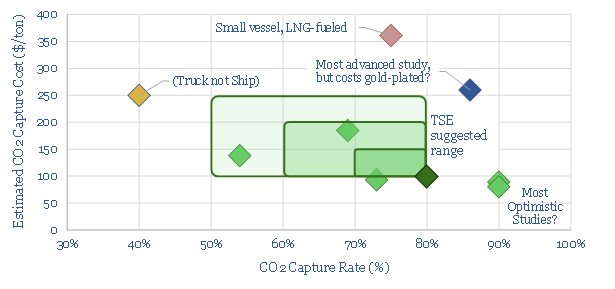

CCS is adapting to ‘go to sea’. 80% of some ships’ CO2 emissions could be captured for a cost of c$100/ton and an energy penalty of just 5%, albeit this is the best case within a broad range. This 15-page note explores the opportunity, challenges, progress and who might benefit.

Different options to decarbonize the shipping industry are compared and contrasted on pages 2-4, including the abatement costs of different blue and green fuels.

But what about CCS? The technology is mature. However, CCS on a ship would have different parameters from onshore. We discuss three key considerations on pages 5-7.

Will it actually work? The question is whether you can put an amine plant on a floating structure, store the CO2 as a liquid, and expect the entire system to function. We believe the answer is yes, based on reviewing technical papers, as summarized on 8-10.

$100/ton economics are possible. We use our models to outline what you need to believe to reach these numbers, including sensitivities, and applicability to different shipping types and routes (pages 11-12).

Which companies benefit? We explore implications for leading capital goods companies, chemicals companies and small-scale LNG on page 13.

A new infrastructure industry would also be required, to handle CO2 in ports, move it to disposal sites, or integrate with CO2-EOR. We discuss this theme on pages 14-15.

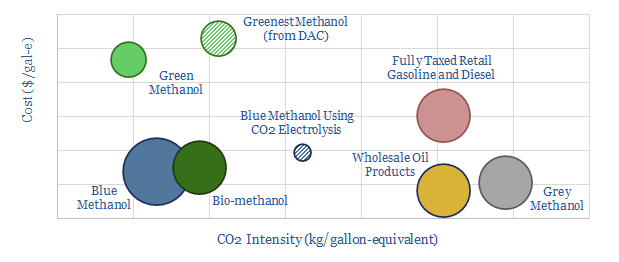

Methanol is becoming more exciting than hydrogen as a clean fuel to help decarbonize transport. Specifically, blue methanol and bio-methanol are 65-75% less CO2-intensive than oil products, while they can already earn 10% IRRs at c$3/gallon-equivalent prices. Unlike hydrogen, it is simple to transport and integrate methanol with pre-existing vehicles. Hence this 21-page note outlines the opportunity.

The objectives and challenges of hydrogen are summarized on pages 2-3. We show that clean methanol can satisfy the objectives without incurring the challenges.

An overview of the methanol market is given on pages 4-5, to frame the opportunity, particularly in transportation fuels and cleaner chemicals.

Conventional methanol production is described on 6-8. We focus upon the chemistry, the costs, the economics and the CO2 intensity.

Bio-methanol is modelled on pages 9-10. We also focus upon the costs, economics and CO2 intensity, including an opportunity for carbon-negative fuels.

Blue methanol is outlined on pages 11-15. Converting CO2 and hydrogen into methanol is fully commercial, based on recent case studies, which we also use to model the economics and CO2 credentials.

Green methanol is more expensive for little incremental CO2 reduction, and indeed some routes to green methanol production are actually higher-CO2 (pages 16-18).

Companies in the methanol value chain are profiled on pages 19-20. We focus upon leading incumbents, technology providers and private companies commercializing clean methanol.

Our conclusion is that methanol could excite decision-makers in 2021, the way that hydrogen excited in 2020. This thesis is spelled out on page 21.

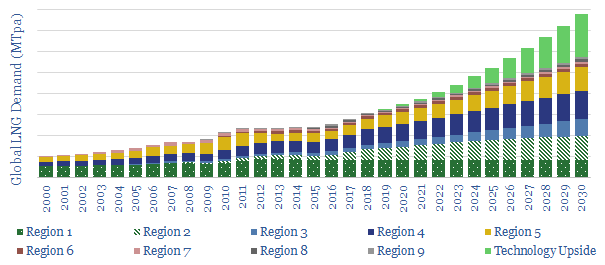

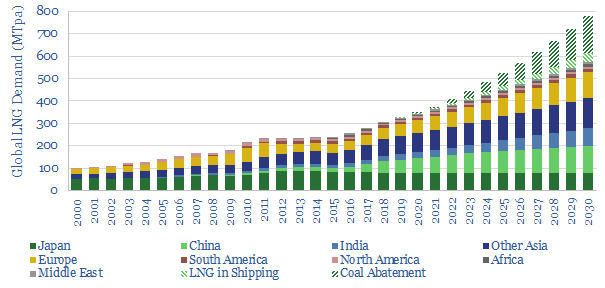

Gas demand could treble by 2050, gaining traction not just as the world’s cleanest fossil fuel, but also the most economical. The ascent would be driven by technology. Hence this note outlines 200MTpa of potential upside to consensus LNG demand, via de-carbonised power and shipping fuels. LNG demand could thus compound at 8% pa to 800MTpa by 2030, justifying greater investment in unsanctioned LNG projects.

