Coal-to-gas switching halves the CO2 emissions per unit of primary energy. This data-file estimates the CO2 abatement cost. Gas is often more expensive than coal. But as a rule of thumb, a $30-60/ton CO2 price makes $6-8/mcf gas competitive with $60-80/ton coal. CO2 abatement costs are materially lower in the US and after reflecting efficiency. Commodity price volatility in 2022 does not change long-term abatement costs.

Introduction: why do combustion fuels feature in the energy system?

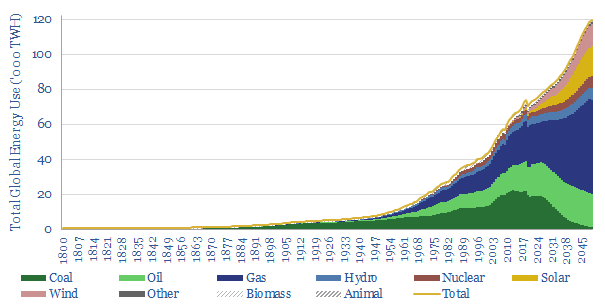

Coal versus gas in the world’s energy system? The year is 2021. The global economy has been slowly recovering from COVID. Total useful energy consumption across all human civilization is running just above 70,000 TWH per year (model here). 26% of that total comes from burning 7.8 bn tons of coal, releasing 19GTpa of CO2, almost 40% of total global CO2 emissions. Conversely, around 33% of the world’s total useful energy comes from burning 390 bcfd of gas, releasing 9GTpa of CO2, or around 18% of total global CO2. These numbers are remarkable in themselves.

As part of the energy transition, we are going to move Heaven and Earth, to ramp wind, solar, next-gen nuclear, biofuels, other renewables, electrification and other efficiency initiatives. As much as possible. As quickly as possible. This all goes without saying.

But if you simply do the numbers on supply and demand, 65% of the world’s useful energy in 2050 is still going to come from burning some kind of combustion fuel. So which fuel is most pragmatic, and how do we minimize the costs of the energy transition?

What is the CO2 intensity of coal versus gas?

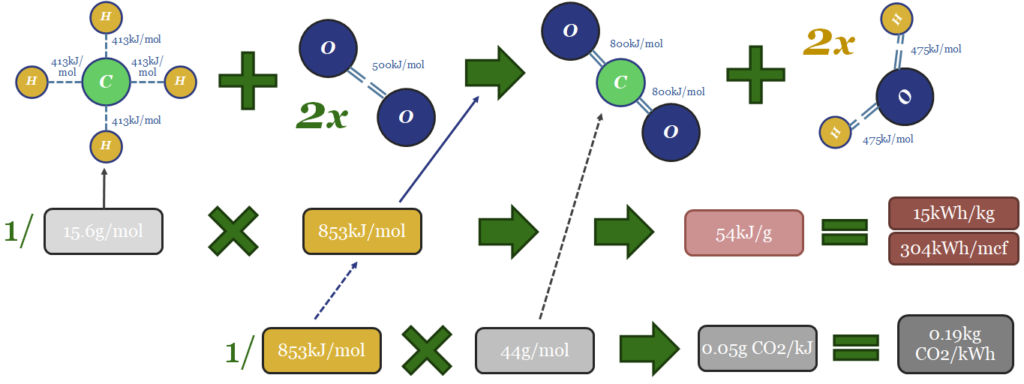

Gas is a 50% lower-carbon combustion fuel than coal. The reason is that 54% of all the energy in the methane molecule (CH4) comes from the hydrogen atoms, which combust into innocuous water vapor.

Hydrogen atoms are 12x lighter than carbon atoms. Thus burning 1 ton of natural gas (CH4) releases 2x more energy than burning 1 ton of pure carbon (C), in the form of the world’s purest petcokes and anthracites.

Stated another way, CO2 intensity is around 0.18 kg/kWh-th when combusting natural gas and around 0.37 kg/kWh-th when combusting coal. You can explore these numbers further by delving into the chemistry of bond enthalpies.

Historical costs of coal-to-gas switching?

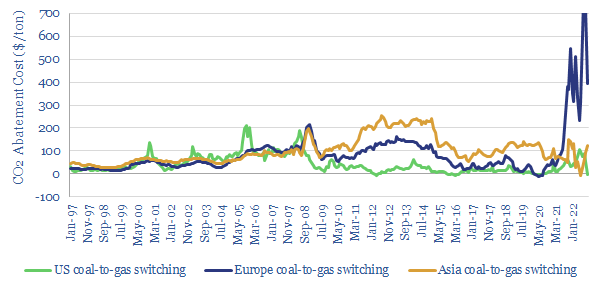

Switching coal for gas is most likely going to halve CO2 intensity per unit of energy, when combustion fuels are needed in the energy system. But what is the cost? The first way to answer this question is to turn to history, which we have aggregated in this data-file (chart below, updated through YE23 in the data-file).

The most relevant numbers on the chart above come from Europe and the US during the relatively stable decade from 2010-2019.

