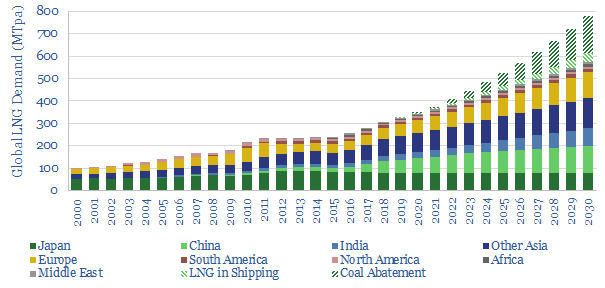

Gas demand could treble by 2050, gaining traction not just as the world’s cleanest fossil fuel, but also the most economical. The ascent would be driven by technology. Hence this note outlines 200MTpa of potential upside to consensus LNG demand, via de-carbonised power and shipping fuels. LNG demand could thus compound at 8% pa to 800MTpa by 2030, justifying greater investment in unsanctioned LNG projects.

[restrict]

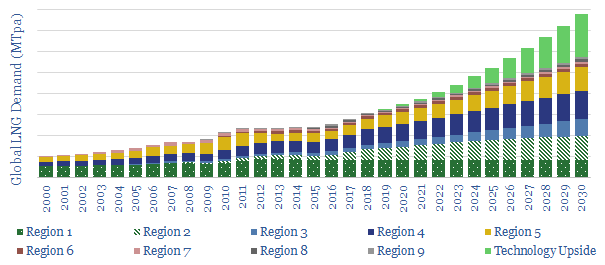

Consensus LNG demand?

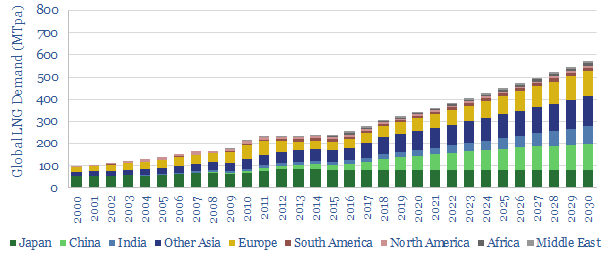

A simple model of global LNG demand is shown below (and downloadable here). It is created by extrapolating recent trends in key LNG-consuming regions. The total market grew at 5.7% pa in 2013-18. At a 5.4% forward CAGR, it would reach c570MTpa by 2030. These numbers are not far from other LNG forecasters’, and thus serve as a reasonable consensus.

What excites us is the potential for technology to accelerate LNG demand. Markets are slow to reflect technological breakthroughs. Hence these new demand sources likely do not feature in consensus forecasts yet. In our view, this makes them worthy of attention.

Upside from De-Carbonised Power Generation?

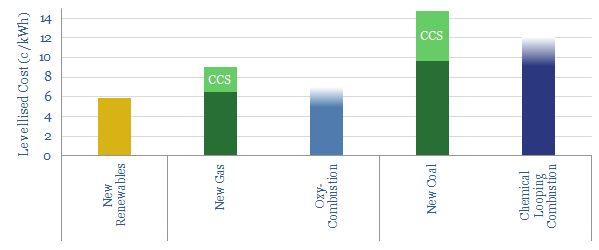

The first opportunity is in de-carbonised power generation, as we have discussed in our deep-dive report, ‘de-carbonising carbon‘. We think novel technologies are reaching maturity, which can generate cost-competitive electricity (chart below) alongside an exhaust stream of pure CO2, for use in industry or for immediate sequestration. The full details are in our report.

Let us now make some approximate calculations: The world consumes 7.7bn tons of coal per annum. In energy terms, this is equivalent to c165TCF of gas, or 3,300MTpa of LNG. We believe it would be economic, and achievable, to convert c5% of this coal power to gas by 2030. Converting it to decarbonised gas could save c1bn tons of CO2 emissions per annum. In turn, this could be achieved by 200GW of de-carbonised gas-power, in 500 x 400MW power plants, each burning c50mmcfd of input gas, fed by 165MTpa of LNG. This is the first area where technology can greatly accelerate LNG demand.

Upside in Shipping?

