Nuclear

-

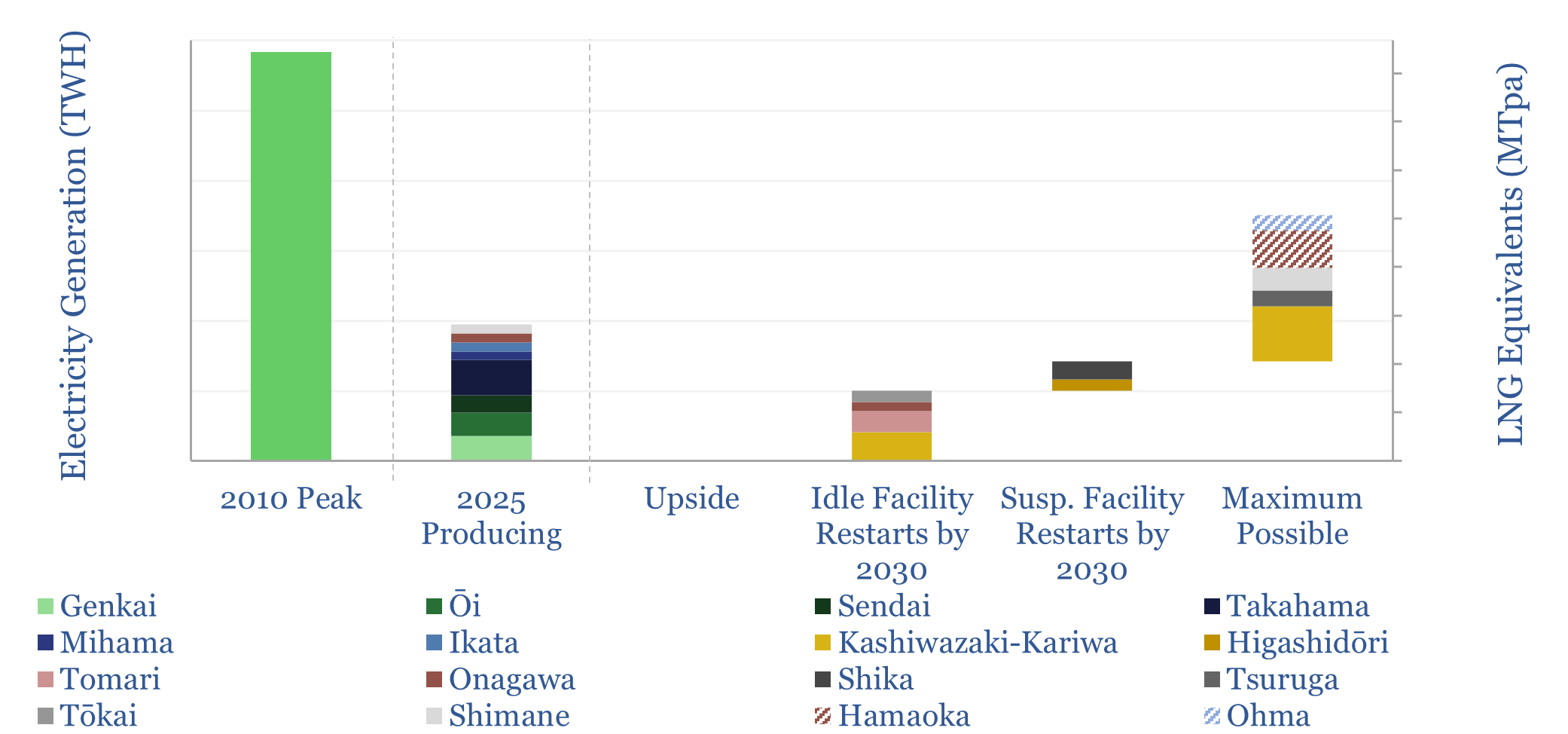

Japan: nuclear restart tracker?

