Digital

-

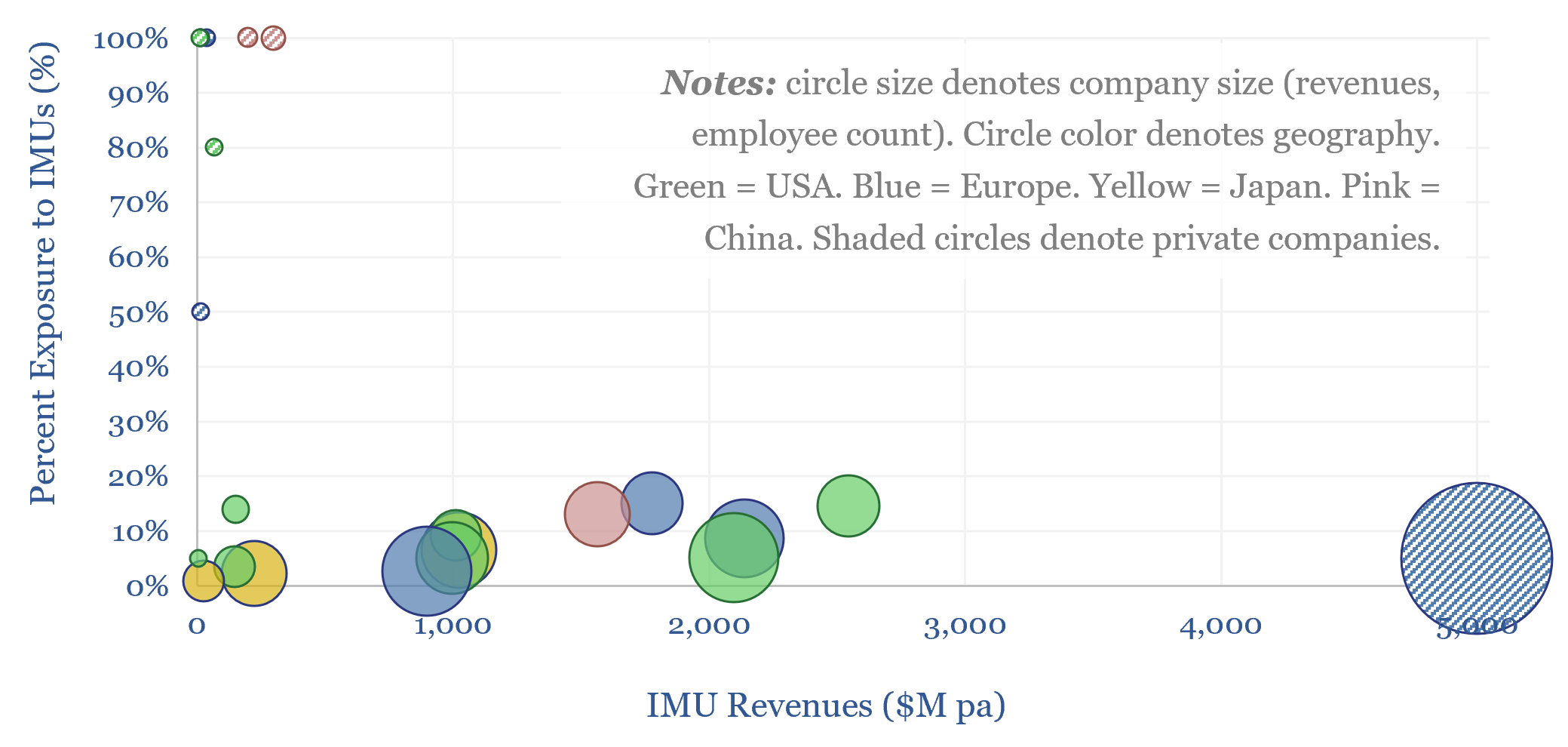

Inertial measurement units: force to reckon with?

Inertial Measurement Units (IMUs) comprise accelerometers, gyroscopes and possibly magnetometers. These sensors tell you how far/fast you are traveling, and in which direction. The market is $30bn pa and expands to $80bn by 2035, due to the rise of physical AI. This 14-page report is our overview and covers leading sensor companies.

