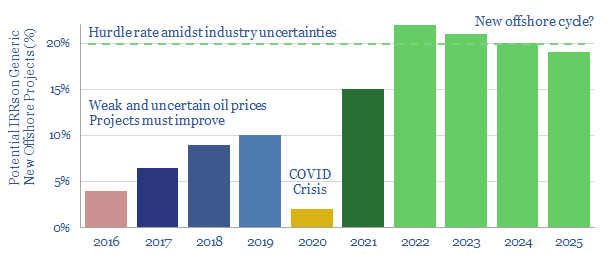

Oil markets look primed for a new up-cycle by 2022, which could culminate in Brent surpassing $80/bbl. This is sufficient to unlock 20% IRRs on the next generation of offshore projects, and thus excite another cycle of offshore exploration and development. Beneficiaries include technology leaders among offshore producers, subsea services, plus more operationally levered offshore oil services. The idea is laid out in our 17-page note.

Our oil market outlook is detailed on pages 2-5, seeing 2Mbpd of under-supply by 2022 and a potential inventory draw of 2.5bn bbls.

>$80/bbl oil prices are needed to instigate a new offshore cycle, as modelled and explained on pages 6-9.

Can’t the next oil cycle be quenched purely by ramping up short-cycle shale, instead of another offshore cycle? We answer this pushback on pages 10-11.

Is another offshore cycle compatible with the energy transition and global decarbonization? We answer this pushback on pages 12-13, with detailed data on CO2 emissions per barrel offshore versus elsewhere.

Who benefits? We present the technology leaders among producers, service companies and emerging technologies on pages 14-17, drawing on our prior patent screens and technical research.

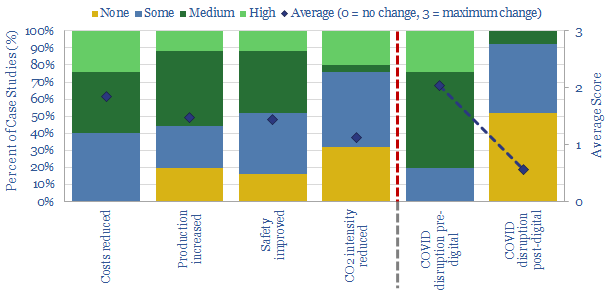

Digitization offers superior economics and CO2 credentials. But now it will structurally accelerate due to higher resiliency: Just 8% of digitized industrial processes will be materially disrupted due to COVID-19, compared to 80% of non-digitized processes. In this 22-page research report, we have constructed a database of digitization case studies around the energy industry: to quantify the benefits, screen the most digital operators and identify longer-term winners from the supply chain.

Pages 2 outlines our database of case studies into digitization around the energy industry.

Page 3 quantifies the percentage of the case studies that reduce costs, increase production, improve safety and lower CO2.

Pages 4-6 show how digitization will improve resiliency by 10x during the COVID-crisis, stoking further ascent of energy industry digitization.

Page 7 generalizes to other industries, arguing digitization will accelerate the theme of remote working, esepcially in physical manufacturing sectors.

Pages 8-9 screen for digital leaders among the 25 largest energy companies in the world, based on our assessment of their patents, technical papers and public disclosures.

Pages 10-11 identify leading companies from the supply chain, which may benefit from the acceleration of industrial digitization; again based on patents and technical papers.

Pages 12-22 present the full details of the digitization case studies that featured in our database, highlighting the best examples, key numbers and leading companies; plus links to delve deeper, via our other research, data and models.

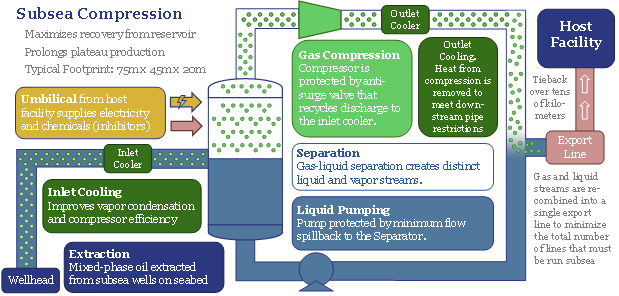

Offshore developments will change dramatically in the 2020s, eliminating new production platforms in favour of fully subsea solutions. The opportunity can increase a typical project’s NPV by 50%, reduce its breakeven by one-third and effectively eliminate upstream CO2 emissions. We have reviewed 1,850 patents to find the best-placed operators and service providers, versus others that will be disrupted. Overall, the theme supports the ascent of low-carbon natural gas, which should treble in the energy mix by 2050. This 22-page note presents the opportunity.