This data-file looks through 17 major nuclear plants in Japan with 45GW of operable capacity, covering the key parameters and restart news on each facility. Japan’s nuclear restart had ramped output back to 97TWH pa by 2025, and may rise by a further 80 TWH by 2030, to meet targets for 20% nuclear in the…

-

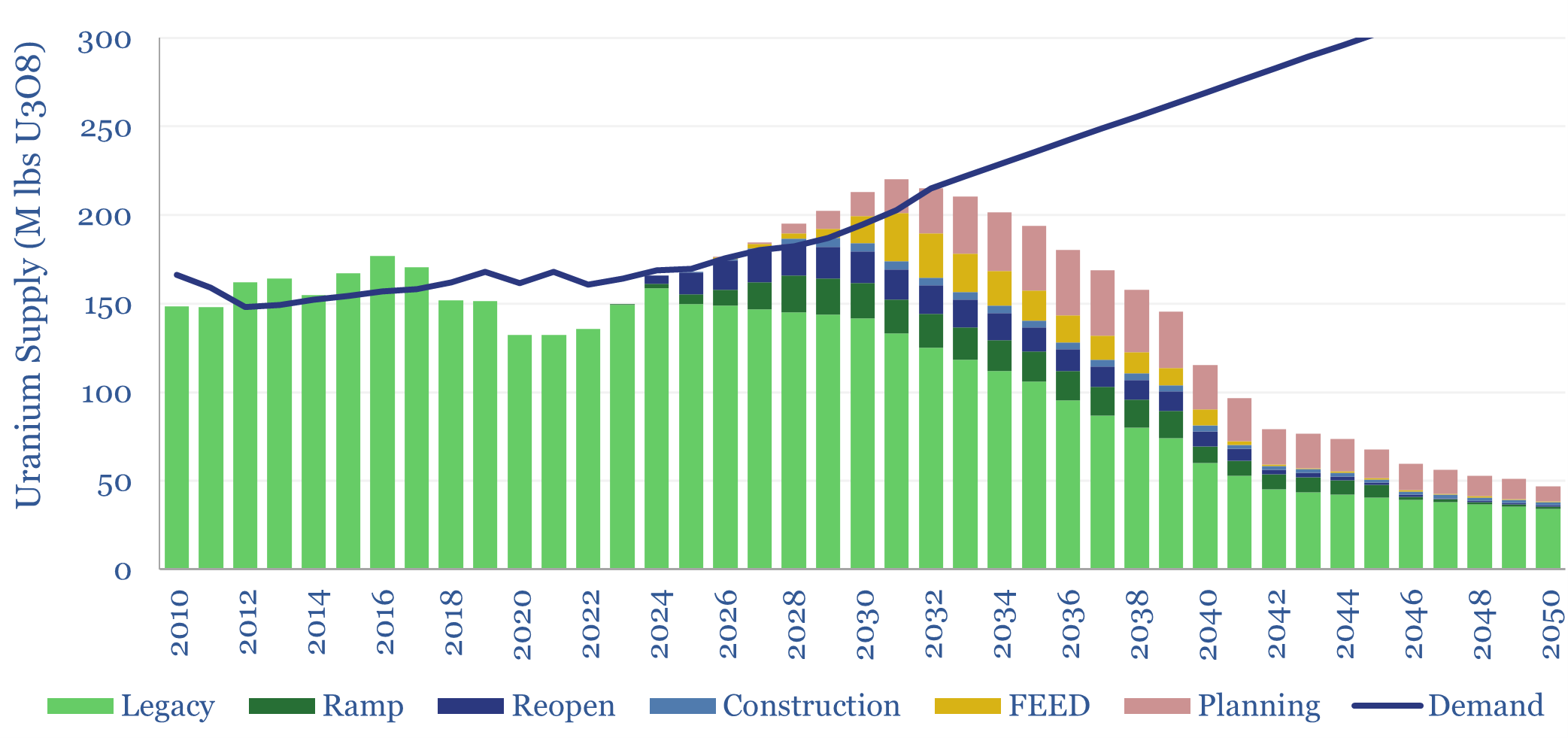

Global uranium supply-demand?