-

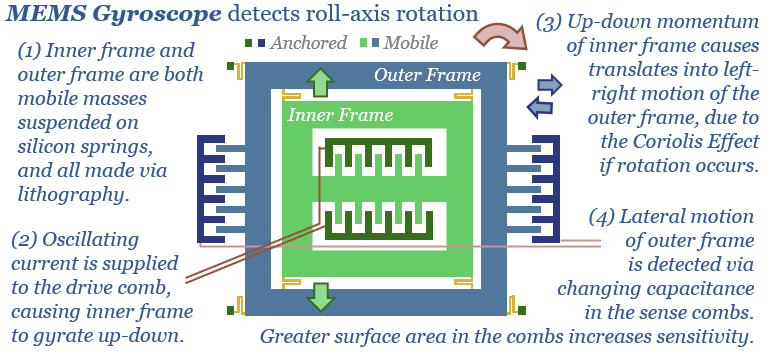

Inertial sensors: leading companies?

Learing inertial sensor companies are screened in this data-file, capturing 25 producers of inertial measurement units, accelerometers, gyroscopes and other MEMS sensors, as well as the price, performance and technical parameters of underlying IMU products.

-

Ten investment themes for 2026-30?

The global energy and industrial landscape is undergoing an AI energy transition. We have also recently published our top ten themes for 2H26. Hence what would be the top ten investment themes for 2026-30, amidst these new technologies, policies and opportunities? This article sets out the ideas that excite us most, with links to supporting…