The offshore oil and gas industry’s progress towards ‘fully subsea’ developments, without any platforms or surface infrastructure being necessary, is reviewed in detail in pages 2-5, covering key projects and milestones from 1985-2000.

30% economic savings in both capex and opex are quantified line-by-line, across c50 cost lines, in pages 6-9.

1.5x NPV uplifts and 4pp IRR uplifts are quantified by modelling a representative fully greenfield gas-condensate project on pages 11-12.

CO2 emissions can be virtually eliminated by a fully subsea development solution. Pages 12-13 add up the impacts of higher efficiency, power from shore, fewer materials and the elimination of PSV/helicopter trips.

The key engineering challenges for fully subsea systems, which remain to be resolved, are summarized on page 14.

Who benefits from the trend toward fully subsea systems, is described from page 15 onwards after reviewing 1,850 patents around the industry. This includes both the leading service companies and operators (primarily Equinor, but also TOTAL, Shell).

The leaders in subsea compression technology are assessed on pages 16-17.

The leaders in subsea power systems are described on pages 18-19.

The leaders in next-generation subsea robotics are assessed on pages 20-21.

Others are disrupted, as is described in detail in page 22.

Covered service companies in the report include ABB, Aker, Eelume, GE, Kraken, Oceaneering, OneSubsea, Saipem, Siemens, Technip-FMC, Wood Group, the PSV and helicopter sector, and c20 early stage companies in next-generating subsea robotics.

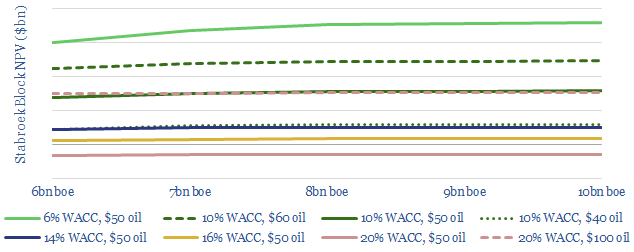

Prioritising low carbon barrels will matter increasingly to investors, as they can reduce total oil industry CO2 by 25%. Hence, these barrels should attract lower WACCs, whereas fears over the energy transition are elevating hurdle rates elsewhere and denting valuations. In Guyana’s case, the upshot could add $8-15bn of NAV, with a total CO2 intensity that could be c50% below the industry average.

Pages 2-3 introduce our framework for decarbonisation of the global energy system. Within oil, this requires prioritising lower carbon over higher carbon oil barrels.

Pages 3-6 outline the economic value in Guyana, which is now at the point where it is hard to move the needle with further resource discoveries.

Pages 7-8 show how lower WACCs can be trasnformative to resource value, even more material than increasing oil prices to $100/bbl.

Pages 9-17 outline the top technologies that should minimise Guyana’s CO2 emissions per barrel, including flaring policies, refining quality, midstream proximity, proprietary gas turbine technologies from ExxonMobil’s patents and leading digital technologies around the industry.

Our conclusion is that leading companies must deepen their efforts to minimise CO2 intensities and articulate these initiatives to the market.

Key points on Guyana carbon credentials and oil capital costs are spelled out in the article sent out to our distribution list.

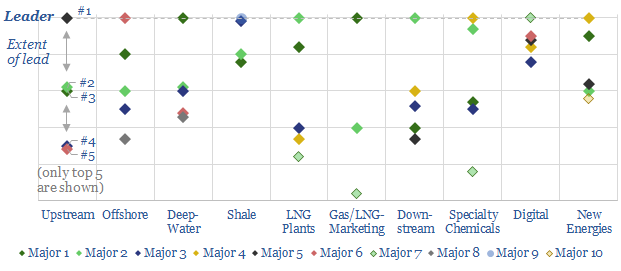

Technology leadership is crucial in energy. It drives costs, returns and future resiliency. Hence, we have reviewed 3,000 recent patent filings, across the 25 largest energy companies, in order to quantify our “Top Ten” patent leaders in energy.