Our global uranium supply-demand model sees the market adequately supplied in 2026-30, even as demand ramps from 170M lbs pa to 210M lbs pa in 2030. However, our project risking is generous and there may be supply disruptions. What implications for broader power markets, decarbonization ambitions, and uranium prices?

-

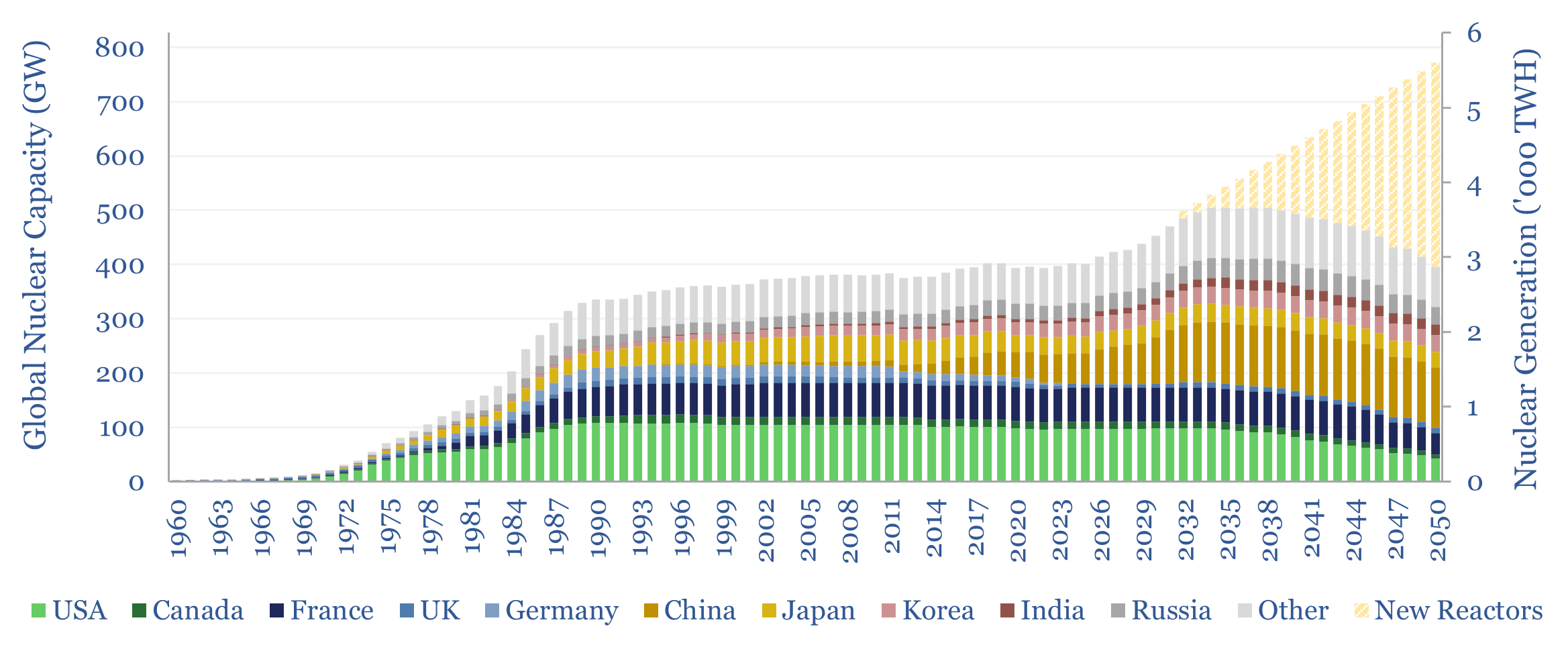

Global nuclear capacity: by reactor, by country, over time?

