If the US had not ramped 12Mbpd of shale oil and 90bcfd of shale gas, over the past 10-15 years, we estimate US CPI would have run +0.7% pa higher, due to expansionist monetary policy, and other environmental policies. Hence this 13-page report explores whether the end of shale deflation now points to higher US inflation ahead?

Fifteen years ago, in a world before shale, the top of the global oil cost curve was gas-to-liquids, and the top of the US gas market cost curve was geared off LNG economics. Hence what if the US had never ramped shale?

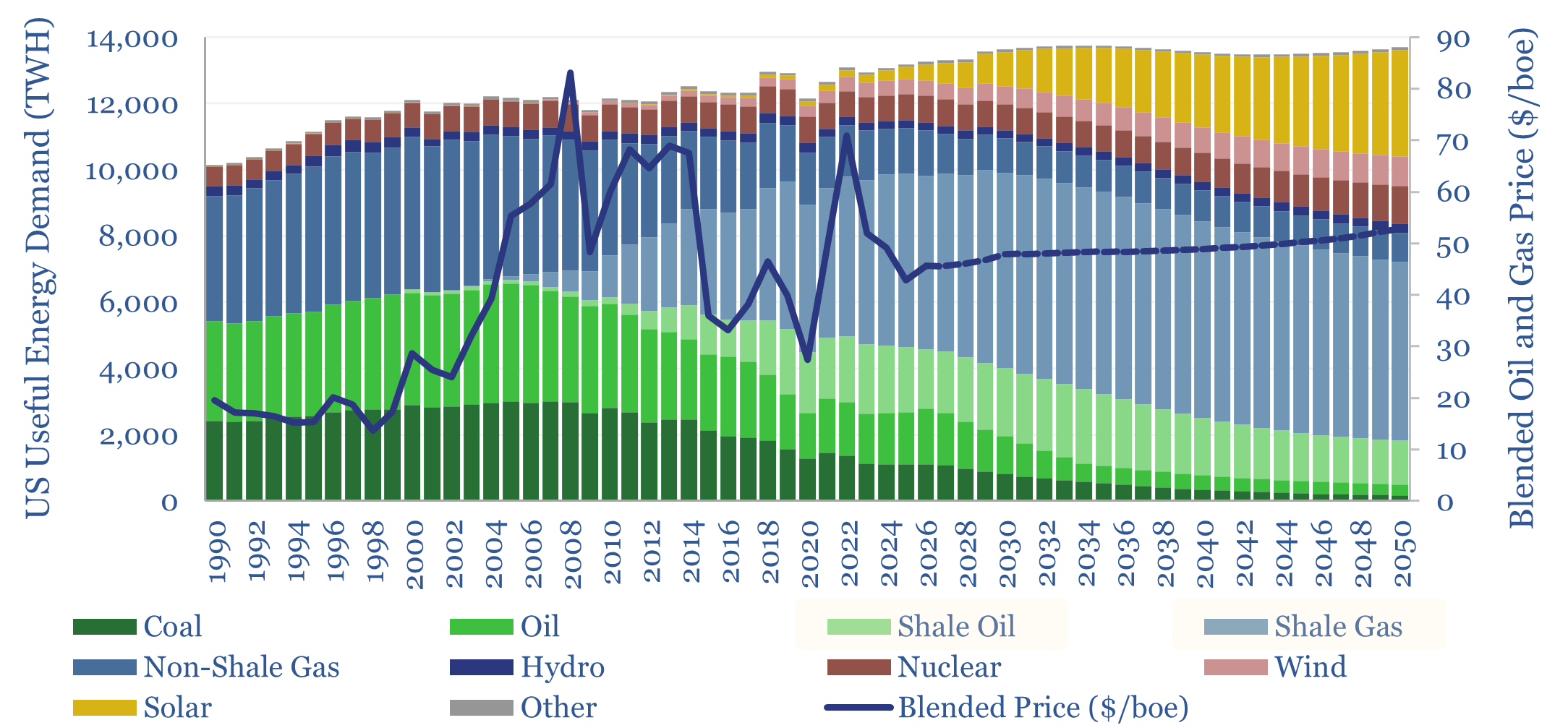

What would oil and gas prices have been, from 2011-2025, in a world without horizontal drilling and hydraulic fracturing in the US? Our answers are on pages 2-4.

The direct cost savings from US shale are estimated at almost $1trn per year across the US, but the total cost savings are higher due to multipliers, as shown by our analysis of the US CPI basket, on pages 5-7. Thus we have derived estimates for how much shale slowed US CPI inflation over the past fifteen years.

Nevertheless, US CPI did rise, with 2.6% pa inflation over this timeframe. We explore whether the inflation can be attributed to monetary policies, or environmental policies, on pages 7-9.

Another impact of US shale has been to stoke the US economy. Real GDP growth rose by 1.8% from 2001 to 2011, but accelerated to 2.6% from 2011 to 2024. What is staggering is that US emissions nevertheless declined by -20% over this timeframe, due to coal-to-gas switching, per page 10.

Looking more globally, shale has brought US energy independence, and reduced the US’s need to ensure global stability in order to stabilize the cost of energy imports. This may augur for a less stable world, with more focus on self-sufficiency and competitiveness, per page 11.

Numerically, it would be impossible for shale to continue providing the deflationary benefits to the US economy, on a go-forwards basis, as it provided in the past. By 2025, signs of resource maturation are also appearing for shale gas and for shale oil. Future inflation implications are discussed on pages 12-13.