In the US, the price of delivered coal averaged $43/ton over the 2010-2019 timeframe, according to data from the EIA, which translates into a ridiculously cheap 0.7 c/kWh of thermal energy (kWh-th). Over the same timeframe, the average price of natural gas was $3.3/mcf, which translates into 1.1 c/kWh-th. Thus the excess cost of natural gas was around 0.4 c/kWh-th. Directly substituting coal fuel for gas fuel therefore incurred a cost of $20/ton of CO2 that was ‘avoided’. This is low on our CO2 abatement cost curve.

In Europe, the price of imported coal averaged $87/ton over the 2010-2019 timeframe, which translates into 1.2 c/kWh-th. The price of gas averaged $8.2/mcf, which translates into 2.7c/kWh-th. Thus the premium for natural gas was around 1.5c/kWh-th. Directly substituting coal fuel for gas fuel therefore incurred a cost of $80/ton of CO2 that was avoided.

In Japan, for completeness, the price of imported gas was higher than in Europe, at $12.2/mcf in 2010-19, resulting in a coal-to-gas switching cost of $150/ton of CO2 avoided. This was due to distorting impacts of the Fukushima nuclear disaster, which suddenly shut down 300 TWHpa of Japanese nuclear capacity (overview here), whose direct replacement with gas would have required the equivalent of 40MTpa of LNG imports, over 10% of overnight tightening in global LNG market.

Philosophical problem #1: historical volatility?

Commodity prices volatility raises a philosophical problem for assessing the CO2 abatement costs (or “green premiums”) of replacing one type of fuel with another. Historical prices are volatile. They vary vastly. Thus our ‘switching costs’ are apparently changing all the time.

2022 has been a sobering reminder of volatility, as European gas prices spiked to $70/mcf in August-2022, at which time, the ‘CO2 abatement cost’ for replacing coal with gas spiked to $1,000/ton of CO2 avoided. But this is clearly not a good long-term basis for generalization. The medium-term future is more important than the recent past.

Beware of over-generalizing in strange times. In my teenage years, I was a keen cross-country runner. Keen but not brilliant. I never quite figured out how to ‘pace myself’ so that I had enough energy to sprint the final stretch. I would often come in the “top five” of regional meets. There were always one or two runners, at other schools, who would outpace me, as we traversed the fields and forests of the Greater London Area. But I did actually win a race on precisely one occasion. After an outbreak of norovirus at a rival school!! In that precise moment, it might have been tempting to declare myself “the fastest teenager in the Greater London Area”. But sadly, by the next week, I was back to fourth or fifth place.

In a similar vein, it seems unfair to under-invest in gas for a decade, see gas markets fall into deep under-supply as a result of that under-investment, see prices spike to record levels in 2022; and then criticize “gas is too expensive to be a decarbonization fuel”. It is expensive because of historical under-investment, which has also allowed Russia to weaponize its supplies. Effectively, 2022 is the “gas industry with norovirus”.

If you think about how supply-demand dynamics work, then the more gas you build, then the lower the future CO2 abatement cost of coal-to-gas switching will be. Whereas the less gas you build, and the more under-supplied gas markets are, then the higher the CO2 abatement cost of coal-to-gas switching will be. The outcome is path-dependent!

What future-minded decision-makers should care about is go-forwards costs. In other words, what is the medium-long term outlook, if you are deploying new capital, with a multi-decade time horizon?

Go forwards: what CO2 abatement costs from switching coal to gas?

On a go forward basis, the US can likely ramp from 90bcfd of gas production in 2021 to 130-150bcfd of gas production by mid-late decade (model here). The marginal hub-level cost to ramp US shale gas is $2-3/mcf (model here).

Thus if coal costs $40-60/ton, the CO2 abatement cost for switching coal to gas is effectively zero in the US (download this data-file to stress test). Replacing coal with gas halves CO2 and adds almost no primary energy cost.

This is why US coal production has already fallen from 1 GTpa in 2000-2008 to 500MTpa in 2021 (model here). US CO2 emissions have fallen from 6.8 GTpa to 5.8GTpa over the same timeframe, of which 65% is directly due to coal-to-gas switching.

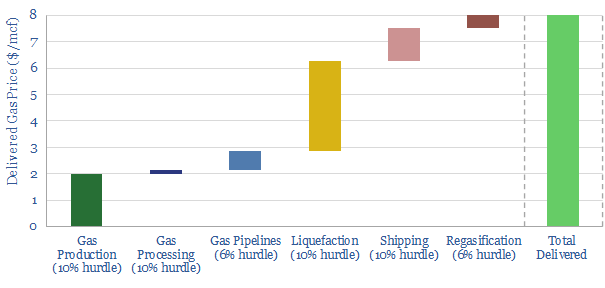

Europe is likely to be short of gas throughout the 2020s. However, the relevant go-forwards is about signing new LNG import agreements. We have pieced together the end-to-end costs of producing, purifying, piping, liquefying, shipping and regassing US LNG (chart above). Across the value chain, delivered prices of $8/mcf are a realistic aspiration.