-

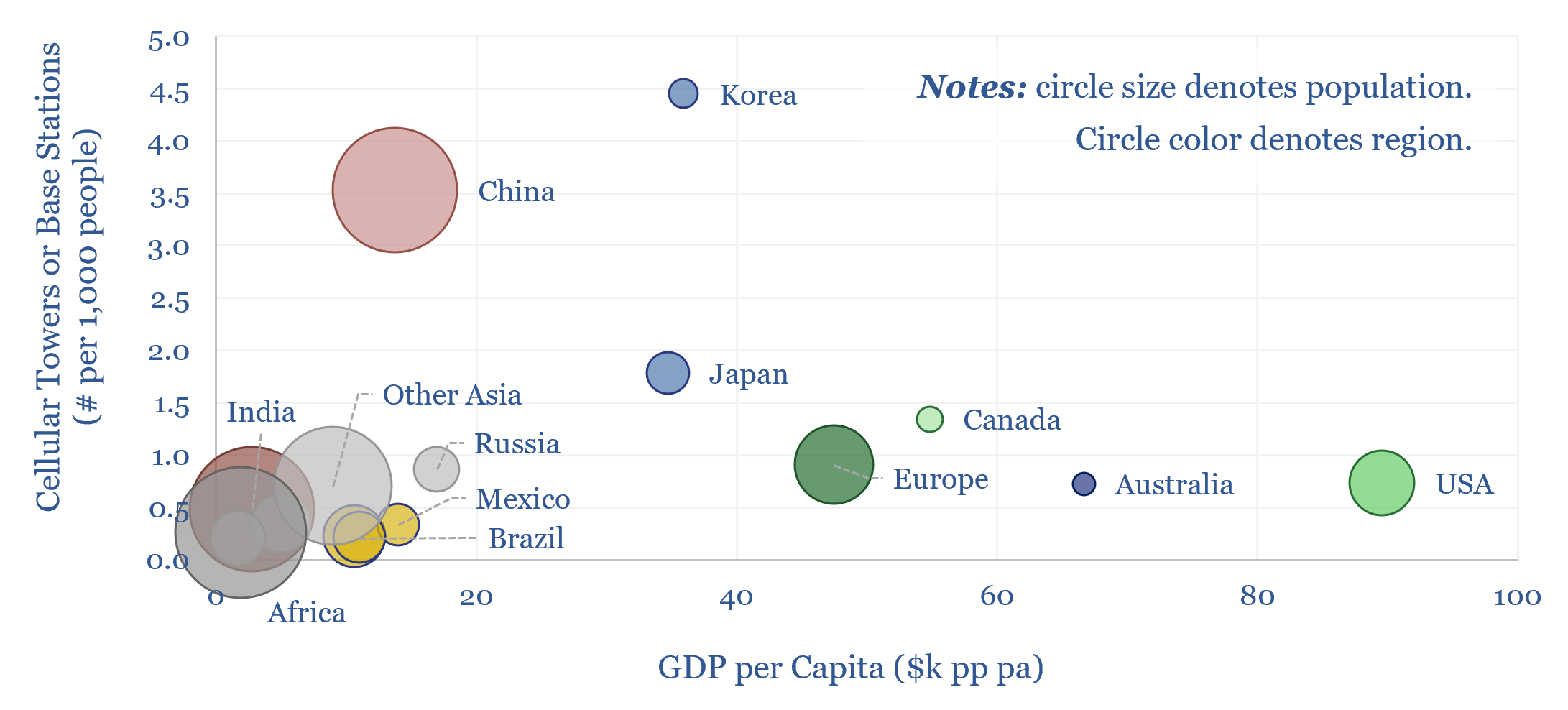

Cellular networks: how much energy consumption?

The energy consumption of global cellular networks is estimated at 250TWH pa in this data-file, by tabulating the deployment of 5G base stations, and other cellular towers, region-by-region. This matters as physical AI may require more cellular connections, across autonomous vehicles, drones and robotics.

-

Delivery drones: flight trajectory?

Delivery drones are finally taking off? Pilot projects in the US are achieving strong safety records, exciting consumers and raising the prospect of sub-$1 deliveries within 10-minutes. This 13-page report explores the future impacts of delivery drones in energy, materials and capital goods.

