-

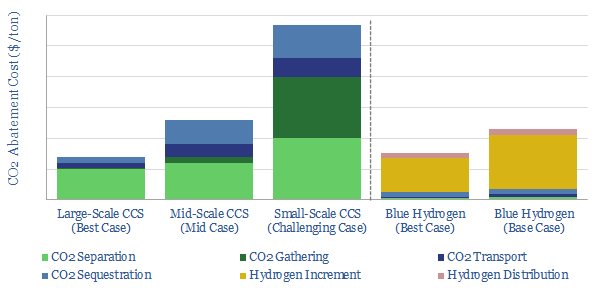

Deep blue: cracking the code of carbon capture?

Carbon capture is cursed by colossal costs at small scale. But blue hydrogen may be its saviour. Crucial economies of scale are guaranteed by deploying both technologies together. The combination is a dream scenario for gas producers. This 22-page note outlines the opportunity and costs.

-

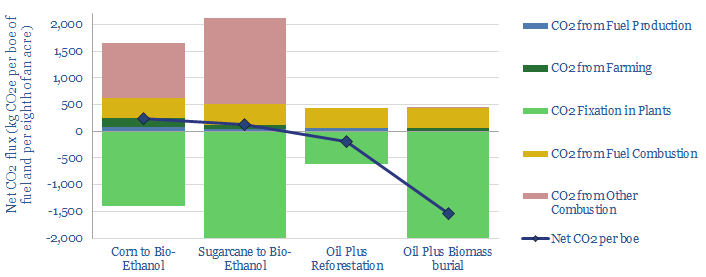

Biofuels: better to bury than burn?

The global bioethanol industry could be disrupted by a carbon price. Somewhere between $15-50/ton, it becomes more economical to bury the biofuel crop, rather than convert it into biofuels. This would remove 8x more CO2 per acre, at a lower total cost. Ethanol mills and blenders would be displaced.

-

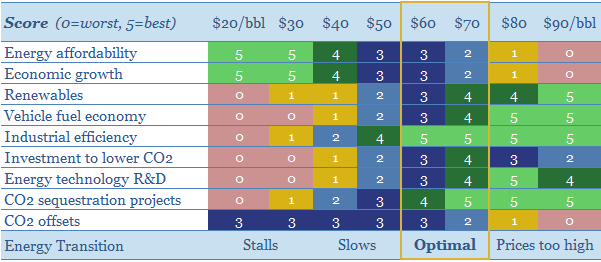

What oil price is best for energy transition?

$30/bbl oil prices stall the energy transition. They kill the relative economics of electric vehicles, renewables, industrial efficiency, flaring reductions, CO2 sequestration and new energy R&D. This 15-page note finds $60/bbl oil is ‘best’ for decarbonization. Policymakers should target $60 oil.

-

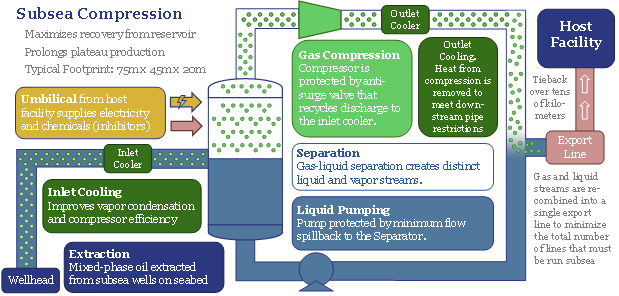

The future of offshore: fully subsea?

Offshore developments will change dramatically in the 2020s, eliminating production platforms in favour of fully subsea solutions. The opportunity increases a project’s NPV by 50% and effectively eliminates upstream CO2. We reviewed 1,850 patents to find the best-placed operators and services. Others will be disrupted. The theme supports the ascent of low-carbon natural gas.

-

Ten Themes for Energy in the 2020s

We presented our ‘Top Ten Themes for Energy in the 2020s’ to an audience at Yale SOM, in February-2020. The audio recording is available below. The slides are available to TSE clients.

-

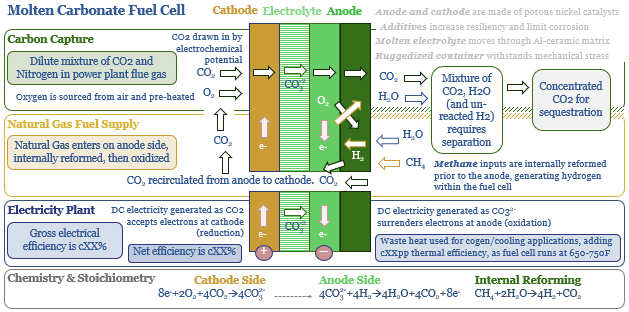

MCFCs: what if carbon capture generated electricity?

