Nature

-

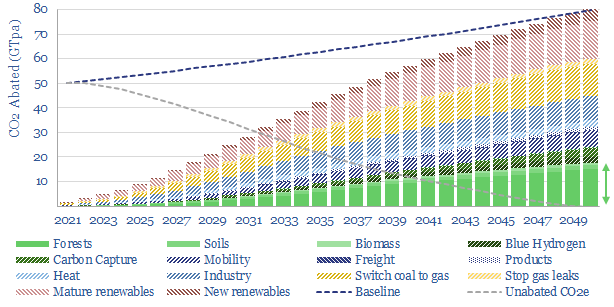

Nature based solutions to climate change?

Nature based solutions are likely to deliver c20-25% of the decarbonization in a realistic roadmap to net zero. Reforestation is low-cost (c$50/ton), technically ready, convenient and helps nature. Key challenges are improving the quality of nature-based CO2 removals and accelerating momentum. We see upside for companies that can clear these hurdles. Our top ten conclusions…

-

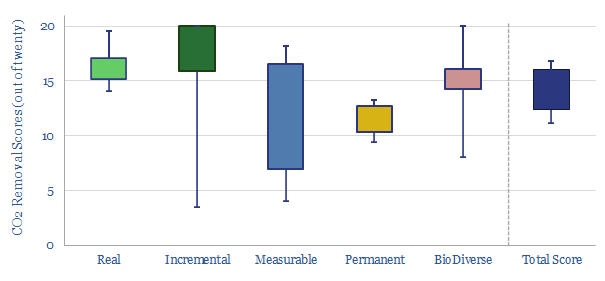

Nature-based CO2 removals: a summary?

This data-file aggregates the details of different nature-based CO2 removals projects that we have been supporting at Thunder Said Energy. The average nature-based reforestation initiative that we supported in 2022 scored 70/100 on our framework. Statistical details and distributions are explored.

