The CO2 intensity of oil and gas production is tabulated for 425 distinct company positions across 12 distinct US onshore basins in this data-file. Using the data, we can break down the upstream CO2 intensity (in kg/boe), methane leakage rates (%) and flaring intensity (mcf/boe), by company, by basin and across the US Lower 48.

In this database, we have aggregated and cleaned up 957 MB of data, disclosed by the operators of 425 large upstream oil and gas acreage positions. The data are reported every year to the US EPA, and made publicly available via the EPA FLIGHT tool.

The database covers 70% of the US oil and gas industry from 2021, including 8.8Mbpd of oil, 80bcfd of gas, 22Mboed of total production, 430,000 producing wells, 800,000 pneumatic devices and 60,000 flares. All of this is disaggregated by acreage positions, by operator and by basin. It is a treasure trove for energy and ESG analysts.

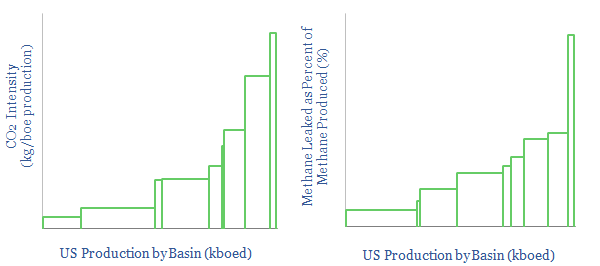

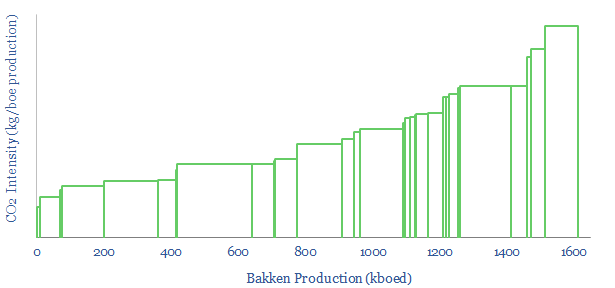

CO2 intensity. The mean average upstream oil and gas operation in 2021 emitted 10kg/boe of CO2e. Across the entire data-set, the lower quartile is below 3kg/boe. The upper quartile is above 13kg/boe. The upper decile is above 20kg/boe. And the upper percentile is above 70kg/boe. There is very heavy skew here (chart below).

