This page aggregates all of our research into Eni, in chronological order. The research notes or data-files here specifically discuss Eni and its exposure to themes in the energy transition. Another goal is to identify challenges and opportunities for Eni in the energy transition.

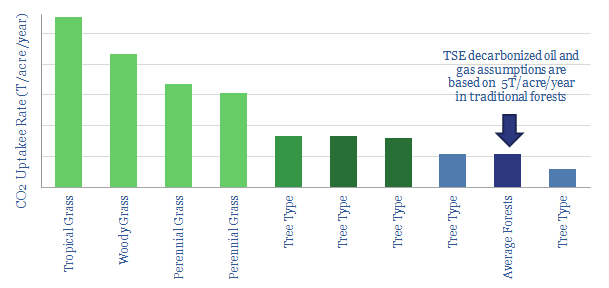

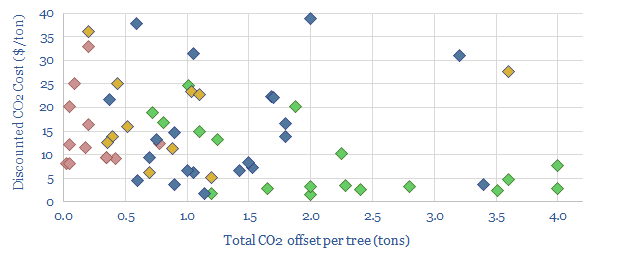

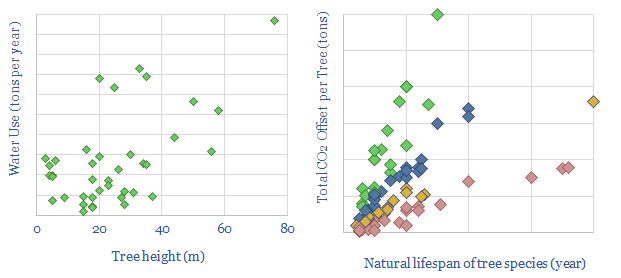

Nature-based solutions are among the most effectiveways to abate CO2. Forest offsets will cost $2-50/ton, decarboning liquid fuels for <$0.5/gallon and natural gas for <$1/mcf (chart below).

The data-file tabulates hundreds of data-points from technical papers and industry reports on different tree and grass types. It covers their growing conditions, survival rates, lifespans, rates of CO2 absorption (per tree and per acre) and their water requirements (examples below).

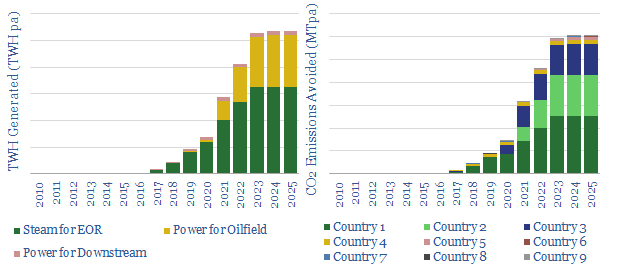

This data-file tabulates 20 solar projectsbeing undertaken within the oil industry, in order to clean up production and reduce emissions. More projects are needed, as the total inventory will obviate <1% of oil industry CO2 by 2025.

For each project, we estimate total TWH of power generation per annum, the CO2 emissions avoided, the timeline; and we also summarize the project details.

Leading examplesinclude the use of concentrated solar for steam-EOR in Oman and California, Solar PV in the Permian, and leading efforts from specific companies: such as Occidental, Shell, Eni and other Majors.

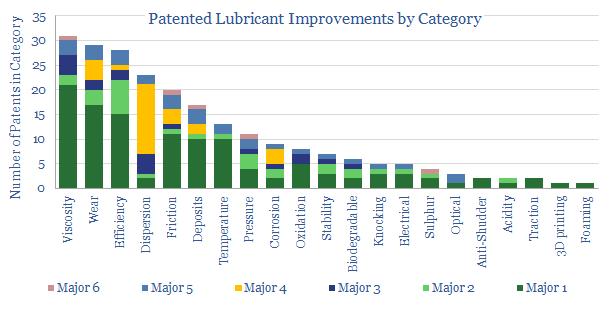

This data-file presents our “top five” conclusions on the lubricants industry, after reviewing 240 patents, filed by the Oil Majors in 2018. The underlying data on each of the 240 patents is also shown in the ‘LubricantPatents’ tab.

We are most impressed by the intense pace of activity to improve engine efficiencies(chart above), across over 20 different categories. As usual, we think technology leadership will drive margins and market shares. ‘Major 1’ stands out, striving hardest to gain an edge, by a factor of 2x. ‘ Major 2 has the ‘greenest’ lubricant patents, across EVs and bio-additives. Major 4 has the single most intriguing new technology in the space.