-

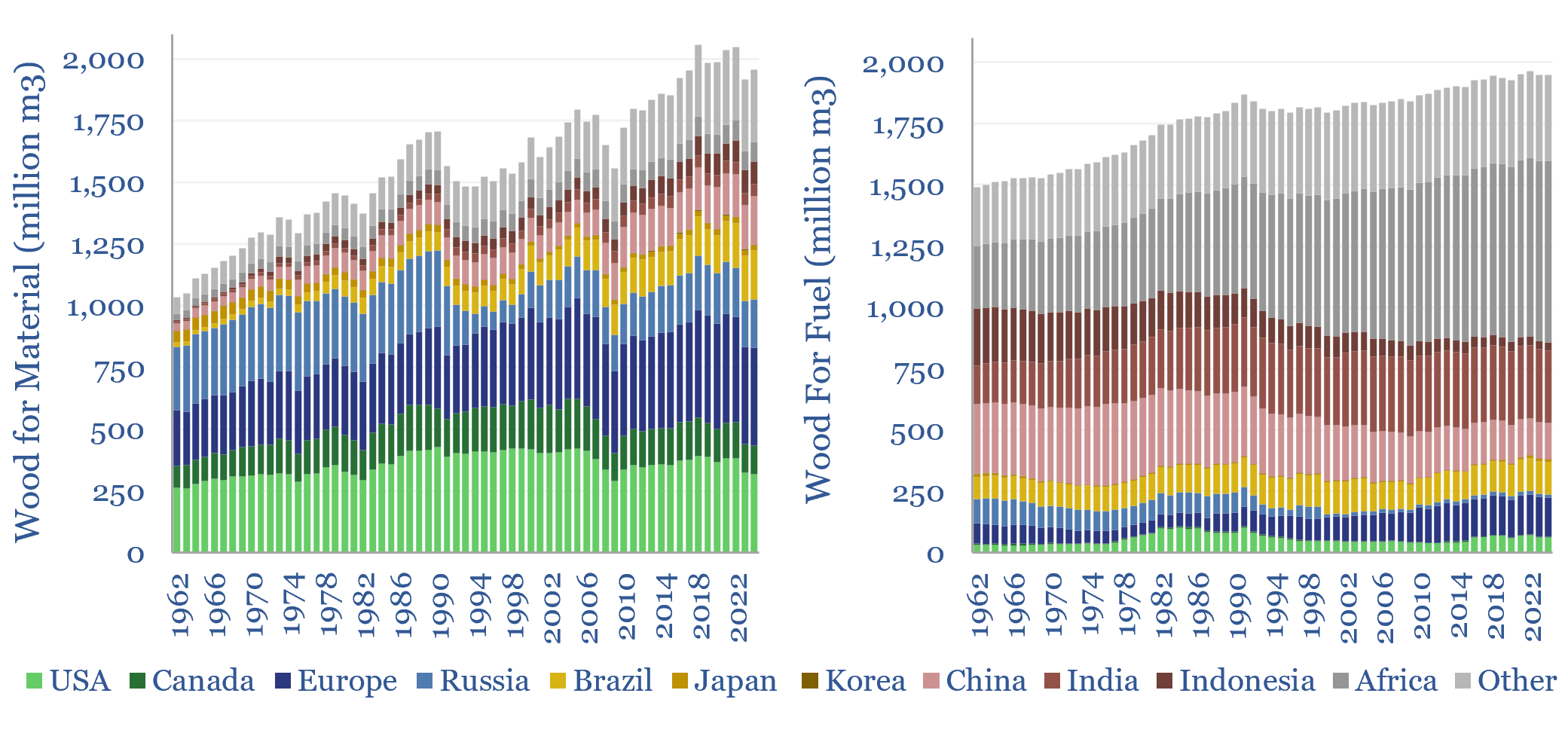

Global wood production: supply by country by year?

This data-file quantifies global wood production, country-by-country, category-by-category, back to 1960, using granular data from the FAO. 4bn m3 of wood is harvested per year (2GTpa by mass). There is a read-across for how commodities peak. And major upside for LNG.

