A dozen companies comprise 90% of all grid-scale battery storage systems (BESS), acting as the “battery integrators”, packaging lithium ion cells into containerized modules, which can be deployed and grid-connected. 2025 economics included $30bn of revenues, $250/kWh module prices and 8.5% operating margins. But competition is intensifying, including on cost, energy density, safety, operating systems and ease of deployment.

2025 has seen an acceleration in grid-scale battery deployments. But in fact, LFP cells only make up half of the mass, and 20-40% of the delivered cost of grid-scale batteries. Why is this?

Grid-scale batteries require integrating thousands of cells into racks within a module, then adding battery management systems, energy management systems, power conversion systems to achieve two-way energy flow, liquid cooling, fire suppression, instrumentation, controls and other power electronics.

Battery integrators acquire lithium ion cells and other power electronic components – either self-produced or from third-party suppliers, and then combine them into fully functional, installable and operable modules. They may also provide monitoring and maintenance services, once these systems are installed.

A dozen battery integrator companies are tracked in this data-file, generating $30bn of BESS revenues in 2024, at an average operating margin of 8.5%. Two-thirds of the companies are headquartered in China. Details on each company are tabulated in the companies tab of this data-file.

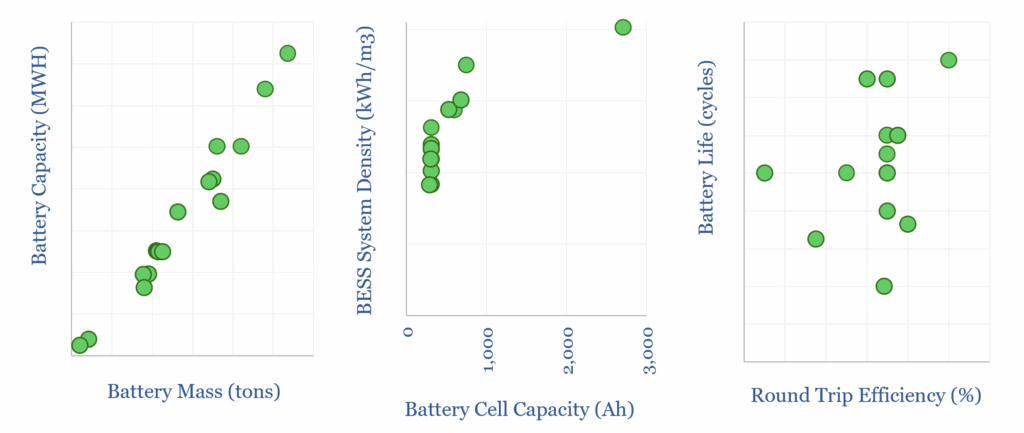

We have tabulated the details of 20 grid-scale battery products on the Products tab of the data-file, capturing the average module capacity (in MWH and MW), cell type (in Ah), cell energy (in kWh), number of cells, round-trip efficiency (%), rated life (years), rated number of cycles (in ‘000s), mass (tons), length (m), volume (m3), energy density (in Wh/kg and kWh/m3), and other details into cooling, fire suppression and operations.

What makes battery integration challenging is the product cycle. Two-thirds of the battery module products in the data-file have only been released in the past year, or are pre-release. Battery integrators are continually competing on making their products lower-cost, more energy dense, safer, easier-to-install, with more sophisticated management software.

Intense competition in the battery space may limit the potential for excess returns among battery integrators, may reward integration, and most of all may benefit those deploying batteries in power grids, for solar co-developments, for round-the-clock solar. This chimes with our recent outlook into the future of batteries.