-

Nature based CO2 removals: theory of evolution?

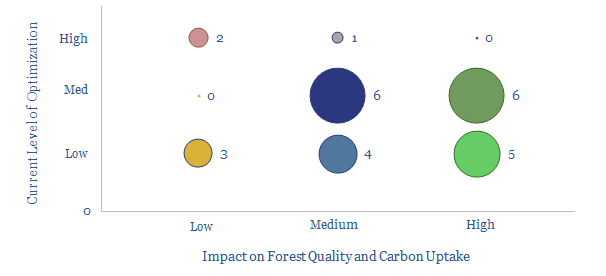

Learning curves and cost deflation are widely assumed in new energies but overlooked for nature-based CO2 removals. Support for NBS has already stepped up sharply in 2021. This 15-page note finds the CO2 uptake of well-run reforestation projects could double again.

-

Integrated energy: a new model?

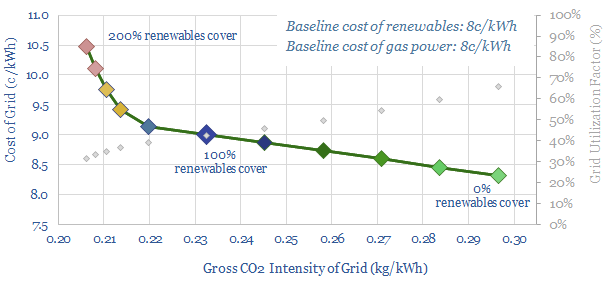

This 14-page note lays out a new model to supply fully carbon-neutral energy to a cluster of commercial and industrial consumers, via an integrated package of renewables, low-carbon gas back-ups and nature based carbon removals. This is remarkable for three reasons: low cost, high stability, and full technical readiness.

-

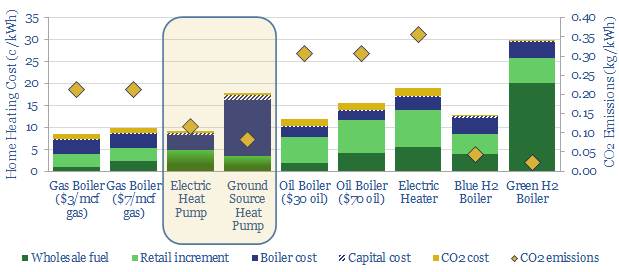

Heat pumps: hot and cold?

Some policymakers now aspire to ban gas boilers and ramp heat pumps 10x by 2050. In theory, the heat pump technology is superior. But in practice, there are ten challenges. It could become a political disaster. The most likely outcome is a 0-2% pullback in European gas by 2030.

-

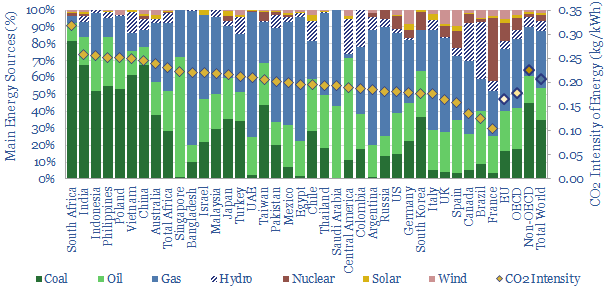

Border taxes: a carbon curtain has descended?

Europe has proposed a ‘border adjustment mechanism’ to mitigate carbon leakage. Its initial formulation is modest. But it will snowball. And ultimately divide the global economy in two. This 15-page report lays out our top five predictions for CO2 border taxes to reshape energy markets and the world.

-

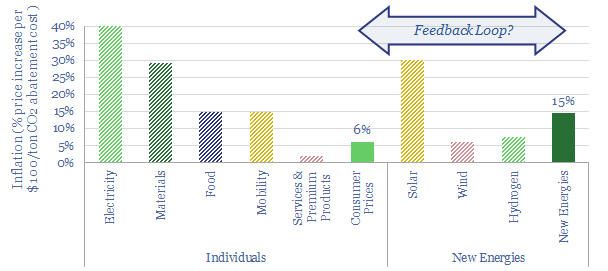

Inflation: will it de-rail the energy transition?

New energy policies will exacerbate inflation in the developed world, raising price levels by 20-30%. Or more, due to feedback loops. We find this inflation could also cause new energies costs to rise over time, not fall. As inflation concerns accelerate, policymakers may need to choose between delaying decarbonization or lower-cost transition pathways.