The relative number of patents into Electric Vehicle Lubricants is also revealing. It shows the Majors’ true attitudes on electrification, in a context where they are incentivised to sell new products into the EV sector. Our lubricant demand forecasts to 2050 are also noted.

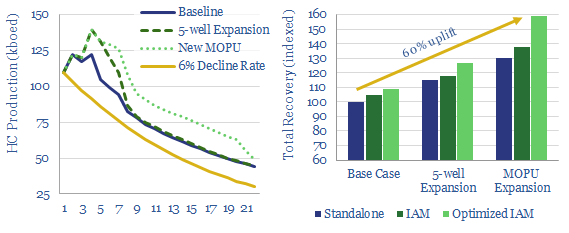

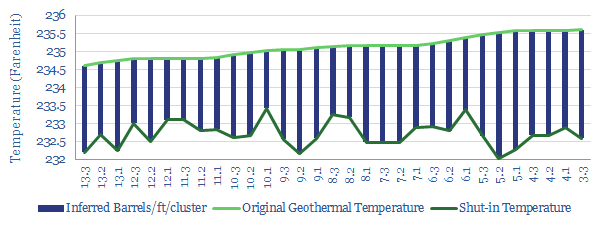

Advanced reservoir modelling can stave off production declinesat complex offshore assets. This data-file illustrates how, tabulating production estimates based on a technical paper published by Eni, an industry leader in applying high-speed computing power in its upstream operations.

Specifically, the paper simulates an offshore field-cluster in a single, Integrated Asset Model that covers 31 wells, drilled into 3 reservoirs (each is modelled in detail, with a total of 1.9M reservoir cells), 34 pipes, 4 oil platforms and 3 delivery points. Each iteration of this model takes an average of 3.5-hours to run.

Production can be uplifted by 60% according to the simulation, both in terms of EUR and in terms of year 5-7 production rate. 9pp of the uplift is achieved by simple reservoir optimisation. Another 21pp of uplift is achieved by identifying the key bottleneck, and building a new separation & boosting platform to alleviate it. A further 29pp of uplift comes from optimising the development plan for the new platform.

Emerging digital technologies appear to be keeping LT oil-markets better supplied than many expect, with production upside for the industry’s technology-leaders.

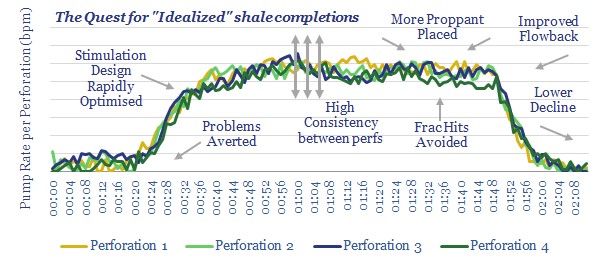

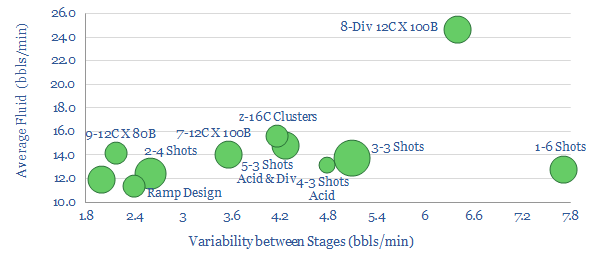

Completing a shale well depends on over 40 variables. Each one can be optimised using data. It follows that next-generation data could deliver next-generation shale productivity.

This note focuses on the most exciting new data methodologywe have seen across the entire shale space: distributed acoustic sensing (DAS) using fiber-optic cables. It has now reached critical mass.

DAS will have six transformational effectson the shale industry. Leading operators and service companies are also assessed.

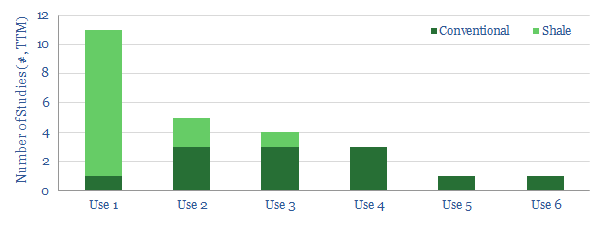

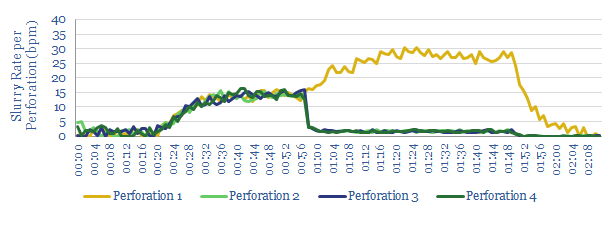

This data-file summarises 25 of the most recent technical papers around the industry, using fiber-optic cables for Distributed Acoustic Sensing (DAS). The technology is hitting critical mass to spur shale productivity upwards.