[restrict]

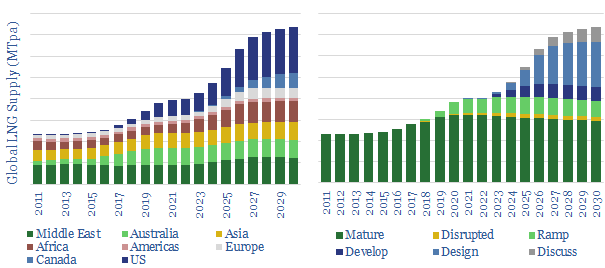

Consensus LNG demand?

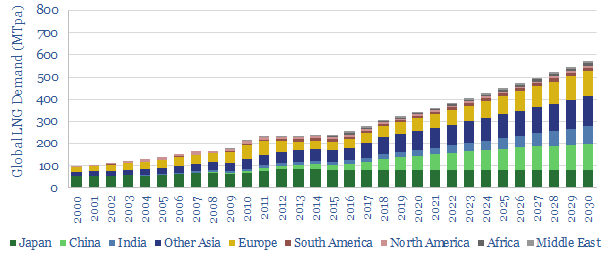

A simple model of global LNG demand is shown below (and downloadable here). It is created by extrapolating recent trends in key LNG-consuming regions. The total market grew at 5.7% pa in 2013-18. At a 5.4% forward CAGR, it would reach c570MTpa by 2030. These numbers are not far from other LNG forecasters’, and thus serve as a reasonable consensus.

What excites us is the potential for technology to accelerate LNG demand. Markets are slow to reflect technological breakthroughs. Hence these new demand sources likely do not feature in consensus forecasts yet. In our view, this makes them worthy of attention.

Upside from De-Carbonised Power Generation?

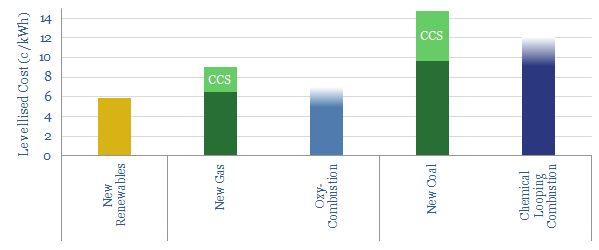

The first opportunity is in de-carbonised power generation, as we have discussed in our deep-dive report, ‘de-carbonising carbon‘. We think novel technologies are reaching maturity, which can generate cost-competitive electricity (chart below) alongside an exhaust stream of pure CO2, for use in industry or for immediate sequestration. The full details are in our report.

Let us now make some approximate calculations: The world consumes 7.7bn tons of coal per annum. In energy terms, this is equivalent to c165TCF of gas, or 3,300MTpa of LNG. We believe it would be economic, and achievable, to convert c5% of this coal power to gas by 2030. Converting it to decarbonised gas could save c1bn tons of CO2 emissions per annum. In turn, this could be achieved by 200GW of de-carbonised gas-power, in 500 x 400MW power plants, each burning c50mmcfd of input gas, fed by 165MTpa of LNG. This is the first area where technology can greatly accelerate LNG demand.

Upside in Shipping?

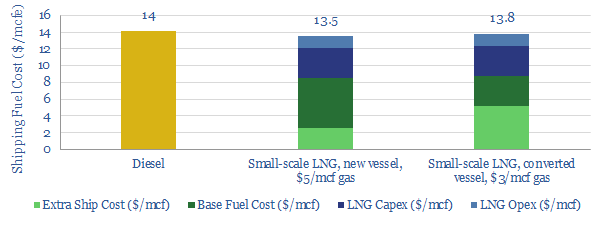

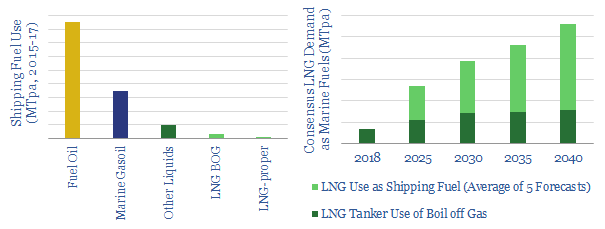

The second opportunity is in LNG as a shipping fuel, which will become increasingly economical after IMO 2020 sulphur regulations re-shape the marine sector. The economics are shown below and modelled here.

