Leading gas turbine component manufacturers are tabulated in this company screen. 20 companies produce almost $5bn pa of precision-made blades, vanes, rings and ancillaries for gas turbines, at 17% EBIT margins, but a diversified manufacturing footprint that often overlaps with other aerospace applications. What implications?

A large industrial gas turbine will comprise over 100,000 specialty components, as disaggregated in our gas turbine breakdown data-file. Many need to be forged or investment cast, then CNC-machined, and extensively tested, before being shipped out. Hence who are the companies that make these components?

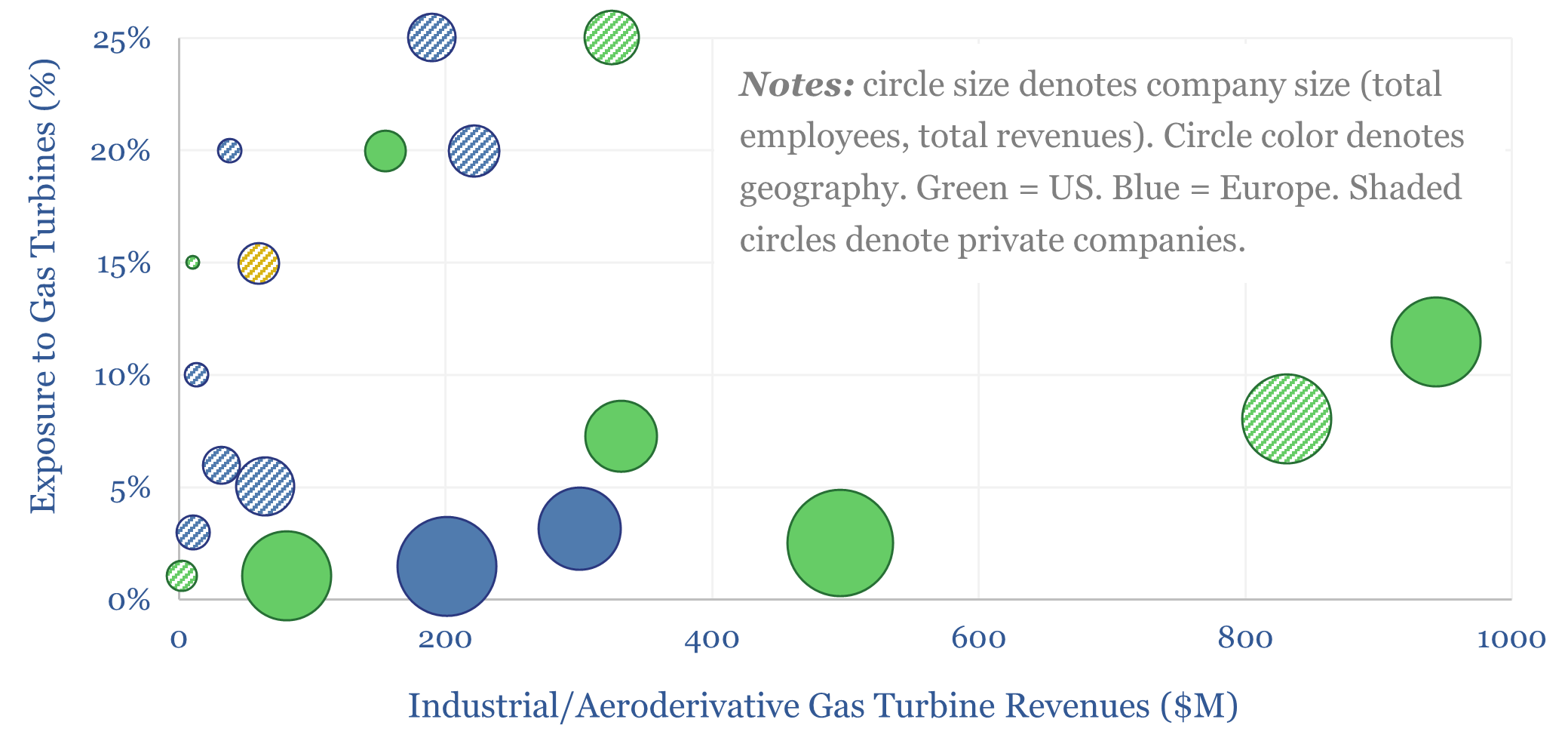

This data-file is a screen of 20 leading gas turbine component manufacturers, which likely sell c$4.5bn of components into the c$30bn pa gas turbine industry. This matters as our recent work into gas turbine manufacturing capacity concludes that it is often the specialty components that are particularly bottlenecked, rather than the headline gas turbine assembly capacity.

Note that we are specifically talking about the component manufacturers here, of which the largest example would be Howmet. This is distinct from the large gas turbine manufacturers, such as GE Vernova and Siemens Energy, which will both make their own underlying components and source from the third-parties in this data-file.

Strong demand for gas turbines is noted in the data-file and the average EBIT margin among these, where available, has risen to 17% in 2025. In addition, the more specialized and high-grade the components, the higher the margin.

In the face of strong demand, many companies are also expanding the capacity to make gas turbine components. For example, in June-2025, Howmet announced it would hire 217 employees as part of an expansion in Tennessee, and in December-2025, it acquired Consolidated Aerospace Manufacturing.

The average company in our screen is surprisingly diversified, however, and only 5% exposed to gas turbine components overall. The most common adjacent industry to be served is aerospace. Indeed, if we look at turbomachinery more broadly, we estimate that the total market is $95bn, of which aerospace is $60bn and industrial power generation is $35bn pa.

Hence it is fascinating to consider whether tightness in gas turbine supply chains could infect the aerospace supply chains, delaying or inflating the costs of delivering new aircraft engines, or even entire aircrafts.

Details on each of the gas turbine component manufacturers are covered in the data-file: year founded, geography, company type, employee count, patent filings, revenues ($M), EBIT ($M), EBIT margins (%), estimated exposure to gas turbines (in % of revenues, and in $M), and detailed underlying notes.