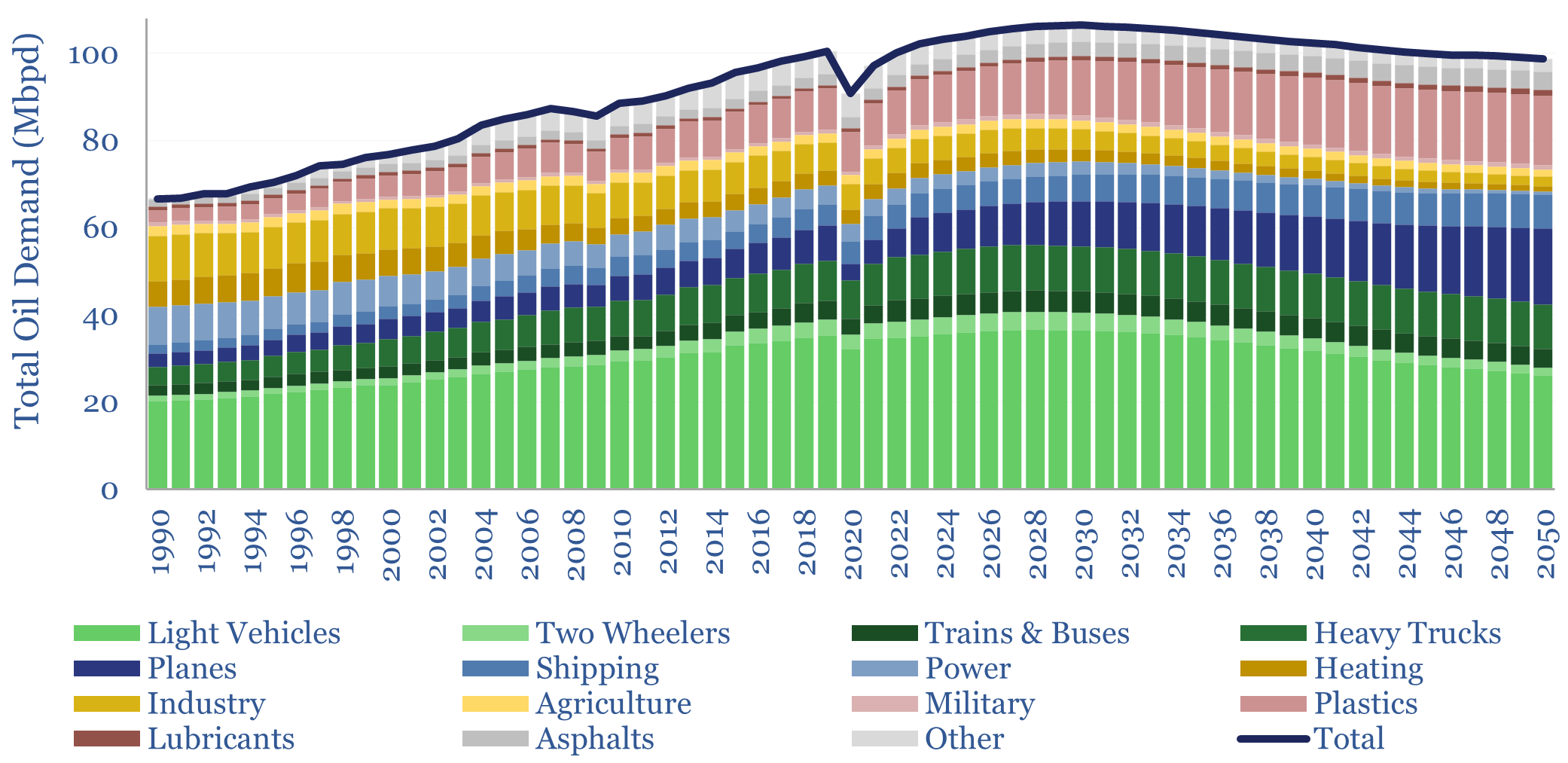

This model forecasts long-run global oil demand to 2050, by end use, by year, and by region; across the US, the OECD and the non-OECD. We see demand rising from 104Mbpd in 2025 to a plateau of 107Mbpd in 2030, then easing back to 100Mbpd by 2050.

The model forecasts long-term global oil demand, based off of 25 input variables, such as GDP sensitivity, electric vehicles, energy efficiency initiatives, vehicle miles traveled, and substitution effects. You can flex these input assumptions, to assess long-term global oil demand through 2050.

Our own scenario foresees oil demand increasing from c100Mbpd in 2022 to a plateau of 107Mbpd in 2030, then declining mildly to 100Mbpd in 2050. This is most likely associated with 2-3C of warming in our latest roadmap to net zero, but the job of this data-file is forecasting not fantasy.

The biggest shift for global oil demand is the disruption of c40Mbpd of oil demand for light vehicles, which is based on all of our vehicle research, the ramp-up of electric vehicles (linking to our vehicle database below), plus continued displacement of oil in power and industry.

It is harder to envisage large-scale disruptions in other categories of global oil demand, such as long-distance trucks, planes, plastics and shipping.

