Today’s power grids fire up peaker plants to meet peak demand. But the grid is changing rapidly. Hence this 17-page report outlines the economics of gas peaker plants. Rising volatility will increase earnings and returns by 40-50%, before grid-scale batteries come into the money for peaking?

25% of global electricity came from burning 150bcfd of natural gas in 2023. An overview of simple-cycle gas turbines, combined-cycle gas turbines, and gas peaker plants is re-capped on pages 2-3.

There is a problem with levelized cost analysis. Peakers do not access ‘the same prices’ as other generation sources. They access the upper tail of a statistical distribution. This crucial point is outlined on pages 4-5.

That statistical distribution is lognormal. We show how actual power prices in actual grids tend to be lognormally distributed on pages 6-7.

The economics of gas peaker plants across different utilization rates and grid conditions can thus be properly quantified, on pages 8-9.

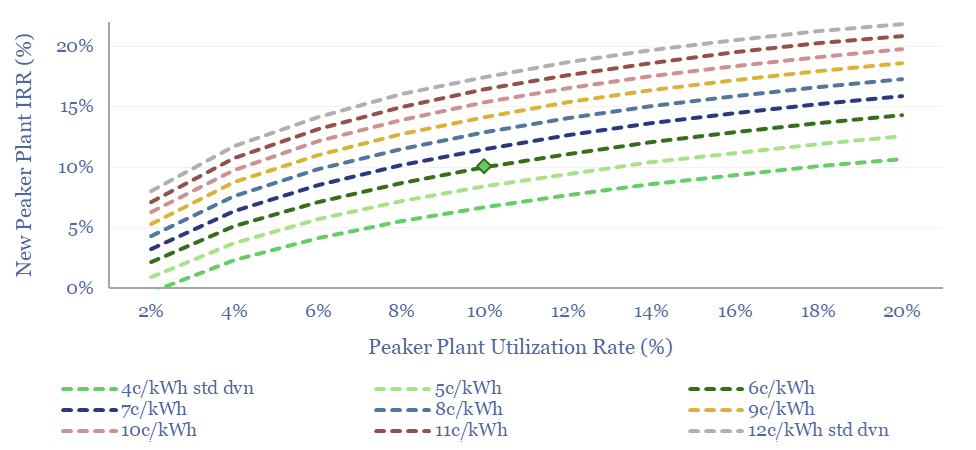

Rising volatility in global power markets results in higher standard deviations for power price distributions, and in turn, increases potential returns and earnings of peaker plants, as quantified on pages 10-11.

Is there upside or downside for gas peaker plants? Other supply-demand considerations are presented on page 12.

Will grid-scale batteries displace peakers? For the first time, we are able to properly compare the economics of gas peakers and grid-scale batteries, in a way that is truly apples for apples, on pages 13-14.

Which companies operate the most gas peakers? To answer this question, we have expanded our database of all US gas generation facilities and identified 30 of the largest fleets. Two listed IPPs stood out with relatively higher exposure to gas peakers, while ten of the larger companies are discussed on pages 15-17.