Natural Gas

-

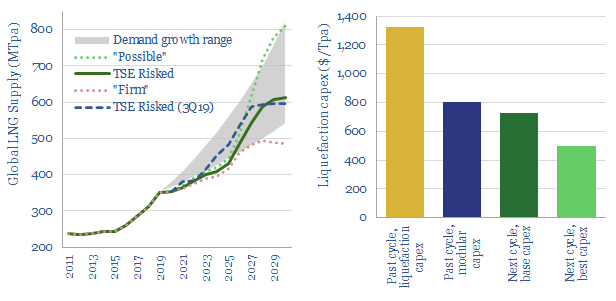

LNG in the energy transition: rewriting history?

A vast new up-cycle for LNG is in the offing, to meet energy transition goals, by displacing coal. 2024-25 LNG markets could by 100MTpa under-supplied, taking prices above $9/mcf. But emerging technologies are re-shaping the industry, so well-run greenfields may resist the cost over-runs that marred the last cycle.

-

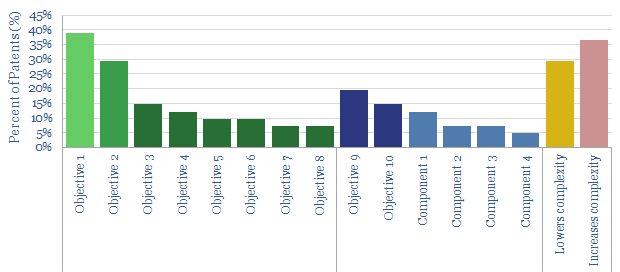

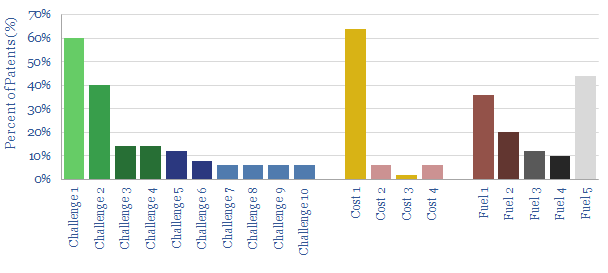

LNG liquefaction: what challenges and opportunities?

This data-file reviews 40 recent LNG patents, to draw conclusions and identify leading companies. Lowering capex costs matters, but should not be done at the expense of higher opex or emissions. The next generation of modular plants offer a step-change improvement. And new process technologies are also coming through.

-

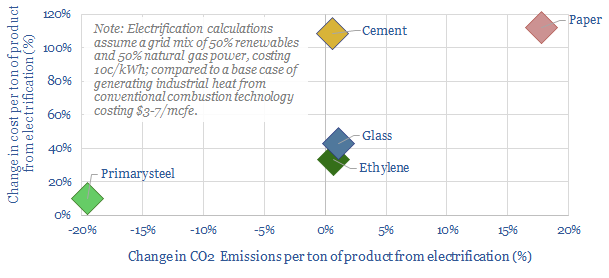

Industrial heat: the myth of electrify everything?

“Electrify everything then decarbonize electricity”. This mantra is dangerously incorrect for industrial heating. It raises output costs by 10-110% without lowering CO2. Our 19-page note presents case studies in the steel, cement, glass, petrochemical and paper industries, which exceed 15% of global CO2.

-

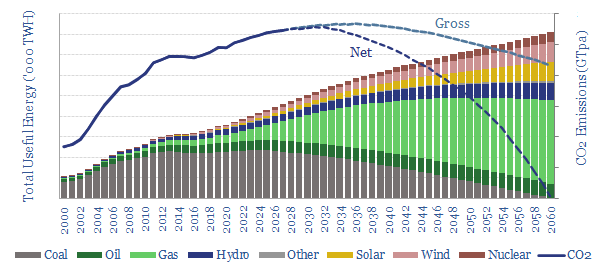

China: can the factory of the world decarbonize?

China now aspires to reach ‘net zero’ CO2 by 2060. But is this compatible with growing an industrial economy and attaining Western living standards? The best middle-ground sees China’s coal phased out and gas rising by a vast 10x to 300bcfd. The biggest challenges are geopolitics and sourcing enough LNG.

