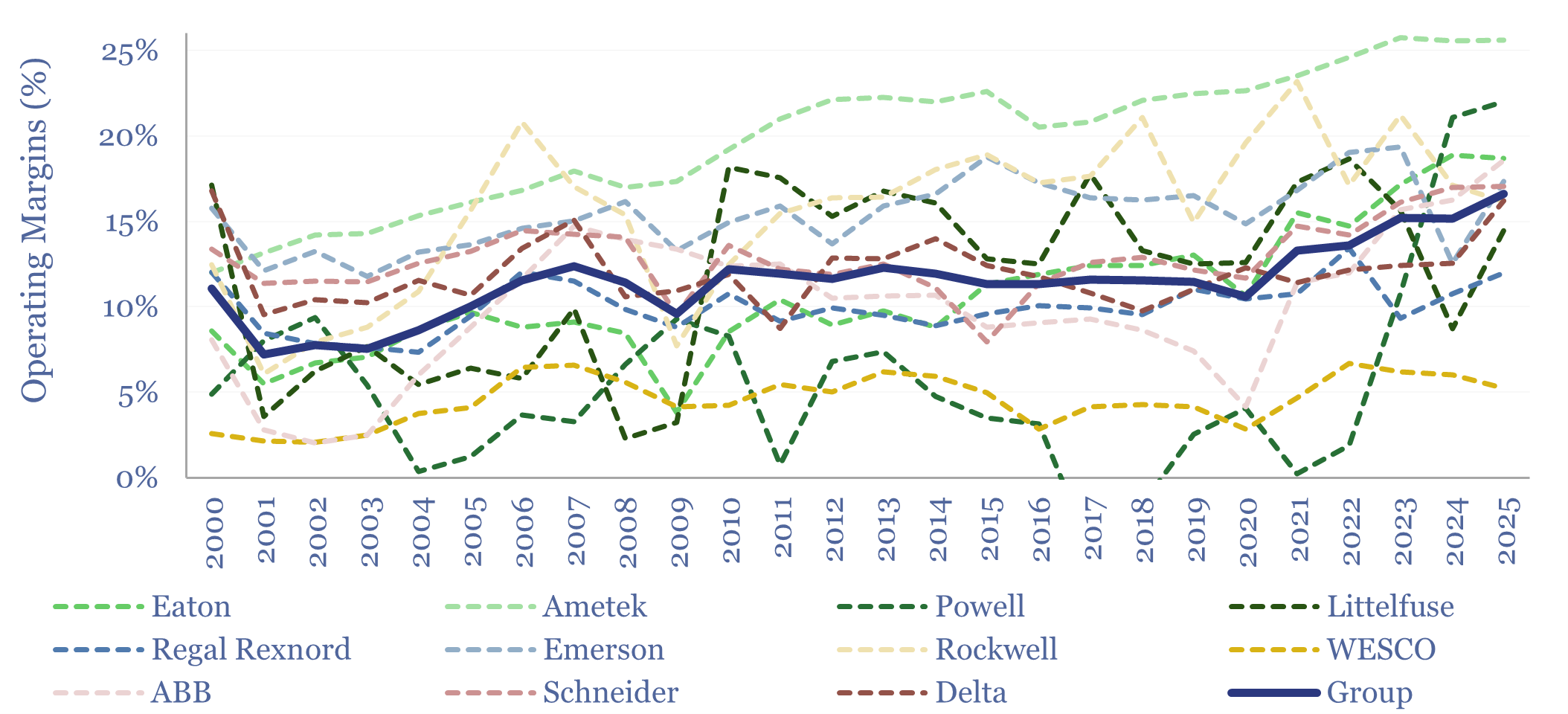

This data-file tracks power electronic capital goods company margins over time, rising from 10% in 2000-2010, to 12% in 2010-20 and then inflecting to a record 16% in 2025. The increase is mostly driven by higher- and medium-voltage categories, linked to re-accelerating load growth in the United States. Details on each company are in the data-file.

Power electronics capital goods companies tend to be industrial conglomerates, manufacturing thousands of SKUs, from low-voltage micro-electronics to high-voltage transmission equipment. Underlying components are discussed in our research into power electronics.

This data-file screens power electronics capital goods companies. In particular, we focused in on US-listed companies, with consistent reporting, running back at least 25-years, to see how operating margins and returns on capital have evolved.

Our screen includes Eaton, Emerson, Ametek, Rockwell, WESCO, Littelfuse, Powell and Regal Rexnord. On the companies tab, we have included a short overview of each company, summarizing its size, revenue mix and a breakdown of the businesses’ segments and product lines.

The average operating margin for power electronics capital goods companies has risen steadily, from 10% in the 2000s, to 12% in the 2010s, tripping lower during recessions such as 2009 and 2020, but then rising rapidly from 2021 to 2025.

In aggregate, power electronic capital goods companies’ margins are running at record levels in 2025. This is driven, in particular, by margins for high-voltage and medium-voltage switchgear, linked to US reindustrialization and broader US load growth.

Amazingly, Eaton’s market cap has trebled since our 2022 deep-dive into its SKUs. But the sharpest margin increase has occurred for Powell, which specializes in engineered-to-order electrical distribution systems, at medium voltage, especially for the power control rooms of energy- and industrial infrastructure, from chemicals plants to LNG facilities.

Our 2025 research has wondered about slowing electrification initiatives linked to energy transition, and faster momentum for instrumentation and controls that will help AI get deployed across the industrial eco-system. Hence we have explored case studies from Emerson and case studies from Rockwell.

Operating margins and returns on capital have not yet increased for the power electronic capital goods companies in our screen that are focused on instrumentation and controls, such as Emerson and Rockwell. We will be tracking the deployment of AI across the industrial eco-system in our ongoing research.