Company Diligence

-

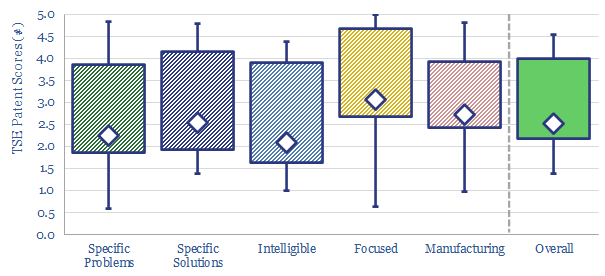

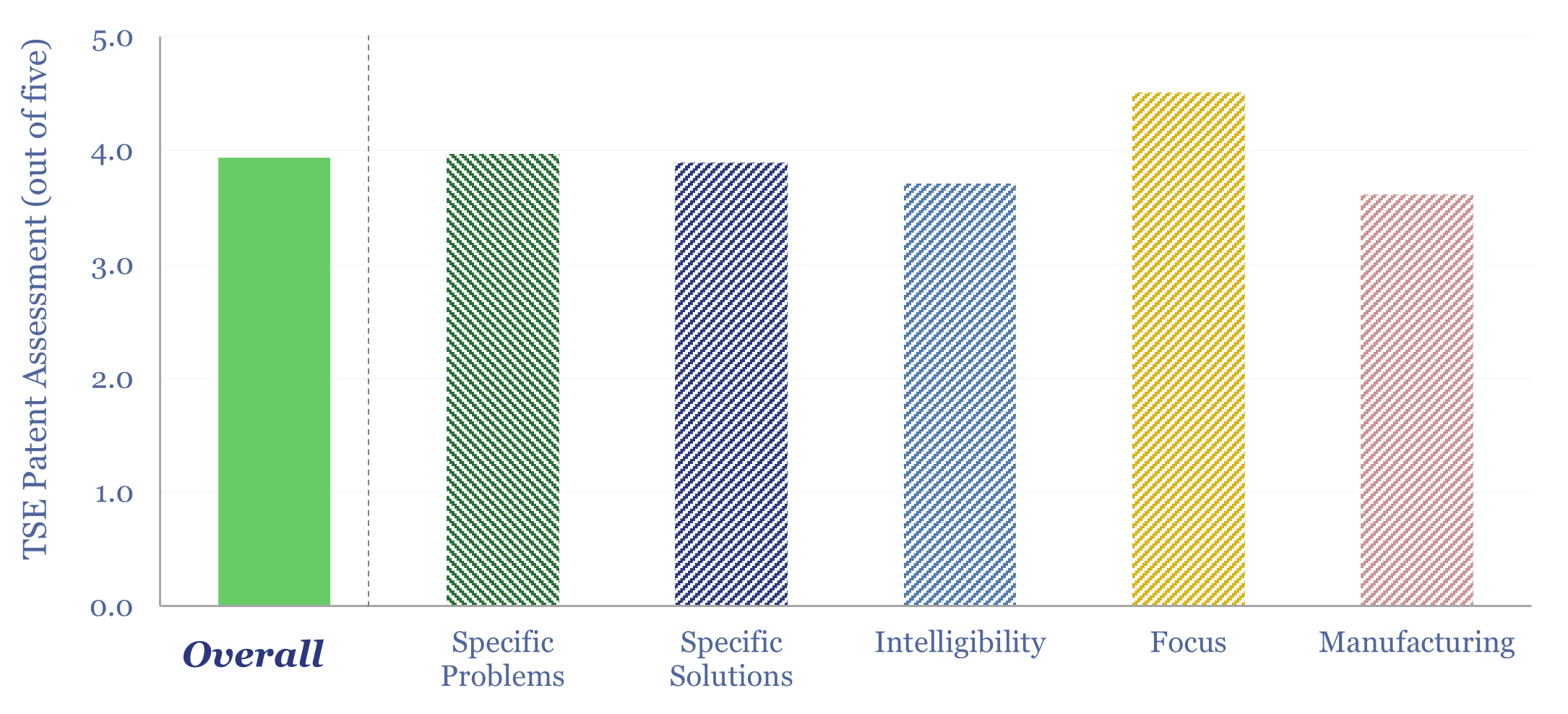

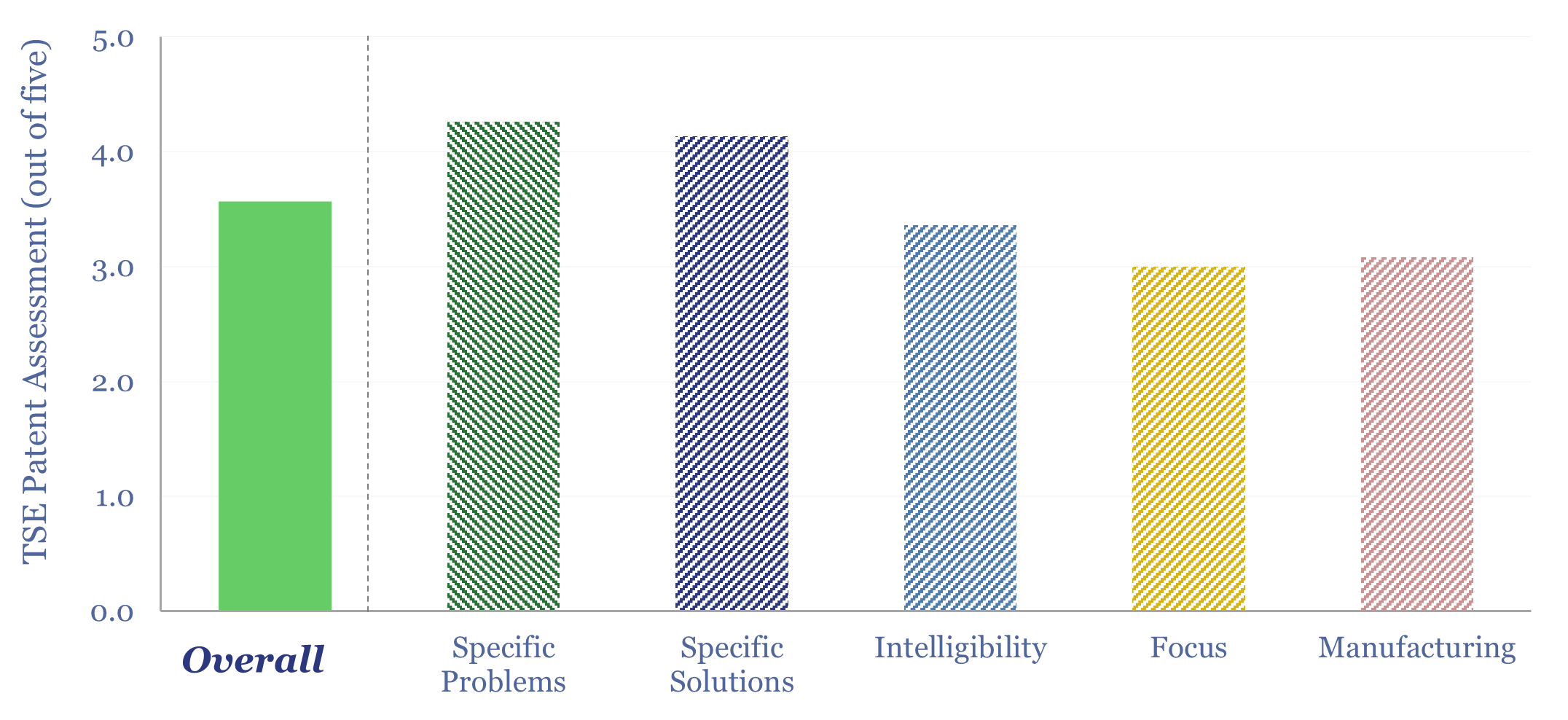

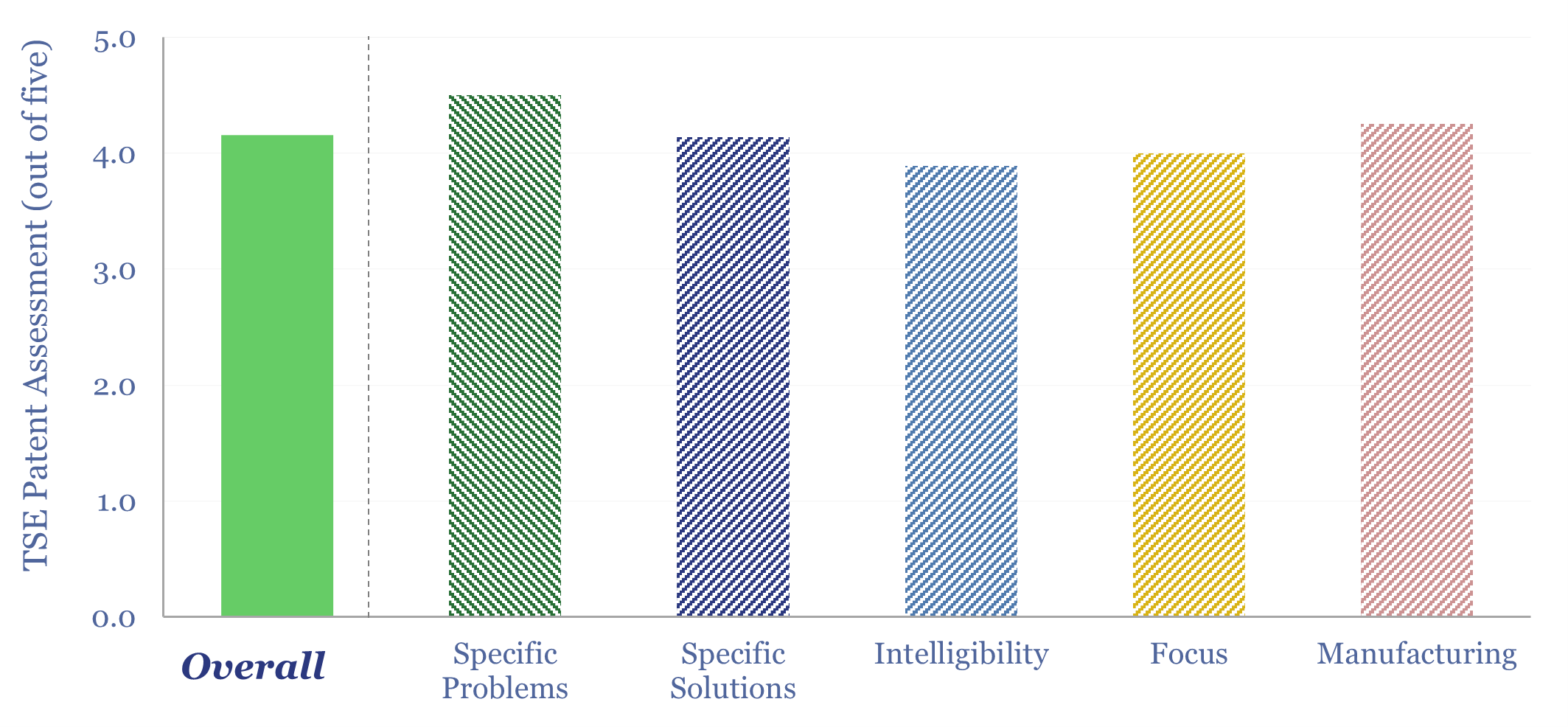

TSE Patent Assessments: a summary?

This data-file aggregates all of our patent assessments into a single reference file, so different companies’ scores can be compared and contrasted. Our average score is 3.5 out of 5.0. Skew is to the downside. Intelligibility is the biggest challenge. Scores correlate with TRL and revenues.

