-

Energy costs of lithium ion batteries?

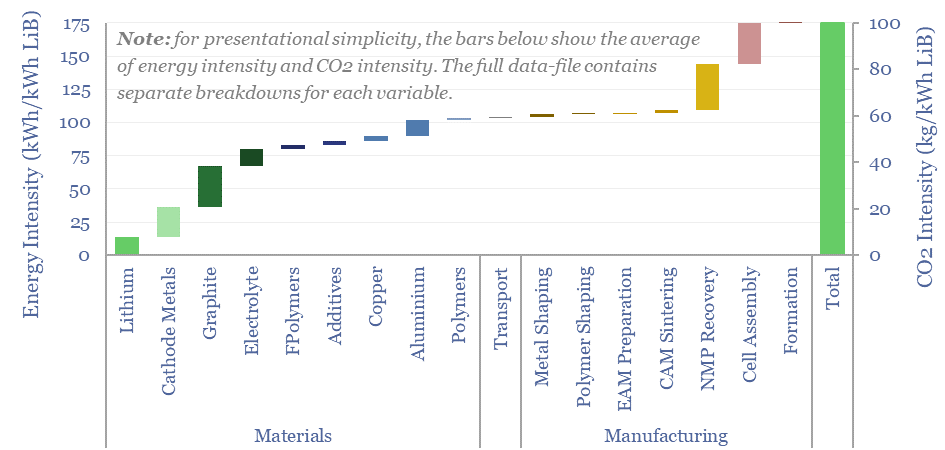

This data-file estimates the energy costs of lithium ion batteries across 17 lines. Our best estimate in 2024 is that manufacturing 1 kWh of lithium ion batteries requires 175 kWh of useful energy and emits 100kg of CO2. When a lithium ion battery is used in an electric vehicle, these up-front energy and CO2 costs…

-

Smart Energy: technology leaders?

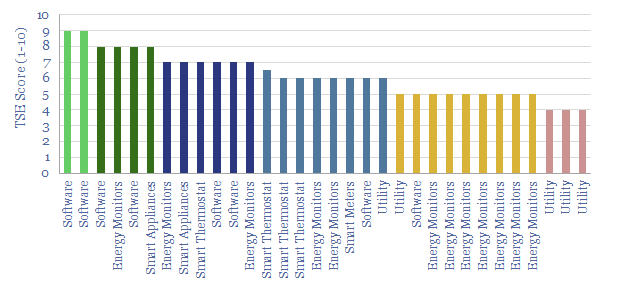

Smart meters and smart devices are capable of transmitting and receiving real-time consumption data and instructions. This data-file tracks 40 leading companies, mostly at the venture and growth stages. They help lower demand, smooth grid volatility and encourage appliance upgrades.

-

Lithium ion batteries for electric vehicles: what challenges?

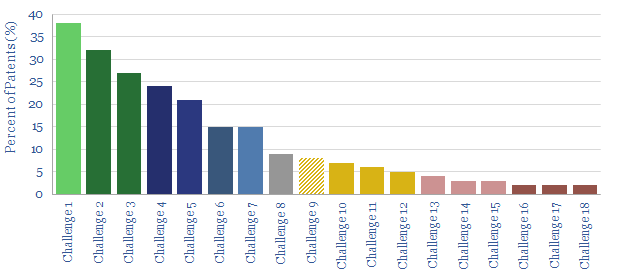

This data-file tabulates the greatest challenges for lithium ion batteries in electric vehicles, which have been cited in 2020’s patent literature. Conclusions are spelled out in detail, covering energy density, “million mile” longevity and electric semi-trucks. Companies profiled include Tesla, CATL, LG, Sumitomo, et al.

-

Oxycombustion: economics of zero-carbon gas?

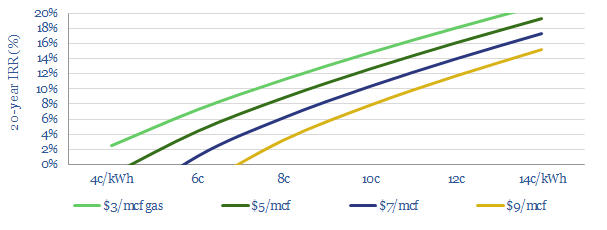

Oxy-combustion is a next-generation power technology, burning fossil fuels in an inert atmosphere of CO2 and oxygen. It is easy to sequester CO2 from its exhaust gases, helping heat and power to decarbonise. We argue that IRRs can be competitive with conventional gas-fired power plants.

-

Ten Themes for Energy in the 2020s

This short presentation describes our ‘Top Ten Themes for Energy in the 2020s’. Each theme is covered in a single slide. For an overview of the ideas in the presentation, please see our recent presentation, linked here.

-

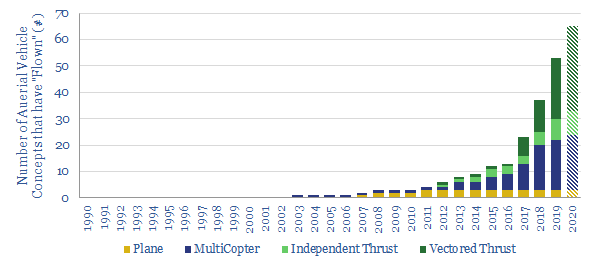

Aerial Vehicles: Which Ones Fly?

