-

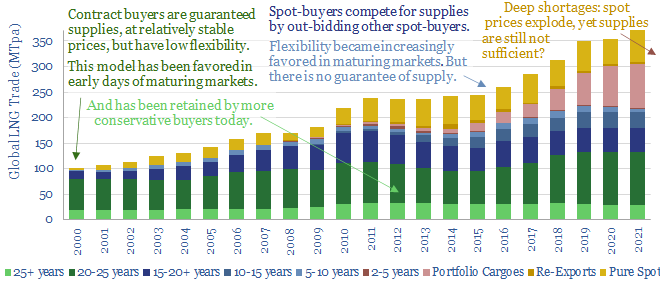

Energy security: the return of long-term contracts?

Spot markets have delivered more and more ‘commodities on demand’. But is this model fit for energy transition? Many markets are now short, causing explosive price rises. Sufficient volumes may still not be available at any price. This note considers a renaissance for long-term contracts.

-

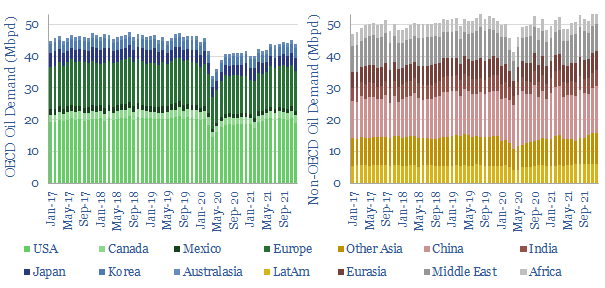

Global oil demand: rumors of my death?

‘Rumors of my death have been greatly exaggerated’. Mark Twain’s quote also applies to global oil consumption. This note aggregates demand data for 8 oil products and 120 countries over the COVID pandemic. We see 3.5Mbpd of pent-up demand ‘upside’, acting as a floor on medium-term oil prices.

-

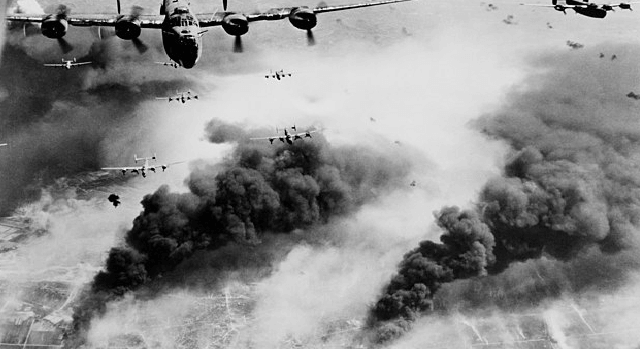

Oil and War: ten conclusions from WWII?

The second world war was decided by oil. Each country’s war-time strategy was dictated by its availability, quality and attempts to secure more of it, including by rationing non-critical uses of it. Ultimately, halting the oil meant halting the war. Today’s short note outlines out top ten conclusions from reviewing the history.

-

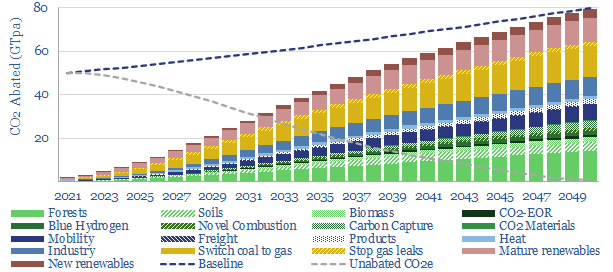

Decarbonizing global energy: the route to net zero?

This 18-page report revises our roadmap for the world to reach ‘net zero’ by 2050. The average cost is still $40/ton of CO2, with an upper bound of $120/ton, but this masks material mix-shifts. New opportunities are largest in efficiency gains, under-supplied commodities, power-electronics, conventional CCUS and nature-based CO2 removals.

-

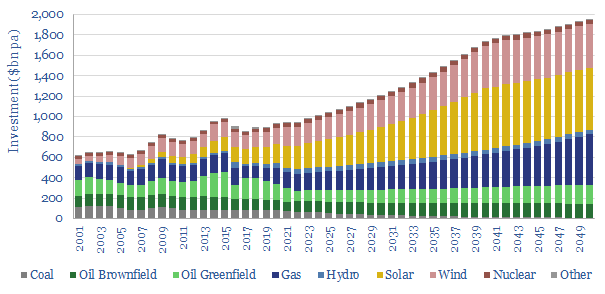

Is the world investing enough in energy?

Global energy investment in 2020-21 has been running 10% below the level needed on our roadmap to net zero. Under-investment is steepest for solar, wind and gas. Under-appreciated is that each $1 dis-invested from fossil fuels must be replaced with $25 in renewables. Future capex needs are vast.

-

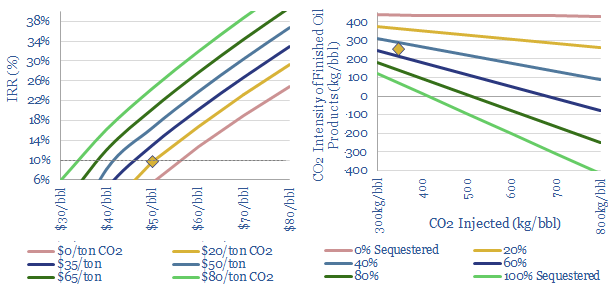

CO2-EOR: well disposed?

