Global LNG output ran at 406MTpa in 2024. This model estimates global LNG production by facility across 150 LNG facilities. Our latest forecasts are that global LNG demand will rise at a 6% CAGR, to reach 710MTpa by 2035, for an absolute growth rate of +30MTpa per year, but there is a supply-crunch in 2024-26, then a construction boom?

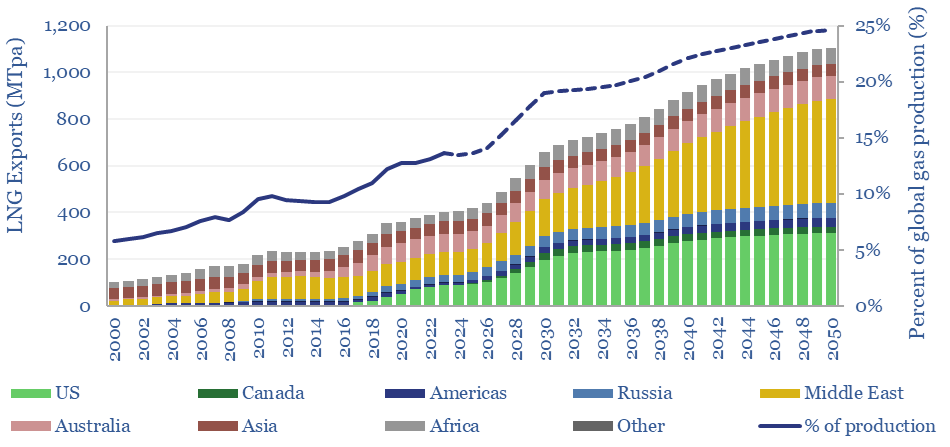

Global LNG production in 2024 ran at 406MTpa, of which 22% was from the United States, 20% was from Qatar and 20% was from Australia, as the three largest producers. Over the past decade, global LNG production has risen at +17MTpa each year.

This data-file breaks down global LNG production by facility, across each of 150 LNG plants, assessing recent news flow, and then estimating their production in each year from 2018-2035. For pre-FID facilities, we ascribe a ‘risking factor’, according to their likelihood of being built.

A short-term supply crunch has intensified for 2024-26. Global supplies only grew by +4MTpa YoY in 2024, missing forecasts for +10-20MTpa due to outages and delays.

Out of 70 upcoming developments tracked in our database, 27 saw delays (i.e., 40%) in 2024, relative to our expectations at the start of the year. Hence the 2025-26 supply outlook is tighter. This matters for our energy balances in Europe, China and Japan.

The cavalry arrives in 2027-2030, with the potential for 40-60MTpa of LNG supply growth each year in this time frame (charts above). 50MTpa of the 2026-28 supply growth is from Qatar’s North Field expansion. 20MTpa is from new LNG in Canada.

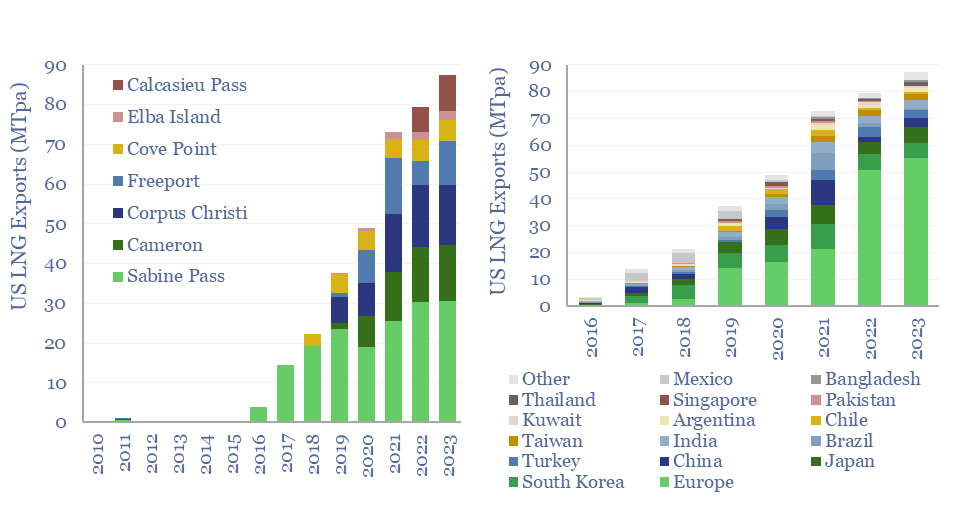

US LNG exports are seen with most potential to ramp from here, which is one reason we think the US gas market outlook is turning into the stuff of dreams. We see supplies almost trebling from 80 MTpa in 2022-23 to 240 MTpa by 2035. Our notes and risking on each project are in the data-file. We can also track where these cargoes go.

Looking out longer term, we see potential for the global LNG industry to reach 1,100MTpa by 2050 as part of the energy transition. This would take LNG from 10% of global gas a decade ago, through 13.5% of global gas in 2023, to 25% of global gas in 2050.

One of the biggest risks for global energy security, in our view, is paralysis in progressing pre- and post-FID LNG projects. LNG liquefaction economics are modeled here. In turn, this hands upside to incumbent LNG producers.

We also see upside for spot cargoes in a world that is persistently under-supplied with energy yet remains overly cautious of signing long-term contracts, and increasingly for LNG marketers, amidst the build-out of renewables, there is value in volatility.

Global LNG production by facility: model mechanics. This data-file of global LNG supplies works by assigning a “risking level” to each upcoming project. You can flex the output in the ProjectByProject tab to stress test “firm” supplies, various risking levels, and a “best case” production scenario. As a historical record, we have also ‘frozen’ all of our forecasts from 2022, 2023 and 2024 in the dark grey tabs. The main database covers our supply forecasts across 140 LNG facilities and projects, other project parameters, and detailed notes.