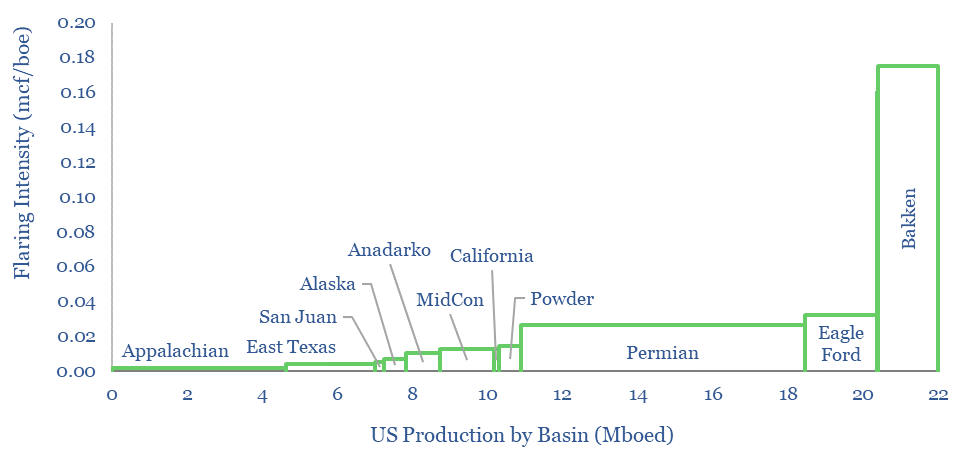

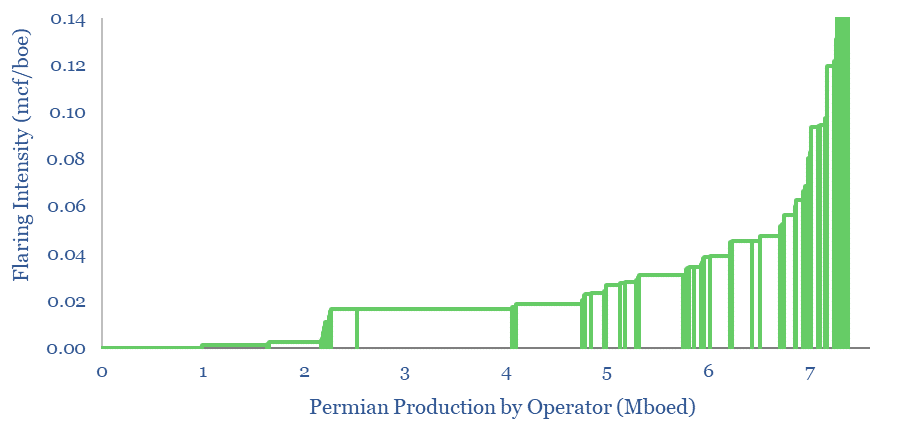

The main reasons are methane leaks and flaring. The mean average asset in our sample has a methane leakage rate of 0.21%, and a flaring intensity of 0.03 mcf/bbl. There is a growing controversy over methane slip in flaring, which also means these emissions may be higher than reported. Flaring intensity by basin is charted below.

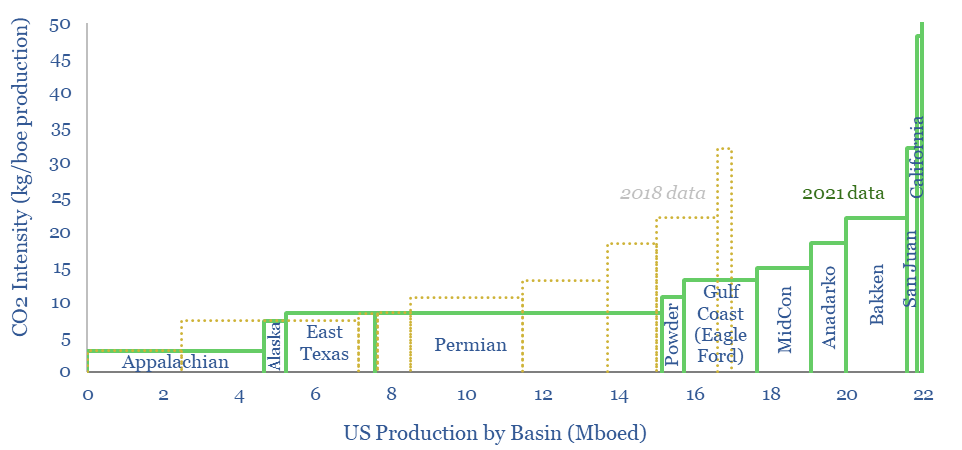

US CO2 intensity has been improving since 2018. CO2 intensity per basin has fallen by 17% over the past three years, while methane leakage rates have fallen by 22%. Activity has clearly stepped up to mitigate methane leaks.

(You can also see in the data-file who has the most work still to do in reducing future methane leaks. For example, one large E&P surprised us, as it has been vocal over its industry-leading CO2 credentials, yet it still has over 1,000 high bleed pneumatic devices across its Permian portfolio, which is about 10% of all the high-bleed pneumatics left in the Lower 48, and each device leaks 4 tons of methane per year!).

