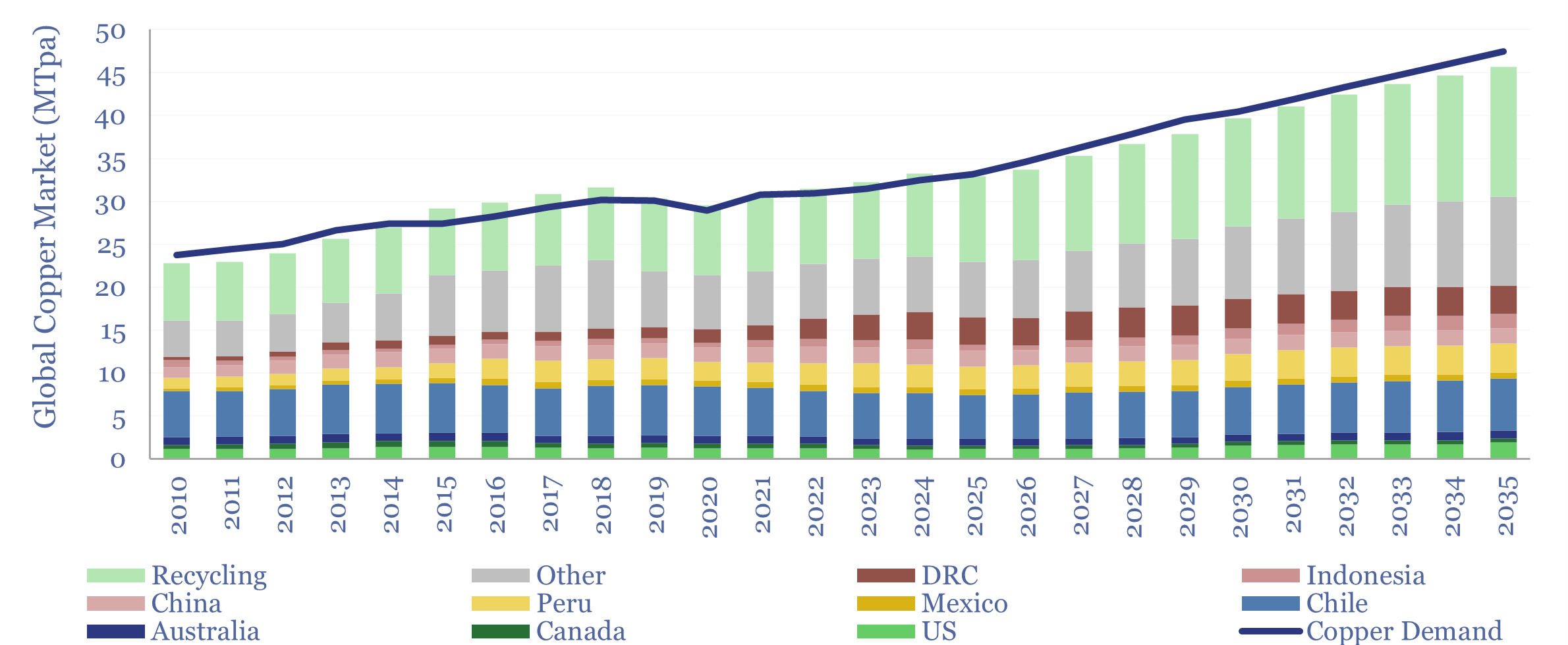

Global copper supply-demand is tabulated in this data-file, looking across 90 mines and upcoming projects, by country, and over time. Markets were 5% undersupplied when prices spiked in 2010-11, 6% over-supplied when they collapsed in 2015-16, and returned to undersupply in 2025. Undersupply persists through 2035, most likely at -3% pa, as demand grows by 3.6% pa.

Global copper demand ran at 34MTpa in 2024 and is forecast to rise +3.6% over the next decade, in our model of global copper demand. These numbers are quoted on a gross basis, including directly reused copper, secondary production (i.e., re-refining prior scrap) and alloys (brass, bronze, etc) ran at 34MTpa in 2024.

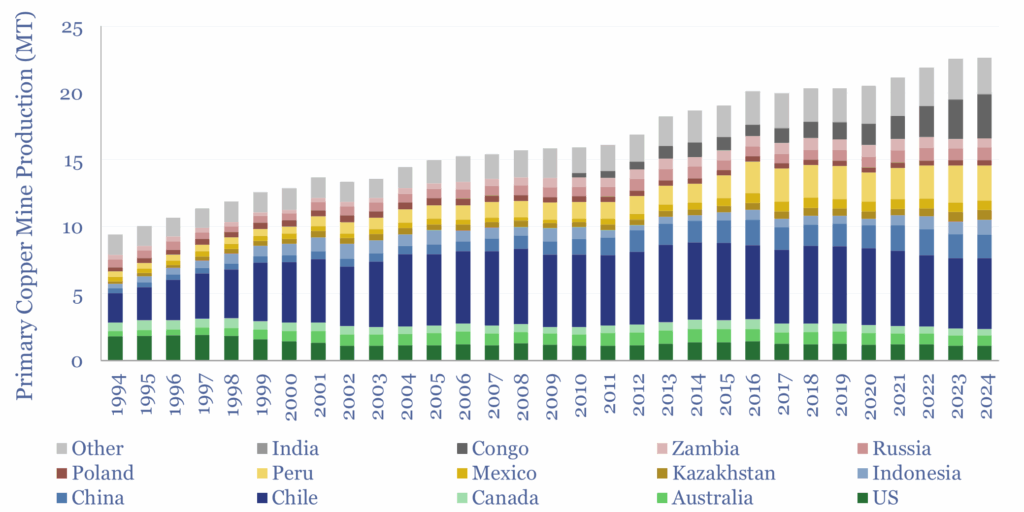

Primary global copper production ran at 23MTpa in 2025, and has hardly grown since 2022, due to well-known supply disruptions (e.g., at Grasberg, Cobre Panama and broader issues in Chile).

This data-file contains a breakdown of global copper production, looking across 35 of the largest mines currently operating (e.g., Escondida, the largest copper mine in the world) and c60 upcoming copper projects, whose future supply has been appropriately risked.

Inputs come mainly from copper producers, while we have also tabulated project costs in our model of copper economics.

Copper production is concentrated in Chile (22% of global primary production), the Democratic Republic of Congo (14%), Peru (12%), China (8%), the US (5%), Australia (4%), Indonesia (3%), Mexico (3%) and Canada (2%).

Global copper supply-demand looks tight through 2035, with undersupply averaging -3% pa. This is with no room for further disruptions, minimal declines from the producing base, and requires ramping up 1.6MTpa of development-stage projects by 2030 and 1.5MTpa of earlier-stage projects, which although risked in our models, could slip back further due to inevitable delays.

Risks to the upside. Without timely progress in the developing new mines, progressing early-stage projects and expanding recycling, copper markets could be 7MTpa undersupply by 2030, which is 17% of potential demand.

Risks to the downside are whether record high copper prices, and a 2026 slowdown in both solar and EVs, could detract from demand. And in the medium-term, we may also see a step-change in copper recycling from next-gen waste management.

Upside-downside scenarios to global copper supply-demand can be stress-tested in this data-file, looking project-by-project, or flexing recycling rates/secondary supplies.

Longer-term historical global copper production is also disaggregated in the data-file, on a mined basis (chart below), and on a refined basis, using data from the USGS.