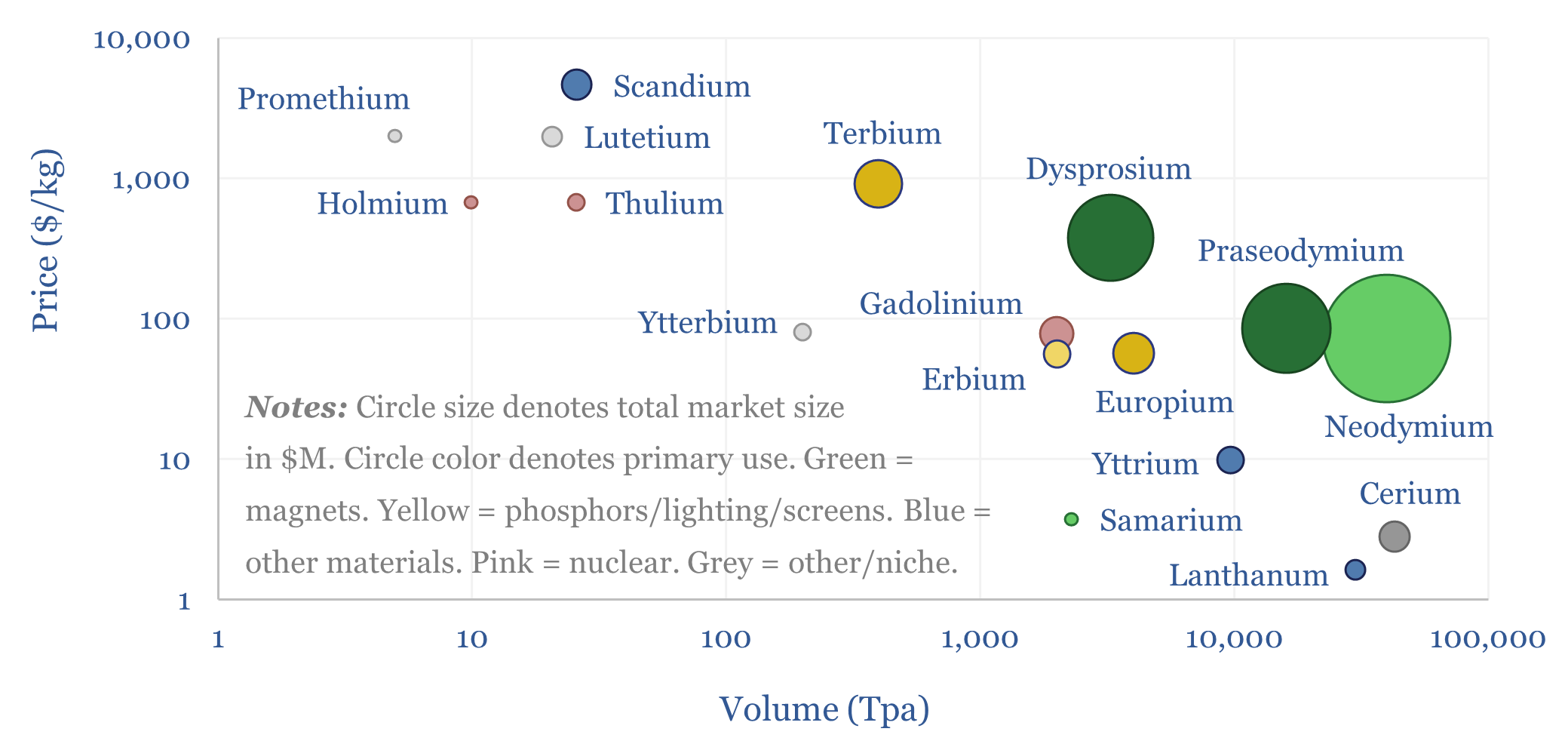

Rare Earth market: by metal, by use, by value?

The global Rare Earth market is 390kTpa of mined Rare Earth Oxide equivalents, which is processed to yield 150kTpa of sellable Rare Earth materials, with a value of $7bn pa. But “price” is not “value”. This data-file breaks down the global Rare Earth market, by metal, by price (in $/kg), by volume (in Tpa), and…