Global nuclear capacity, by reactor, by country, and over time, are built up in this data-file, by reviewing the construction, operation and shutdowns of 800 global nuclear reactors. After running sideways for 20-years, at 2,800 TWH pa, global nuclear generation rises at c3% pa to 2030, and c3% pa to 2050, reaching 5,600 TWH pa.

-

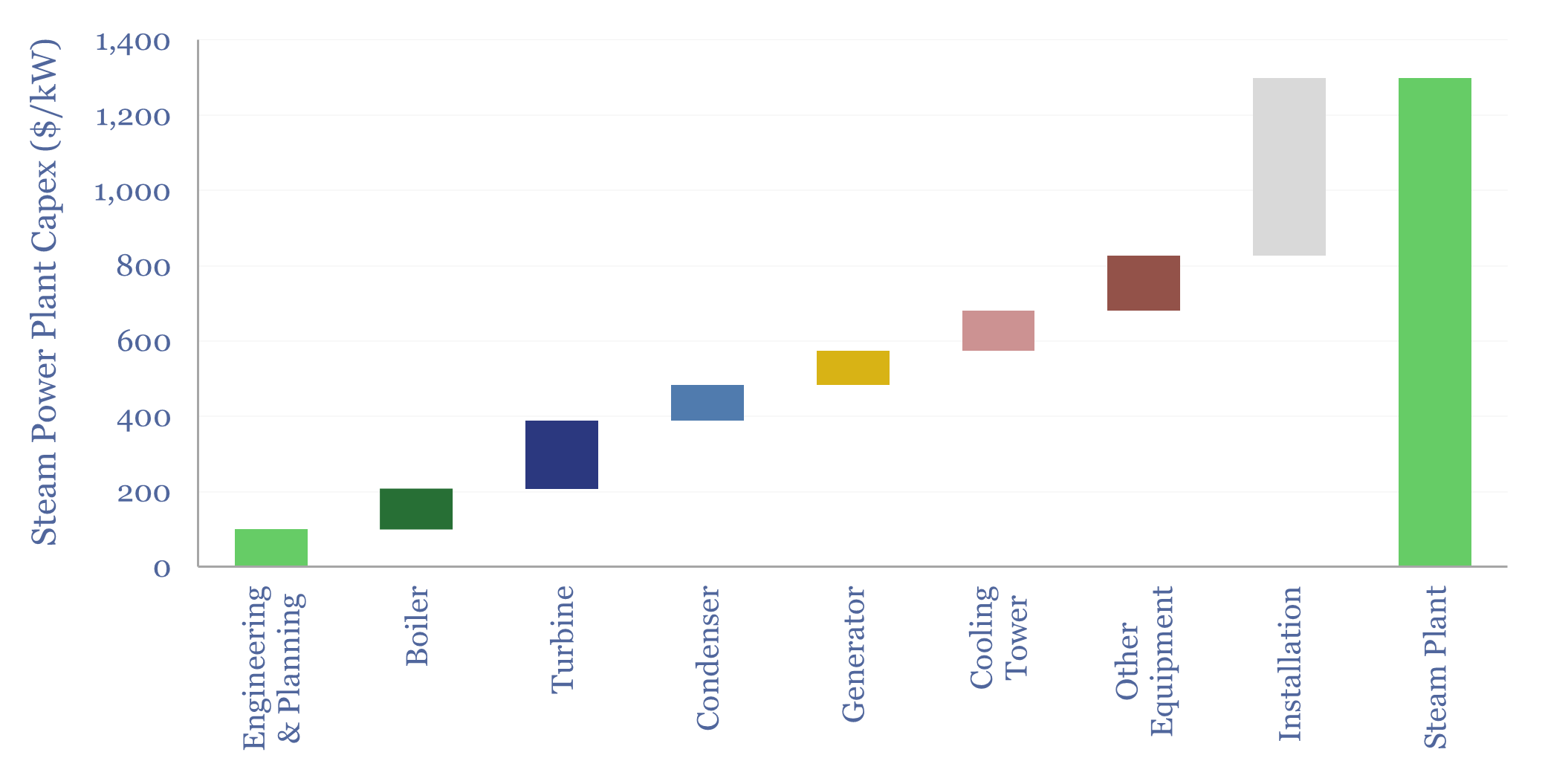

Steam generation: capex costs?