-

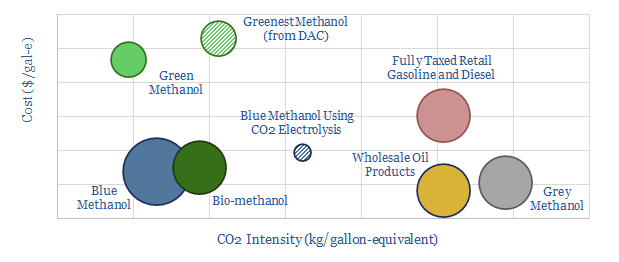

Methanol: the next hydrogen?

Methanol is becoming more exciting than hydrogen as a clean fuel to help decarbonize transport. Specifically, blue methanol and bio-methanol are 65-75% less CO2-intensive than oil products, while they already earn 10% IRRs at c$3/gallon prices. Unlike hydrogen, it is simple to transport and integrate methanol with pre-existing vehicles.

-

Methanol production: the economics?

This model captures the economics and CO2 intensity of methanol production in different chemical pathways. We find exciting potential for bio-methanol and blue methanol. These are logistically simple substitutes for oil products, but with lower carbon content. Full cost breakdowns can be stress-tested in the data-file.

-

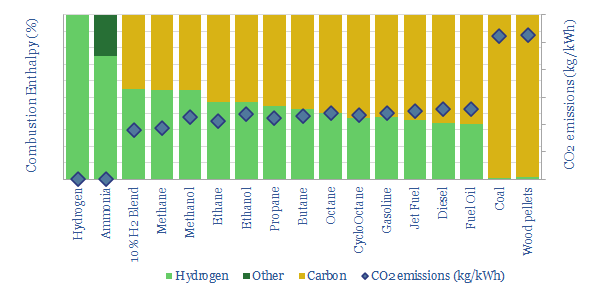

Energy economics: energy content of combustion fuels?

The purpose of this data-file is to disaggregate the energy economics of combusting different fuels, including natural gas, different oil products, NGLs, coal, hydrogen, methanol, ammonia et al. The most effective way to blend more hydrogen into the energy mix is coal-to-gas switching, followed by using lighter oil products.

-

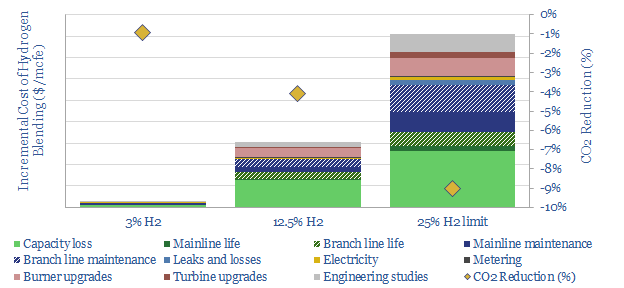

Hydrogen blending: costs and complexities?

This data-file estimate the costs of blending hydrogen into pre-existing natural gas pipeline networks. Costs are relatively low per mcf of gas, but very high per ton of CO2 abated. Costs also rise exponentially, as more hydrogen is blended into the mix.

-

Solid oxide fuel cells: what challenges?

This data-file reviews fifty patents into solid oxide fuel cells, filed by leading companies in 2020. The key focus areas are improving the longevity and efficiency of SOFCs. But unfortunately, we find many of the proposed solutions are likely to increase end costs. Potential is interesting, but deflation may take longer.

