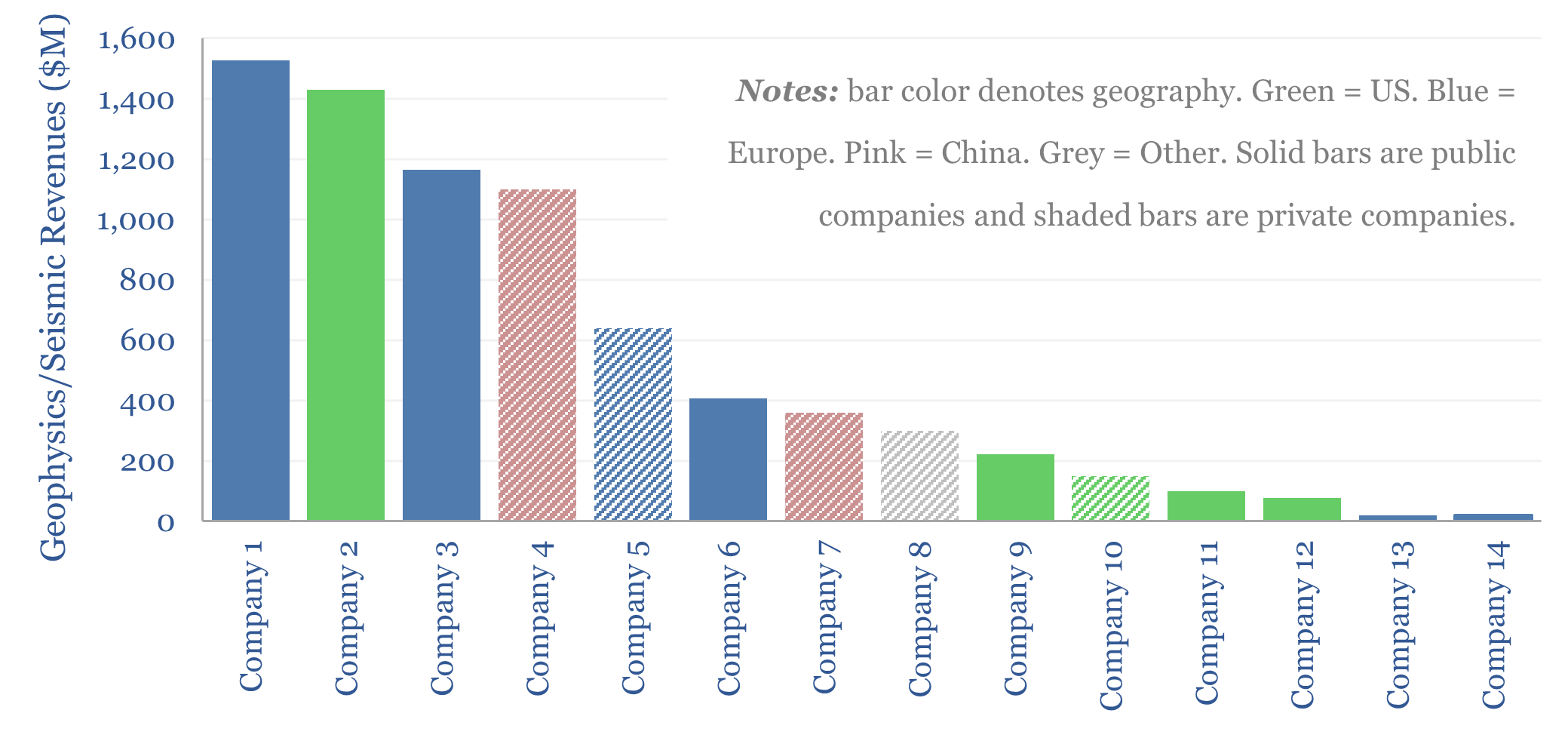

This data-file screens 14 leading seismic and geophysics companies, based on company disclosures and reviewing c500 patents over the past 20-years. This restructured and increasingly consolidated industry is now worth $10bn pa. Companies have recently generated c10% EBIT margins. But capabilities are growing and costs are deflating through deploying AI?

Leading seismic and geophysics companies are compared in the ‘Screen’ tab of this data-file, highlighting when each company was founded, its market cap, net debt, EV, 2025 revenues, seismic/geophysics revenues, EBIT margin, employee count, patent activity, companies notes and AI/digitization notes.