-

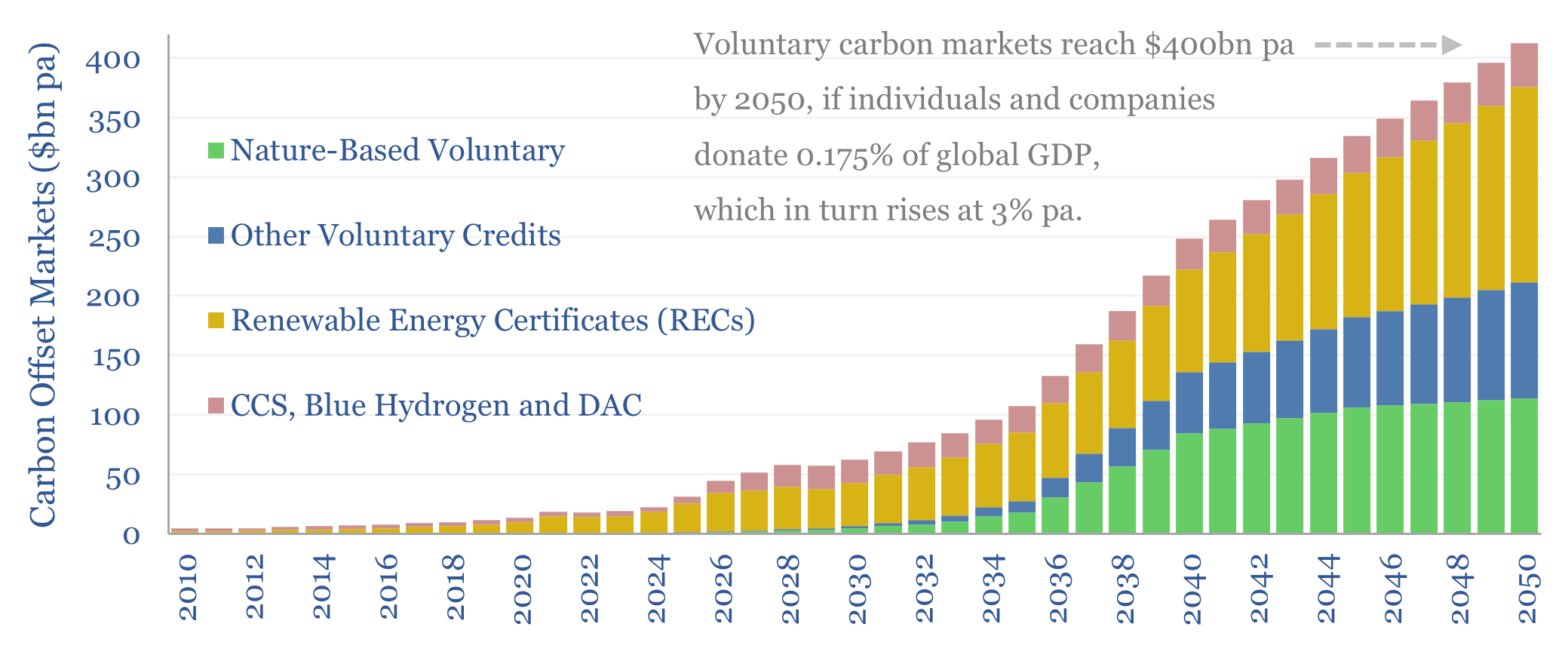

Carbon markets: charity case?

Carbon markets incentivize renewable energy, CCS, DAC, nature-based solutions and other CO2 offsets. In the past, we naïvely assumed these would grow as much as needed to reach Net Zero by 2050. This 14-page note revises our forecasts, by analogy to other forms of charitable giving. We see voluntary carbon markets reaching $400bn pa by…

-

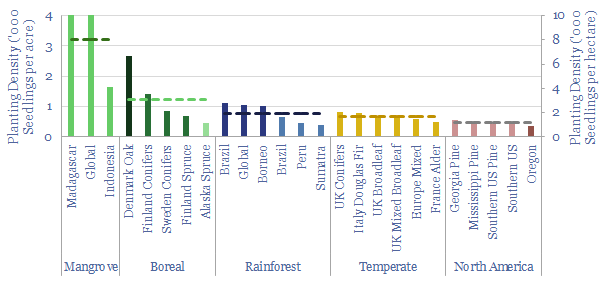

Reforestation: what planting density for seedlings?

What is the typical planting density for reforestation projects globally? This matters as it can determine the costs of reforestation. Hence in this data-file we have collated data from 25 different case studies globally, which have tended to plant a median of 670 seedlings per acre (1,650 per hectare).

-

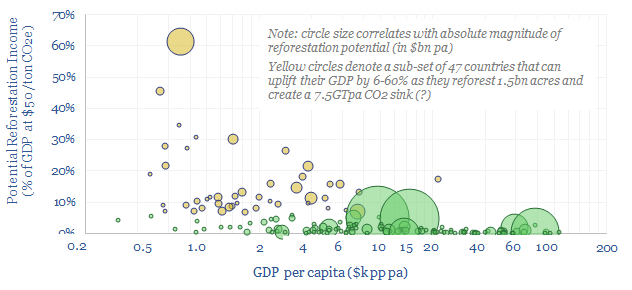

Growing economies: reforest and reinvest?

CO2 removal credits could add 6-60% to the GDP of 47 emerging countries as they reforest 1.5bn acres and create a 7.5GTpa CO2 sink, while the resultant cash flows could double these countries’ investment rates. Reinvesting in wind, solar, electrification avoids higher carbon fuels and deforestation for firewood. Reinvesting in timber value chains maximizes CO2…

-

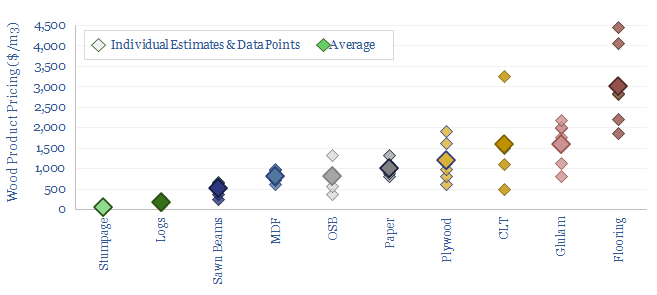

Wood products: typical pricing?