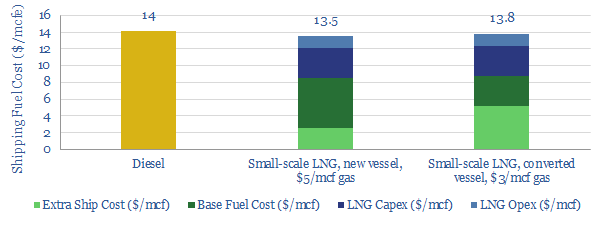

The second opportunity is in LNG as a shipping fuel, which will become increasingly economical after IMO 2020 sulphur regulations re-shape the marine sector. The economics are shown below and modelled here.

New technologies in small-scale LNG will accelerate adoption in smaller ports, moving beyond the large port-sizes required for bunkering. The technologies and economics are explored in detail, in our deep-dive note, LNG in Transport. The economics are modeled here. To assist, Shell is also pioneering new solutions for LNG in transport.

The upshot could be 40MTpa of incremental LNG demand in the maritime industry by 2030. This is the second area where technology can greatly accelerate LNG demand.

Less positive on trucking

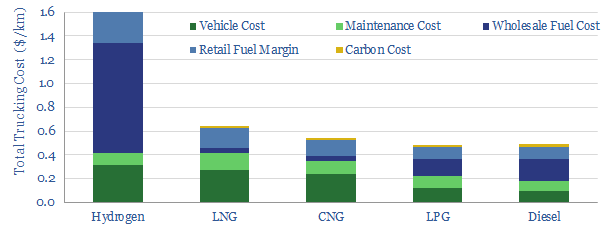

Is there further upside? One might expect, in an overview of LNG technologies, to find incremental upside in road vehicles: either directly in LNG-fired trucks, in gas-fired vehicles, or to produce hydrogen for fuel-cells. None of these opportunities are yet captured in our models.

The reason is economics. Compared to diesel-powered trucks, we find compressed natural gas to be c10% more expensive, LNG to be 30% more expensive and hydrogen to be around 4x more expensive (model here, chart below). We also find hydrogen to be 85% costlier than gasoline, to powers cars in Europe (model here). In most cases, electrification is the better option, as superior vehicle concepts emerge.

Our numbers do not include any incremental LNG demand in the road-transportation sector. However, it is noteworthy that replacing 1Mbpd, or c2% of the world’s road fuels with LNG would consume an incremental 50MTpa of LNG. This could cushion delays or shortfalls in decarbonised gas-power.

Potential supplies can meet the challenge.

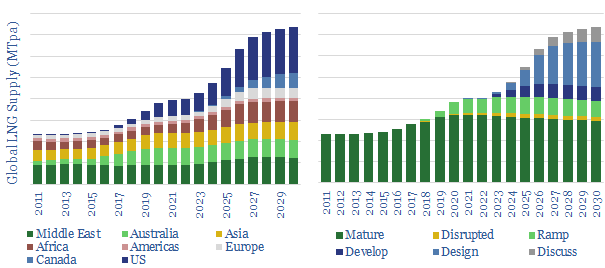

It is only possible for the world to consume 800MT of LNG in 2030 if it is also possible to supply 800MT. While our risked forecasts are for c600MT of LNG supply in 2030 (chart below), our numbers are including just c60% of the 230MTpa of LNG capacity that is currently in the design phase, and just 15% of the 180MTpa that is currently in the discussion phase. In a generous scenario, our forecasts rise close to the 800MTpa level that is required. Please download our risked, LNG supply model to see our scenarios, and the LNG projects included.

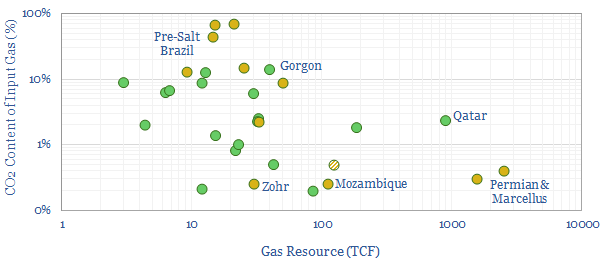

LNG technology could thus unlock incremental LNG facilities. We are most positive on low-cost, low-CO2 sources of gas, particularly in stable and low-tax countries. To help assess the potential, we have therefore compiled a data-file of the world’s great gas resources and their CO2 content, downloadable here. Our positive outlook on US LNG is further underpinned by our positive outlook on US shale.

Conclusions: path dependency?

The numbers above are not hard forecasts. We do not believe hard forecasts are possible in a market that is shaped by unpredictable geopolitics, technologies, weather and its own price-reflexivity. However, we have argued that new technologies may unlock materially more LNG demand than is currently embedded in consensus expectations. Leading companies with leading LNG projects may benefit.

[/restrict]