Joe Biden’s presidency will prioritize energy transition among its top four focus areas. Below we present our top ten pieces of research that gain increasing importance as the new landscape unfolds. We are cautious that aggressive subsidies may stoke bubbles and supply shortages in the mid-2020s. Decisions-makers will become more discerning of CO2. As usual, we focus on non-obvious opportunities.

(1) Kingmaker? There are two policy routes to accelerate the energy transition. An escalating CO2 tax could decarbonize the entire US by 2050, for a total abatement cost of $75/ton, while unlocking $3.5trn of investment. The other approach is with subsidies. This is likely to be Biden’s preferred approach. However, giving subsidies to a select few technologies tends to crowd out progress elsewhere. Who gets the subsidies is arbitrary, and thus ensues a snake-pit of lobbying. It is also more expensive, with some subsidies today costing $300-600/ton. Finally, subsidies will only achieve limited decarbonization on our models. Our 14-page note outlines these ideas and backs them up with data, to help you understand the policy landscape we are entering.

(2) Bubbles? The most direct risk of aggressive subsidies is that we fear they will stoke bubbles in the energy transition. Specifically, we have argued a frightening resemblance is appearing between prior and notorious investment bubbles (from Dutch tulips to DotCom stocks) and many of the best-known decarbonization themes today. It is driven by an expectation that government policies will grow ever more favorable, thus technical and economic challenges are being overlooked. Our 19-page note evaluates the warning signs, theme by theme, to help you understand where bubbles may be likely to build and later burst.

(3) Overbuilding renewables is a potential bubble. Our sense is that Biden’s policy team prefers to subsidize renewables today and defer the resultant volatility issues for later. But eventually, we model that this will result in power grids becoming more expensive and more volatile, which could end up having negative consequences, both for consumers and industrial competitiveness. More interestingly, we find expensive and volatile grids have historically motivated installations of combined heat and power systems behind the meter, which can also cut CO2 emissions by 6-30% compared to buying power from the grid, at 20-30% IRRs. The reason is that CHPs capture and use waste heat. Thus they achieve c70-80% thermal efficiencies, where simple cycle gas turbines only achieve c40%. The theme and opportunity are therefore explored in our 17-page note below.

(4) Over-building electric vehicles? Subsidies for EVs are also more likely under a Biden presidency. This is widely expected to destroy fossil fuel demand. Indeed a vast scale-up of EVs is present in our oil demand forecasts helping global oil demand to peak in 2023. However, our 13-page note finds this electrical vehicle ramp-up will actually increase net fossil fuel demand by +0.7Mboed from 2020-35, with gains in gas exceeding losses of oil. The reason is that manufacturing each EV battery consumes 3.7x more energy than the EV displaces each year. So there is an energy deficit in early years. But EV sales are growing exponentially, so the energy costs to manufacture ever more EVs each year outweighs the energy savings from running previous years’ EVs until the EV sales rate plateaus.

(5) Under-investment in fossil fuels? A sticking point in the presidential debates was whether President Biden would ban fracking. An impressive understanding of the energy industry was shown by his response that instead “we need a transition”. However, some have commentators continued fearmongering. We think the fearmongering is overdone. Nevertheless, at the margin, Biden’s presidency may reduce investment appetite for oil and gas. In turn, this would exacerbate the shortages we are modelling in the 2020s. A historical analogy is explored in our 8-page note, which looks back at whale oil, a barbaric lighting fuel from the 19th century. Amidst the transition to kerosene and electric lighting, whale oil supply peaked long before whale oil demand, causing strong price performance for whale oil itself, and very strong price performance for by-products such as whale bone.

(6) Under-investment in oil? Our oil market outlook in 2021-25 is published below. New changes include downward revisions to US shale supplies (particularly from 2022), increased chances of production returning in Iran, and increased production from Saudi Arabia and Russia to compensate for lower output in the US. Steep under-supply is seen in 2022, over 1Mbpd, even after OPEC has exited all production cuts. Restoring market balance in 2024-25 requires incentivizing an 8Mbpd shale scale-up. We do not believe Biden’s policies will block this shale ramp, but they may help its incentive costs re-inflate by c$5-15/bbl, particularly if Trump-era tax breaks are reversed.

(7) Under-investment in gas? Where US shale growth slows, there is clearly going to be less associated gas available to feed US LNG facilities. But there may also be a lower investment appetite to construct US LNG facilities. This matters because our 12-page note below finds gas shortages are likely to be a bottleneck on decarbonization in Europe, which compounds our fears that Europe’s own decarbonization objectives could need to be walked back. Specifically, Europe must attract another 85MTpa of global LNG supplies before 2030 to meet the targets shown on the chart. This is one-third of the 240MTpa risked LNG supply growth due to occur in the 2020s, of which 100MTpa is slated to come from the United States. There is no change to our numbers yet.

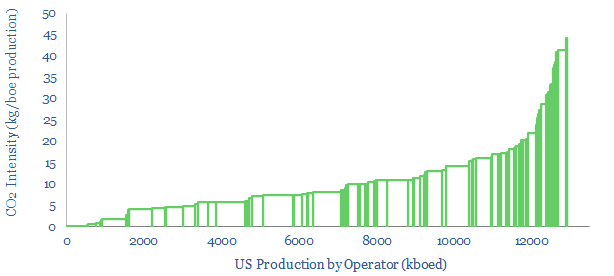

(8) Lower carbon beats higher carbon? We are not fearmongering that oil and gas investment will stall under a Biden presidency. But we do believe that investment in all carbon-intensive sectors will proceed somewhat more discerningly than it would have under Trump. Low-carbon producers will be more advantaged in attracting capital, while higher-carbon producers will be penalized with higher capital costs and lower multiples. In order to help you rank different operators, we have assembled a data-file covering 13Mboed of production from major US basins, operator-by-operator (below and here) alongside our broader screens of CO2 intensity, which span across 30 different sectors, such as LNG plants, refineries, chemical facilities, cement and biofuels (here).

(9) Mitigating methane? Biden’s presidency will likely re-strengthen the EPA. Our hope is that this will accelerate the industry’s assault on leaking methane, which is a 25-120x more powerful greenhouse gas than CO2. Methane accounts for 25-30% of all man-made warming, of which c25% derives from the oil and gas industry. If 3.5% of gas is leaked across the value chain, then debatably gas is no greener than coal (the number is less than 1% in the US but can be greatly improved). Our 23-page note evaluates the best emerging technology options to mitigate methane. We are excited by replacing high-bleed pneumatics, as profiled in our short follow-up note (also below). We also see shale operators accelerating their quest for ‘CO2-neutral’ production (note below).

(10) The weatherization of 2M homes is a central part of Joe Biden’s proposed energy policy. Hence we created a data-file assessing the costs and benefits of different options. The most cost-effective way to lower home heating bills is smart thermostats. They can cut energy use c18%. Leading providers include Nest (Google), Honeywell, Emerson, Ecobee. Second most cost-effective is sealing air leaks. GE Sealants is #1 by market share in silicone sealants. Advanced plastics would also see a modest boost in demand. More questionable are large and expensive construction projects, which appear to have larger up front costs and abatement costs per ton of CO2.