Steam power generation requires boilers, turbines, condensers and generators, which are often integrated into a steam generation “island” at coal, nuclear and CCGT power plants. Steam generation capex costs are estimated at $1,300/kW in this data-file, based on sampling component costs across 35 past projects.

-

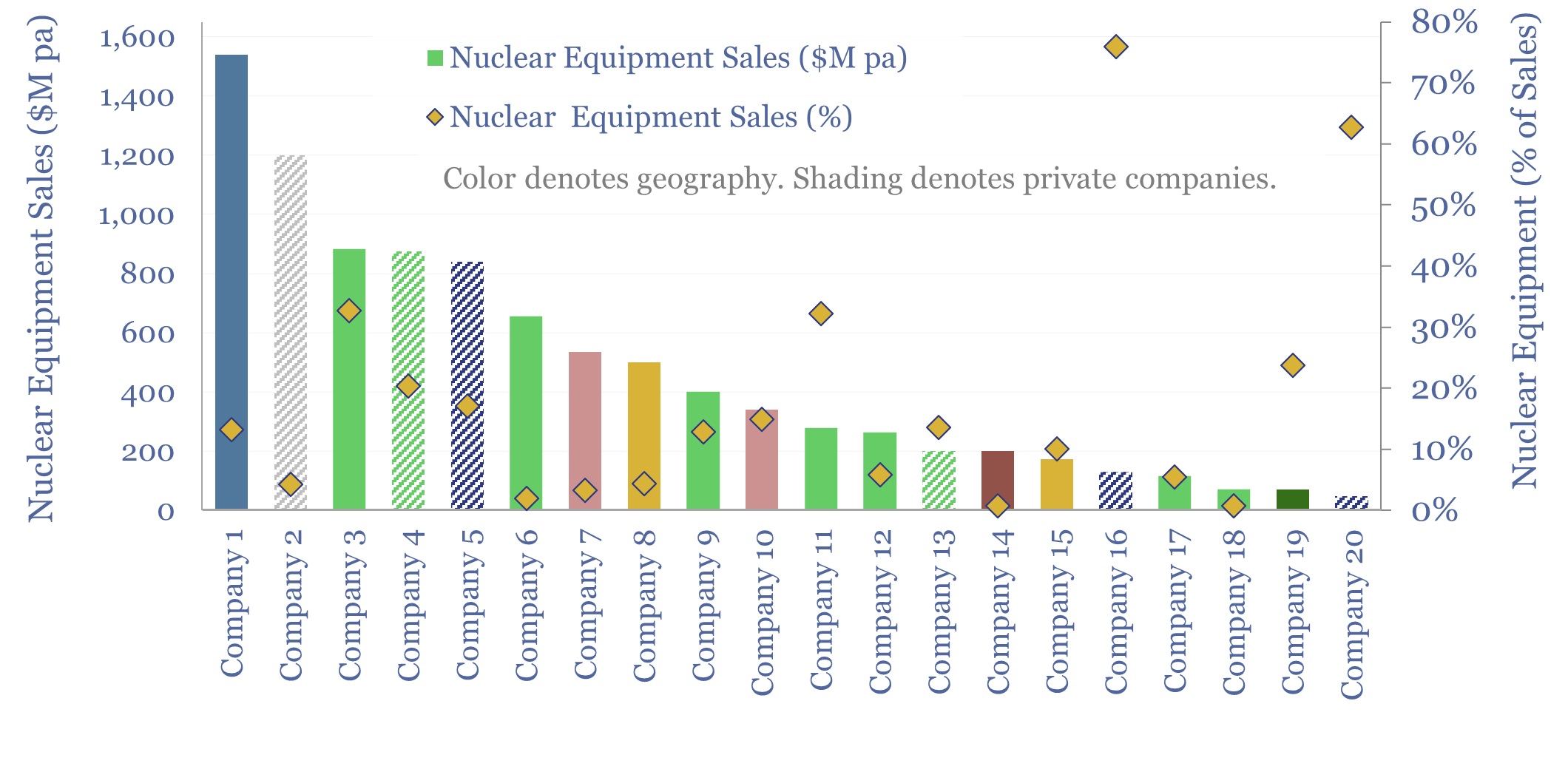

Nuclear equipment manufacturers: company screen?