We have updated our database of over 100 companies, which have already flown c50 aerial vehicles (aka “flying cars”), to identify the leading contenders. We categorize each vehicle by fuel type, speed, range, fuel economy and credibility. The data strongly imply aerial vehicles taking off in the 2020s.

-

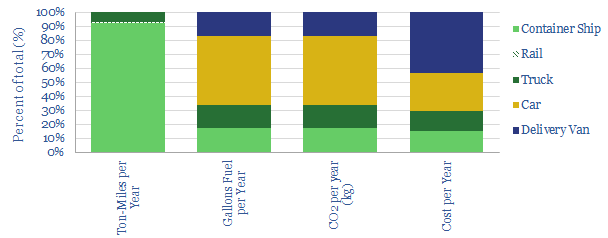

Distribution Costs: Ships, Trucks, Trains and Delivery Vans?

Distributing goods to the typical US consumer costs 1.5bbls of fuel, 600kg of CO2 and $1,000 per annum. The costs will increase 20-40% in the next decade, as the share of online retail doubles to c20%, hence new technologies are needed in last-mile delivery. This data-file provides a full breakdown of the numbers, across container-ships,…

-

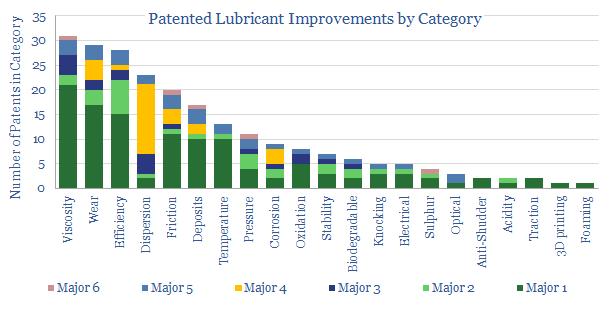

Lubricant Leaders: our top five conclusions

We present our “top five” conclusions on the lubricants industry, after reviewing 240 patents, filed by Oil Majors in 2018. We are most impressed by the intense pace of activity to improve engine efficiencies. Technology will drive margins and market shares, hence three clear market leaders are identified. The relative number of patents into Electric…

-

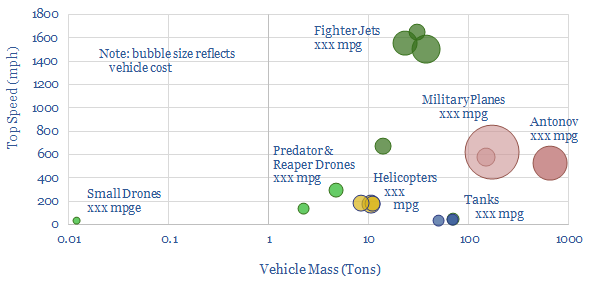

Drones attack military fuel economy?

Swarms of drones are emerging as the most devastating military weapon of the 21st century. This was evidenced by the recent attack on Saudi oil infrastructure. But drones’ impact on 0.7Mbpd of global military oil demand could be even more devastating. This data-file quantifies their fuel economy at >1,000 mpge compared to today’s fighter jets,…

-

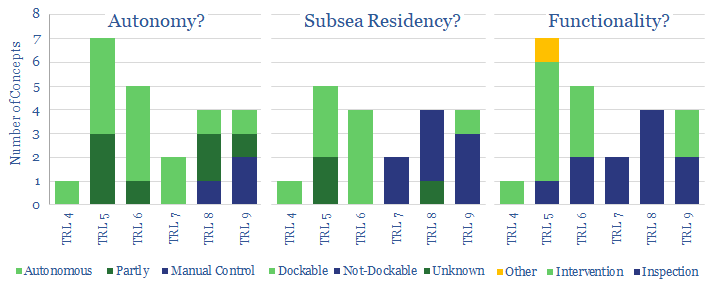

Subsea Robots: the next generation?

Over 20 next-generation subsea robotics concepts are presented. These electric solutions are increasingly autonomous, they reside subsea and can conduct more thorough inspection/intervention work. Inspection is 2-6x faster, and maintenance costs can be halved, yielding savings of $0.5-1/boe at a typical field. The data-file also summarizes the leading Majors and Service Companies in the space.

Content by Category

- Batteries (89)

- Biofuels (44)

- Carbon Intensity (49)

- CCS (63)

- CO2 Removals (9)

- Coal (38)

- Company Diligence (94)

- Data Models (838)

- Decarbonization (160)

- Demand (110)

- Digital (59)

- Downstream (44)

- Economic Model (204)

- Energy Efficiency (75)

- Hydrogen (63)

- Industry Data (279)

- LNG (48)

- Materials (82)

- Metals (80)

- Midstream (43)

- Natural Gas (148)

- Nature (76)

- Nuclear (23)

- Oil (164)

- Patents (38)

- Plastics (44)

- Power Grids (130)

- Renewables (149)

- Screen (117)

- Semiconductors (32)

- Shale (51)

- Solar (68)

- Supply-Demand (45)

- Vehicles (90)

- Wind (44)

- Written Research (354)