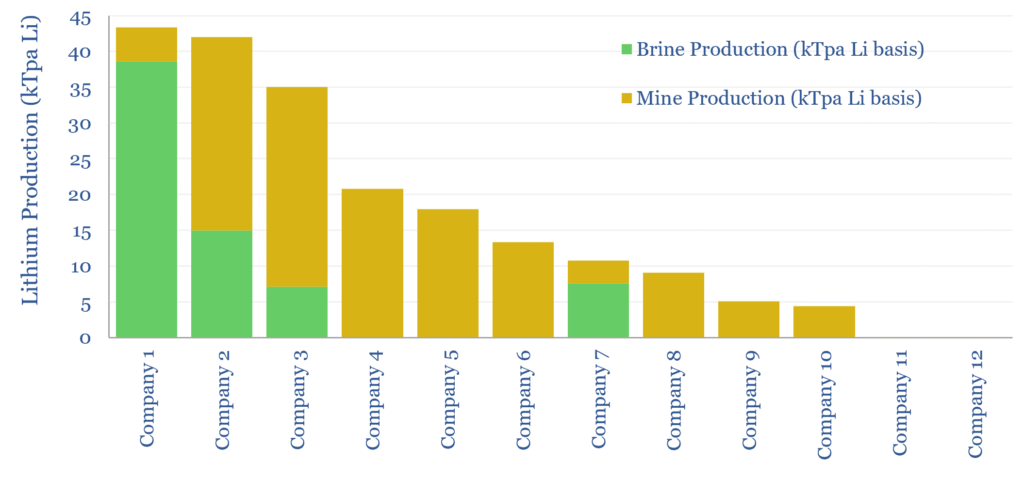

This data-file screens lithium producing companies, their asset bases and financials. Ten companies currently produce almost 80% of the world’s lithium. 65% is from mining assets, 35% from brines and evaporation ponds. What outlook for lithium producers in an AI energy transition?

Global battery demand grows by 8x by 2050, driven by electric vehicle sales, grid storage, robotics and other themes in the AI energy transition. LFP has emerged as the most economical battery chemistry. For cost reasons, we also do not currently see lithium being disrupted by sodium ion batteries until lithium prices return to $40/kg. Hence we see 9% pa lithium demand growth.

