This data-file is a screen of leading reciprocating gas engine companies, covering an industry with 15GW pa of manufacturing capacity, EBIT margins averaging 10-20% (and rising), and an overlap with efficient engines used in diesel generators, marine, construction, mining and agricultural industries. Several companies stood out.

Reciprocating gas engines have stood out in our research into different gas generation solutions, especially for powering AI data-centers, because they can be rapidly deployed, and paralleled to achieve very high reliability. This has underpinned a surge in orders for companies such as Voltagrid and others in mobile micro-grids. We have also modeled the economics of recips.

Hence in this data-file, we wanted to screen reciprocating gas engine companies: i.e., the underlying equipment manufacturers, their capacities, margins, expansion plans, and key locations where reciprocating gas engines are produced.

Difficulty level = fiendish. Companies that make reciprocating gas engines also tend to make diesel engines and other heavy-duty engines for the marine, construction, mining and agricultural industries, while some also make engines for heavy-duty trucks. The companies mostly do not split out sales or capacities for gas engines alone. We gathered what we could from company disclosures in the data-file.

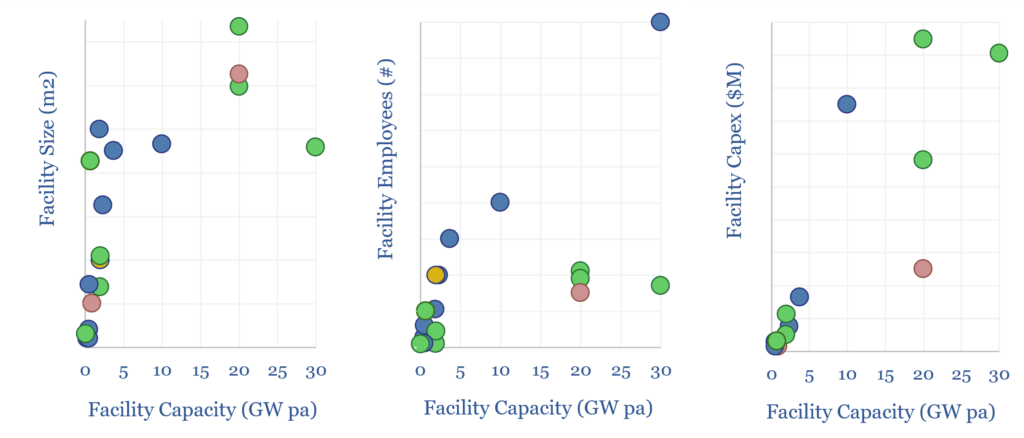

However our approach in the data-file has been to profile the underlying manufacturing facilities. Often, reciprocating gas engines are manufactured in just a handful of key locations. Hence we aggregated the size of these facilities (in m2 or sq ft), their employee counts, and the capex that has likely gone into each facility. For some facilities, we have a good idea of the production run-rate — e.g., Wärtsilä handily gives a periodic update on the total GW of engines it has sold into the power sector, and almost all of these engines are made in Vaasa, Finland. For other facilities, we can interpolate to what the production capacity might be, based on our scatter plots (see below).

The total production capacity for reciprocating gas engines sold into the power sector today is estimated to be c15GW, with another 1GW under construction.

The top ten reciprocating gas engine companies account for 75-80% of total global production, with larger companies in the space producing 1-3 GW pa of recips. However, the median company in the screen derives just 4% of its revenues from recips, due to heavy diversification across other engine types, serving other industrial segments.

Three companies derive over 20% of their revenue and EBIT from reciprocating gas engines, of which two are listed.

Please download our screen of reciprocating gas engine companies for our notes and observations into each company and capacity estimates by company and by manufacturing facility.