This 34-page note ranks the industry’s “Top 10 technology-leaders”: in upstream, offshore, deep-water, shale, LNG, gas-marketing, downstream, chemicals, digital and renewables.

For each topic, we profile the leading company, its edge and the proximity of the competition.

Companies covered by the analysis include Aramco, BP, Chevron, Conoco, Devon, Eni, EOG, Equinor, ExxonMobil, Occidental, Petrobras, Repsol, Shell, Suncor and TOTAL.

Upstream technology leaders have been discussed in greater depth in our April-2020 update, linked here.

More information? Please do not hesitate to contact us, if you would like more information about accessing this document, or taking out a TSE subscription.

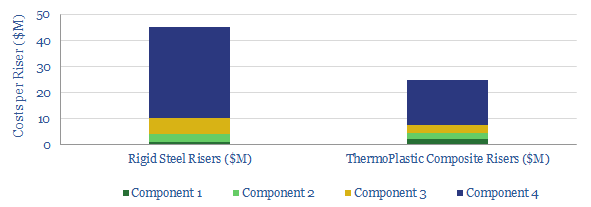

Petrobras has patented next-generation riser designs, to handle sour-service crude from pre-salt Brazil. This is needed after prior cases of riser-failure, e.g., at Lula. Its new solution could also support development of higher-CO2 fields, such as Libra. But complexity is an order of magnitude higher. A simpler alternative is the growing potential from thermo-plastic composite pipe, which resists corrosion and is 45% more economical than conventional risers.

Pre-salt riser failures from CO2-corrosion

In 2017, Upstream Newspaper reported that Petrobras had suffered two riser failures, injecting high-CO2 gas back into the Lula and Sapinhoa reservoirs. The failures occurred after just 3-years, at risers designed to last for 25.

These failures were induced by stress-corrosion, which in turn derives from the high CO2 content in the pre-salt. For example, CO2 is reported at 8-12% at Lula.

As Petrobras moves to develop even higher-CO2 fields, such as Mero (Libra), where the gas is up to 30% CO2, it has also sought to minimise the use of flexible risers, to protect against corrosion.

New solutions… new challenges?

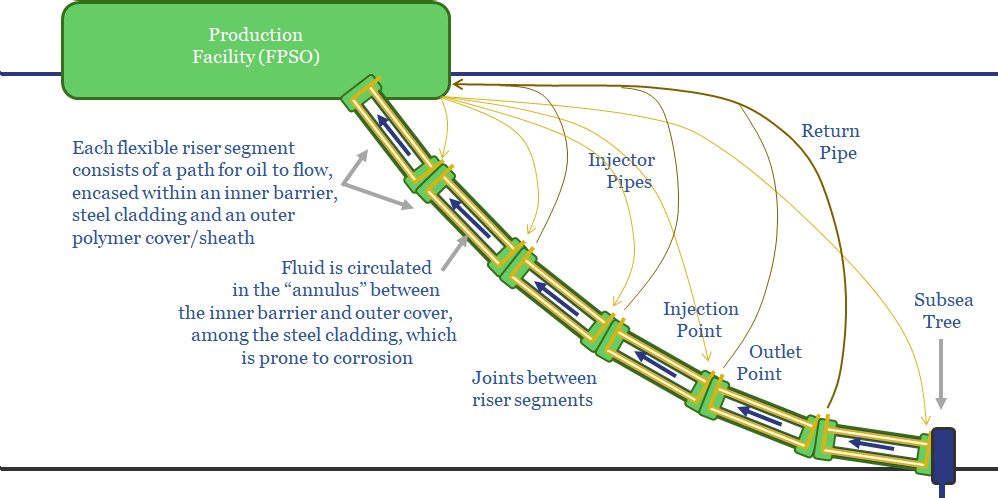

Improved riser solutions feature prominently in Petrobras’s 2018 patent filings, which we have reviewed. One patent localises the problem of stress-corrosion to the risers’ steel cladding, which is situated in the annulus between the riser’s barrier layer and outer sheath. The barrier layer can sometimes be breached by fluids moving through the riser.

Petrobras states:“Stress corrosion is caused by CO2 and not well-covered by international standards for flexible pipes...there is normally no way to displace gases from the annulus or minimise their corrosive effects”.