New technologies in small-scale LNG will accelerate adoption in smaller ports, moving beyond the large port-sizes required for bunkering. The technologies and economics are explored in detail, in our deep-dive note, LNG in Transport. The economics are modeled here. To assist, Shell is also pioneering new solutions for LNG in transport.

The upshot could be 40MTpa of incremental LNG demand in the maritime industry by 2030. This is the second area where technology can greatly accelerate LNG demand.

Less positive on trucking

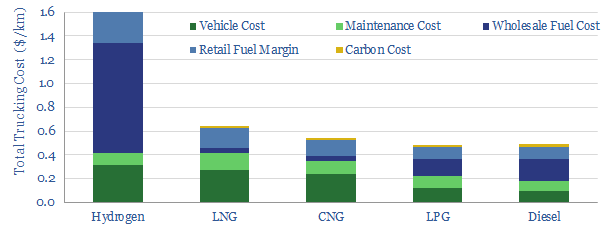

Is there further upside? One might expect, in an overview of LNG technologies, to find incremental upside in road vehicles: either directly in LNG-fired trucks, in gas-fired vehicles, or to produce hydrogen for fuel-cells. None of these opportunities are yet captured in our models.

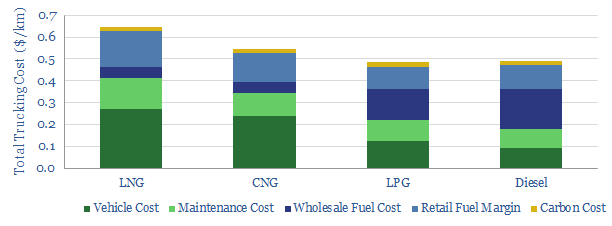

The reason is economics. Compared to diesel-powered trucks, we find compressed natural gas to be c10% more expensive, LNG to be 30% more expensive and hydrogen to be around 4x more expensive (model here, chart below). We also find hydrogen to be 85% costlier than gasoline, to powers cars in Europe (model here). In most cases, electrification is the better option, as superior vehicle concepts emerge.

Our numbers do not include any incremental LNG demand in the road-transportation sector. However, it is noteworthy that replacing 1Mbpd, or c2% of the world’s road fuels with LNG would consume an incremental 50MTpa of LNG. This could cushion delays or shortfalls in decarbonised gas-power.

Potential supplies can meet the challenge.

It is only possible for the world to consume 800MT of LNG in 2030 if it is also possible to supply 800MT. While our risked forecasts are for c600MT of LNG supply in 2030 (chart below), our numbers are including just c60% of the 230MTpa of LNG capacity that is currently in the design phase, and just 15% of the 180MTpa that is currently in the discussion phase. In a generous scenario, our forecasts rise close to the 800MTpa level that is required. Please download our risked, LNG supply model to see our scenarios, and the LNG projects included.

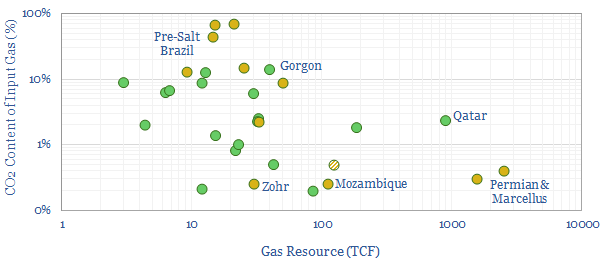

LNG technology could thus unlock incremental LNG facilities. We are most positive on low-cost, low-CO2 sources of gas, particularly in stable and low-tax countries. To help assess the potential, we have therefore compiled a data-file of the world’s great gas resources and their CO2 content, downloadable here. Our positive outlook on US LNG is further underpinned by our positive outlook on US shale.

Conclusions: path dependency?

The numbers above are not hard forecasts. We do not believe hard forecasts are possible in a market that is shaped by unpredictable geopolitics, technologies, weather and its own price-reflexivity. However, we have argued that new technologies may unlock materially more LNG demand than is currently embedded in consensus expectations. Leading companies with leading LNG projects may benefit.

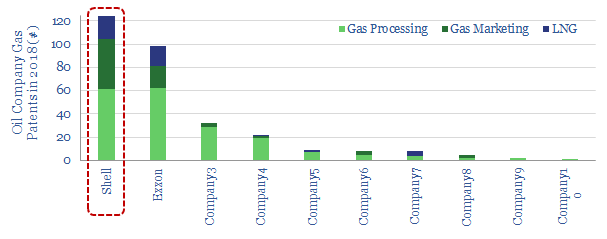

Shell is the leading Major in driving new LNG demand, based on patent filings (chart above). As an example, we highlight a leading new technology to promote LNG demand in transportation, by mitigating the problem of boil-off.