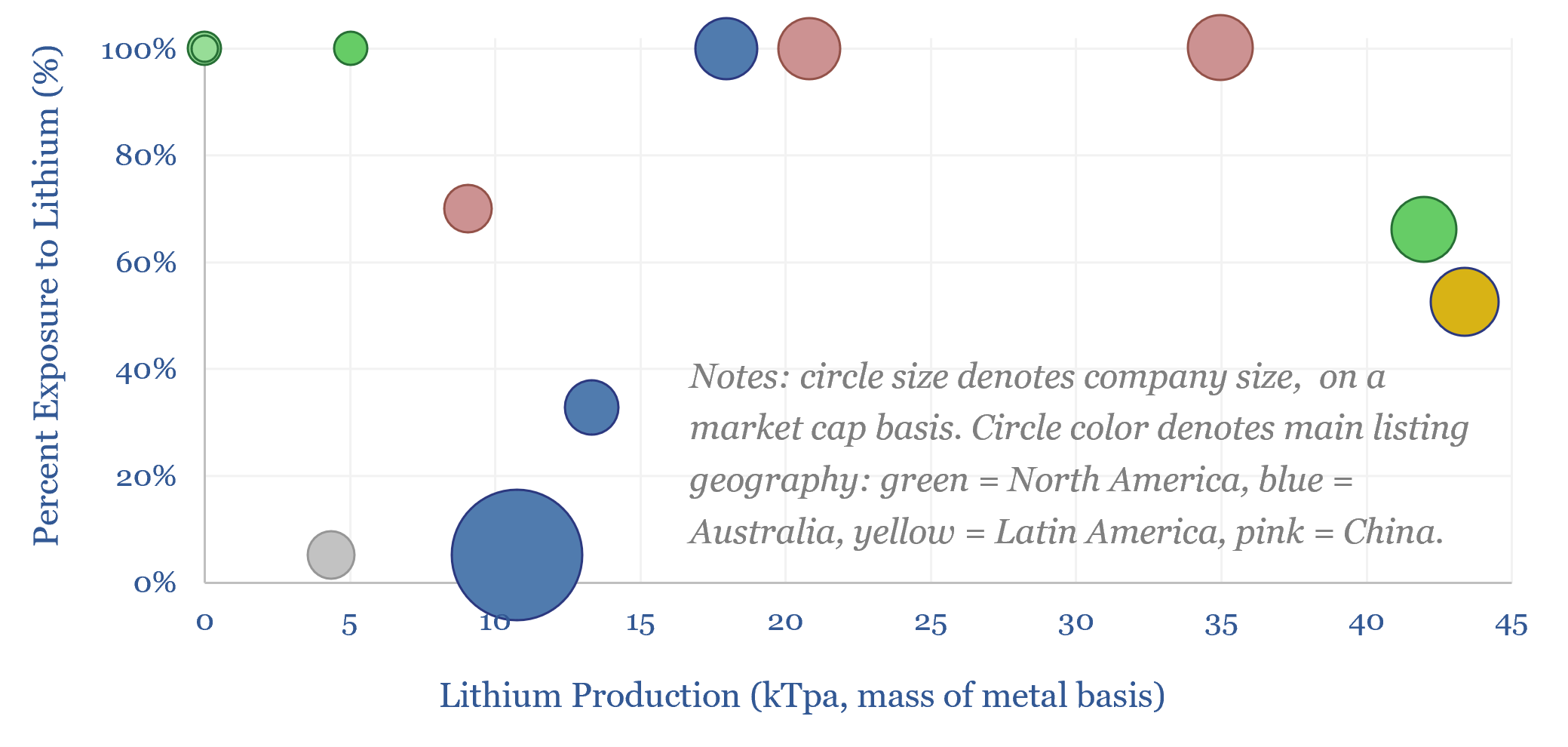

For each major lithium producing company in this data-file, we have tracked employee counts, market cap, production from mines, brines, downstream chemical processing facilities, revenues, EBIT, net income, exposure to lithium, and key company details.

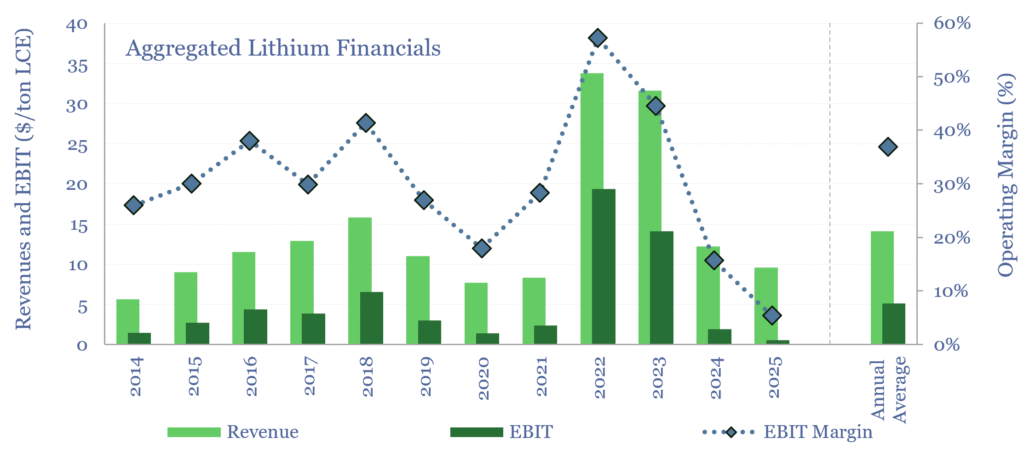

Lithium pricing has been volatile over the past decade, rising from $10/kg (lithium carbonate basis) in 2014-20, to $40/kg in 2022-23, then back to $12/kg in 2025.

Accordingly, our peer group’s lithium businesses generated 30% EBIT margins from 2014-20, EBITDA rose by 10x in 2022-23, while EBIT margins came back down to 10% in 2024-25, and the sector was loss-making at the net level in 2025.

Consolidation and maturation have taken place across the industry over the past five years. The clearest example would be the merger of Orocobre and Galaxy Resources in 2021, to form Allkem, the subsequent merger of Allkem with Livent in 2024, to form Arcadium, and then the acquisition of Arcadium by Rio Tinto, for $6.7bn in cash in 2024.

Lithium production from evaporating lithium brines is usually more economical than lithium mining-refining. And all the more so in 2026. It takes 8 tons of hot sulfuric acid, at 250-300◦C, to leach each ton of lithium from mined spodumene concentrate. But in 2026, half of the seaborne sulfur market has been unable to transit through the Strait of Hormuz, pushing sulfur prices from $150/ton to $300/ton.

There remains a long list of junior lithium miners, in the pre-production phase, and we are tracking their projects in our lithium supply-demand data-file. But in this data-file, we focus in more on producers and larger project developers. The Western world’s large lithium producer, famously, is Albemarle. We have also screened Albemarle’s patents.

Please download the data-file, for our outlook on leading lithium producers, their asset bases, and financial indicators over the past decade, which we have tabulated where available.