-

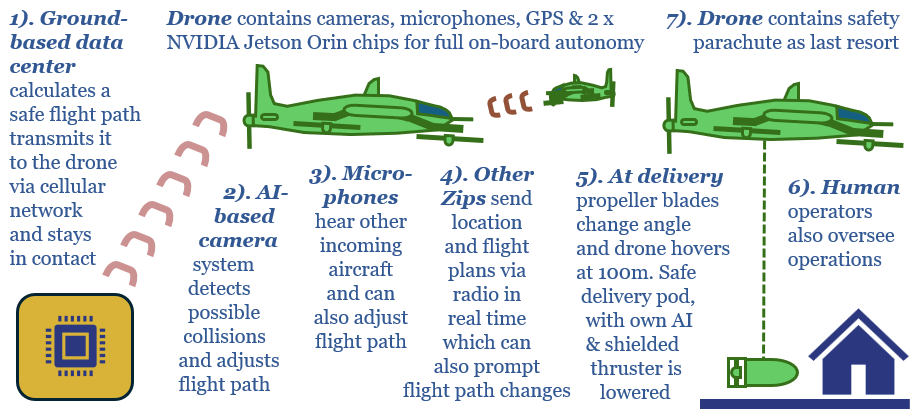

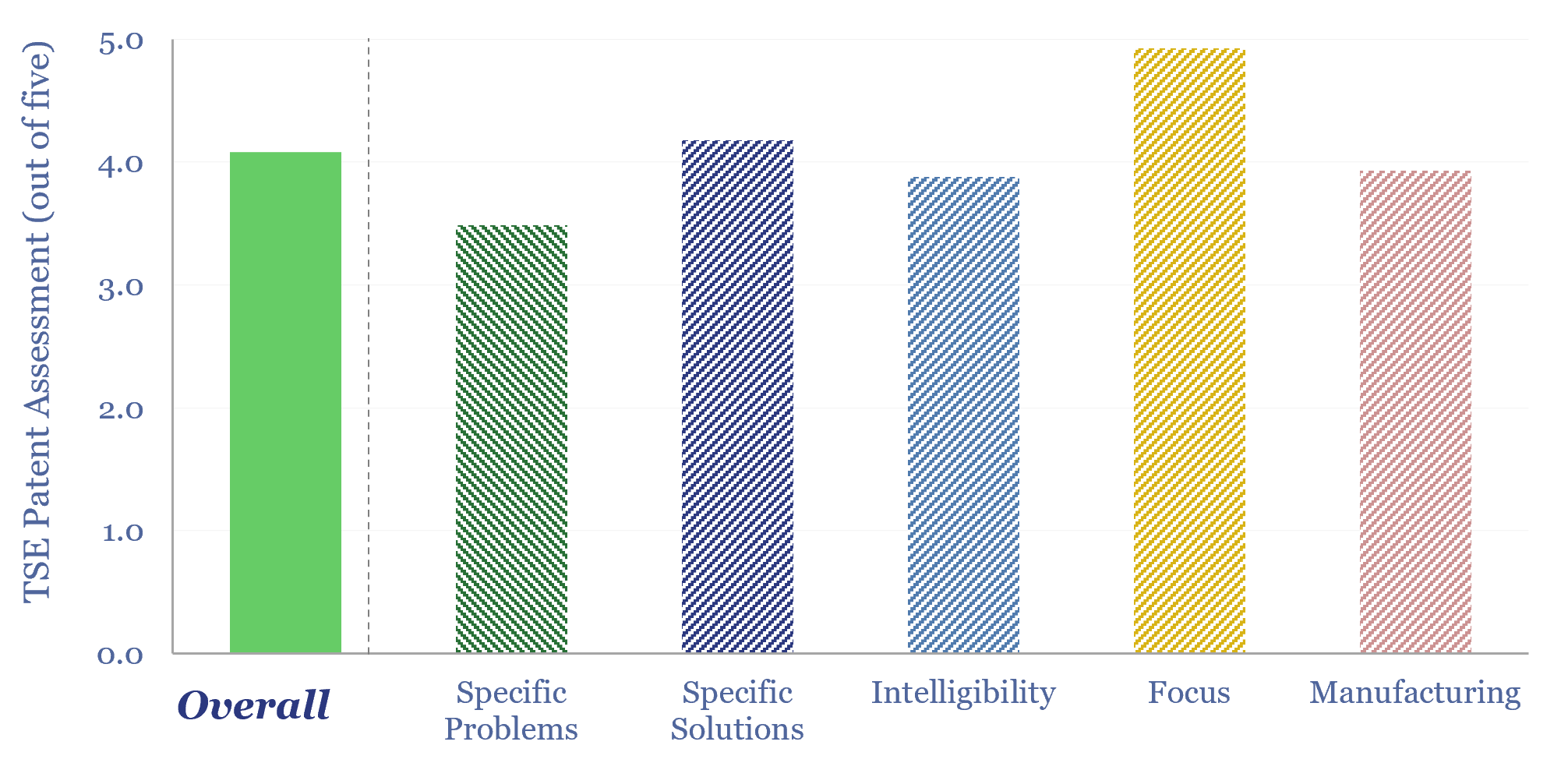

Zipline: drone delivery technology?

Details of Zipline drone delivery technology are derived in this data-file, based on reviewing over 15 highly detailed patent families from the company. We see a moat around specific hardware innovations, a low cost sensor suite, inherent safety from seven layers of safety protections, and a sophisticated fleet management system.