[restrict]

What is limiting LNG in transport?

LNG’s potential upside in transportationis exciting, particularly in shipping, as technologies improve and new sulphur regulation sweeps through the maritime industry (chart below, for full details see our deep-dive note, LNG in Transport: Scaling Up by Scaling Down). But challenges must also be acknowledged.

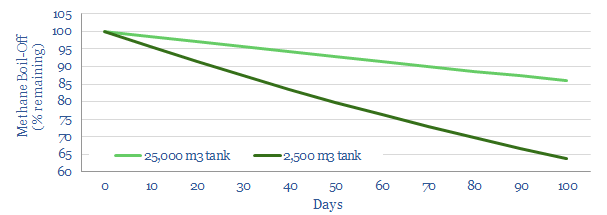

Most prominent is boil-off of LNG, which inhibits its storage over long time-frames. Boil-off typically runs at 0.15% per day, in a large, 25,000m3 tank, which means that c15% of the cargo would be lost over a 100-day period. For smaller-scale LNG, the rate is steeper, averaging c0.45% per day for a 2,500m3 tank, which in turn would cost c35% of the cargo over a 100-day period (chart below). In extremis, 1% per day boil-off is not unheard of.

Managing boil-off requires a vapor management system. Otherwise, as liquid evaporates into gas, the pressure exerted gradually rises, and eventually there is risk of exceeding the tank’s design pressure. This one one reason for the additional costs of converting a vessel to run on LNG, which can reach $17-35M for the largest tankers.

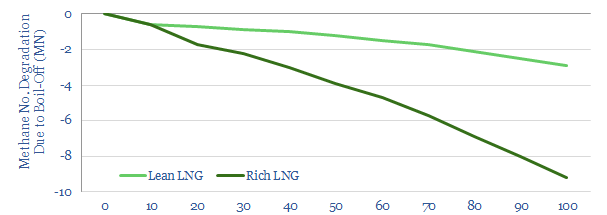

Gas Weathering is another challenge, less well-known, but crucially important. LNG is a mixture of hydrocarbon gases, all with different boiling points. Lower boiling-point components vaporize more readily. Hence over time, the higher boiling point constituents become more concentrated in the fuel tank, lowering the “methane number” of the fuel (chart below). This causes challenges. Most engine makers specify methane must comprise >80% of the fuel in a gas-fired engine. Below this level, the engine performs sub-optimally, knocking, misfiring, over-heating and potentially damaging components such as piston crowns and exhaust valves.

Shell’s improvements: a sub-cooler

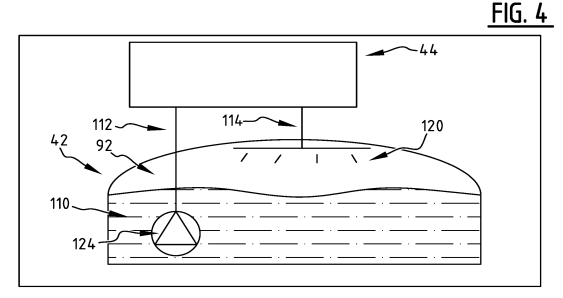

To support LNG’s ascent in transportation, Shell has been the most active Major in developing new technologies. We will be elaborate further, in our upcoming research. But in 2019, one patent stands out, as the company has developed a new ‘sub-cooler’ (pictured below), to met the challenges described above.

The sub-cooler (44) is fluidly connected to the LNG storage tank (42) on a LNG-powered vessel. The tank’s temperature is continually monitored. When it exceeds a predetermined upper threshold, by say 0.25C, a small volume of LNG is pumped out (through 112) , sub-cooled (in 44) then sprayed back into the tank’s vapor space (via 114), until the tank is cooled back below a lower threshold, say, 1C below methane’s boiling point.

The invention’s equipment includes a compressor, a turbine, two heat-exchangers and use of the Brayton Cycle, most likely Air Liquide’s Turbo-Brayton refrigeration cycle using Nitrogen and/or Helium. Its advantage is reliability and low maintenance, which matter for long voyages.

Eight Advantages are Cited

Storage capacity is increased by providing constant and continuous vapor management, using the sub-cooling system.

Weathering is prevented, by sub-cooling and recycling liquefied gas, thus preserving the composition of the liquefied gas.

Fuel economy is thus maximised by avoiding the sub-optimal fuel-consumption caused by weathering. Shell states “Utilization of this system on gas fueled vessels will also allow for greenhouse gas emissions to be optimized”.

Longer journeys are thereby made more feasible.

Capex is saved. By employing Shell’s sub-cooler, no auxiliary consumer is required, lowering the cost of the system, potentially elminating GVU units, control valves, double wall piping, and labor and installation costs.