Nuclear equipment manufacturers are captured in this company screen, covering 20 companies, with $10bn pa of revenues, c10% EBIT margins, and a 5% average sales exposure to nuclear components. Our notes also capture key details, equipment specializations, and recent focuses of each company.

-

Deep Fission: next-gen nuclear technology?

Deep Fission is designing a next-generation nuclear reactor, placing small modular reactors in 1-mile-deep boreholes, which provide exceptional containment, and may eliminate up to 80% of the surface costs of large nuclear plants. We find strong inherent safety features and can de-risk c50% lower costs than large fission reactors via the Deep Fission technology.

-

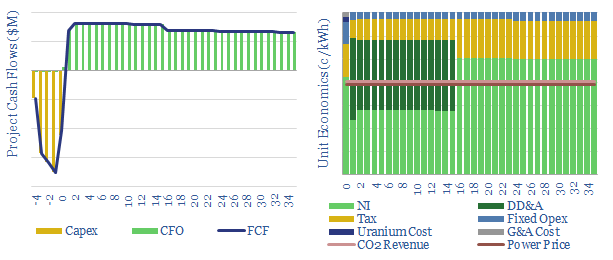

Nuclear Power Project Economics

This data-file models the costs of nuclear power project, based on technical papers and past projects around the industry. An up-front capex cost of $6,000/kW might yield a levelized cost of 15c/kWh. But 6-10c/kWh is achievable via a renaissnace in next-generation nuclear.

-

Nuclear uprates: capex costs?

Nuclear uprates could add 5-10GW to the US’s 100GW nuclear fleet, simply by running existing reactors harder or upgrading their equipment. The capex costs of nuclear uprates are tabulated in this data-file, across a dozen case studies, ranging from $200 – $7,000/kW. Does this position uprates ahead of SMRs on the nuclear cost curve?

-

Nuclear SMRs: grown ups?

Can small modular reactors (SMRs) reignite growth in the nuclear industry, by halving capex to $3,000-4,000/kW, thus reducing levelized costs of zero-carbon electricity to 8-10 c/kWh? This 18-page report presents five considerations around SMR costs, to help understand the risks of persistently high capex requirements. We still see gas and solar dominating future load growth.

-

Next-generation nuclear companies: future fission and fusion?

This data-file screens c30 next-generation nuclear companies at the cutting edge of fission and fusion technology. The median one employs 100 people, is developing a 150MWe reactor, and could reach commerciality by 2035. But how has this landscape of companies progressed in the past few years?

Content by Category

- Batteries (96)

- Biofuels (44)

- Carbon Intensity (48)

- CCS (64)

- CO2 Removals (9)

- Coal (44)

- Commentary (65)

- Company Diligence (105)

- Data Models (928)

- Decarbonization (163)

- Demand (131)

- Digital (92)

- Downstream (47)

- Economic Model (222)

- Energy Efficiency (76)

- Hydrogen (63)

- Industry Data (311)

- LNG (56)

- Materials (86)

- Metals (89)

- Midstream (45)

- Natural Gas (163)

- Nature (76)

- Nuclear (28)

- Oil (178)

- Patents (39)

- Plastics (44)

- Power Grids (156)

- Renewables (153)

- Screen (139)

- Semiconductors (36)

- Shale (58)

- Solar (72)

- Supply-Demand (53)

- Vehicles (94)

- Video (24)

- Wind (46)

- Written Research (410)