Molten carbonate fuel cells (MCFCs) could be a game-changer for CCS and fossil fuels. They capture CO2 from combustion facilities; while at the same time, generating electricity from natural gas. The first pilot plant is being tested in 1Q20, by ExxonMobil and FuelCell Energy. Economics range from passable to phenomenal.

-

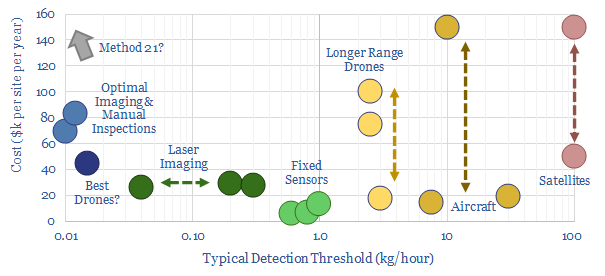

Global gas: catch methane if you can?

Scaling up natural gas is among the largest decarbonisation opportunities. But this requires minimising methane leaks. Exciting new technologies are emerging. This 28-page note ranks producers, positions for new policies and advocates developing more LNG. To seize the opportunity, we also identify 35 companies geared to the theme. Global gas demand will not be derailed…

-

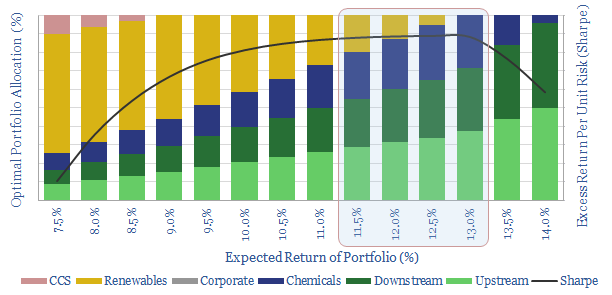

Ramp Renewables? Portfolio Perspectives.

It is often said that Oil Majors should become Energy Majors by transitioning to renewables. But what is the best balance based on portfolio theory? We constructed a mean-variance optimisation model and find a c5-13% weighting to renewables best increases risk-adjusted returns. Beyond 35%, returns decline rapidly.

-

CO2-Labelling for an Energy Transition?

CO2-labelling is the most important policy to accelerate the energy transition: making products’ CO2-intensities visible, so they can sway purchasing decisions. Expect 4-8% savings across global energy, which will lower the net costs of decarbonisation by $200-400bn pa. Digital technologies also support wider eco-labelling compared. Leading companies are preparing their businesses.

-

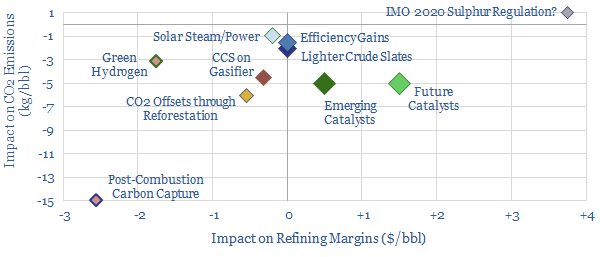

Decarbonise Downstream?

Refining has the highest carbon footprint in global energy. Next-generation catalysts are the best opportunity for improvement: uniquely, they could cut refineries’ CO2 by 15-30%, while also uplifting margins, which get obliterated by other decarbonisation approaches. Catalyst science is undergoing a digitally driven transformation. Hence this 25-page note outlines a new ESG opportunity around refining…

Content by Category

- Batteries (87)

- Biofuels (42)

- Carbon Intensity (49)

- CCS (63)

- CO2 Removals (9)

- Coal (38)

- Company Diligence (92)

- Data Models (822)

- Decarbonization (159)

- Demand (110)

- Digital (58)

- Downstream (44)

- Economic Model (200)

- Energy Efficiency (75)

- Hydrogen (63)

- Industry Data (275)

- LNG (48)

- Materials (81)

- Metals (74)

- Midstream (43)

- Natural Gas (146)

- Nature (76)

- Nuclear (23)

- Oil (162)

- Patents (38)

- Plastics (44)

- Power Grids (124)

- Renewables (149)

- Screen (112)

- Semiconductors (30)

- Shale (51)

- Solar (67)

- Supply-Demand (45)

- Vehicles (90)

- Wind (43)

- Written Research (347)