Opex may improve, due to better fuel economy, and as a larger range of input fuels can be used,

Safety is improved during transfer of LNG from a discharging tank to a receiving tank, providing the ability to lower temperature to 0.5-3C below the gas’s boiling temperature and “thereby limit flashing in the receiving tank during transfer”.

Versatility. The system can be installed in new LNG-powered vessels, new conversion of diesel vessels or retro-fitted onto existing LNG vessels. It can also be deployed in a broad range of LNG-transportation concepts (the patent mentions cruise ships, tankers, container vessels, ferries, barges, tugs… and more exotically, rail, truck, car and even planes!).

Economic Impacts to spur the ascent of gas?

The improvements above may stoke the ascent of LNG for shipping, where we are most positive with 40-60MTpa of upside seen to LNG demand after 2040 (see LNG in Transport: Scaling Up by Scaling Down).

Small-scale liquefaction for shipping is already going to be highly economical after IMO 2020, while bunkered LNG can be rendered as economic if it can harness economies of scale (model here).

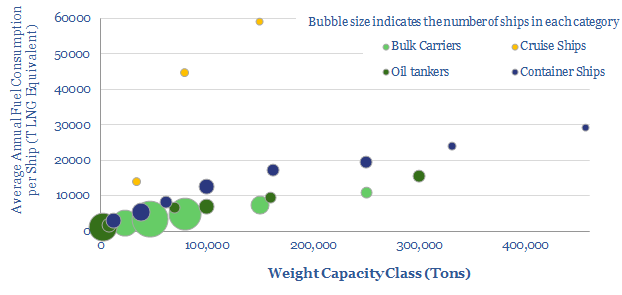

The most attractive vessels to convert to run on LNG are cruisers and large container ships (data-file here).

Economics are currently more challenging for LNG trucks (model here). However, this is due to 2.5x higher vehicle costs and 2x higher maintenance costs per mile. But technical progress such as Shell’s will help.

Source: Hutchins, W. R. & Hartman, S. J. S. (2019). Liquid Fuel Gas System and Method. Royal Dutch Shell Patent US2019024847

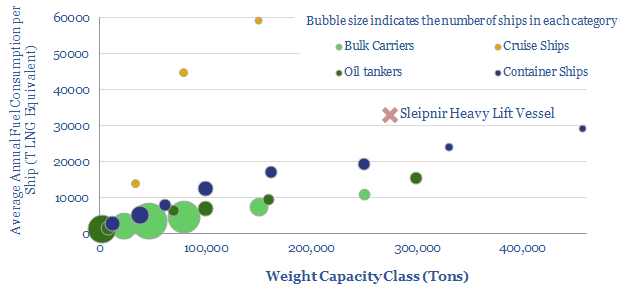

Multiple records have just been broken for an LNG-powered ship, as construction completed at Heerema’s “Sleipnir” heavy-lift vessel (charted above). It substantiates our recent deep-dive note, which sees 40-60MTpa upside to LT LNG demand, from large, fuel-intensive ships, after IMO 2020.

Sleipnir is a record-setting crane-lift vessel, with capacity to pick up 20,000T. This eclipses the prior records in offshore oil and gas, which were around 12,000T, set by the Heerema Thialf and the Saipem 7000. Hence Sleipnir has already lined up 18 contracts, starting with the 15,800T topsides for Israel’s Leviathan gas field, and progressing on to Johan Sverdrup Phase II.

Sleipnir is a record-setting LNG vessel, burning gas as its primary fuel (although it can also burn diesel). With a displacement of 273,700T, we estimate it is the heaviest LNG-powered vessel ever built (eclipsing the largest such container ships, at 220,000T). With a cost of $1.5bn, we estimate it is also the most expensive LNG-powered ship ever built (eclipsing Carnival’s $1.1bn AidaNova cruise ship). It has the world’s first Type-C LNG tank in an enclosed column. Numbers are updated in our data-file here.

There is upside to LNG demandin large, fuel-intensive ships, especially cruise- and container ships, after IMO 2020. Small-scale LNG may offer an economic “bridge”, while bunkering becomes increasingly attractive as volumes per port scale past c80kTpa. Forward-thinking Majors are already investing to capture the future market.

Finally, for a video of the construction vessel being constructed…

The downstream industry is currently debating whether IMO 2020 sulphur regulations will be resolved quickly or slowly. We think the market-distortions may be prolonged by under-appreciated technology challenges.

[restrict]

As context, from 2020, it will no longer be permitted to burn fuels with 3.5% sulphur in the marine segment. Their maximum permitted sulphur content will fall to 0.5%. In principle, refining cracks will move, advantageously for low-sulphur diesel and disadvantageously for high-sulphur fuel oil.

Over time, this should provide an economic incentive to construct incremental hydro-processing and hydro-conversion technologies. However, it still may not be so simple as to construct a few extra hydro-processing units. Not all sulphur is equal.