The seismic industry is worth c$10bn pa, and generated c10% EBIT margins in 2025, across acquisition vessels, data-processing, data-interpretation and the licensing of prior multi-client surveys. The average offshore seismic survey costs $10,000 per km2, based on our data-file tracking the costs of seismic.

Restructurings have transformed the offshore seismic industry in the past decade. CGG became Viridien, PGS merged into TGS, Schlumberger exited seismic acquisition, Chinese companies like BGP have gained share, Polarcus liquidated and its assets transferred to Shearwater and PXGEO.

However leading Western companies retain world-class hardware, manufacturing facilities, large multi-client seismic libraries, software and personnel, and increasingly, the ability to do more with AI in seismic.

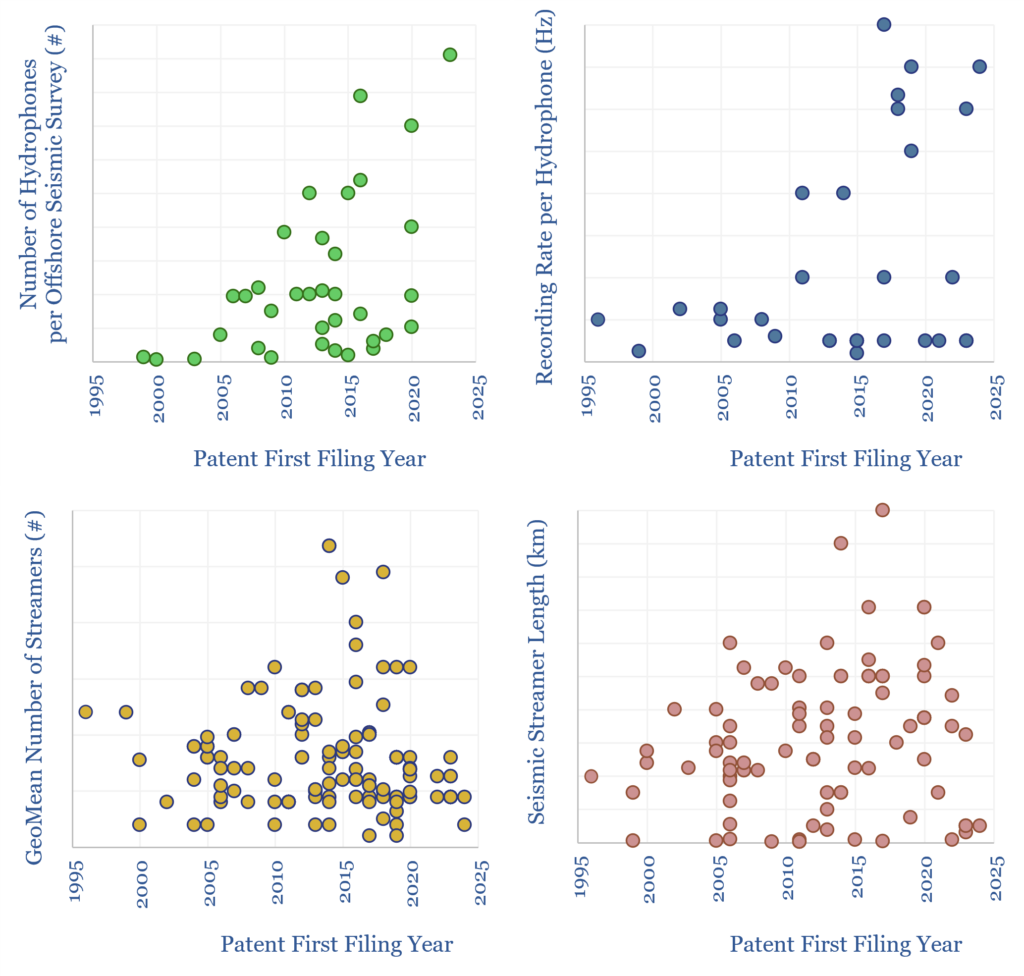

Seismic surveys have also become capable of capturing more data over time, to improve resolution. We have drawn datapoints from over 500 patents. How these patents are increasing resolution is in the ‘Patents’ tab.

Hydrophones per offshore survey have trebled in the past decade and recording rate has doubled. A typical survey still tows maybe 7 streamers, each 6km long, although this is now often supplemented with data from higher-resolution ocean-bottom nodes. In the past half-decade 20% of patents involve AI.

Many seismic companies have tried to broaden their scope to new energies, including seismic studies for CCS reservoirs, or weather/geophysics data for wind and solar projects, but these businesses remain smaller. The best prospects are perhaps still found in hydrocarbon exploration.