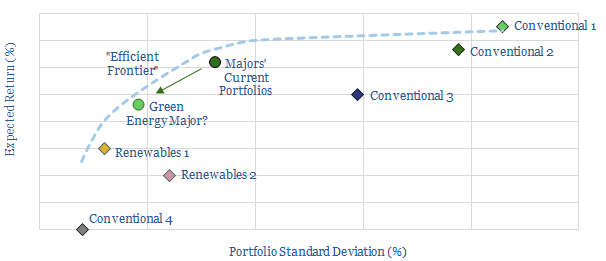

This data-model calculates risk-adjusted returns available for different portfolio weightings in the energy sector, as companies diversify across upstream, downstream, chemicals, corporate, renewables and CCS investments. The methodology is a mean-variance optimisation based on modern portfolio theory.

Should Oil Majors become Renewable Energy Majors? Our model indicates returns would decrease by allocating more capital to renewables, but certain renewable allocations can nevertheless increase risk-adjusted returns, as quantified using Sharpe Ratios.

Please download the model to test the impacts of flexing portfolio weightings; either at our own risks, returns and diversification benefits; or under your own assumptions which can be tweaked in the model.