-

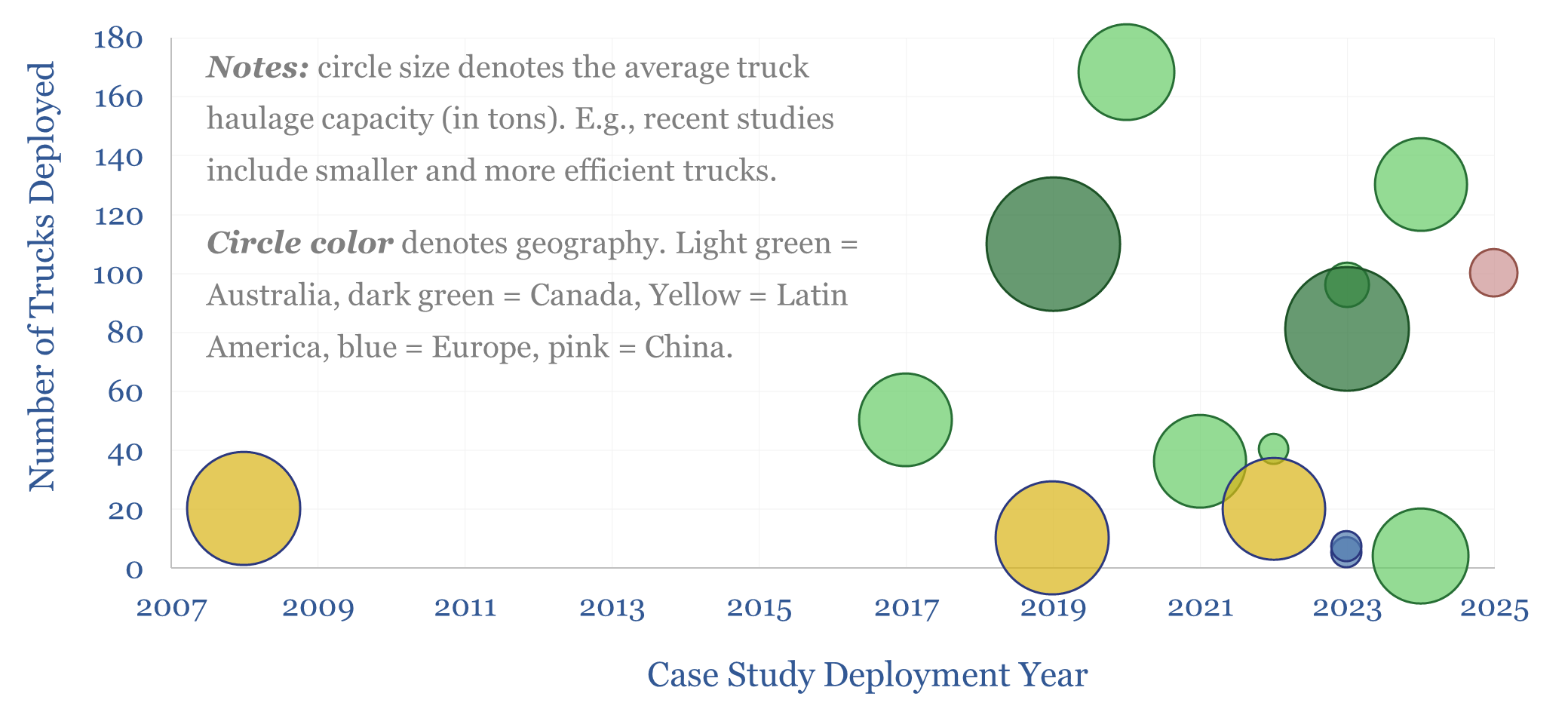

Autonomous mining trucks: case studies?

Autonomous mining trucks have been gaining share since 2010, and now number almost 2,000 in total, across dozens of mines globally. So this data-file presents some case studies of autonomous mining trucks, and provides yet another example of digital progress. The work also shows leading companies in autonomous mining trucks, among adopters and mining equipment…