-

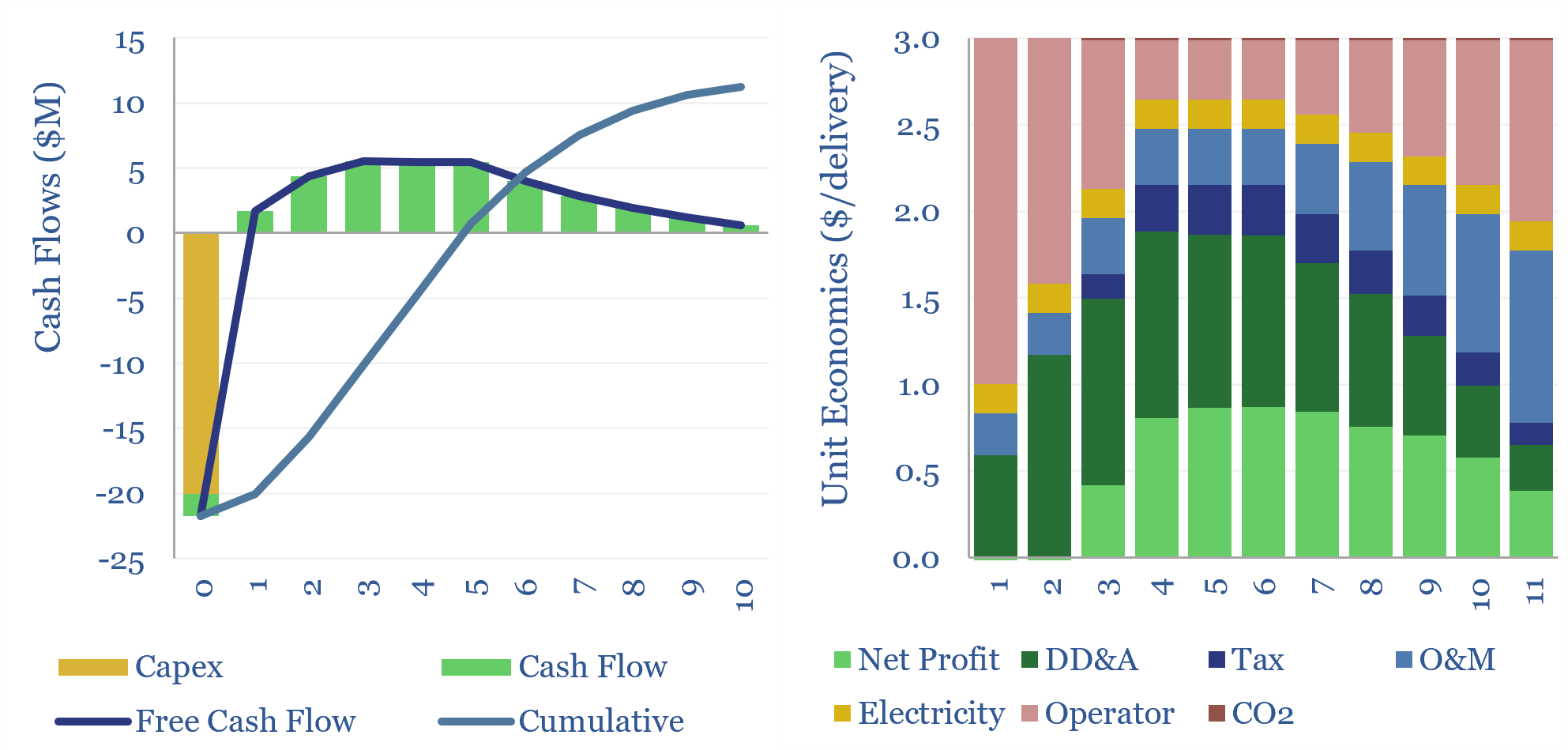

Costs of delivery drones: the energy economics?

The energy economics of delivery drones, which can travel autonomously, over 30km at 100kmph, are captured in this data-file. In our base case, a delivery drone that costs $20k, and makes 8 deliveries per day, must charge a fee of $3/delivery to generate a 10% IRR. Costs, speeds and energy use can be 5-20x superior…

-

Heat potential: what if AI can load-shift hot water tanks?

Residential heat is 13% of global energy. So what if AI could optimize residential electric heating? This 16-page report finds that load-shifting hot water tanks can unlock 1.5-8.5% additional flexibility in grids and make air source heat pumps the lowest cost option for heat in Europe, eclipsing gas-combi boilers, saving $300 per household per year?