-

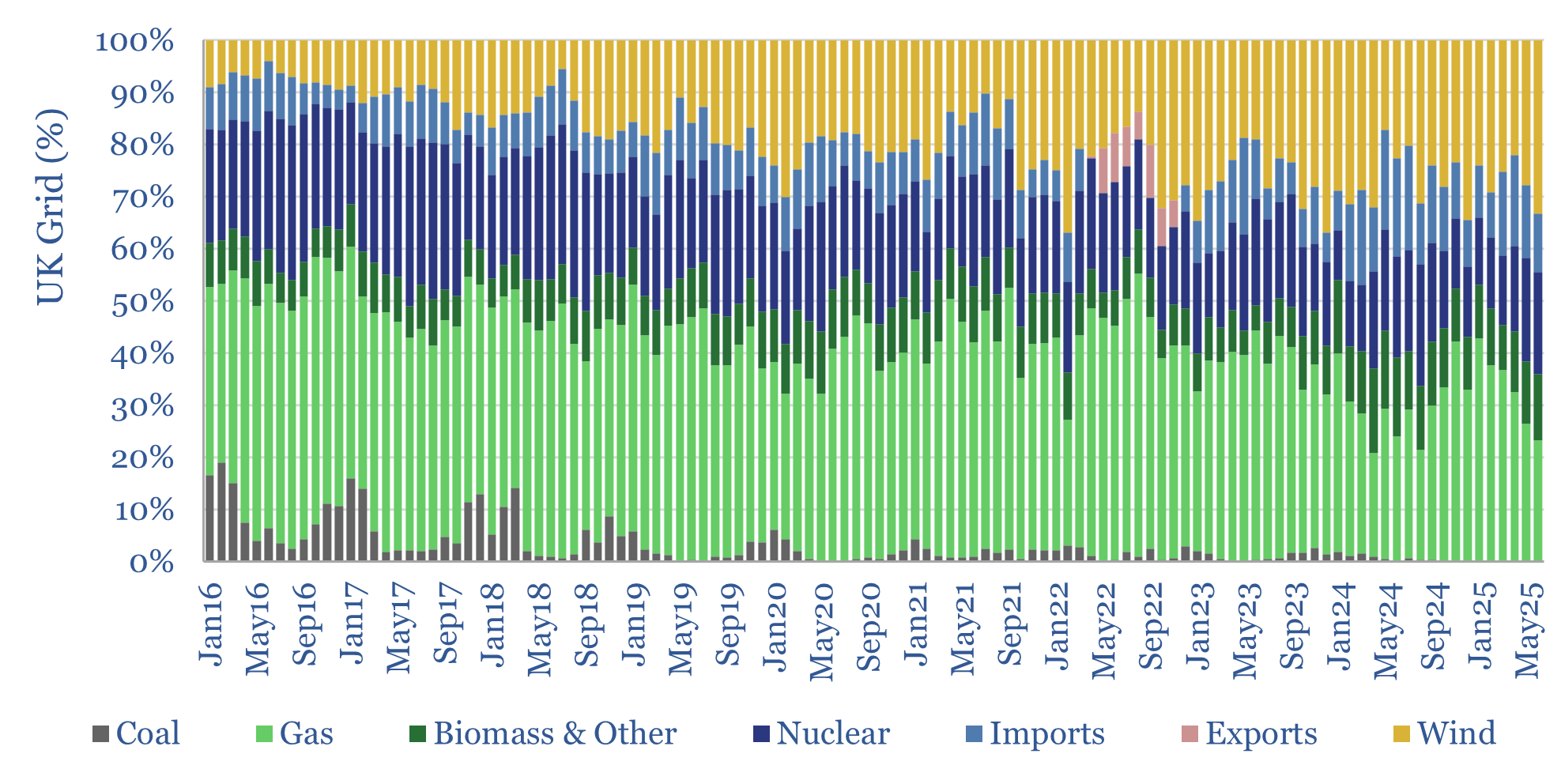

UK grid volatility as renewables gain share?

This data-file contains the output from some enormous data-pulls, evaluating UK grid power generation by source, its volatility, and the relationship to hourly traded power prices. We conclude the grid is growing more expensive and volatile, with the increasing share of wind.

Content by Category

- Batteries (96)

- Biofuels (44)

- Carbon Intensity (48)

- CCS (64)

- CO2 Removals (9)

- Coal (41)

- Commentary (65)

- Company Diligence (104)

- Data Models (921)

- Decarbonization (162)

- Demand (129)

- Digital (86)

- Downstream (47)

- Economic Model (220)

- Energy Efficiency (76)

- Hydrogen (63)

- Industry Data (308)

- LNG (56)

- Materials (86)

- Metals (88)

- Midstream (45)

- Natural Gas (161)

- Nature (76)

- Nuclear (28)

- Oil (175)

- Patents (39)

- Plastics (44)

- Power Grids (155)

- Renewables (153)

- Screen (137)

- Semiconductors (35)

- Shale (58)

- Solar (72)

- Supply-Demand (53)

- Vehicles (95)

- Video (24)

- Wind (47)

- Written Research (406)