10 companies have recently launched AI-enabled robotics to recover value from the world’s 2.3GTpa of solid waste. Picking rates are 4x faster than humans. <1-year paybacks are quoted. Hence today’s 17-page report explores the implications for gas, power, metals, materials and oil markets, amidst a step-change in the circular economy.

The ideal place to deploy robotics is in contexts that are ‘dull, dirty, distant and dangerous’, as discussed in our recent research into industrial robots and inspection robots. Waste management facilities tick all of these boxes, for the reasons discussed on pages 2-3.

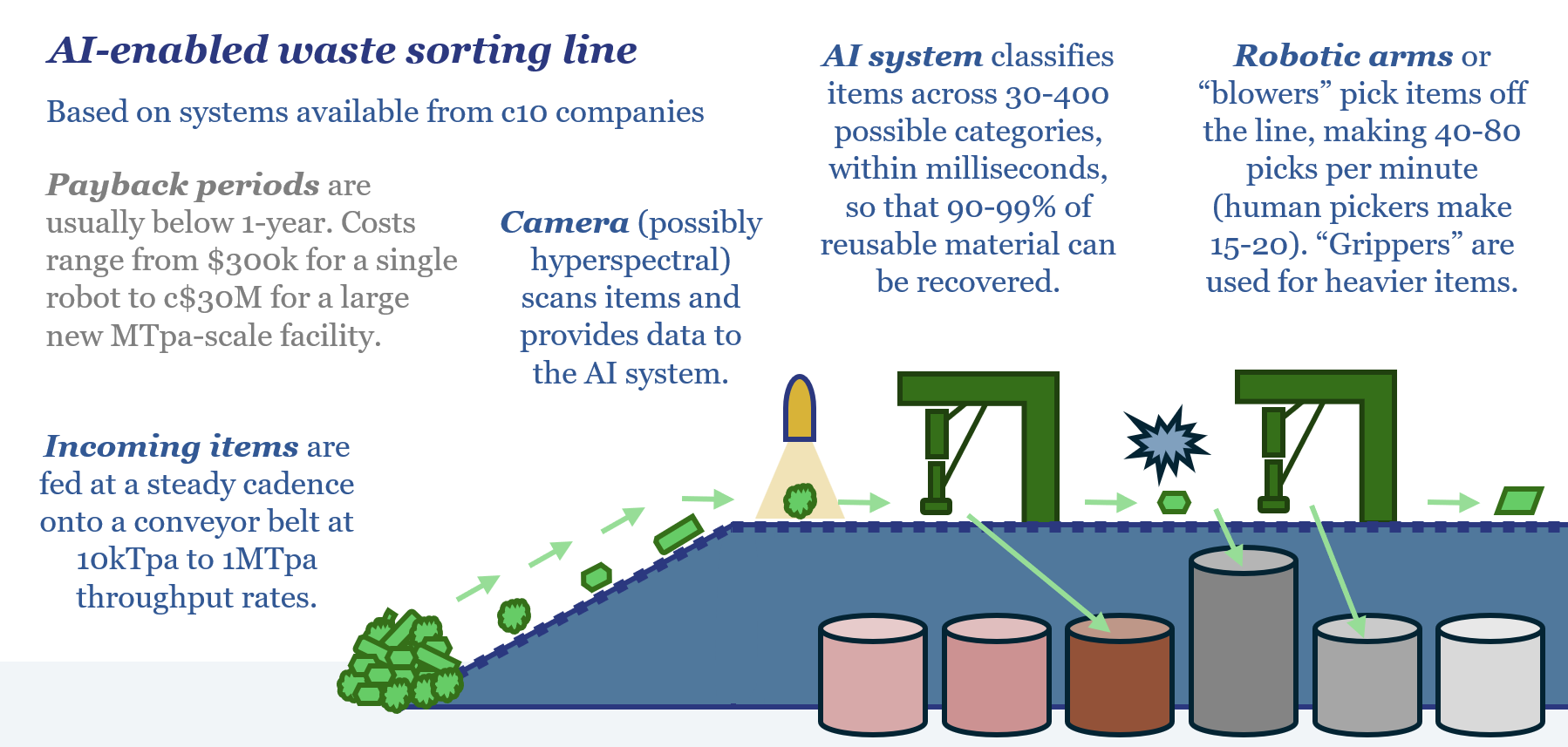

Hence we wanted to see whether any companies are deploying AI-enabled robots, to accelerate recycling and materials recovery, as part of the circular economy. What we found was an amazing, vibrant landscape of companies using AI for waste sorting, as summarized on pages 4-6.

Hence the purpose of this note is to explore possible implications across gas, power, metals, materials and oil markets, if AI-enabled robotics can recover more value from the world’s 2.3GTpa of municipal solid waste. We are clearly not going to be de-risking all of this just yet. But the numbers are large.

In gas and power, we lean on our models for biogas economics and waste incineration. In theory, there is enough recoverable energy in all the world’s waste to power all of 2030’s AI data centers about 2x over. Numbers, and biogas forecasts, are on pages 7-8.

In metals, AI could theoretically recover much MORE material from waste streams than is needed to build data centers and robots. This could impact copper supply-demand, steel, aluminium, battery materials (especially lithium), Rare Earth magnets, silver and other PGMs, per pages 9-10.

Even oil markets, where combustion might seem to offer immunity from recycling, could be impacted by several Mbpd by a step-change in waste management, across our oil models, plastics models and finding feedstocks for renewable diesel, per pages 11-12.

Clearly we are not going to be de-risking all of the “blue sky” implications across our models straight away, but the magnitudes in question do suggest that the theme needs to be tracked in our ongoing models. How real is it? How much is actually happening? To answer this question, we present detailed notes on a dozen leading companies, on pages 13-17.

There are also interesting implications for companies providing equipment, components and for companies recycling metals and materials (which may see greater feedstock availability). All of this is discussed along the way.