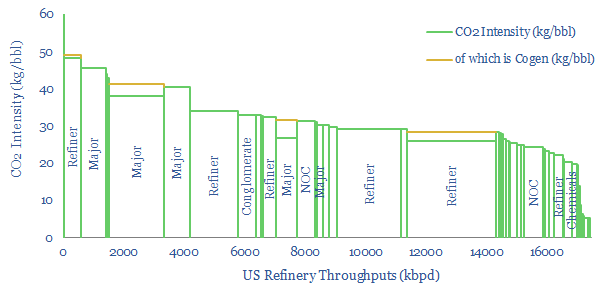

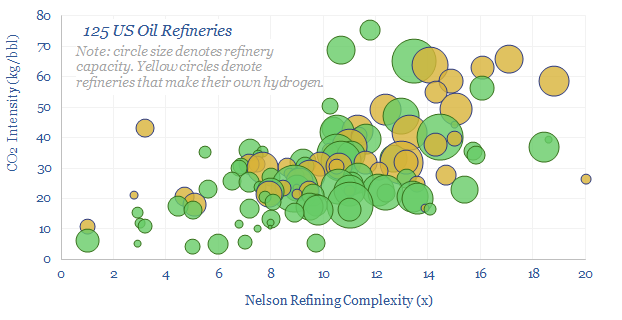

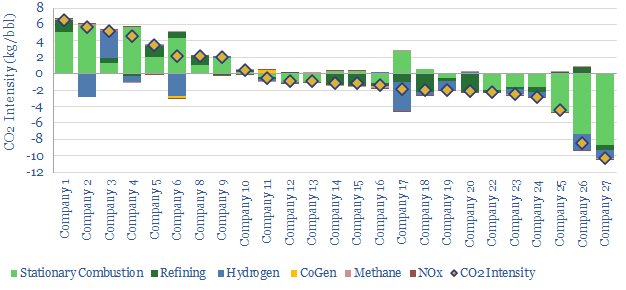

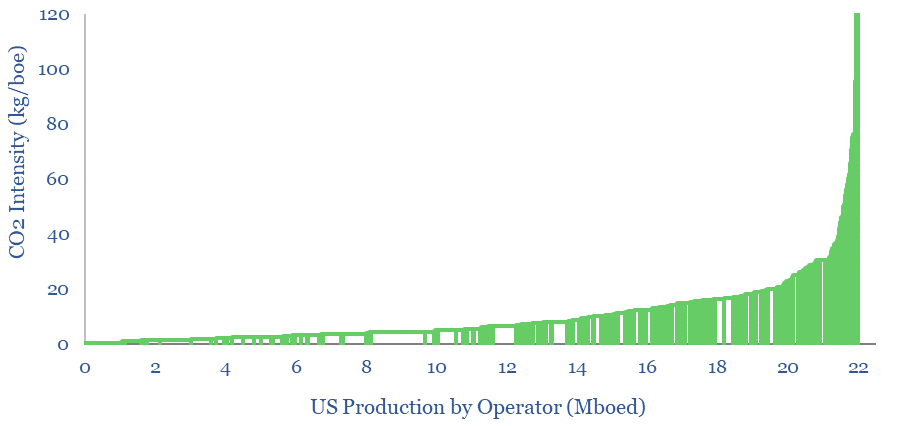

Most interesting is to rank the best companies in each basin, using the granular data, to identify leaders and laggards (chart below). A general observation is that larger, listed producers tend to have lower CO2 intensity, fewer methane leaks and lower flaring intensity than small private companies. Half-a-dozen large listed companies stand out, with exceptionally low CO2 intensities. Please consult the data-file for cost curves (like the one below).

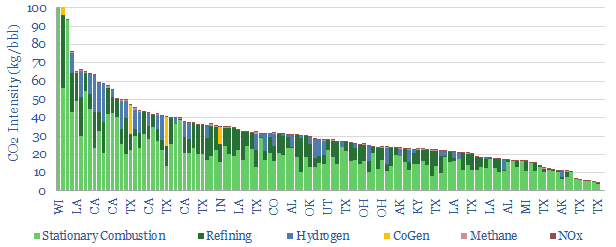

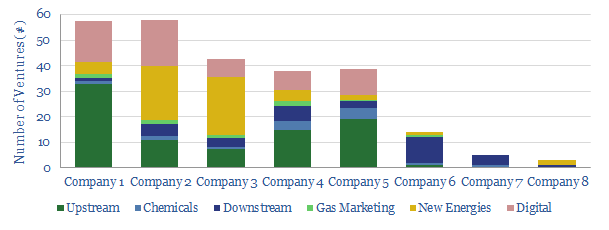

Methane leaks and flaring intensity can also be disaggregated by company within each basin. For example, the chart below shows some large Permian producers effectively reporting zero flaring, while others are flaring off over 0.1 mcf/bbl.

All of the underlying data is also aggregated in a useful summary format, across the 425 different acreage positions reporting in to EPA FLIGHT, in case you want to compare different operators on a particularly granular basis.