-

Zipline: drone delivery technology?

Details of Zipline drone delivery technology are derived in this data-file, based on reviewing over 15 highly detailed patent families from the company. We see a moat around specific hardware innovations, a low cost sensor suite, inherent safety from seven layers of safety protections, and a sophisticated fleet management system.

-

CATL: sodium ion battery breakthrough?

Contemporary Amperex Technology Co. Limited (CATL) is a Chinese battery manufacturer, HQ’d in Fusian, founded in 2011, with >30,000 employees. It may produce as many as one-third of all the lithium ion batteries in the world. This data-file assesses whether it has made a breakthrough in sodium ion batteries.

-

Fervo Energy: enhanced geothermal technology?

Fervo Energy is a leader in enhanced geothermal systems, harvesting 400°F+ heat from hot, deep rock formations, as fluids flow from fracced horizontal injectors to fracced horizontal producers. This Fervo Energy technology review is based on reviewing a dozen patent families. Fervo draws on fiber optic sensing data to optimize the well completion process and…

-

Schlumberger: AI and machine learning patents?

We have screened 65 Schlumberger AI and machine learning patents, filed in 2024-25. This is more than any other energy company. We expect AI to improve shale well productivity, entrench the reliance on Schlumberger tools and services, while also reducing costs, labor, time and net energy use in oil and gas.

-

Aixtron: power GaN MOCVD technology?

Aixtron has a market leading position in GaN MOCVD technology, which is increasingly used in the power electronics of data centers, solar and EVs. This data-file assesses 20 patents from Aixtron and Veeco, to unpack how GaN MOCVD works, what are the key challenges, and to quantify Aixtron’s potential moat.

-

Enphase: GaN microinverter technology?

Enphase is a global leader in microinverters. In 2026, it released its first GaN-based microinverter, reducing weight by 25% and volume by 35%. Specific innovations come out in the patents and suggest more radical changes lie ahead, for even more power dense microinverters based on cycloconverter topologies. But does this confer any kind of edge…

-

ANYbotics: quadrupedal inspection robots?

ANYbotics’ quadrupedal inspection robot, ANYmal, has been ruggedized for industrial inspections. We reviewed ANYbotics’ patents and case studies, which suggest growing applications, a moat around the technology, and great upside for robots across energy, mining and manufacturing. Details and conclusions are in this data-file.

-

Lancium: can AI data-centers load shift?

Lancium data center technology is used to develop Clean Campuses, which can separate large compute requirements into critical and flexible clusters. The flexible clusters tackle non-time critical loads, often powered directly by microgrids, and providing a Controllable Load Resource, which can demand shift to smooth the volatility of renewables? Hence we reviewed Lancium’s patents.

-

Rockwell Automation: IoT acronyms?

Rockwell Automation is the largest pure-play automation company in the world. It integrates real-time data and controls thousands of components across typical industrial facilities, often saving energy, costs and raising throughputs. This data-file reviews its product offering, case studies and IoT and automation acronyms.

Content by Category

- Batteries (96)

- Biofuels (44)

- Carbon Intensity (48)

- CCS (64)

- CO2 Removals (9)

- Coal (44)

- Commentary (65)

- Company Diligence (105)

- Data Models (927)

- Decarbonization (162)

- Demand (131)

- Digital (89)

- Downstream (47)

- Economic Model (222)

- Energy Efficiency (76)

- Hydrogen (63)

- Industry Data (310)

- LNG (56)

- Materials (86)

- Metals (89)

- Midstream (45)

- Natural Gas (163)

- Nature (76)

- Nuclear (28)

- Oil (178)

- Patents (39)

- Plastics (44)

- Power Grids (156)

- Renewables (153)

- Screen (138)

- Semiconductors (35)

- Shale (58)

- Solar (72)

- Supply-Demand (53)

- Vehicles (94)

- Video (24)

- Wind (46)

- Written Research (409)