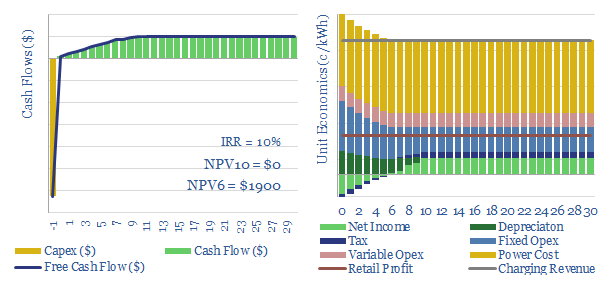

An electric vehicle charging station typically needs to charge 20-25 c/kWh, to earn a 10% return on its up-front capex costs, as it buys power for 10c/kWh and sells it on to electric vehicles with 10-50% utilization rates. Larger, fast-chargers seem most economic. Especially where retail revenues support the economics of EV-charging.

This data captures the economics of EV charging, at Level II chargers, Level III AC chargers, and DC fast-chargers, that can reach up to 150-350kW power ratings. A good rule of thumb is that the charger needs to add a spread of 6-15c/kWh.

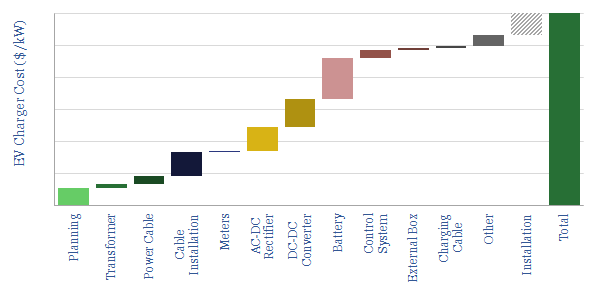

First, we disaggregate the capex costs of EV chargers, across materials, electronic components, labor, permitting, fees, opex and maintenance (below). Next, we model what fees need to be charged by the charging stations (in c/kWh) in order to earn 10% IRRs.

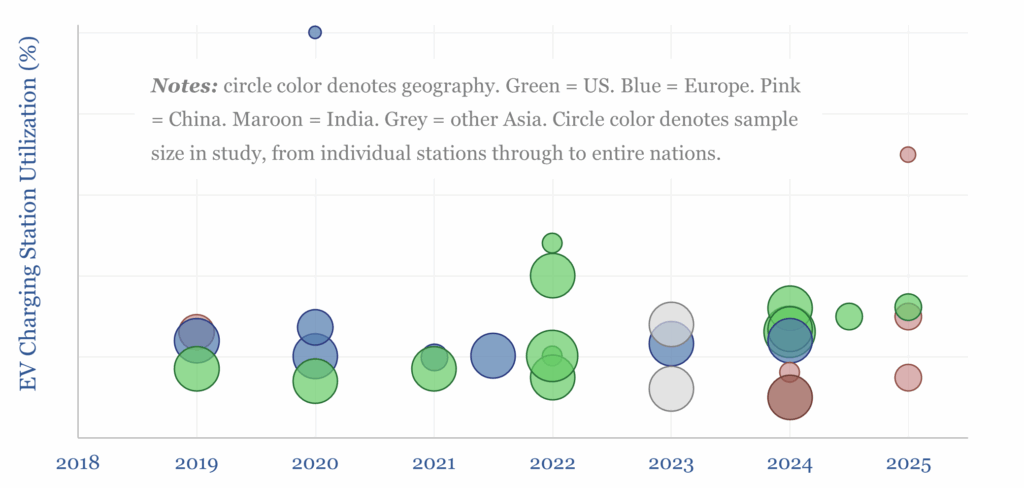

Utilization rates of EV chargers dictate how many MWH of electricity each charge-point will sell each year, in order to recoup its capex costs and generate a return. To inform our estimates, we have aggregated 30 data-points from companies and past technical papers, with an average of 13% utilization.

There has long been a hope that rapidly accelerating EV sales will improve utilization rates, but this has not entirely materialized. Indeed, in some cases, it has looked as though the EV charging network is prone to being overbuilt.

Economics of EV charging are most favorable where they can lead to incremental retail purchases and for larger, faster chargers. Economics are least favorable around multi-family apartments, charging at work and for slower charging speeds.

An economic increment can also be added to reflect the benefits of demand shifting to backstop increasingly renewable-heavy grids.

What will be a game-changer for the economics of EV charging, in our view, is the emergence of autonomous vehicles, which can route themselves to unoccupied charging infrastructure, especially to benefit from excess solar. Solar+EVs can be more economical than ICEs.