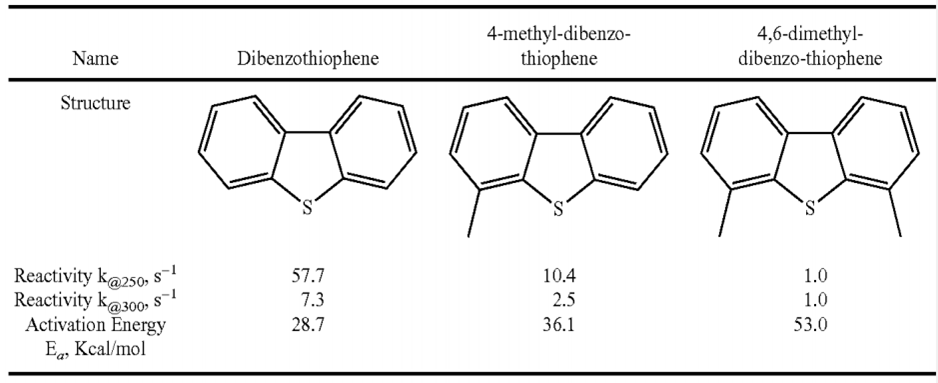

Hard Sulphur and Easy Sulphur

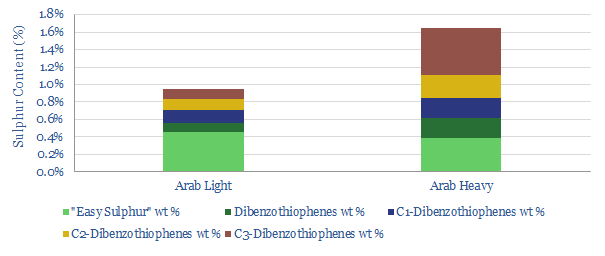

On the one hand, aliphatic sulphur compounds are easily treated. The process uses a hydrogen partial pressure of 10-30kg/cm2, 180-370C temperatures, and liquid:catalyst ratio up to 4:1. The catalyst contains Cobalt, Nickel and/or Molybdenum on an aluminium oxide framework. This is industry-standard technology, available to all.

However, highly branched molecules are harder. One class, dibenzothiophenes, is pictured below. Their structure impedes the sulphur “heteroatom” from reaching the active site on the catalyst. Run it through a low-spec hydrotreater, and it comes out the other side… unchanged.

Another challenge with aromatic sulphur-containing compounds is their under-saturation. Traditional hydroprocessing techniques, aimed primarily at reducing sulphur, also tend to saturate these aromatic rings which “can increase the amount of hydrogen consumed during hydroprocessing by as much as an order of magnitude”. This is problematic at refineries with limited hydrogen. It adds cost.

It may be under-appreciated how much of the sulphur in the world’s fuel market is “difficult sulphur”, rather than “easy sulphur”. For example, if we take Saudi Arabia’s production, comprising the most abundant crude oil streams on the planet, the more challenging sulphurs comprise 0.5% of Arab Light, and 1.3% of Arab Heavy.

As Aramco’s patents note “it is very difficult to upgrade existing hydrotreating reactors” and “the economical removal of refractory sulfur-containing compounds is exceedingly difficult to achieve”. Especially if the end target is to reach higher European and US standards of 0.1% sulphur caps.

Resolving the Impasse: Large Investments?

There are solutions to this challenge. Indeed, Aramco has filed patents for methods of removing these more challenging sulphurs. One is to build a new separation unit, distill the crude into two separate streams, isomerise the ‘hard sulphur’ stream, re-combine it with the ‘easy sulphur’ stream, then hydro-treat the mixture. Hydrocracking these compounds is another option, breaking them down into lighter, smaller, “easier sulphur” molecules.

Both of these options require large investment, with multiple processing units and ancillary units. It follows that the ultimate refinery projects used to re-balance the market post-IMO 2020 are not simple hydoprocessing projects.

Against this backdrop, fears over the energy transition make it increasingly difficult to justify large, long-term investments. Particularly in Europe.

[/restrict]

Opportunities amidst the Challenge?

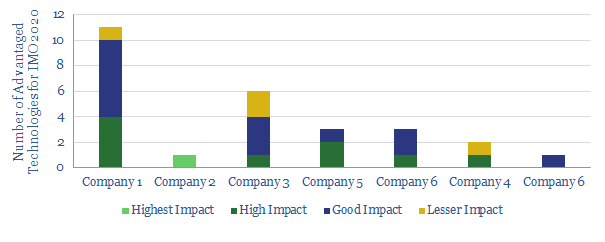

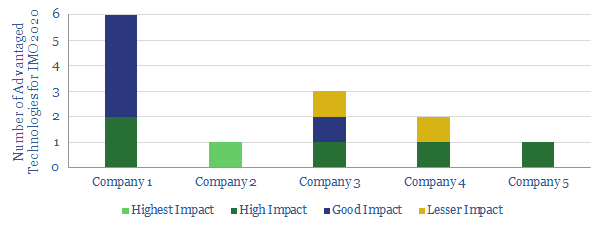

So if the market-distortions of IMO 2020 have longevity, who will stand to benefit? We are maintaining a data-file of the ‘Top Technologies for IMO 2020’ around the industry, which give specific companies an edge. The data file now contains over 25 technologies across 7 Majors.