For each study, our data-file tabulates the company involved, the country of application, the specific purpose and a short summary of findings.

Technical data are also tabulated from some of these papers, including for warm-back analysis, perforation design and cluster flow-allocations.

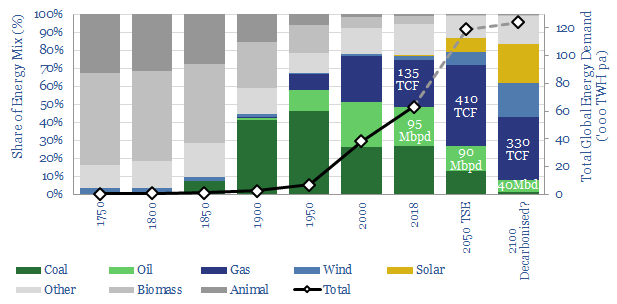

There is only one way to decarbonise the energy system: leading companies must find economic opportunities in better technologies. No other route can source sufficient capital to re-shape such a vast industry that spends c$2trn per annum. We outline seven game-changing opportunities. Leading energy Majors are already pursuing them in their portfolios, patents and venturing. Others must follow suit.

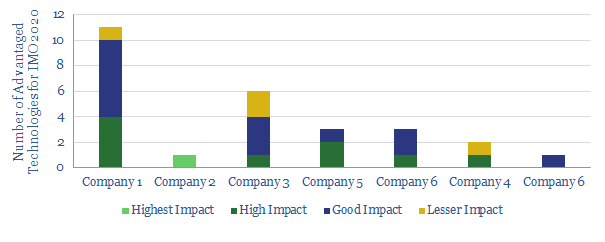

So far we have reviewed 450 patents in the downstream oil and gas industry (ex-chemicals). A rare few prompted an excited thought — “that could be useful when IMO 2020 comes around”. Hence, this data-file summarises the top 25+ proprietary technologies we have seen to capitalise on the opportunity. They are summarised and “scored” by company.

We will also provide you with updates of this file, as we continue reviewing patents and technical papers.

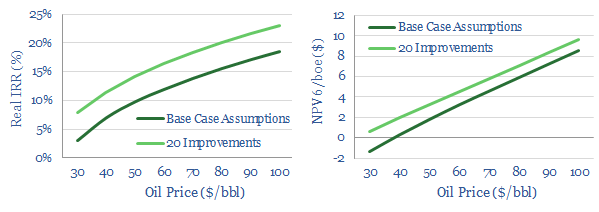

The appetite to invest in new offshore oil projects has been languishing, due to fears over the energy transition, a preference for share-buybacks, and intensifying competition from short-cycle shale. So can technology revive offshore and deep-water? This note outlines our ‘top twenty’ opportunities. They can double deep-water NPVs, add c4-5% to IRRs and improve oil price break-evens by $15-20/bbl.

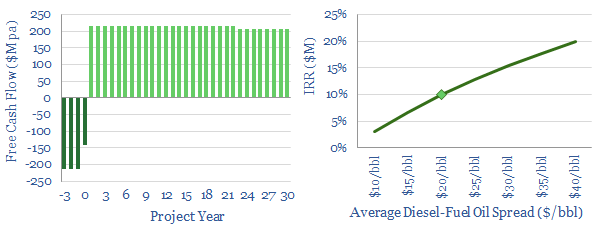

This data-file models the economics of Eni’s Slurry Technology, for hydro-converting heavy crudes and fuel oils into light products. It is among the top technologies we have reviewed for the arrival of IMO 2020 sulfur regulation, achieving >97% conversion of heavy fractions. The catalyst is stable and handles even ultra-heavy inputs. We see 10-20% IRRs at $20-40/bbl upgrading spreads. The data-file also summarises EST’s adoption in refineries to-date, future plans, and technical details of the EST process.

Cookies?

This website uses necessary cookies. Our cookies are simply to improve your experience. We do not undertake any advertising or targeting via our cookies. By clicking 'accept' or continuing to use the website, you consent to our use of cookies.AcceptRead More

Privacy & Cookies Policy

Privacy Overview

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.