-

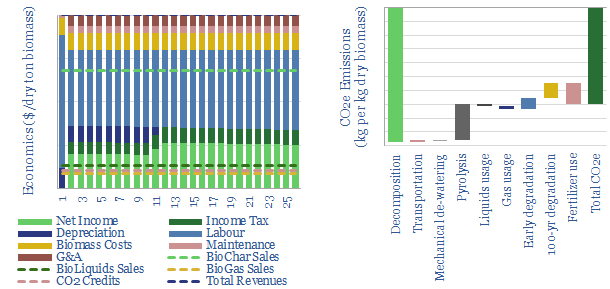

Biochar: burnt offerings?

Biochar is a miraculous material, improving soils, enhancing agricultural yields and avoiding 1.4kg of net CO2 emissions per kg of waste biomass. IRRs surpass 20% without CO2 prices or policy support. Hence this 18-page note outlines the opportunity.

-

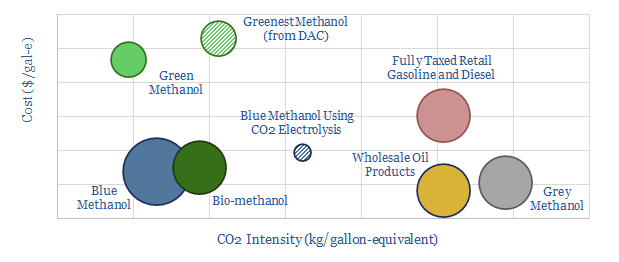

Methanol: the next hydrogen?

Methanol is becoming more exciting than hydrogen as a clean fuel to help decarbonize transport. Specifically, blue methanol and bio-methanol are 65-75% less CO2-intensive than oil products, while they already earn 10% IRRs at c$3/gallon prices. Unlike hydrogen, it is simple to transport and integrate methanol with pre-existing vehicles.

-

Biden presidency: our top ten research reports?

Joe Biden’s presidency will prioritize energy transition among its top four focus areas. Thus we present our top ten pieces of research that gain increasing importance as the new landscape unfolds. We are cautious on bubbles and supply shortages. But decision-makers will become more discerning around CO2.

-

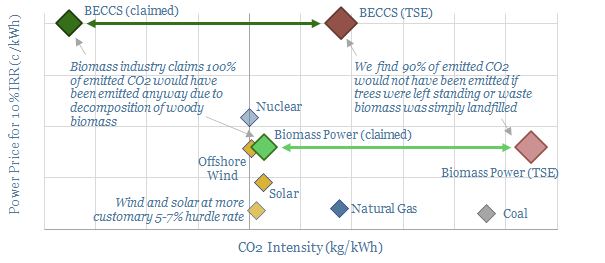

Biomass and BECCS: what future in the transition?

20% of Europe’s renewable electricity currently comes from biomass, mainly wood pellets, burned in facilities such as Drax’s, 2.6GW Yorkshire plant. But what are the economics and prospects for biomass power as the energy transition evolves? This 18-page analysis leaves us cautious.

-

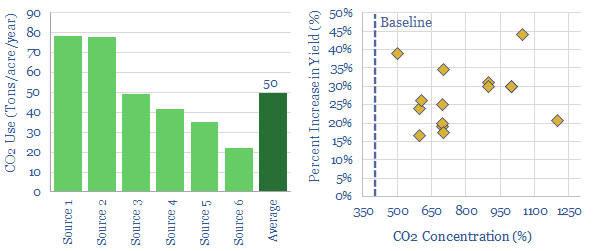

Greenhouse gas: use CO2 in agriculture?

Enhancing CO2 in greenhouses can improve yields by c30%. It costs $4-60/ton to supply this CO2, while $100-500/ton of value is unlocked. The challenge is scale, limited to 50MTpa globally. Around 50Tpa of CO2 is supplied to each acre of greenhouses. But only c10% is sequestered.

Content by Category

- Batteries (87)

- Biofuels (42)

- Carbon Intensity (49)

- CCS (63)

- CO2 Removals (9)

- Coal (38)

- Company Diligence (92)

- Data Models (822)

- Decarbonization (159)

- Demand (110)

- Digital (58)

- Downstream (44)

- Economic Model (200)

- Energy Efficiency (75)

- Hydrogen (63)

- Industry Data (275)

- LNG (48)

- Materials (81)

- Metals (74)

- Midstream (43)

- Natural Gas (146)

- Nature (76)

- Nuclear (23)

- Oil (162)

- Patents (38)

- Plastics (44)

- Power Grids (124)

- Renewables (149)

- Screen (112)

- Semiconductors (30)

- Shale (51)

- Solar (67)

- Supply-Demand (45)

- Vehicles (90)

- Wind (43)

- Written Research (347)