-

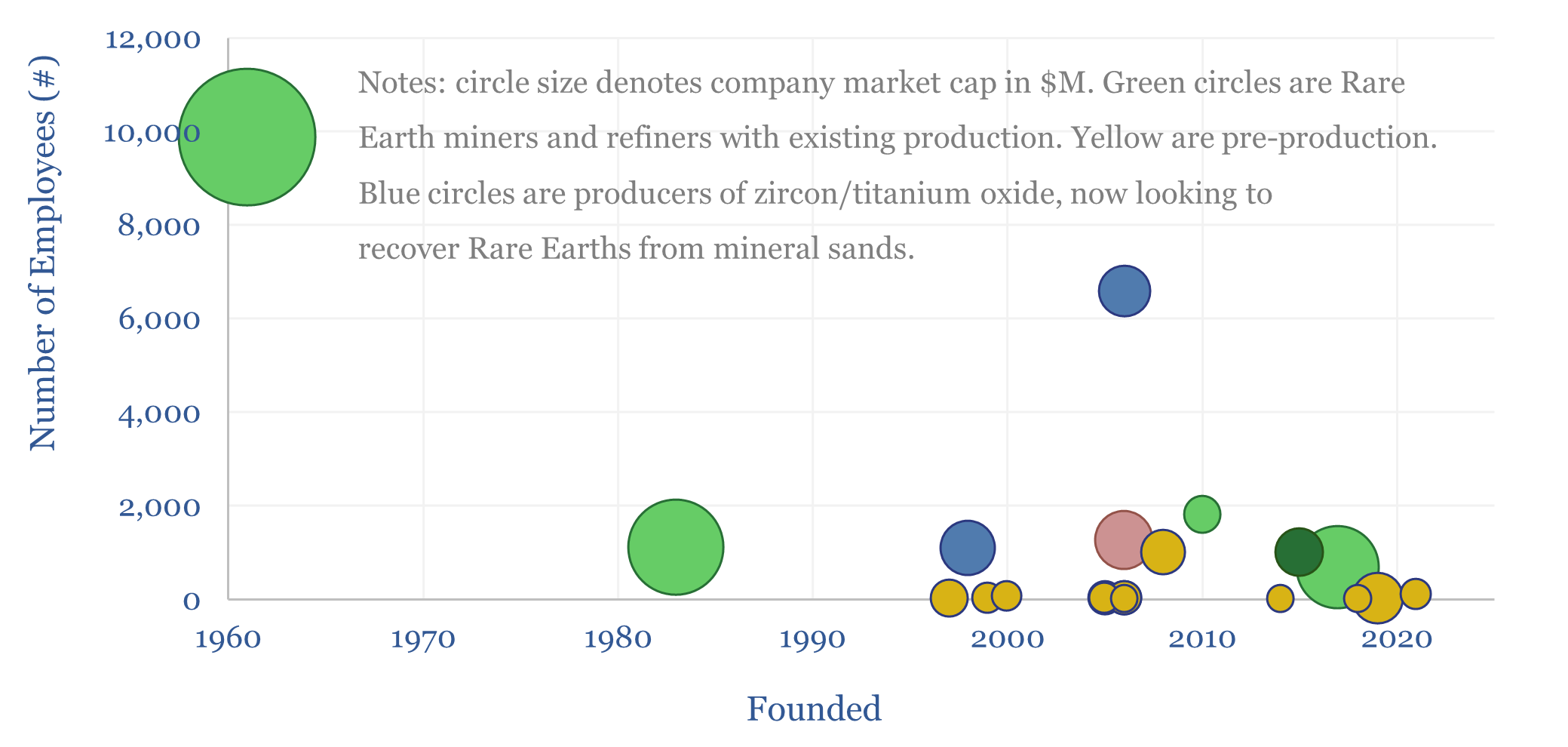

Rare earth companies: screen of miners and refiners?

This screen of Rare Earth miners and refiners captures 20 Rare Earth companies, their flagship projects, and economic parameters such as capex, ore grades, end products and NPVs. A vibrant landscape is evolving, especially for NdPr and DyTb, although the market is still risking pre-produdction projects heavily.

-

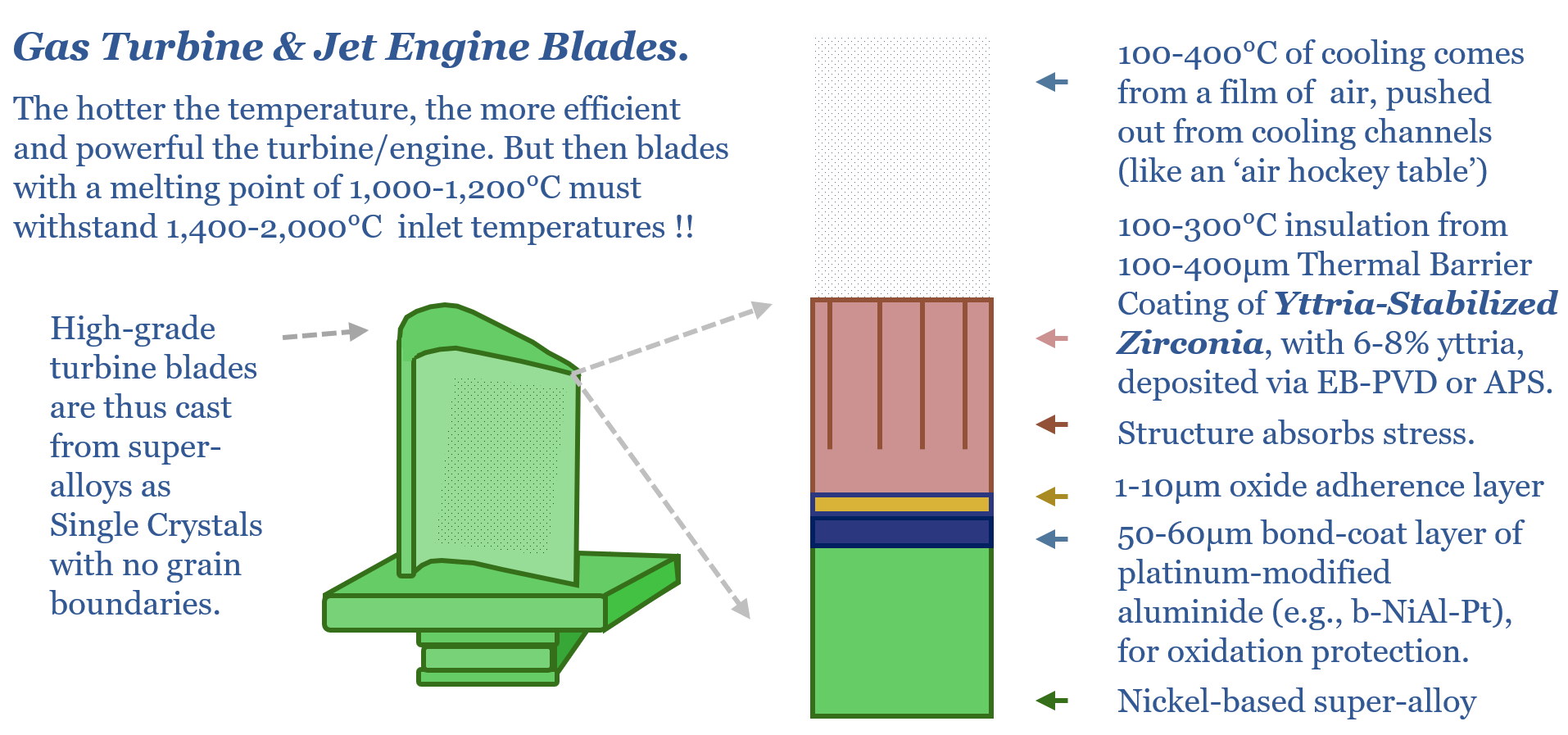

Yttria-stabilized zirconia: sticker shock?

