-

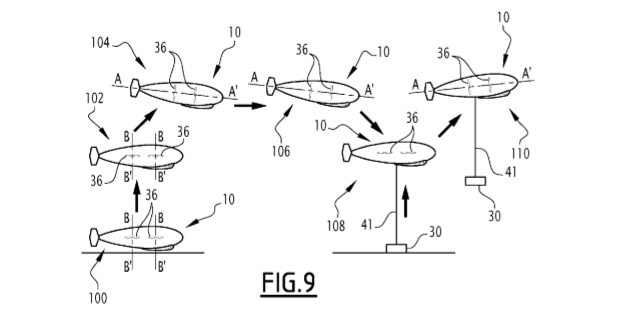

Could new airships displace trucks?

In 2019, TOTAL co-filed two patents with an airship-technology company, Flying Whales, aiming to lower the logistical costs of moving equipment into remote areas. Strong applications are seen in the wind industry. This short note assesses the opportunity, and whether these new airships could displace trucks, or lower diesel demand.

-

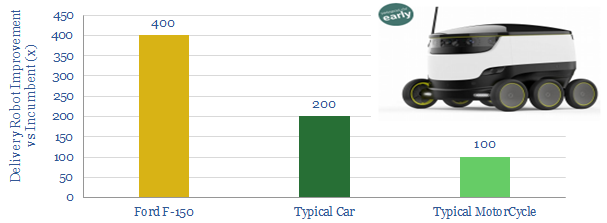

Robot delivery: Unbelievable fuel economy…

Small delivery robots can achieve 100-400x higher fuel economies than conventional, oil-powered vehicles. We profile Starship, whose fleet is now covering c400km/day. Energy demand in transportation is evolving.

-

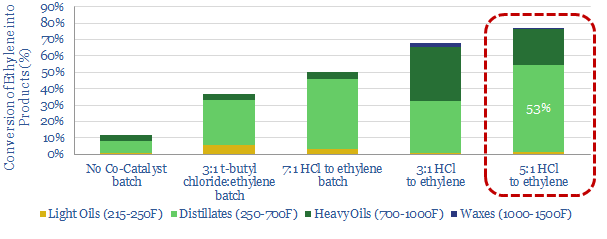

Shale: restoring downstream balance? New opportunities in ethylene and diesel.

Shale’s light mix is often criticised for distorting oil product markets. But distortions create opportunities for Integrateds. This note explores one opportunity, patented by Chevron, to convert ethylene into diesel.

-

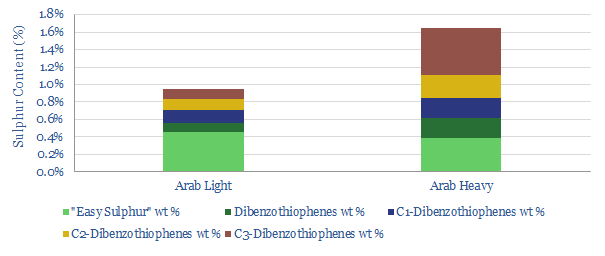

IMO 2020. Fast Resolution or Slow Resolution?

The downstream industry is debating whether IMO 2020 sulphur regulations will be resolved quickly or slowly. We think the market-distortions may be prolonged by under-appreciated technology challenges, which mandate large, increasingly hard-to-finance refinery overhauls.

-

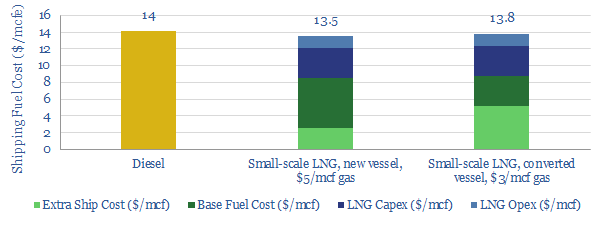

LNG in transport: scaling up by scaling down?

Next-generation technology in small-scale LNG has potential to reshape the global shipping-fuels industry. Especially after IMO 2020 sulphur regulations, LNG should compete with diesel. Opportunities in trucking and shale are less clear-cut.

-

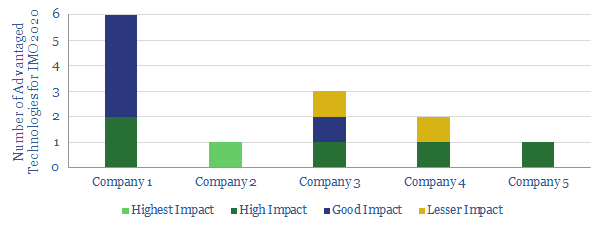

Our Top Technologies for IMO 2020

We review a dozen of the top, proprietary technologies that we have seen to capitalise on IMO 2020 sulfur regulation, across five of the world’s leading refiners.

-

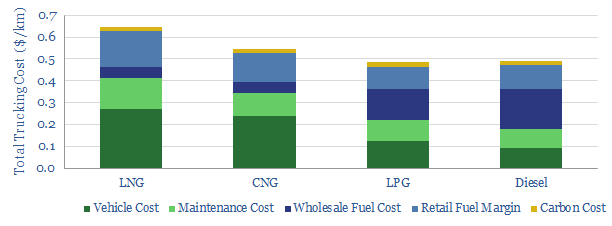

Is gas a competitive truck-fuel?

We have assessed whether gas is a competitive trucking fuel, comparing LNG and CNG head-to-head against diesel, across 35 different metrics (from the environmental to the economic). Total costs per km are still 10-30% higher for natural gas, even based on $3/mcf Henry Hub, which is 5x cheaper than US diesel.

Content by Category

- Batteries (87)

- Biofuels (42)

- Carbon Intensity (49)

- CCS (63)

- CO2 Removals (9)

- Coal (38)

- Company Diligence (91)

- Data Models (821)

- Decarbonization (159)

- Demand (110)

- Digital (58)

- Downstream (44)

- Economic Model (200)

- Energy Efficiency (75)

- Hydrogen (63)

- Industry Data (275)

- LNG (48)

- Materials (81)

- Metals (74)

- Midstream (43)

- Natural Gas (146)

- Nature (76)

- Nuclear (23)

- Oil (162)

- Patents (38)

- Plastics (44)

- Power Grids (123)

- Renewables (149)

- Screen (112)

- Semiconductors (30)

- Shale (51)

- Solar (67)

- Supply-Demand (45)

- Vehicles (90)

- Wind (43)

- Written Research (347)