It is noted that Chevron, Schlumberger and GE have all patent solutions to detect the presence of corrosive fluids reaching the steel cladding of a riser. However, to mitigate this problem, comprehensively, in a flexible, deep-water riser with many segments, Petrobras has filed its own solution (chart below).

Inert fluids are envisaged to be swept through the annulus of the riser, removing any corrosive fluids that have accumulated. The fluid is forced through each independent segment of pipe. Leak tests can be performed to detect damaged sections.

Another argument for composites?

What strikes us about Petrobras’s solution is the added complexity. As pictured above, it will be necessary to maintain a flow of anti-corrosive fluids through each riser segment, via an additional series of injection pipes and return pipes. All of these must be fabricated, installed and maintained.

After weighing up the additional complexity of circulating anti-corrosive fluids through the cladding of flexible pipelines, we grow more positive on the relative simplicity of an alternative: themo-plastic composite risers (TCP).

These next-generation materials are corrosion-resistant, withstanding CO2 concentrations up to 50% and H2S up to 200ppm. They also deliver comparable strength to steel, at 10% of the weight, which simplifies their installation and lowers overall costs for a riser system by 45% (chart below).

For our data-file quantifying the progress-to-date and the costs of TCP, please see here.

Source: Carpigiani de Almeida, M., Cameiro Campello, G., Ribeiro, J., Mello Sobreira, R. G., Loureiro Junior, W. C. & Piza Paes, M. T. (2018). System and Method for Forced Circulation of Fluids Through the Annulus of a Flexible Pipe. Petrobras Patent 2018220361.

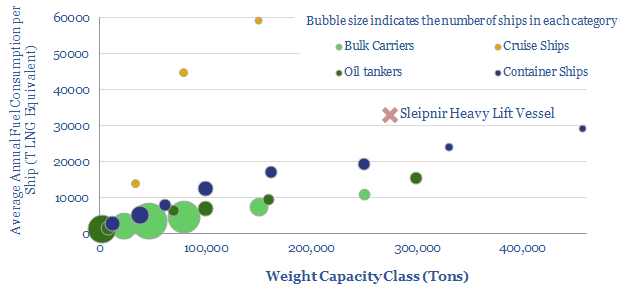

Multiple records have just been broken for an LNG-powered ship, as construction completed at Heerema’s “Sleipnir” heavy-lift vessel (charted above). It substantiates our recent deep-dive note, which sees 40-60MTpa upside to LT LNG demand, from large, fuel-intensive ships, after IMO 2020.

Sleipnir is a record-setting crane-lift vessel, with capacity to pick up 20,000T. This eclipses the prior records in offshore oil and gas, which were around 12,000T, set by the Heerema Thialf and the Saipem 7000. Hence Sleipnir has already lined up 18 contracts, starting with the 15,800T topsides for Israel’s Leviathan gas field, and progressing on to Johan Sverdrup Phase II.

Sleipnir is a record-setting LNG vessel, burning gas as its primary fuel (although it can also burn diesel). With a displacement of 273,700T, we estimate it is the heaviest LNG-powered vessel ever built (eclipsing the largest such container ships, at 220,000T). With a cost of $1.5bn, we estimate it is also the most expensive LNG-powered ship ever built (eclipsing Carnival’s $1.1bn AidaNova cruise ship). It has the world’s first Type-C LNG tank in an enclosed column. Numbers are updated in our data-file here.

There is upside to LNG demandin large, fuel-intensive ships, especially cruise- and container ships, after IMO 2020. Small-scale LNG may offer an economic “bridge”, while bunkering becomes increasingly attractive as volumes per port scale past c80kTpa. Forward-thinking Majors are already investing to capture the future market.

Finally, for a video of the construction vessel being constructed…

A typical offshore operator can very readily save $1/boe via continued, digital deflation; which is tantamount to $1bn per annum at a c3Mboed Oil Major.

Our numbers are derived from a case study by Cognite, which is among the leaders in oilfield digitization, collaborating with cutting-edge E&Ps, as described below.