This data-file aggregates the pricing of different wood products, as storing carbon in long-lived materials matters amidst the energy transition. It can also add economic value. While upgrading raw timber into high value materials can uplift realized pricing in reforestation projects by 20-60x, which improves the permanence of nature-based CO2 removal credits.

-

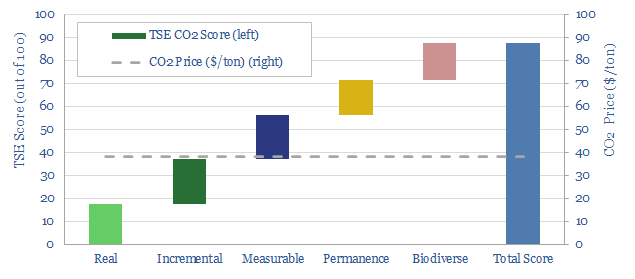

CO2 removals: CO2OL Panama project?

The CO2OL Tropical Mix project has planted 9M trees on 13,000 hectares of degraded pasture land across 45 sites in Panama since 1995. 20-30% of the land is reserved for conservation. The project achieved a relatively high score of 88/100 on our usual assessment framework. CO2 credits are priced at $38/ton. We contributed $1,900 to…

-

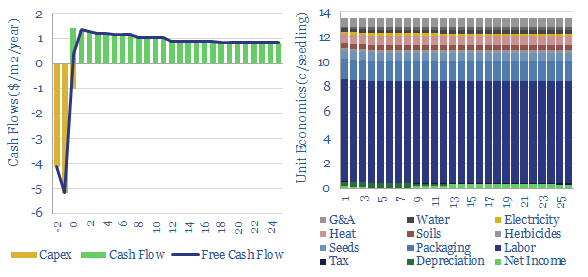

Tree seedlings: costs and economics?

The US plants over 1.3bn tree seedlings per year. Especially pine. These seedlings are typically 8-10 months old, with heights of 25-30mm, root collars of 5mm, and total mass of 5-10 grams, having been grown by dedicated producers. This data-file captures the costs of tree seedlings, to support afforestation, reforestation or broader forestry.

-

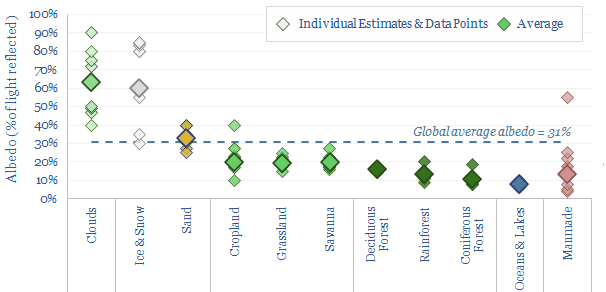

Albedo of different landscapes: a challenge for reforestation?

Forests are darker than their surroundings? So does their low albedo curb our enthusiasm for nature-based solutions? This data-file aggregates the average albedo of different landscapes. The albedo impact of reforestation seems numerically very small. There is even an intriguing link where forests can increase the formation of clouds, which have the highest average albedo…

Content by Category

- Batteries (96)

- Biofuels (44)

- Carbon Intensity (48)

- CCS (64)

- CO2 Removals (9)

- Coal (44)

- Commentary (65)

- Company Diligence (105)

- Data Models (928)

- Decarbonization (163)

- Demand (131)

- Digital (92)

- Downstream (47)

- Economic Model (222)

- Energy Efficiency (76)

- Hydrogen (63)

- Industry Data (311)

- LNG (56)

- Materials (86)

- Metals (89)

- Midstream (45)

- Natural Gas (163)

- Nature (76)

- Nuclear (28)

- Oil (178)

- Patents (39)

- Plastics (44)

- Power Grids (156)

- Renewables (153)

- Screen (139)

- Semiconductors (36)

- Shale (58)

- Solar (72)

- Supply-Demand (53)

- Vehicles (94)

- Video (24)

- Wind (46)

- Written Research (410)