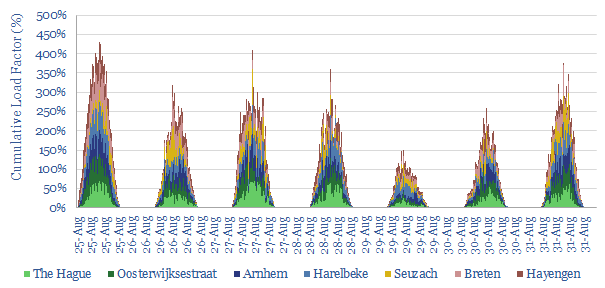

Inter-correlations between solar assets?

…15-min by 15-min output is 60-80% correlated, which is even greater than for offshore wind (data here). These issues suggest solar can provide a meaningful portion of decarbonizing grids, but…

the research consultancy for energy technologies

…15-min by 15-min output is 60-80% correlated, which is even greater than for offshore wind (data here). These issues suggest solar can provide a meaningful portion of decarbonizing grids, but…

…deflation’ for many renewables technologies, as there are many line items re-inflating in our models. We will continue to look for opportunities in power-electronics and materials. https://thundersaidenergy.com/2021/07/29/offshore-wind-will-costs-follow-moores-law/ https://thundersaidenergy.com/2021/06/10/solar-costs-four-horsemen/ https://thundersaidenergy.com/2021/07/15/lithium-reactive/ https://thundersaidenergy.com/downloads/energy-transition-leading-commodities/…