Global yttrium output is just 10-15kTpa, worth $100M pa, of which c90% is controlled by China. Yet a supply disruption for this critical metal could have ripple effects comparable to an oil shock: de-railing developed world load growth, aircraft manufacturing and the rise of AI? This 15-page report tells the story of yttria-stabilized zirconia, explores…

-

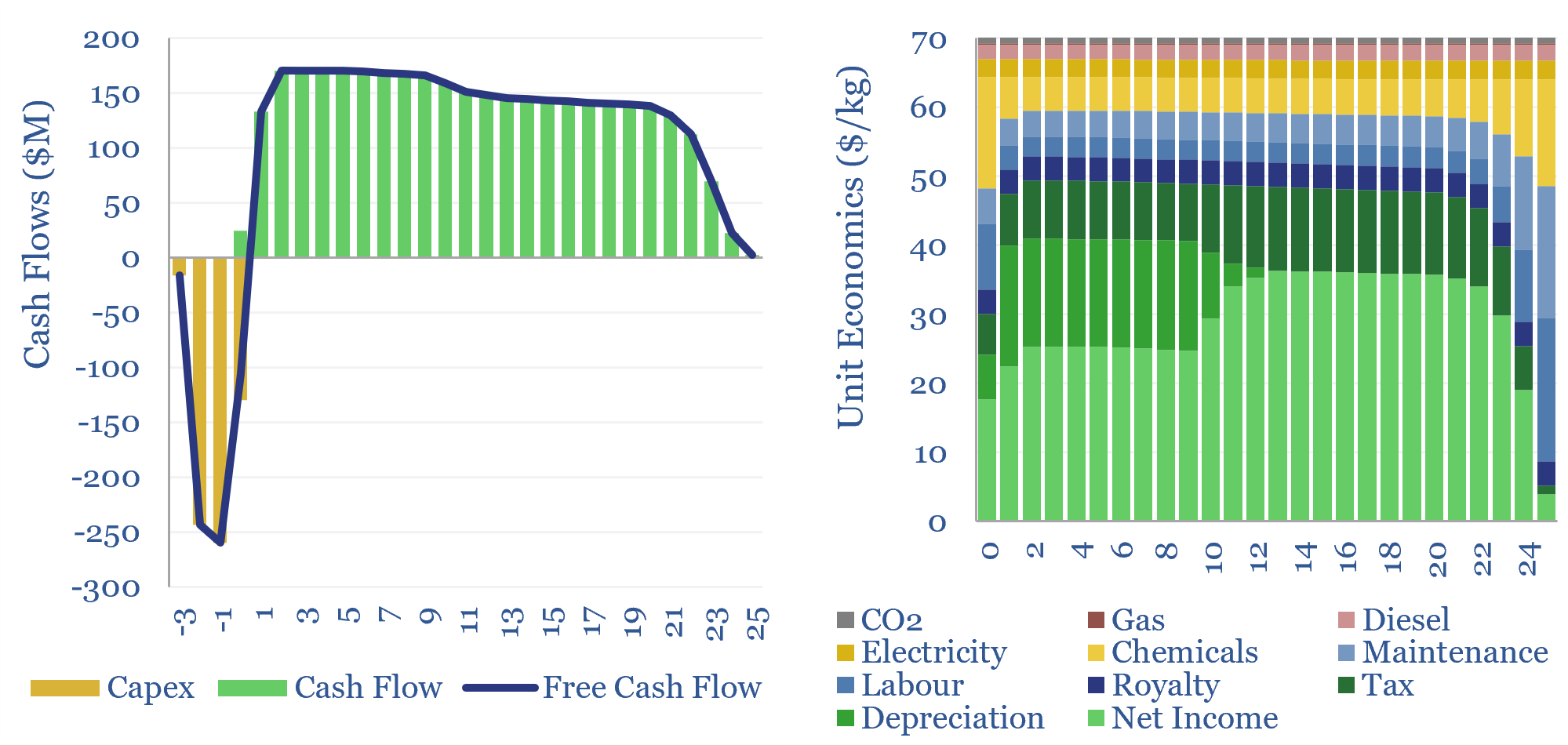

Rare Earth mining and refining: the economics?

The costs of Rare Earth mining and refining are captured in this model, requiring a $70/kg blended product price, to generate a 20% IRR on $150,000/Tpa of capex. Primary energy intensity exceeds 100 MWH/ton and CO2 intensity exceeds 20 tons/ton. Economics are particularly sensitive to ore grade, recovery rates and chemical costs.

