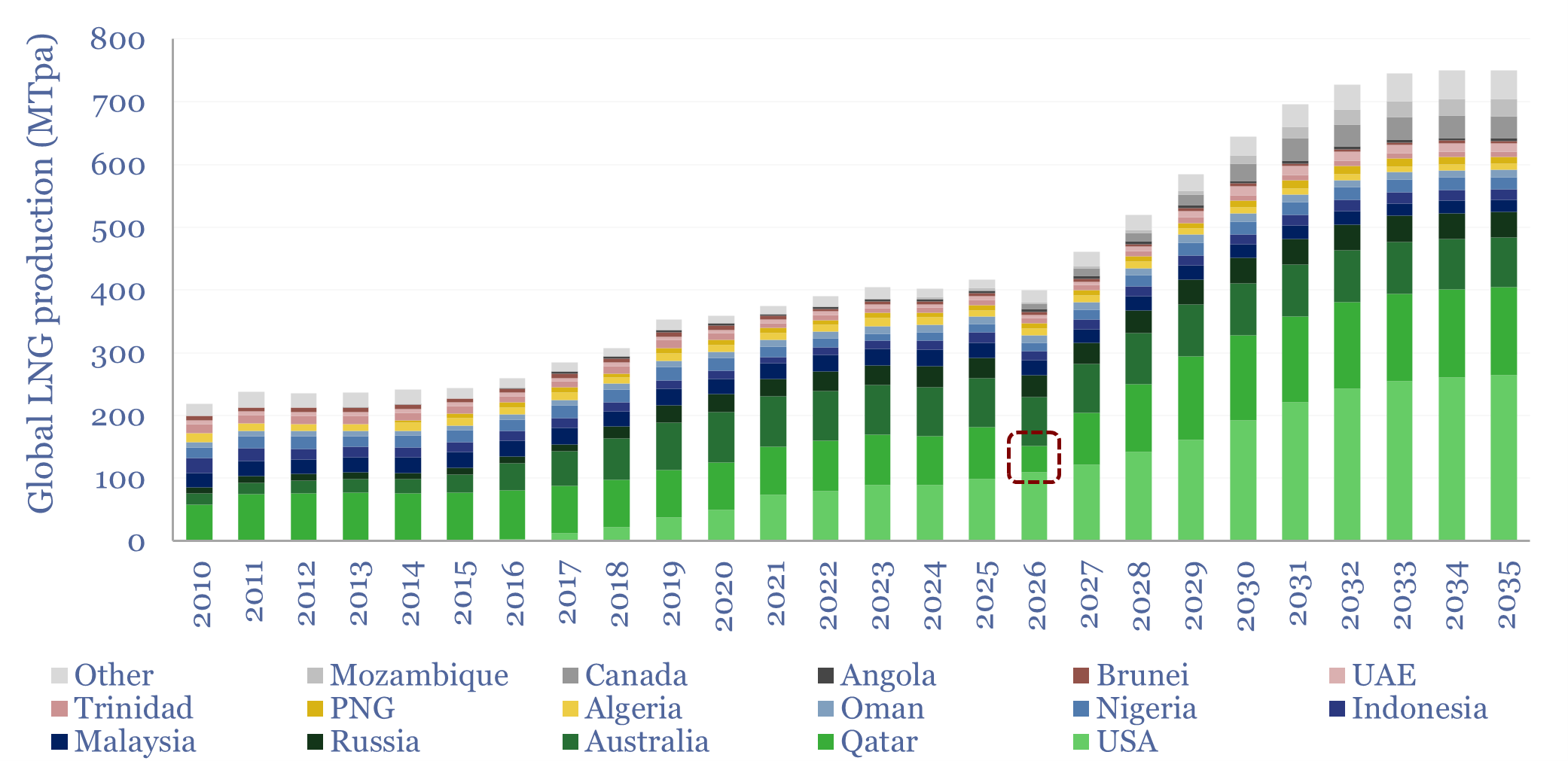

What if Qatar’s LNG output falls by -50% YoY in 2026, i.e., by -40MTpa, which is equivalent to a -0.4% reduction in useful global energy supplies? This 11-page report revisits all of our regional energy models, predicts how each Qatari LNG customer will fill the shortfall and the implications for global energy markets.

Qatar produced 21bcfd of natural gas in 2025, of which 11bcfd was liquefied, to supply the world with almost 80MTpa of LNG. In 2022, we called this the most important energy installation in the world, and worried about escalating chances of a disruption.

On the 5th of March 2026, Qatar’s LNG facilities, at Ras Laffan, were idled as a precautionary measure, after a drone attack, as conflict broke out in the Middle East. In the early hours of the 19th of March 2026, Iran attacked Ras Laffan with missiles, causing “extensive damage”.

Hence our goal in this report is to ask ‘what if’ all Qatari LNG was unavailable to global markets for an entire six-months. This kind of disruption has never happened before in global LNG markets. But what would actually happen?

To answer this question, we look at each region in turn, leaning on our regional energy models, in Europe (page 3), the US, including revised shale forecasts (page 4), in China (page 5), Japan (page 6), India (page 7) and other Asian economies (page 8).

Key themes are that 2026 is not like 2022, when Europe lost a similar magnitude of Russian gas supplies. Impacts of Qatari losses are more distributed, including in countries that are more price sensitive, and have more substitution options, especially coal and solar (see page 9).

The bigger challenges are the products coming from Qatar, derived from its gas, that cannot be replaced, as covered on page 10. We also see rising grid volatility, as grids are deprived of flexible gas and driven towards intermittent solar and less flexible coal. So will this accelerate structural trends in grid modernization? Conclusions and best ideas are on page 11.