References

Al-Shahrani, F., Koseoglu, O. R. & Bourane, A. (2018). Integrated System and Process for In-Situ Organic Peroxide Production and Oxidative HeteroAtom Conversion. Saudi Aramco Patent.

Koseoglu, O. R., (2018). Integrated Isomerisation and Hydrotreating Process. Saudi Aramco Patent CN107529542

Hanks, P. (2018). Trim Alkali Metal Desulfurisation of Refinery Fractiions. ExxonMobil Patent US2018171238

Next-generation technology in small-scale LNG has potential to reshape the global shipping-fuels industry. Especially after IMO 2020 sulphur regulations, LNG should compete with diesel. Opportunities in trucking and shale are less clear-cut.

This note outlines the technologies, economics and opportunities for LNG as a transport fuel, following a three-month investigation.

Why technology matters. Pages 2-4 of the note describe incumbent technologies in small-scale LNG, and the need for superior solutions.

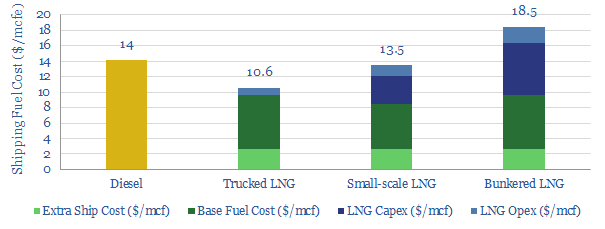

The cutting edge . Pages 5-7 draw on patents and technical papers to describe next-generation technologies, at the cutting edge of small-scale LNG. We model that they are economic. They can can provide LNG to the market at $10/mcf.

Potential to transform shipping-fuels. Pages 9-13 find strong economic upside for novel LNG technologies in the shipping industry, with potential to create 40-60MTpa of incremental LNG demand, looking across the global shipping fleet.

Less positive on LNG as a trucking fuel. Pages 14-15 explain why the economics are more challenging for LNG use in land-transportation, i.e., trucking.

Less positive on LNG use in shale. Page 16 explains, similarly, why LNG is less advantageous in the shale patch than converting rigs and frac spreads to piped gas.

Other technologies. Page 17 notes other companies with interesting offerings in small-scale LNG liquefaction, including advances by Exxon and Shell.

Have further questions? Please contact us and we’ll be happy to help: contact@thundersaidenergy.com

So far we have reviewed 400 patents in the downstream oil and gas industry (ex-chemicals). A rare few prompted an excited thought — “that could be really useful when IMO 2020 comes around”.

Specifically, from January 2020, marine fuel standards will tighten, cutting the maximum sulphur content from 3.5% to 0.5%. It will reduce the value of high-sulphur fuel oil, and increase the value of low-sulphur diesel.

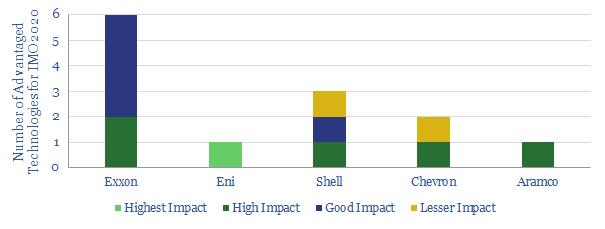

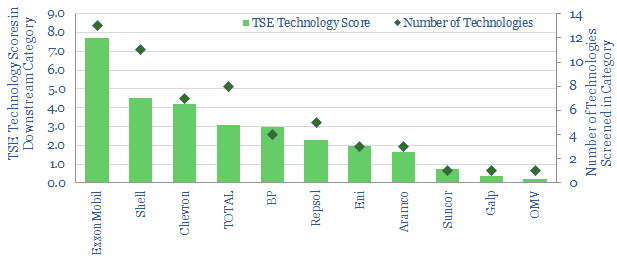

This note summarises the top dozen proprietary technologies we have seen to capitalise on the shift, summarised by company (chart below).