-

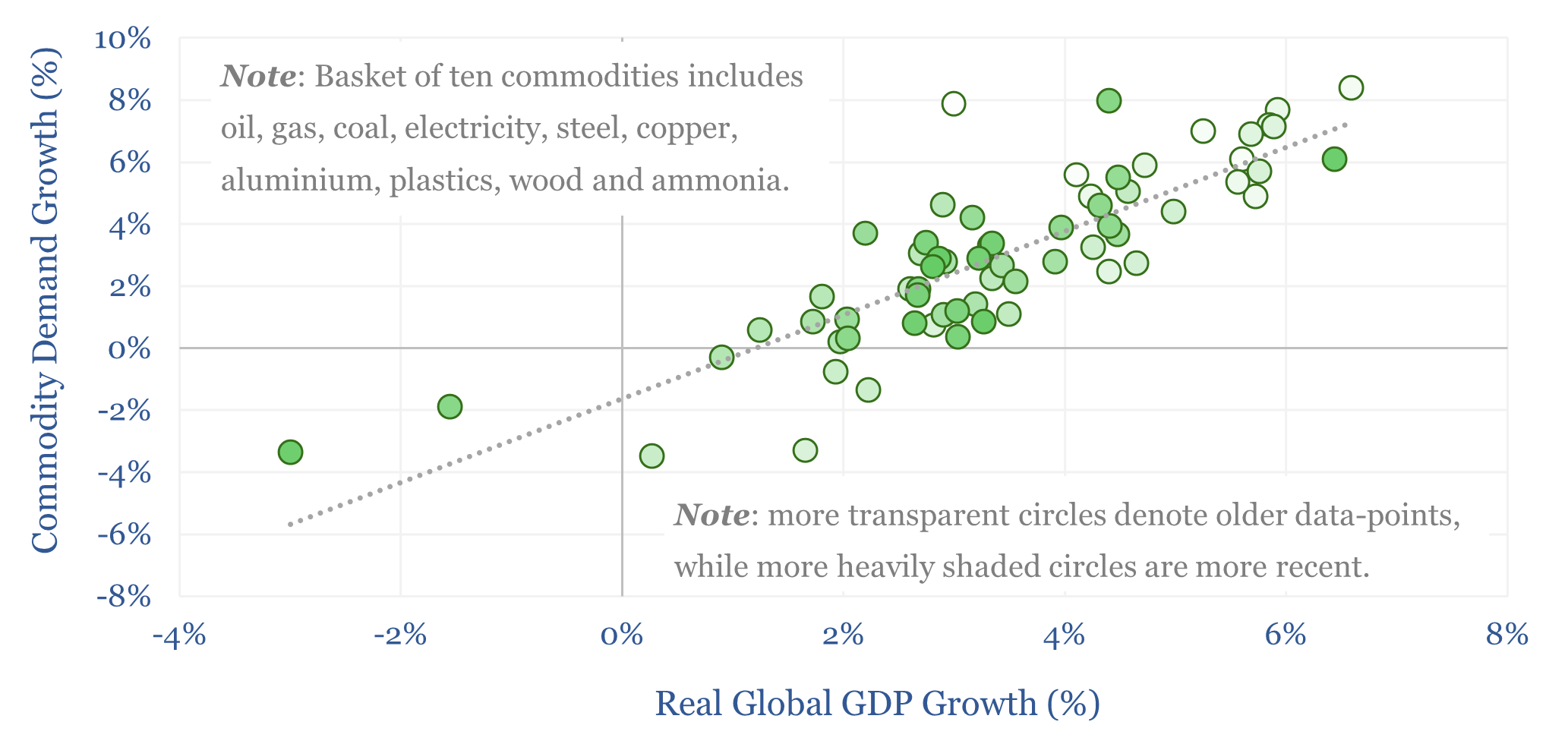

Global commodity demand: sensitivity to GDP?

Global commodity demand is levered to GDP. Specifically, for each +/- 1% acceleration or deceleration in global GDP, commodity demand tends to accelerate or decelerate by +/- 1.4%, with a 70% R-squared, across 25 examples that are indexed in this data-file. Oil demand sensitivity to GDP is particularly interesting.

