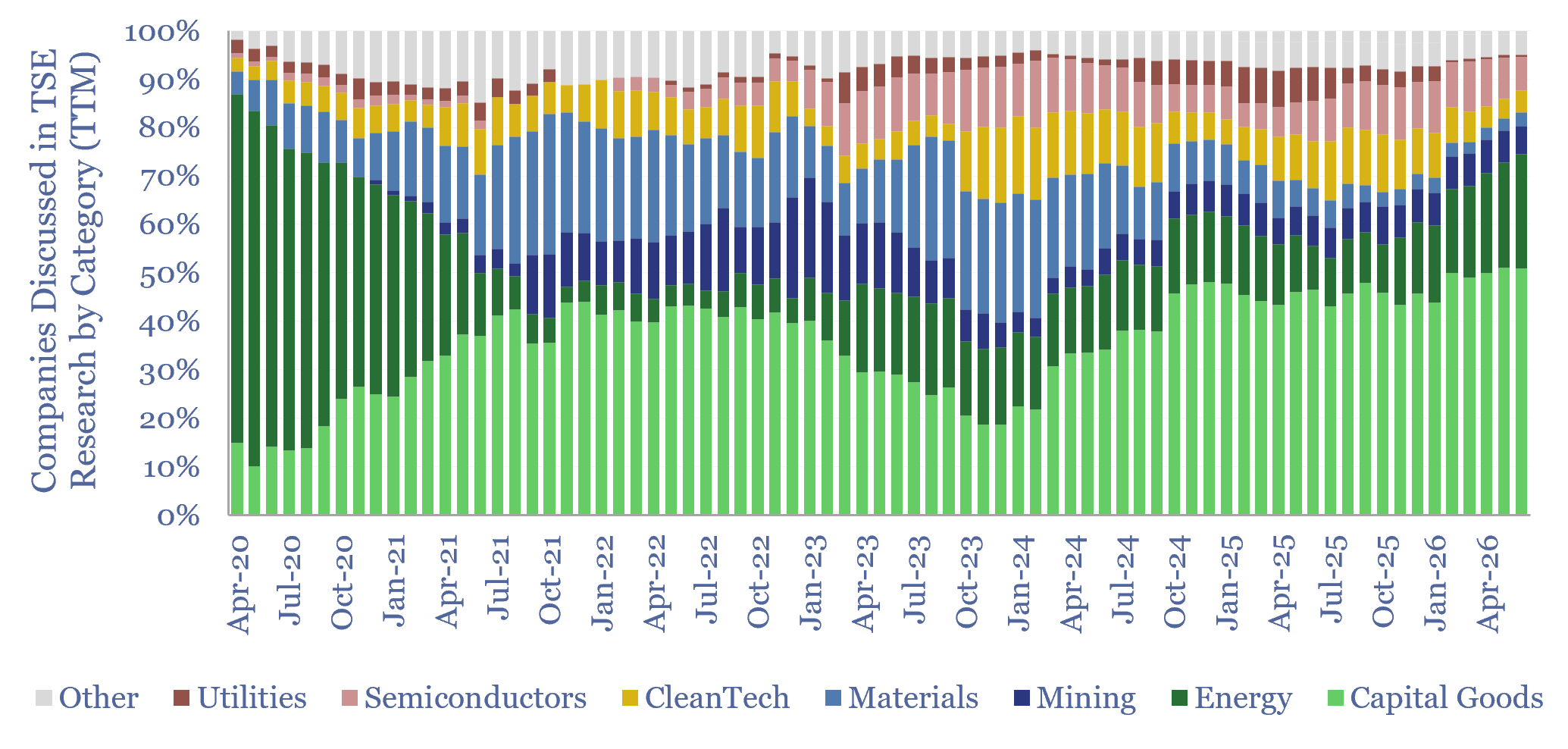

This 12-page report looks back at all of our research from the past year, to draw out our top ten conclusions in energy, industrials and materials. Energy volatility buoys solar and batteries. The ‘AI energy transition’ boosts the physical AI ecosystem more than the data center ecosystem?

As usual, we started this year by publishing our top ten themes for energy in 2026. But the world has changed so much since January that we now need to revisit ten themes for energy in 2H26.

War between the US, Israel, Iran and its proxies started on the 28th of February. This has ignited new fears over energy stability and resource self-sufficiency. Our predictions for the conflict are on page 2.

All roads lead to solar and batteries, amidst energy disruptions, growing demand for self-sufficiency in energy-short regions, and our other major theme which is the AI energy transition.

Where are the opportunities in solar+battery supply chains? Our answer focuses in on select materials where cost curves are changing rapidly, per pages 3-4.

Elsewhere in energy markets, we have revised our outlook for coal, LNG, US gas, global gas turbines, Canadian E&P and new energies, such as next-gen geothermal, which is all covered on pages 5-8.

Another major prediction is that the excitement over AI is shifting away from large data centers to physical devices. At least 80% of the data center pipeline is speculative and ultimately does not get built. Implications of this viewpoint are on pages 9-11.

500,000 AI-related patents were filed in 2025, including by 75% of mega-caps, 54% of large-caps, 31% of mid-caps and 20% of private companies. However we sense that our clients are growing bored by generic statements about AI’s potential. Specific case studies are more interesting. To capture mindshare, you need specific examples. Some of our favorites are on page 12.

Overall, our goal in the report is to distil down our conclusions, and highlight actionable ideas, concisely, for busy decision-makers who have not necessarily had time to read all 250 of our publications from the past year.