-

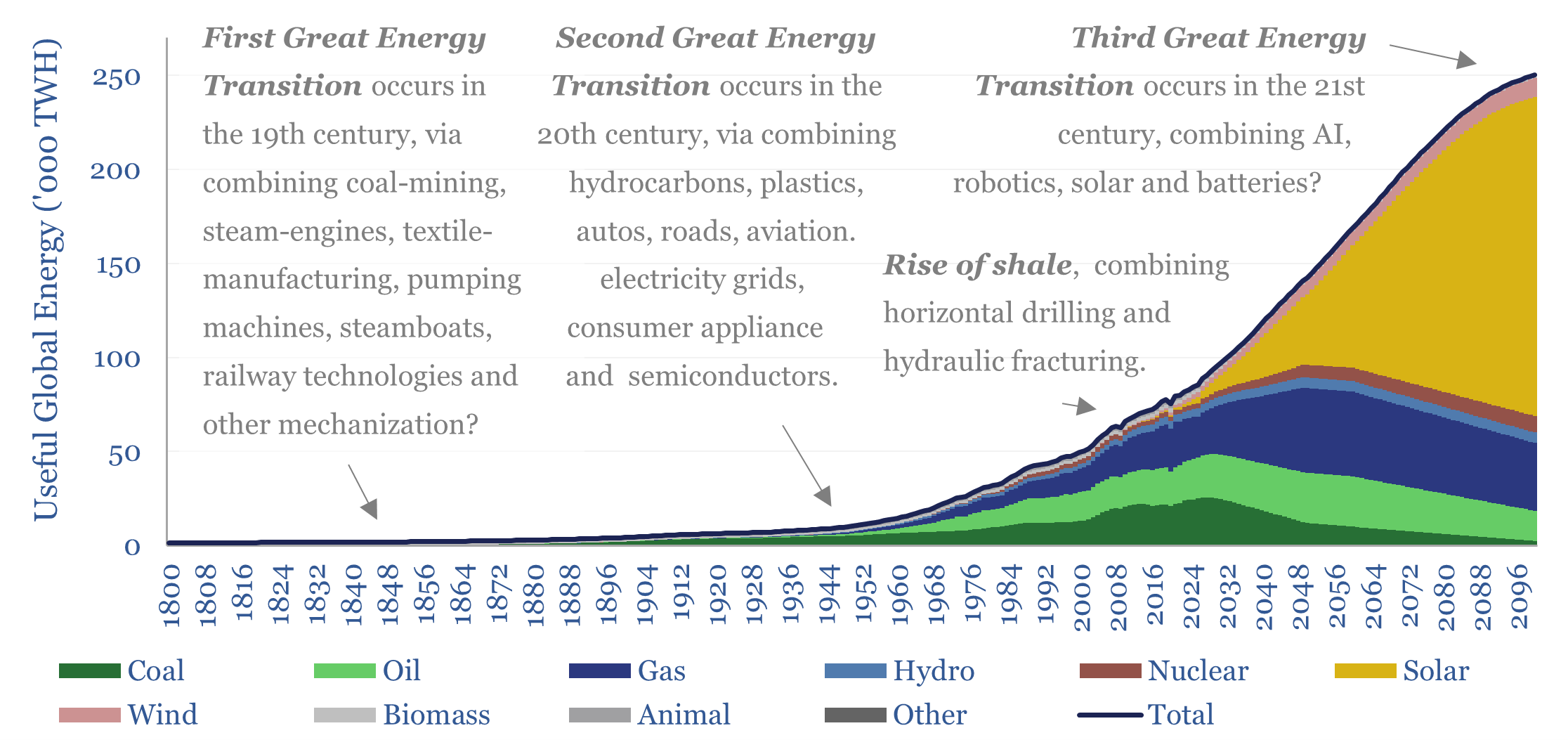

The AI energy transition: technologies collide?

Great industrial leaps often occur when technologies collide. Hence this 20-page report explores how AI, solar, batteries and robotics might all collide together. This is transformative for the world. It represents the next “energy transition”. Hence this also becomes our new roadmap for the evolution of the global energy system.