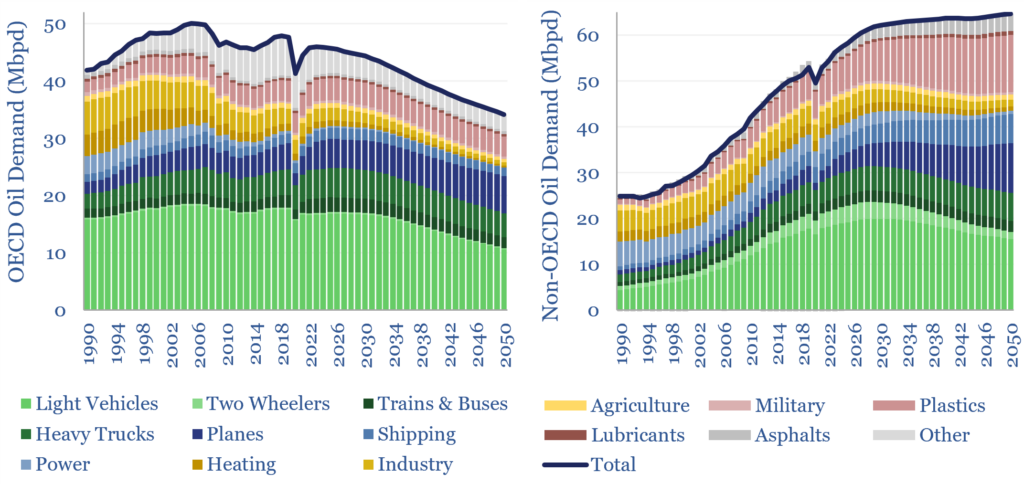

How will long-term oil demand vary by region? Another notable trend in the model is that it embeds different trajectories for oil demand in the developed versus the emerging worlds (charts below).

OECD oil demand has already peaked, at 50Mbpd in 2005, and is seen falling -1.2% pa to 30Mbpd by 2050. In particular, planes and long-distance transport are hard to substitute due to limits on the energy density of lithium ion batteries and myriad issues with hydrogen-based fuels.

Non-OECD oil demand has risen from 35Mbpd in 2005 to 52Mbpd in 2019 and is seen rising to 65Mbpd by 2050. This is assuming 50-60% of EM vehicle sales are electricity in 2040-50.

How will long-term oil demand vary by product? The balance of oil product demand through 2050 is also changing in our model (chart below). Gasoline demand declines from 30% of the total oil market to 20%. Jet fuel rises from 8% to 20%. Materials rise from 13% to 22%. And a few pp of share continues shifting from fuel oil (<10%) to diesel (>30%). To calibrate our model, we also track global oil demand by product by region over time.

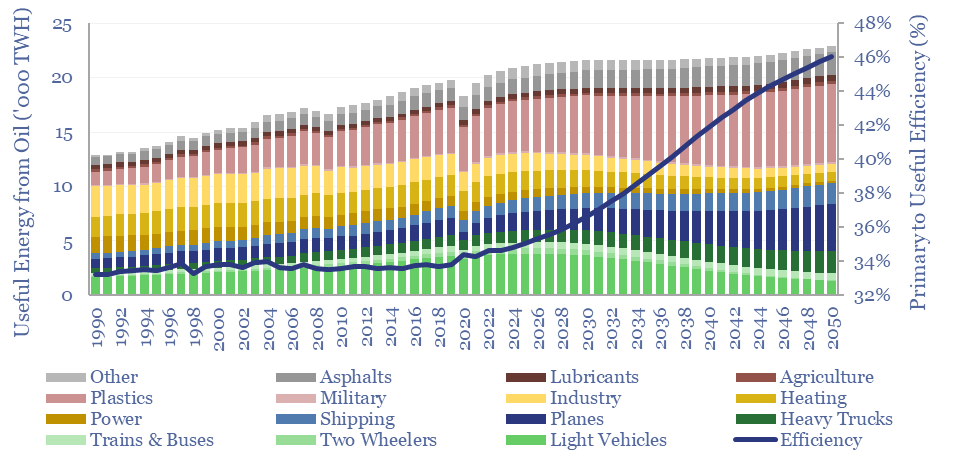

How will the primary-to-useful efficiency of global oil consumption change? A typical gallon of oil products contains 38kWh-th of primary energy. As a blended average, the combustion of oil products in 2023 is 35% efficient in converting primary to useful energy, albeit with sharp variations by category. Primary to useful efficiency of oil rises from 35% to 46% by 2050, of which two-thirds is due to mix-shifts in the oil market, and one-third is underlying efficiency gains of prime movers.

The model has been updated in December-2025. Underlying workings are shown in seven subsequent tabs, covering light vehicles, trucks, jet fuel, plastics, shipping, other products and demographics.

For more granular, month-by-month data, tabulating oil demand by region, we also have a tracker file based on JODI data, which is linked here. Please download the data-file to stress test your own long-run oil demand forecasts, and evaluate oil demand by category, oil demand by region and oil demand by end use.