If future European coal prices average $60/ton, then the extra cost of switching coal to gas would be $90/ton of CO2 saved. If future European coal prices average $90/ton, then the extra cost of switching coal to gas would be $60/ton of CO2 that is saved.

This is all on a primary energy basis, in kWh of thermal energy. But we can achieve better numbers by considering the market on a useful energy basis (for more on the difference between primary energy and useful energy, see our energy efficiency overview).

Philosophical problem #2: useful energy versus primary energy?

The primary energy numbers quoted above are almost certainly too conservative for gas and too generous for coal. The reason is that the energy efficiency factor will almost certainly be higher for gas than coal. In other words, to produce each kWh of useful energy requires less primary gas energy than primary coal energy.

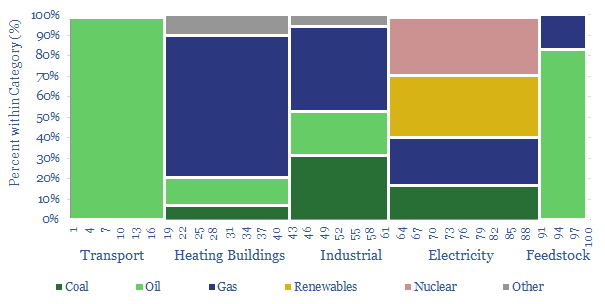

Heating buildings comprises a staggering 25% of all useful energy consumption in Europe (chart below, data here). Now consider some options: A home might have a gas boiler, which is over 90% efficient, in converting the thermal energy from natural gas into heat. Quite high. But very few buildings in Europe or the US have coal furnaces. If you are relying on coal to heat buildings, it is likely by burning the coal in a 40-45% efficient power plant (model here), then transmitting the electricity via a 93% efficient power grid, then using the electricity in a >95% efficient electric heater. So overall, the gas value chain is over 2x more efficient. And the CO2 abatement cost of gas versus coal is zero. Or below zero. Switching back to coal, due to a shortage of gas, adds cost.

For electricity generation our base case assumptions is that the average modern gas turbine will achieve 57% electrical conversion efficiency, while the average modern coal-fired power plant likely achieves 42% efficiency. Thus, on a pure ‘spark spread’ basis, Europe likely needs a CO2 price of $35/ton to incentivize running an existing gas-fired power plant at $8/mcf gas, rather than running an existing coal-fired power plant at $75/ton coal.

Philosophical problem #3: context and ranges?

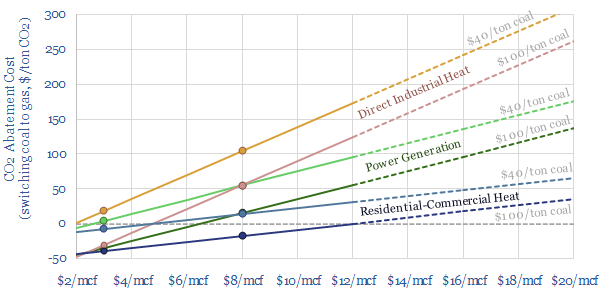

Coal-to-gas switching halves CO2 emissions per unit of primary energy. As a global rule of thumb, a $30-60/ton CO2 price makes $6-8/mcf gas competitive with $60-80/ton coal. While in North America, and in many specific contexts, the CO2 abatements costs can be less than zero.

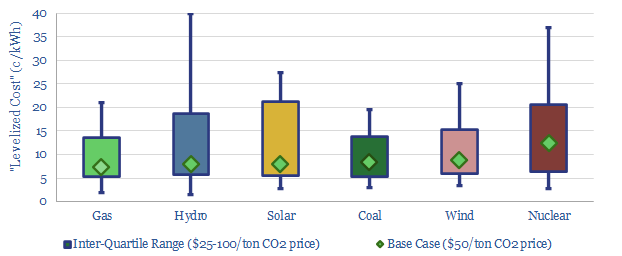

Broad numerical ranges are not very satisfying. But we think they are more appropriate than overly-precise point estimates, given the wide variations in context (for a good discussion, we have recently written up why we ‘hate’ levelized costs, chart below).

The complexity of the counterfactuals for coal-to-gas switching are genuinely interesting. For example, if we have a chemicals or manufacturing plant in coal-consuming Germany or China, should we be modelling the costs of supplying gas to that plant; or shutting it down, and re-locating its output to a gas-rich nation, such as the US or Middle East? (note here). Does the new investment require new costly infrastructure or deflate unit costs for pre-existing infrastructure? (note here). The real world is more complicated than our spreadsheets.

Please download this data-file to stress test some simple relative costs of coal-to-gas switching. The model contains a simple calculator, where you can input gas prices, coal prices, CO2 prices and efficiency factors. It contains historical data on the CO2 abatement costs of coal-to-gas switching in the US, Europe and Asia. And it contains a more elaborate model of full-cycle power generation using coal versus using gas.