What is the price elasticity of oil demand — globally, by region, and by product? This 11-page report argues that a supply disruption of 10-20Mbpd magnitude, lasting for 6-12 months, pushes oil above $250/bbl, and also zeroes global GDP growth. Rationing and solar/EV substitution may cushion the impact.

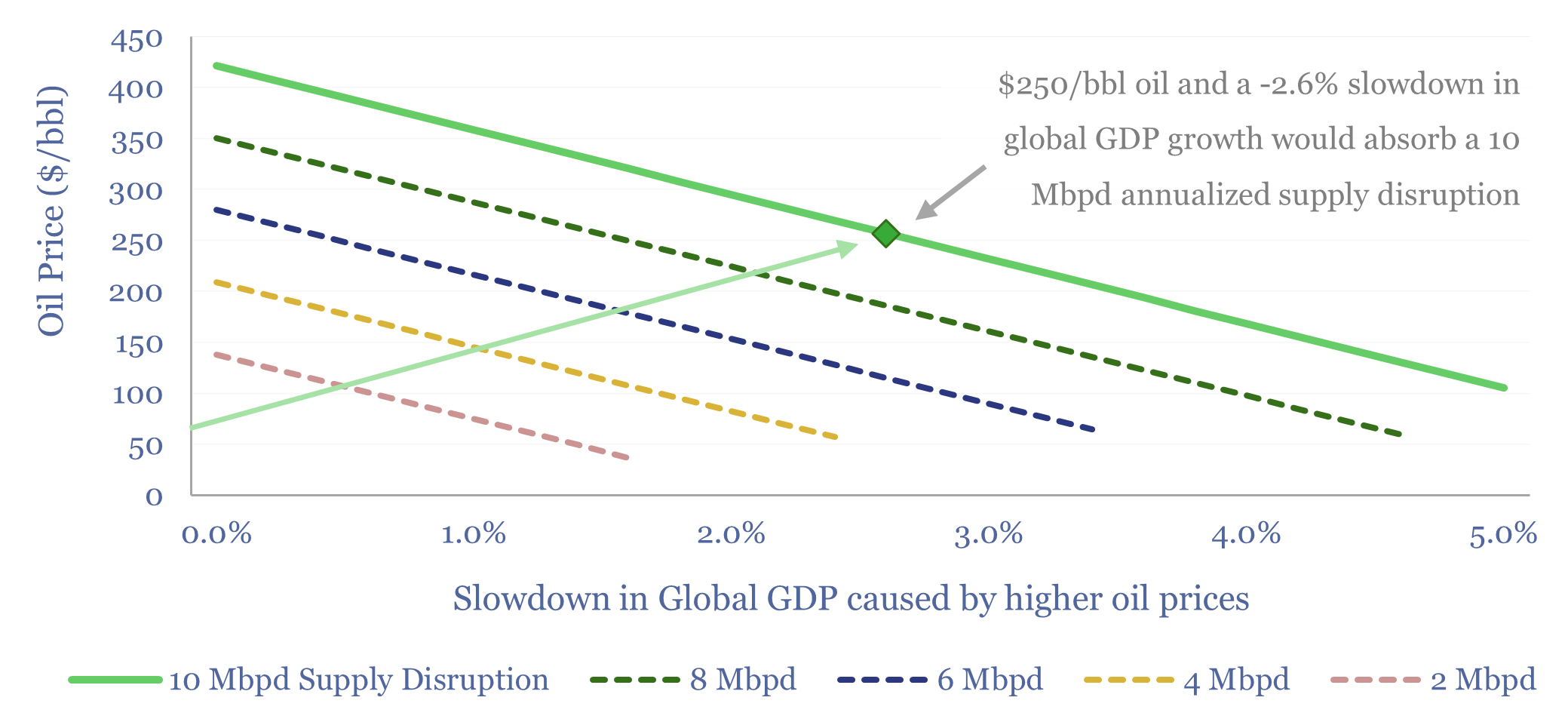

What if global oil supplies were disrupted by an enormous 10Mbpd, over an entire year, possibly due to protracted conflict in the Middle East? How high could prices go?

To answer these questions, this 11-page report evaluates the price elasticity of demand in oil markets. This requires some statistical acrobatics, to disaggregate GDP sensitivity, as explained on pages 2-3.

Hence we can calculate the price elasticity of demand across global oil markets; across product categories such as LPG, gasoline, distillates, jet fuel and plastics; and across regions such as the US, Europe, Asia, India, the Non-OECD and “petro-economies”, on pages 4-7.

Elasticity is low. It takes a large run-up in the price to destroy demand. Hence other levers include lower GDP growth, rationing (discussed on page 8) and substitution (page 9).

Substitution. We have already raised our forecasts for global solar additions by +100GW for 2026, and we are also raising our forecasts for 2026 global electric vehicle sales, from 21M units to 28M units. Impacts on oil markets are quantified on page 10.

Overall, our conclusion is that a 10Mbpd annualized disruption in global oil supplies would push prices upwards by $1/bbl per day, until prices surpassed $250/bbl, while almost zeroing global GDP growth.