Energy importing countries value stable electricity prices. Hence this 18-page report evaluates the optimal grid mix, after taking stability into account? Recent gas price volatility will encourage further diversification for developed world importers, while coal+solar could dominate emerging world growth.

In a research report from June-2024, we argued there was hidden upside in energy marketing portfolios, especially in LNG marketing businesses, because the prices of most commodities have historically been lognormally distributed. Upside volatility exceeds downside volatility.

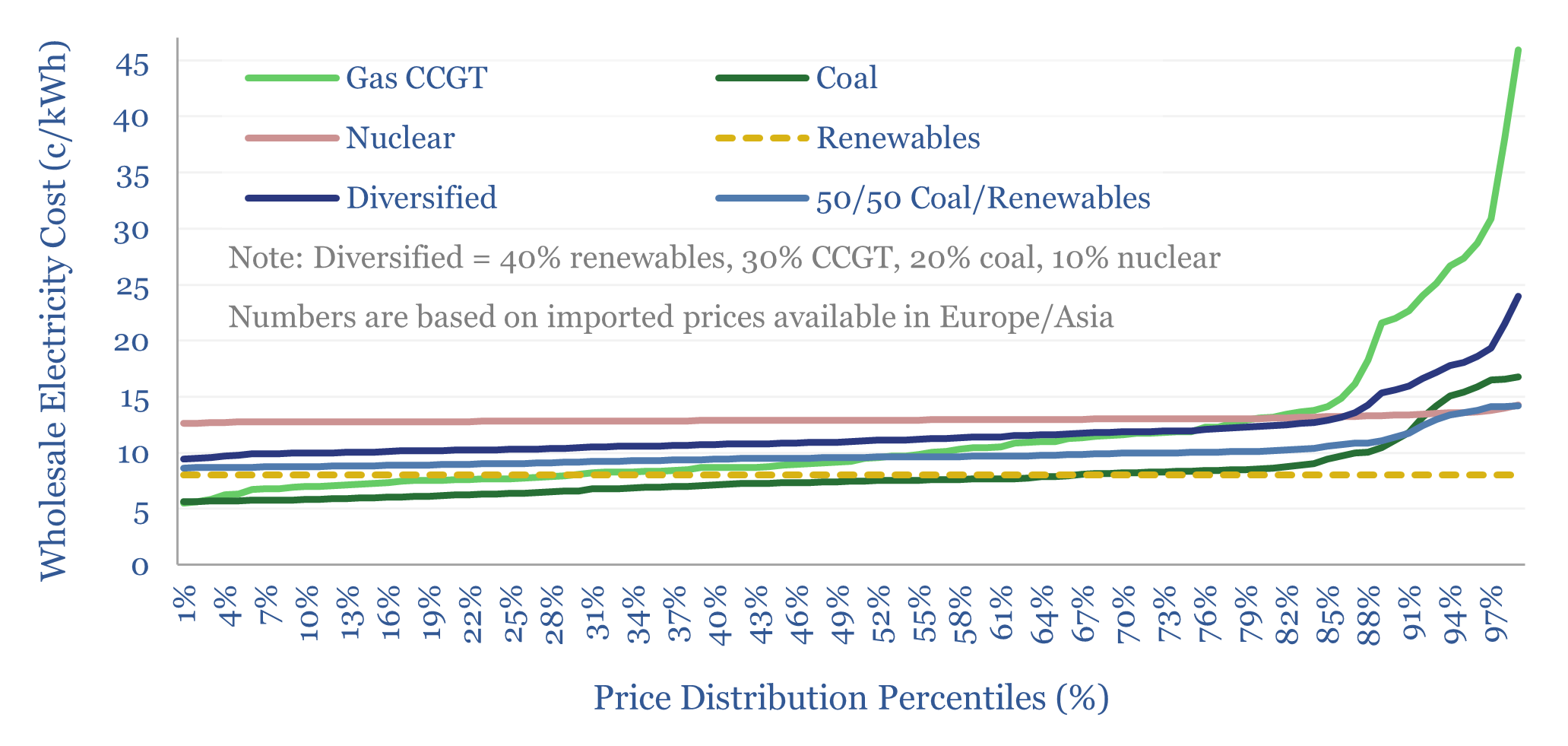

But there is a dark side to upside volatility. It hurts consumers. In turn, after the gas market volatility of 2022, and again in 2026, questions are swirling about the dependability of gas, in importing regions such as Europe, China, Japan, Australia, Korea, and other parts of the emerging world. Importing economies should target moderate but stable energy prices, for the reasons on pages 2-4.

The volatility of electricity prices, from imported natural gas, is quantified on page 5, and in the green line above. For the gas industry, being criticized for price volatility is apt to feel unfair. Especially as government policy in some regions has stifled domestic production, thereby contributing to the very import dependence that is exacerbating the volatility. Nevertheless, our goal in this report is to assess what grid mix is most stable, and how to adapt.

The volatility of electricity prices from other energy sources is then quantified, compared and contrasted with gas, including for nuclear (page 6), coal (page 7), blends (page 8), wind and solar (page 9).

Based on our analysis, Europe is likely to continue diversifying its electricity mix per page 10. Emerging Asia might be justified in industrializing around coal+solar (page 11), which is already happening in India (page 12).

Conversely, for the US, the natural gas super-power, the argument cuts the other way, and the lowest-cost, most stable grid would seem to result from an almost exclusive reliance on gas power (page 13). There is some lesson in here about the value of energy self-sufficiency (page 14).

Overall, our forecasts for coal-to-gas switching are shaken by this analysis. The share of coal in different regions’ grid mixes is re-capped on page 15. China’s coal costs are also now maturing more slowly. Hence we have revised down our forecasts for global gas demand and gas turbine demand, and revised up our forecast for global coal demand and global solar additions, as outlined on pages 15-18. We have also updated our LCOE cost stack.