CO2-EOR is the most attractive option for large-scale CO2 disposal. Unlike CCS, which costs over $70/ton, additional oil revenues cover the costs of sequestration. And the resultant oil is 50-100% lower carbon than usual. The technology is mature. Potential exceeds 2GTpa. This 23-page report outlines the opportunity.

-

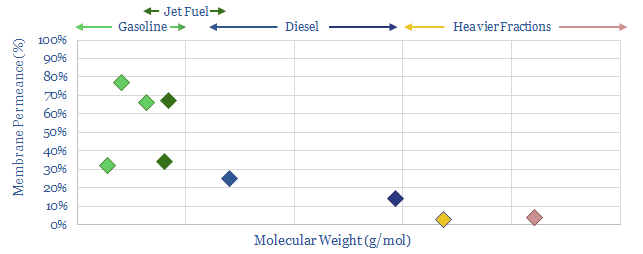

Low-carbon refining: insane in the membrane?

1% of global CO2 comes from distilling crude oil at refineries. An alternative uses precisely engineered polymer membranes to separate crude fractions, eliminating 50-80% of the costs and 97% of the CO2. We reviewed 1,000 patents, including a major breakthrough in 2020. This 14-page note presents the opportunity.

-

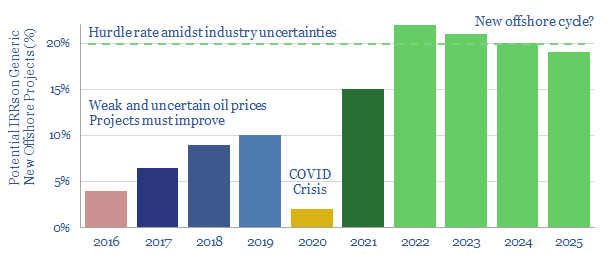

Turning the tide: is another offshore cycle brewing?

Oil markets look primed for a new up-cycle by 2022, which could culminate in Brent surpassing $80/bbl. This is sufficient to unlock 20% IRRs on the next generation of offshore projects, and thus excite another cycle of offshore exploration and development. We address potential pushbacks to the thesis and outlines who benefits.

-

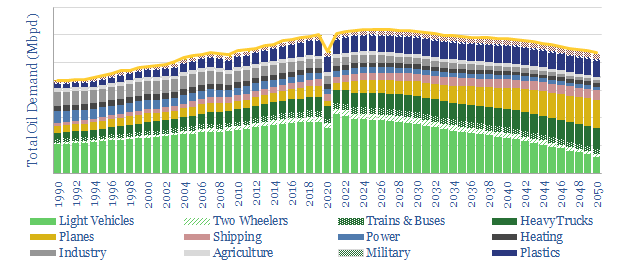

On the road: long-run oil demand after COVID-19?

Another impact of COVID-19 may still lie ahead: a 1-2Mbpd upwards jolt in global oil demand. This 17-page note upgrades our 2022-30 oil demand forecasts by 1-2Mbpd above our pre-COVID forecasts. The increase is from road fuels, reflecting lower mass transit, lower load factors and resultant traffic congestion.

-

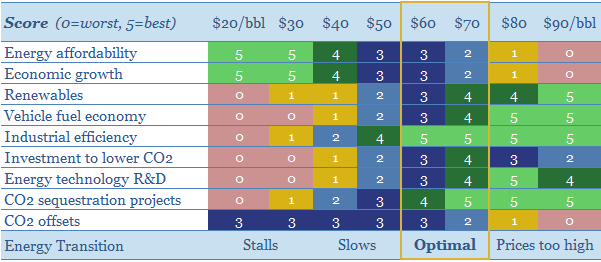

What oil price is best for energy transition?

$30/bbl oil prices stall the energy transition. They kill the relative economics of electric vehicles, renewables, industrial efficiency, flaring reductions, CO2 sequestration and new energy R&D. This 15-page note finds $60/bbl oil is ‘best’ for decarbonization. Policymakers should target $60 oil.

Content by Category

- Batteries (87)

- Biofuels (42)

- Carbon Intensity (49)

- CCS (63)

- CO2 Removals (9)

- Coal (38)

- Company Diligence (90)

- Data Models (816)

- Decarbonization (159)

- Demand (108)

- Digital (56)

- Downstream (44)

- Economic Model (197)

- Energy Efficiency (75)

- Hydrogen (63)

- Industry Data (273)

- LNG (48)

- Materials (79)

- Metals (71)

- Midstream (43)

- Natural Gas (146)

- Nature (76)

- Nuclear (22)

- Oil (162)

- Patents (38)

- Plastics (44)

- Power Grids (123)

- Renewables (149)

- Screen (112)

- Semiconductors (30)

- Shale (51)

- Solar (67)

- Supply-Demand (45)

- Vehicles (90)

- Wind (43)

- Written Research (345)