Gas-fired power generating capacity is in a classic capital cycle. This 16-page report evaluates when the cycle will peak. Gas power demand wants to rise at 3.8% pa through 2050. But high CCGT prices may delay EM growth, bring in new entrants, and substitution towards reciprocating engines.

Forecasting the demand for global gas turbines can feel like a Herculean labor. This is because gas power is often the balancing line in electricity demand models. Demand for gas generation = total demand – demand for wind, solar, nuclear, hydro, coal, and even wood. So we have had to review all of our models.

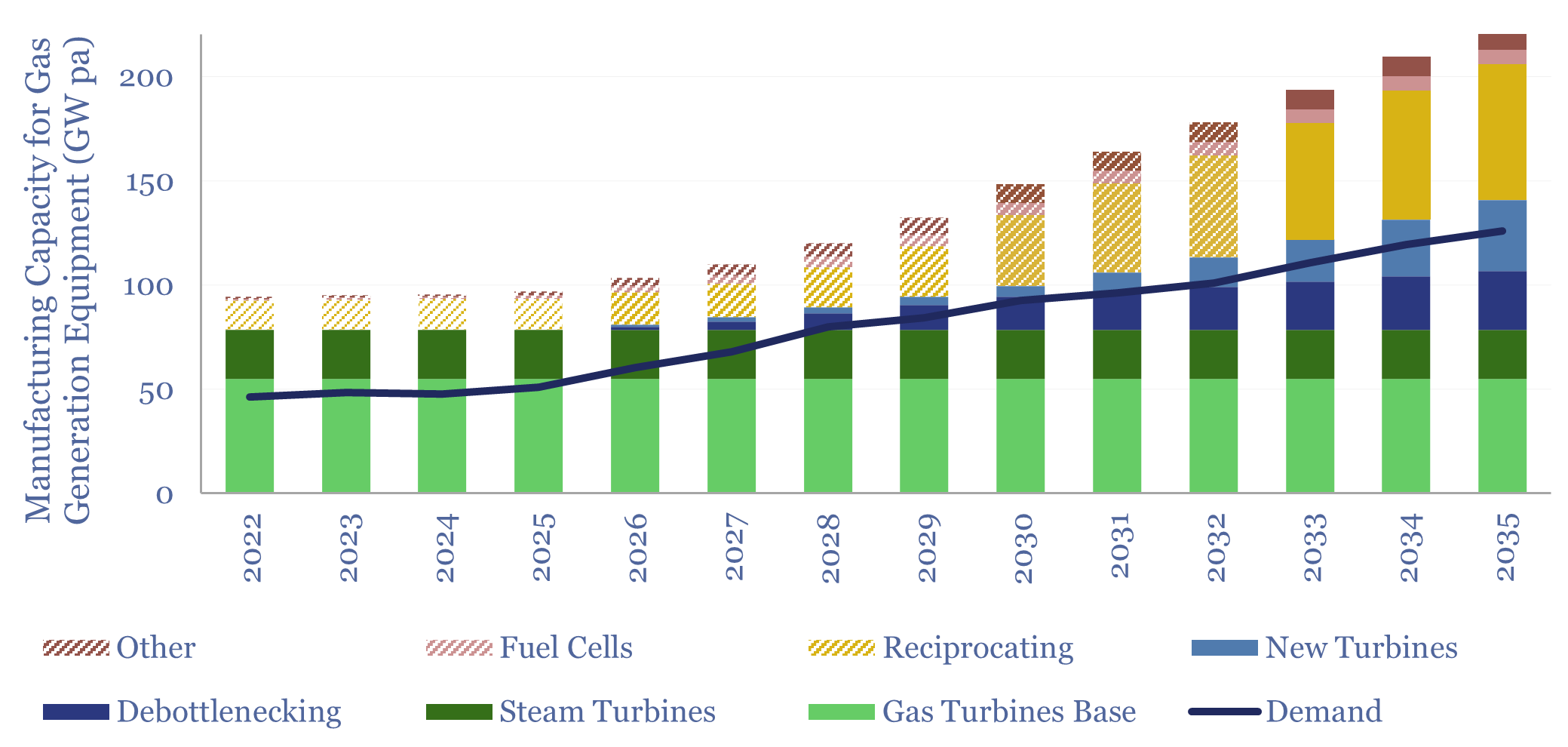

Nevertheless, we have forecast the demand for gas-fired generation capacity, which is inflecting from 50GW in 2019-25 pa to over 100GW pa from 2026-2035, using the methodology and assumptions on pages 2-4 of this report.

So how much capacity to manufacture gas turbines and meet this demand for new gas generation? And how much is gas turbine capacity being expanded? We have reviewed the production facilities from all of the major gas turbine manufacturers. Our analysis shows why the market seems very tight, potentially above 90% manufacturing capacity utilization, from 2028-2035, on pages 5-7.

However, there are different types of gas generation. We estimate the capacity to deploy fuel cells, repurpose jet engines, add steam cycles to pre-existing OCGTs and economically ramp up reciprocating engines, on pages 8-11.

Moreover, 85% of the next decade’s demand for gas-fired generation is in the emerging world. Especially China. We explore whether price sensitivity is higher in the emerging world, and thus persistently high gas turbine prices could push these buyers to other forms of generation, or even slow their growth, on pages 12-13.

In the developed world, rising demand for gas generation is mostly linked to AI data centers. And most of that is in the US. We can quantify how many gas generation projects are under development in the US. But could training efficiency gains, or technology risks with new power delivery architectures, delay the absorption of these turbines? Our views are on pages 14-15.

Ultimately it is an exciting time for gas-fired generation, especially recips, but we must also assess the risks of a gas turbine capital cycle which overshoots both to the upside and the downside. Our recommendations are on page 16.