-

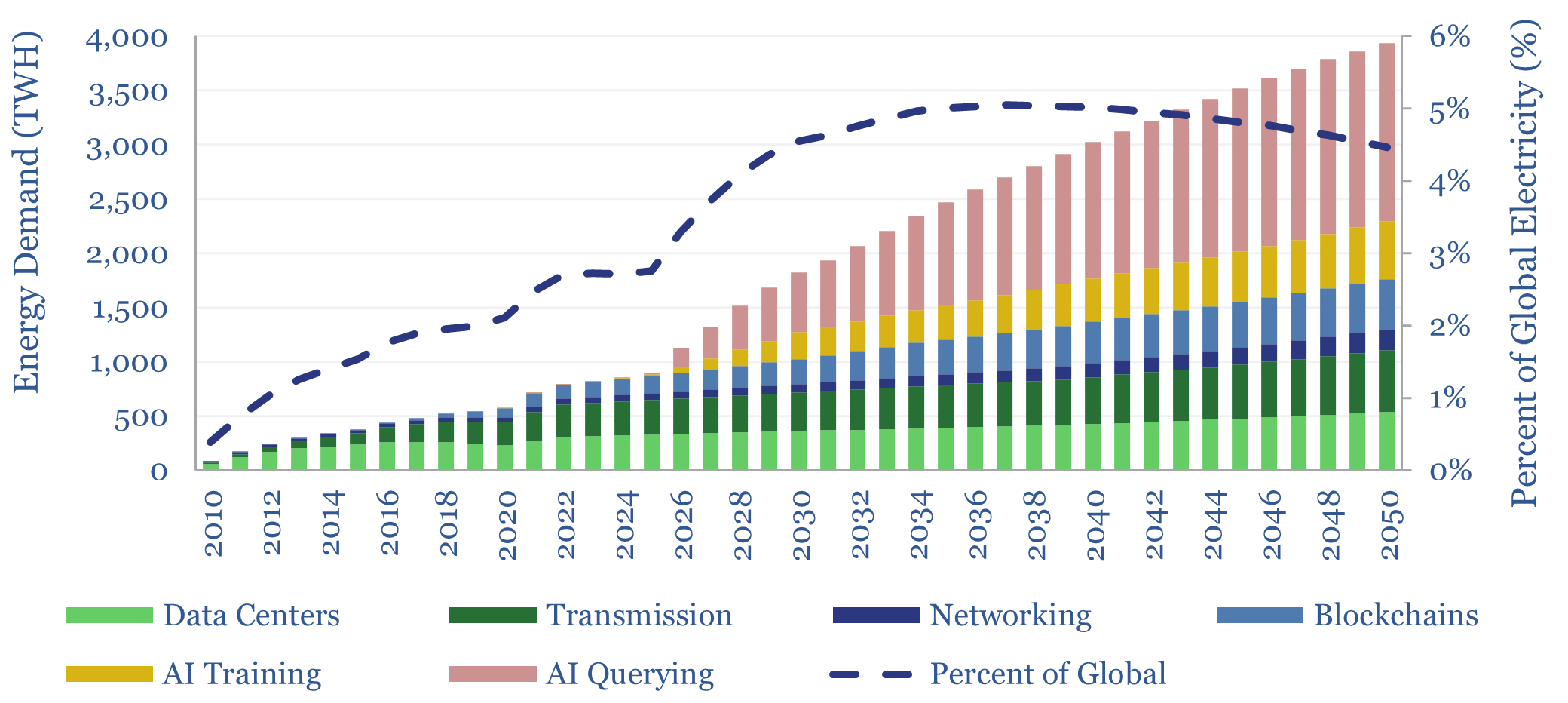

Internet energy consumption: data, models, forecasts?

This data-file forecasts the energy consumption of the internet, rising from 800 TWH in 2022 to 2,000 TWH in 2030 and over 4,000 TWH by 2050. The main driver is the energy consumption of AI, plus blockchains, rising traffic, and offset by rising efficiency. Input assumptions to the model can be flexed. Underlying data are…

Content by Category

- Batteries (96)

- Biofuels (44)

- Carbon Intensity (48)

- CCS (64)

- CO2 Removals (9)

- Coal (44)

- Commentary (65)

- Company Diligence (105)

- Data Models (928)

- Decarbonization (163)

- Demand (131)

- Digital (92)

- Downstream (47)

- Economic Model (222)

- Energy Efficiency (76)

- Hydrogen (63)

- Industry Data (311)

- LNG (56)

- Materials (86)

- Metals (89)

- Midstream (45)

- Natural Gas (163)

- Nature (76)

- Nuclear (28)

- Oil (178)

- Patents (39)

- Plastics (44)

- Power Grids (156)

- Renewables (153)

- Screen (139)

- Semiconductors (36)

- Shale (58)

- Solar (72)

- Supply-Demand (53)

- Vehicles (94)

- Video (24)

- Wind (46)

- Written Research (410)