The downstream industry is currently debating whether IMO 2020 sulphur regulations will be resolved quickly or slowly. We think the market-distortions may be prolonged by under-appreciated technology challenges.

[restrict]

As context, from 2020, it will no longer be permitted to burn fuels with 3.5% sulphur in the marine segment. Their maximum permitted sulphur content will fall to 0.5%. In principle, refining cracks will move, advantageously for low-sulphur diesel and disadvantageously for high-sulphur fuel oil.

Over time, this should provide an economic incentive to construct incremental hydro-processing and hydro-conversion technologies. However, it still may not be so simple as to construct a few extra hydro-processing units. Not all sulphur is equal.

Hard Sulphur and Easy Sulphur

On the one hand, aliphatic sulphur compounds are easily treated. The process uses a hydrogen partial pressure of 10-30kg/cm2, 180-370C temperatures, and liquid:catalyst ratio up to 4:1. The catalyst contains Cobalt, Nickel and/or Molybdenum on an aluminium oxide framework. This is industry-standard technology, available to all.

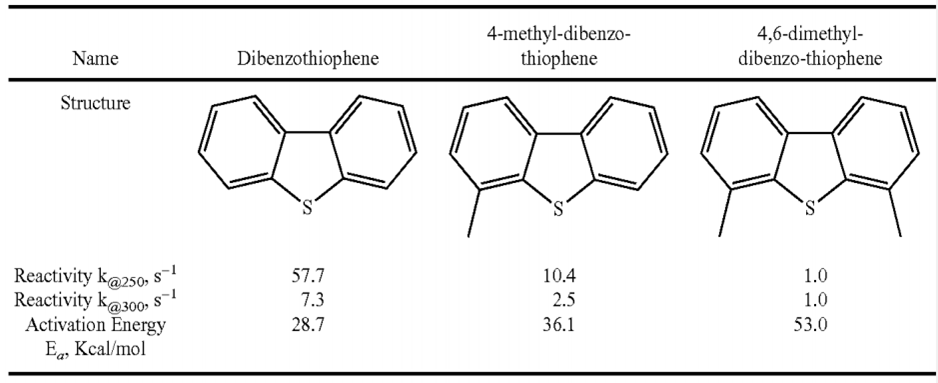

However, highly branched molecules are harder. One class, dibenzothiophenes, is pictured below. Their structure impedes the sulphur “heteroatom” from reaching the active site on the catalyst. Run it through a low-spec hydrotreater, and it comes out the other side… unchanged.

Another challenge with aromatic sulphur-containing compounds is their under-saturation. Traditional hydroprocessing techniques, aimed primarily at reducing sulphur, also tend to saturate these aromatic rings which “can increase the amount of hydrogen consumed during hydroprocessing by as much as an order of magnitude”. This is problematic at refineries with limited hydrogen. It adds cost.

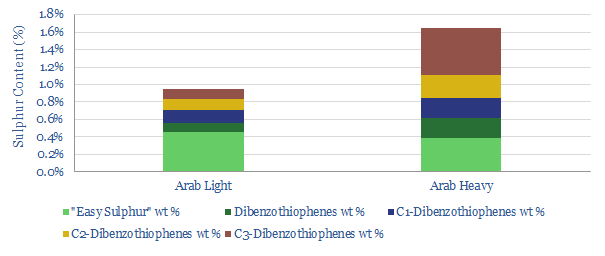

It may be under-appreciated how much of the sulphur in the world’s fuel market is “difficult sulphur”, rather than “easy sulphur”. For example, if we take Saudi Arabia’s production, comprising the most abundant crude oil streams on the planet, the more challenging sulphurs comprise 0.5% of Arab Light, and 1.3% of Arab Heavy.

As Aramco’s patents note “it is very difficult to upgrade existing hydrotreating reactors” and “the economical removal of refractory sulfur-containing compounds is exceedingly difficult to achieve”. Especially if the end target is to reach higher European and US standards of 0.1% sulphur caps.

Resolving the Impasse: Large Investments?

There are solutions to this challenge. Indeed, Aramco has filed patents for methods of removing these more challenging sulphurs. One is to build a new separation unit, distill the crude into two separate streams, isomerise the ‘hard sulphur’ stream, re-combine it with the ‘easy sulphur’ stream, then hydro-treat the mixture. Hydrocracking these compounds is another option, breaking them down into lighter, smaller, “easier sulphur” molecules.

Both of these options require large investment, with multiple processing units and ancillary units. It follows that the ultimate refinery projects used to re-balance the market post-IMO 2020 are not simple hydoprocessing projects.

Against this backdrop, fears over the energy transition make it increasingly difficult to justify large, long-term investments. Particularly in Europe.

[/restrict]

Opportunities amidst the Challenge?

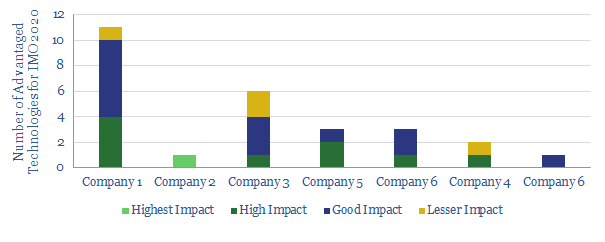

So if the market-distortions of IMO 2020 have longevity, who will stand to benefit? We are maintaining a data-file of the ‘Top Technologies for IMO 2020’ around the industry, which give specific companies an edge. The data file now contains over 25 technologies across 7 Majors.

References

Al-Shahrani, F., Koseoglu, O. R. & Bourane, A. (2018). Integrated System and Process for In-Situ Organic Peroxide Production and Oxidative HeteroAtom Conversion. Saudi Aramco Patent.

Koseoglu, O. R., (2018). Integrated Isomerisation and Hydrotreating Process. Saudi Aramco Patent CN107529542

Hanks, P. (2018). Trim Alkali Metal Desulfurisation of Refinery Fractiions. ExxonMobil Patent US2018171238