Are speculative data center projects, 80% of which will never get built, inflating future load growth forecasts? This 18-page report reviews evidence from land developer returns, recent PUC deliberations and evolving terms in Electrical Service Agreements (ESAs).

In May-2026, we re-published our forecasts for 22GW pa of global data center capacity through 2035, the concomitant electricity demand, and our forecasts for US load growth of 2% pa over the same timeframe (see pages 2-3).

Many readers feel that these numbers “seem low”, especially when compared with the reporting from utilities and grid operators, which potentially indicate 5-10x more AI data center capacity is in various stages of development.

Our goal in this 18-page report is to assess whether our data center forecasts could be too low, potentially much too low. Or conversely, could data center project pipelines be inflated by speculative projects, many of which will never get built?

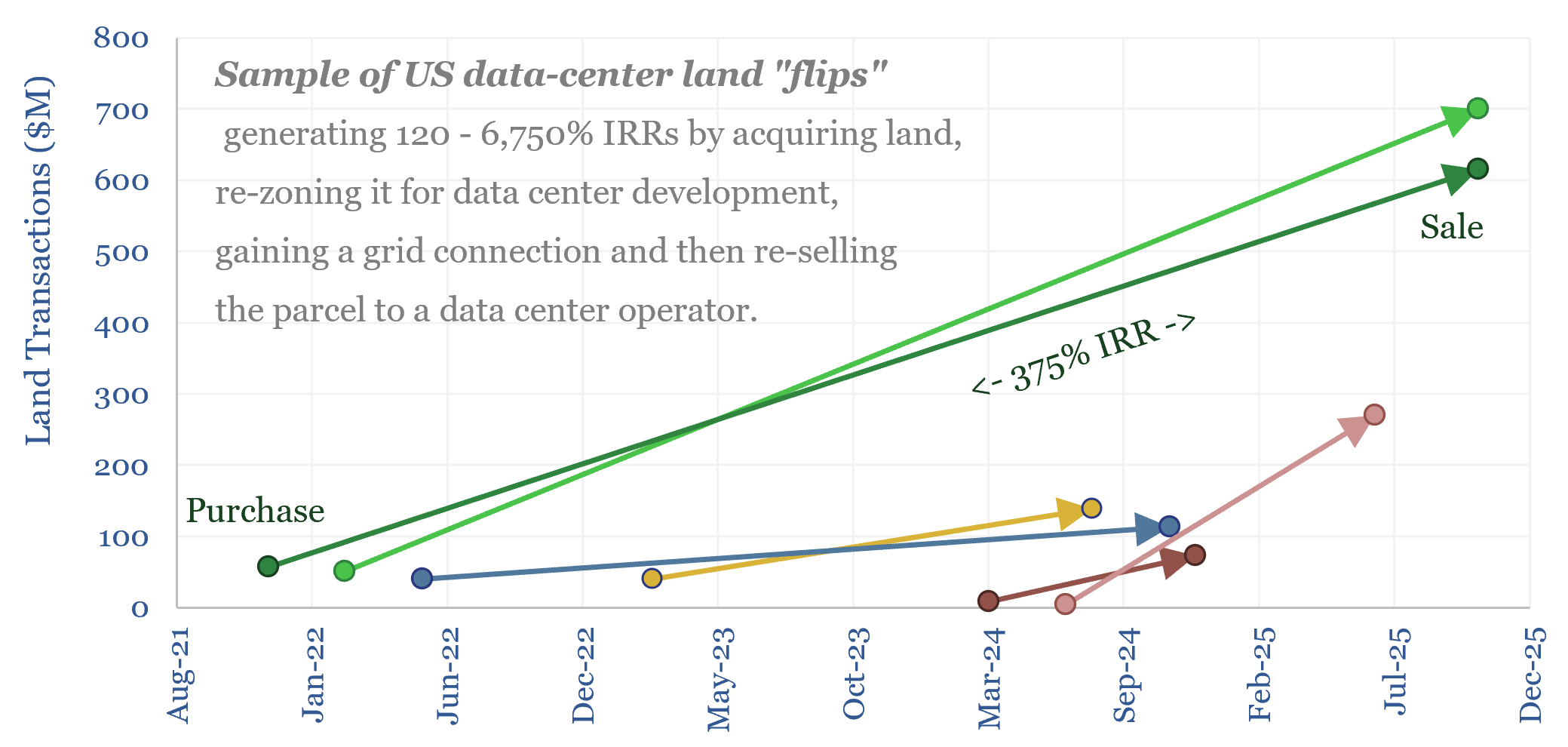

We tracked 20 recent data center land deals, including several with triple-digit IRRs, and built a bottom-up cost model for data center pre-construction on pages 4-7. The underlying data are in our data center economic model.

Astounding returns seem to have been available for land speculators, planning data centers, bringing them to shovel-ready status, then selling to large data center operators. This could warrant speccing out 5x more projects than ever get built.

Public utility commissions, and regional utilities, also seem to recognize that a large portion of the data centers entering their interconnect queues may be somewhat speculative, per pages 8-9.

Electrical Service Agreements (ESAs) are seen as having been too easy to secure in the past, which could leave consumers at risk of paying for stranded assets. We can understand this perspective, after reviewing some of these past ESAs, including for data centers, on pages 10-11.

Just because a project has an Electrical Service Agreement by no means de-risks the project and guarantees that it is going to be built, based on the details in these past ESAs. With apologies, there are quite a lot of nerdy ESA details in the report.

We also reviewed how ESA terms are now tightening, with 10-20 year take-or-pay contracts, and typically 12-24 months of up-front collateral requirements, on pages 12-14. But does this deter speculation or accelerate it?

Our conclusions over future load growth, the proportion of planned data centers that will actually get built, and potential boom-bust dynamics in related capital goods, are on pages 15-18.