-

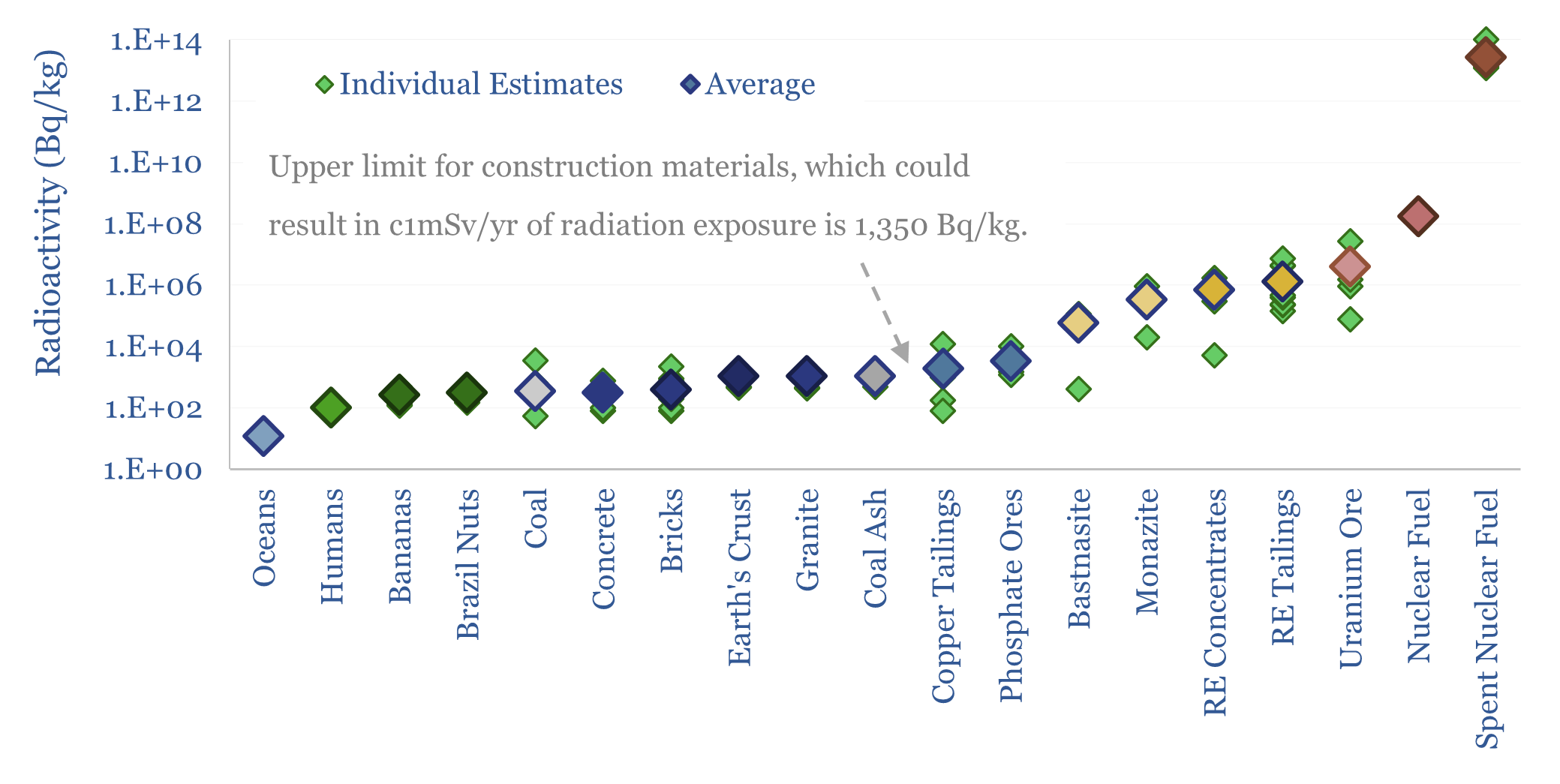

Radioactivity of materials: energy, Rare Earths and nuclear?

This data-file captures the radioactivity of materials: ranging from 10Bq/kg in sea-water, to 100Bq/kg in humans, to 300Bq/kg in Brazil nuts (the most radioactivity food), to 1,000Bq/kg in coal ash, 2,000Bq/kg in copper tailings, 0.5-1MBq/kg in Rare Earth concentrates and tailings, to 4M Bq/kg in uranium ore, 0.2 bn Bq/kg in nuclear fuel and 10-100…