Digitization remains the most promising opportunity to improve offshore economics. But the gains are granular and can only be seen by delving into the detail…

[restrict]

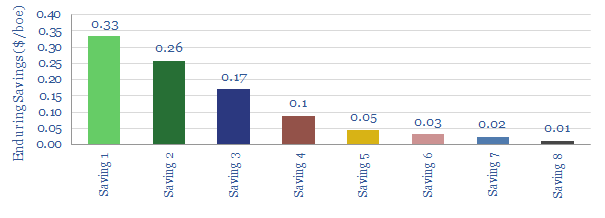

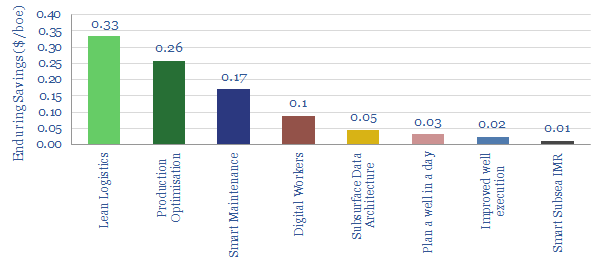

This short note will focus further upon three particular avenues for digital deflation, which collectively account for $0.6/boe of cost savings at a typical offshore operator.

All are achieved using greater data instrumentation, as highlighted in Cognite’s recent case study, based on working alongside Aker-BP, which we calculate can save $1/boe across the operator’s portfolio (chart below).

(1). Production Optimisation can be attained by increasing the throughputs in processing units, such as separators. In Cognite’s example, this is safely achieved by using better data from multi-phase flow-meters upstream of the processing units. Better data enables better performance. Deferrals associated with the flow-meter calibration are also reduced by 30-50%.

(2). Smart maintenance of equipment can be achieved by greater monitoring. For instance, the Ivar Aasen sends data back to shore, in real time, on 90,000 information packages, including 18,000 valves, all the wells, compressors, pumps and generators. Cognite’s example is at these shut-down valves and fire dampers, which now require 80% fewer maintenance hours to check. In addition, the number of hours per miantenance check is reduced by 90%.

(3). Improved information flow to “digital workers” improves productivity. As context, maintenance of a large process unit (e.g., a 1st stage separator) may require 1,300 planning hours per year, but this can be improved using data (video below). In turn, this superior planning reduced the time spent on routine inspections by c50%, increasing the number of monthly maintenance jobs by 10% and with better HSE performance.

A virtual visit to an offshore oil platform, instrumented by Cognite. Live data are displayed and can be further interrogated for planning purposes …

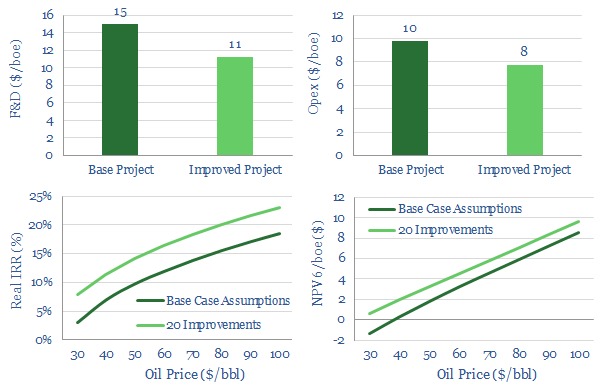

Digital improvements offer great potential to improve offshore economics. However, as we have highlighted, no individual improvement is a magic bullet. Uplifting IRRs, particularly on new greenfield projects by say, 5pp, requires progress on as many as twenty different dimensions (chart below).

This is where Thunder Said Energy can help, screening the economic opportunities and best-practices across different companies, using our databases of patents and technical papers.

The appetite to invest in new offshore oil projects has been languishing, due to fears over the energy transition, a preference for share-buybacks, and intensifying competition from short-cycle shale. So can technology revive offshore and deep-water? This note outlines our ‘top twenty’ opportunities. They can double deep-water NPVs, add c4-5% to IRRs and improve oil price break-evens by $15-20/bbl.

Pages 9-18 of the note outline each of our ‘top twenty’ focus areas, after reviewing 1,500 patents and 300 technologies across the industry. In each case, we outline which companies are most advanced.

Our work shows it is essential to invest with – or have your resources managed by – technology leaders. The industry must also keep improving, to re-excite investment.

Cookies?

This website uses necessary cookies. Our cookies are simply to improve your experience. We do not undertake any advertising or targeting via our cookies. By clicking 'accept' or continuing to use the website, you consent to our use of cookies.AcceptRead More

Privacy & Cookies Policy

Privacy Overview

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.