US shale gas economics are captured in this data-file, requiring a $2.5/mcf hub-level gas price, for a 10% IRR, on a large, $17M shale gas well in a basin such as the Marcellus. The marginal cost for unlocking c3% pa production growth from key shale basins is likely in a range of $3-4/mcf, but the evidence for cost reinflation is relatively mild.

Shale is a technology paradigm where well productivity has risen by 3-7x over the past decade, through ever greater digitization. The production profiles of wells in the Pennsylvania Marcellus continued to make new all-time highs in 2025 and inform the type curves used in this model.

This data-file breaks down the economics of US shale gas, in order to stress-test the NPVs, IRRs and gas price breakevens of future drilling in major US shale basins (predominantly the Marcellus).

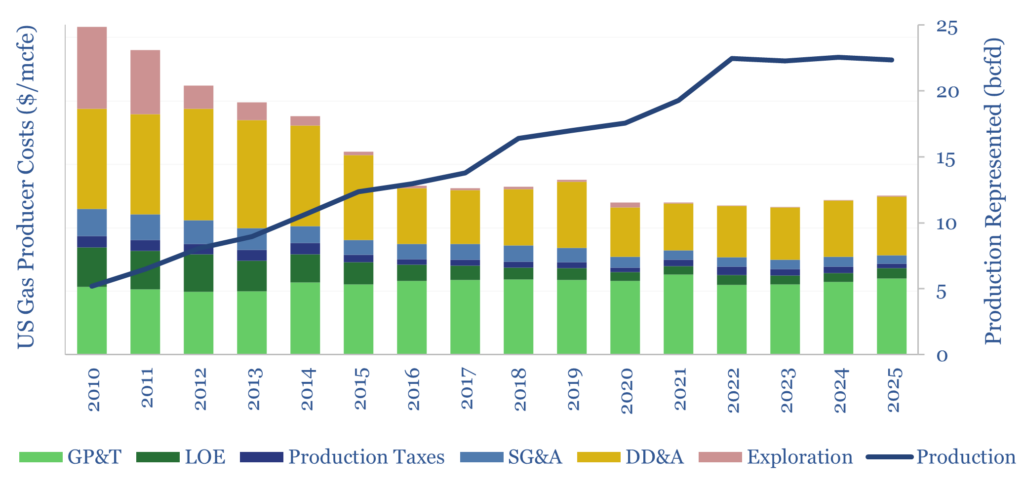

Operating costs of US shale gas production are broken down by aggregating company-level disclosures from seven major US shale gas producers such as EQT, Expand and Range Resources.

Gas production costs halved from 2010 to 2020, due to learning curve effects and increasing economies of scale. Shale gas costs are shown below (in $/mcfe) for Gathering Processing and Transmission (GP&T), Lease Operating Expenses, production taxes, Sales General and Administrative Expenses (SG&A), Depreciation Depletion and Amortization (DD&A) and exploration expenses.

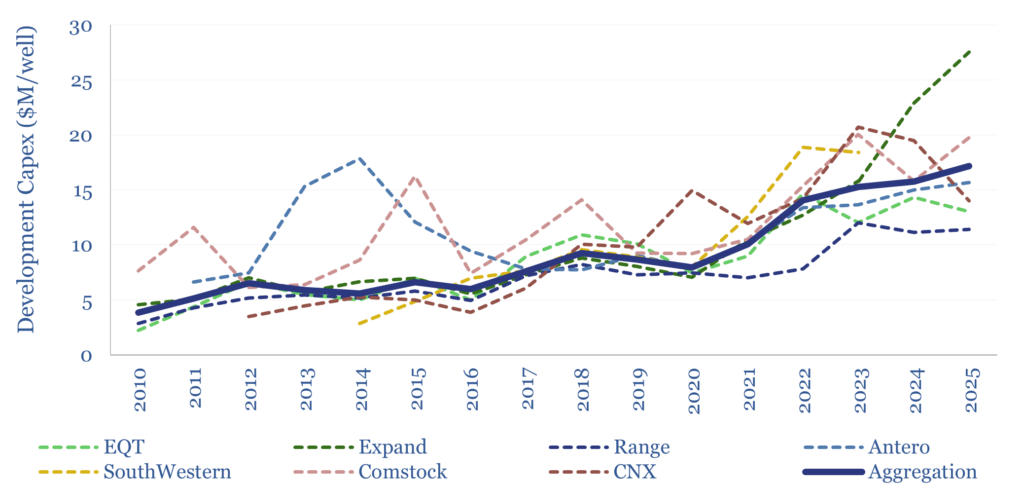

Capex costs of US shale gas production have recently re-accelerated, in order to unlock higher initial production rates and EURs. Capex costs of major producers are charted below. Our model also contains a granular breakdown of capex costs, broken down across 18 components.

We have also published a similar model for the economic costs of US shale oil production, an outlook for US gas demand, and an outlook for US gas supply, as part of our broader shale research.