-

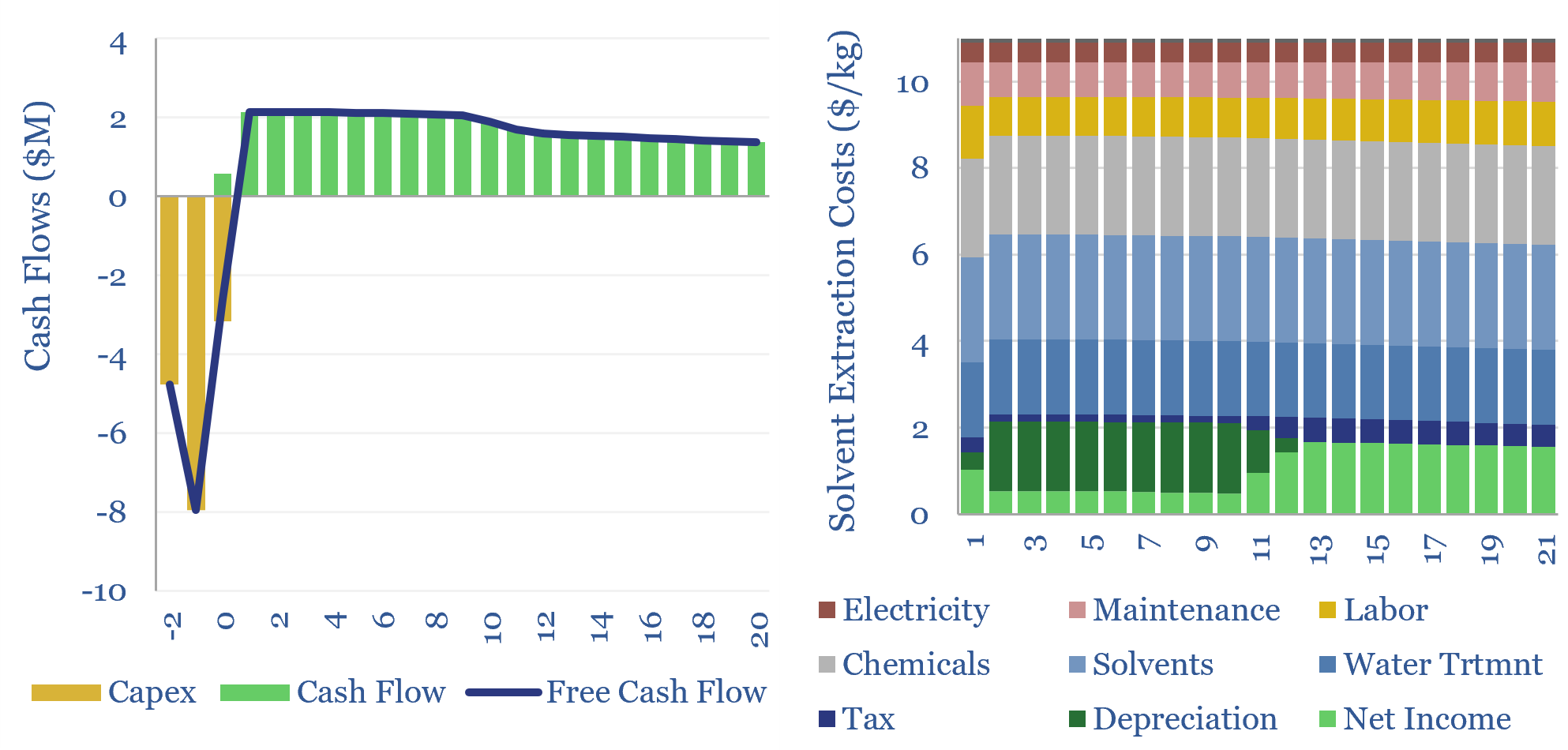

Solvent extraction: Rare Earth separations?

How are Rare Earths separated and concentrated? The process uses solvent extraction in mixer-settlers. It will typically cost over $10/kg, and possibly in the hundreds of dollars per kg. Solvent extraction costs are highly variable and can be stress-tested in this data-file.

-

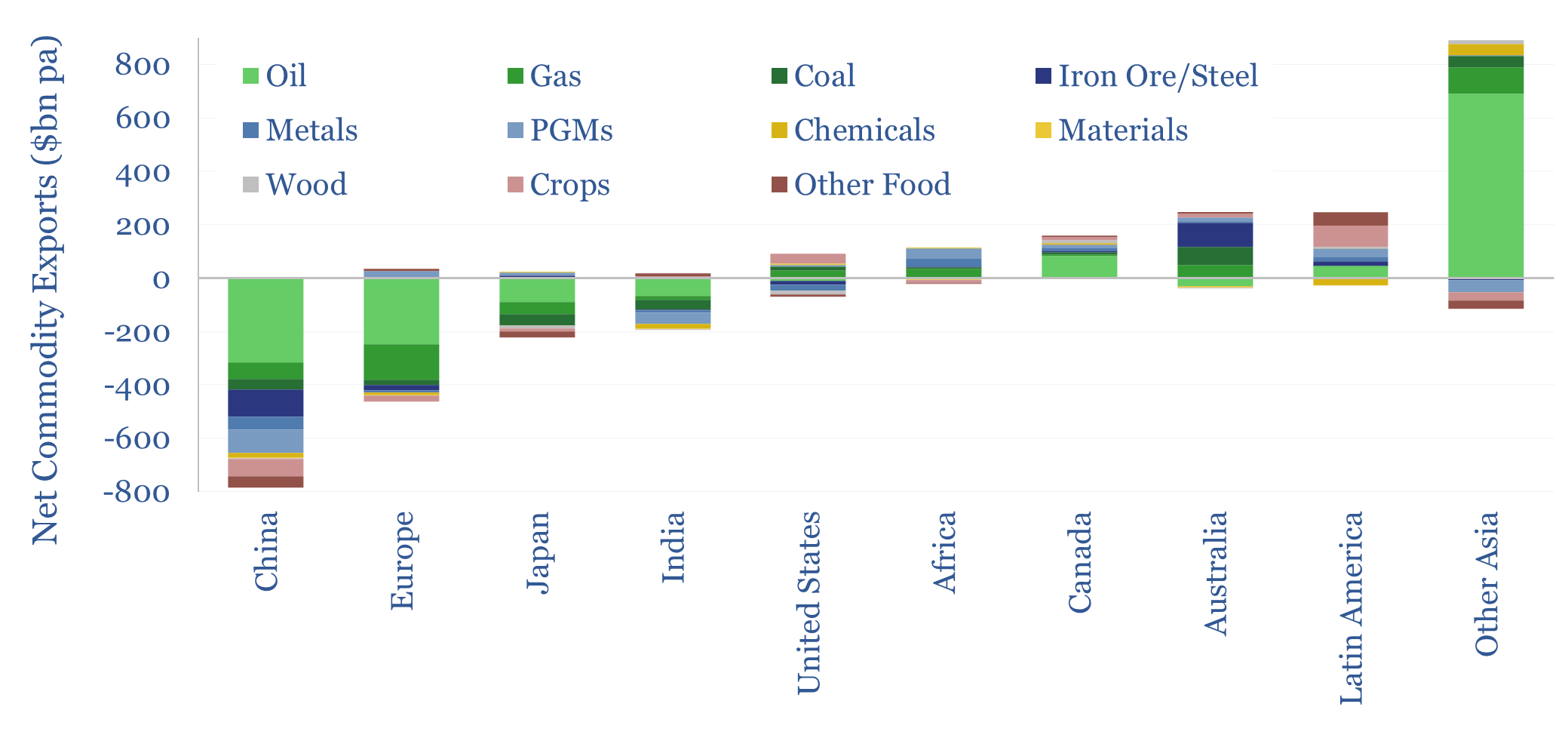

Global commodity trade: by product by region?