[restrict]

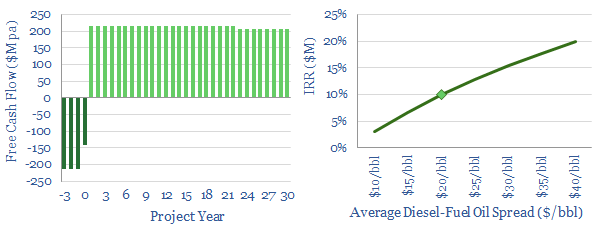

(1) Eni Slurry Technology (EST). Advertised as “the best worldwide technological solution for operators who wish to completely convert the bottom of the barrel”, EST converts >97% of heavy inputs into more valuable fractions. It is a hydroconversion process, which upgrades fuel oil or other heavy crudes, using a slurried, nano-dispersed zeolite, impregnated with Molbdenum/Nickel sulphide salt catalyst, run at 380-440C. $4.5/bbl uplifts to refining margins are cited by the company. It has been licensed by two Chinese refiners (Sinopec, Zhejian), for their own upgrading processes. We estimate EST will yield 10-20% returns, at $20-40/bbl upgrading spreads (chart below, model here).

(2) – (7). ExxonMobil refining technology. So far, ExxonMobil has the most advanced refining technology, out of the patents we have reviewed across the industry (chart below). For IMO 2020, this includes:

(2) Exxon. Hydrocracking. In its public disclosures, Exxon has alluded to using a proprietary catalyst in the $1bn hydrocracker at its 190kbpd Rotterdam refinery expansion, upgrading lower-value vacuum gasoil into Group II base stocks (see below) and ultra-low sulfur diesel.

(3) Exxon. Hydroprocessing. 5 patents were filed in 2018, for hydroprocessing and purifying heavy oil, coker oil or deasphalted slurry oil, to remove sulphur and nitrogen impurities, using a proprietary catalyst prepared from Group VI and Group VIII metals.

(4) Exxon. Lubricants from Fuel Oil. Exxon has filed patents to create Group I-III base oils for its lubricants business using FCC slurry, thermally cracked resids or other “disadvantaged feeds”. Requires high-pressure hydrofinishing to reduce aromatic saturation.

(5) Exxon. Dewaxing Catalysts. In 2018, Exxon patented a new de-waxing process that was achieving “unexpectedly high hydrogenation of feedstocks” without unwanted cracking. The proprietary catalyst combines noble metals and base metals on a zeolite framework. It can be used to improve heavier fuels, such as fuel oil.

(6) Exxon. Reduced Severity FCC. In 2018, Exxon patented a new combination of desaphalting and hydroprocessing. These steps are performed prior to fluid catalytic cracking (FCC). This allows the FCC to be run at less severe conditions. In turn, this reduces the production of light paraffins. It is seen to increase gasoline/diesel yields and lower fuel oil yields.

(7) Exxon. Diesel Range Fuel Blends. Some elastomers in vehicle fuel systems are known to swell when exposed to highly aromatic fuels and to shrink when exposed to renewable diesel components. The elastomers can fail when renewable components surpass 10%, limiting use of renewable diesel. Hence Exxon has tested and patented diesel blends (typically with 20+ components) that can tolerate >20% renewable inputs without shrinking fuel-systems’ elastomers.

(8) Shell. Ebullated Bed Processes. Shell has filed three patents to overcome the problem of sediment-fouling when upgrading heavy, asphaltene-rich hydrocarbons in an ebullated bed reactor. Shell’s solution is a reactor design with an ‘upper section’ and a ‘lower section’, each with its own catalyst composition.

(9) Shell. Hydrodesulfurisation Catalysts. Uses molybdenum-disulfide nano-particles supported on a titanium framework.

(10) Shell. Fuel Oil Composition. Shell has patented its own blend of fuel oil with 0.100% sulphur concentration, suggesting it is gearing up to compete within the fuel oil segment.

(11) Chevron. Improved hydro-conversion catalysts. Chevron filed c35 distinct patents for zeolite catalyst systems in 2018, largely aimed at hydrocracking, and improving energy efficiency. One formulation achieves 37% middle distillate yields from heavy oil, at 193C. Another can yield up to 83% middle distillates, when running C5s at 140-370C. Yields on average heavy inputs are c50%.

(12). Aramco. Advanced Hydrocracking Catalyst. Aramco has patented a system that is achieving higher yields of middle distillate, by avoiding “over-cracking” kerosene and gasoil. It works via a zirconium-hafnium zeolite, which encourages heavier oil into the zeolite mesopores. Do not be surprised to find Aramco in this list: it is a clear technology leader across the 1,440 patents we have reviewed so far.

If you have any questions about this list, or think we’ve missed anything that should be on here, then please let us know: contact@thundersaidenergy.com

[/restrict]

Cookies?

This website uses necessary cookies. Our cookies are simply to improve your experience. We do not undertake any advertising or targeting via our cookies. By clicking 'accept' or continuing to use the website, you consent to our use of cookies.AcceptRead More

Privacy & Cookies Policy

Privacy Overview

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.