Commodities comprise over $6trn of of the world’s $33trn pa in global trade, or around 20%, alongside $10trn in services, $2trn of electronic goods, $1trn in cars, $1trn in mechanical capital goods. This data-file breaks down global commodity imports and exports, by country and by region.

-

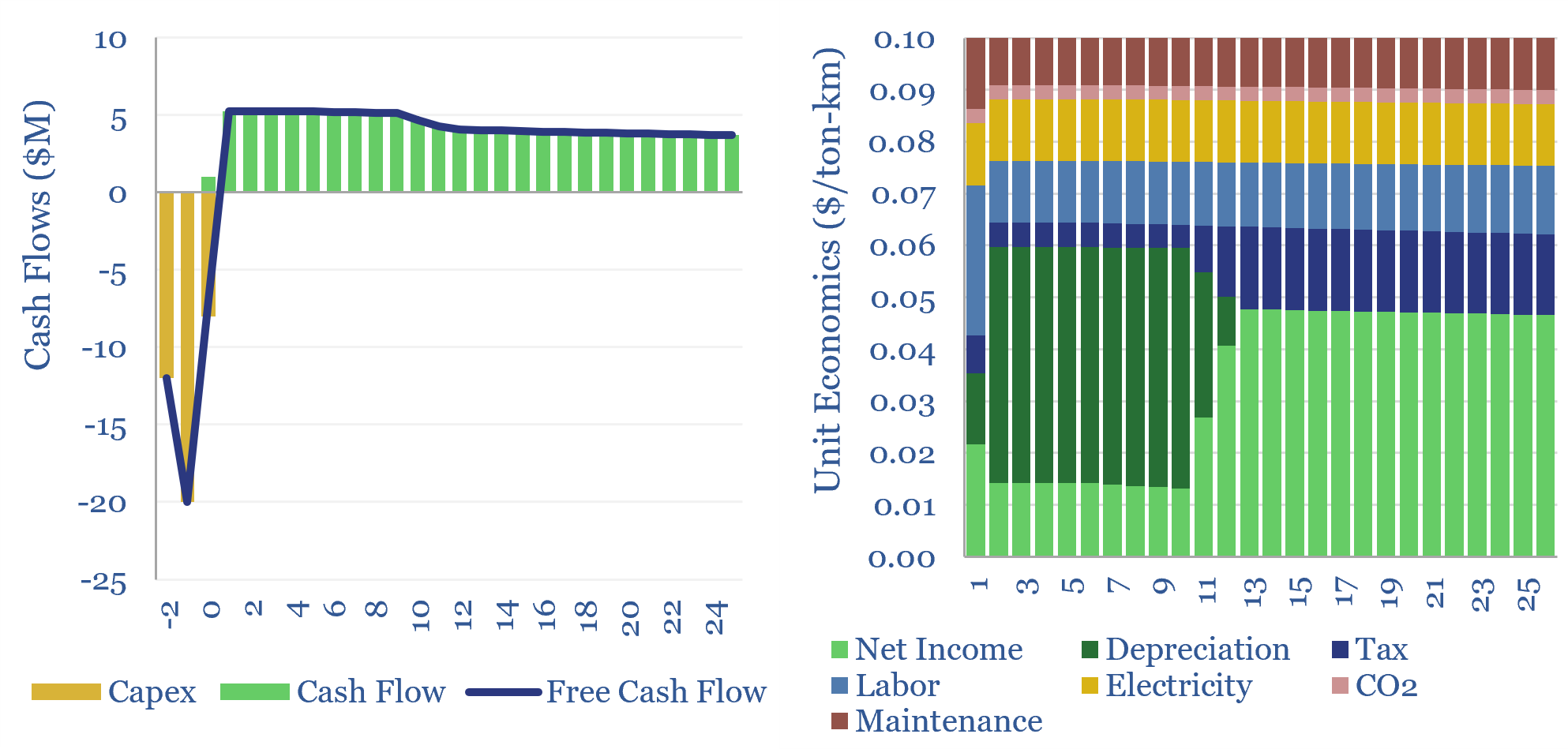

Conveyor costs: economics of moving bulk material?

Conveyors are often the most economical way to move bulk materials over long distances, e.g., from a mine to a processing plant, with an economic cost of $0.1/ton-km, in order to generate a 10% IRR on capex, opex and other costs. These costs are c30% lower than for heavy trucks, opex is at least 60%…

Content by Category

- Batteries (88)

- Biofuels (44)

- Carbon Intensity (49)

- CCS (63)

- CO2 Removals (9)

- Coal (38)

- Company Diligence (93)

- Data Models (834)

- Decarbonization (160)

- Demand (110)

- Digital (59)

- Downstream (44)

- Economic Model (203)

- Energy Efficiency (75)

- Hydrogen (63)

- Industry Data (278)

- LNG (48)

- Materials (82)

- Metals (79)

- Midstream (43)

- Natural Gas (148)

- Nature (76)

- Nuclear (23)

- Oil (164)

- Patents (38)

- Plastics (44)

- Power Grids (127)

- Renewables (149)

- Screen (116)

- Semiconductors (30)

- Shale (51)

- Solar (67)

- Supply-Demand (45)

- Vehicles (90)

- Wind (43)

- Written Research (352)