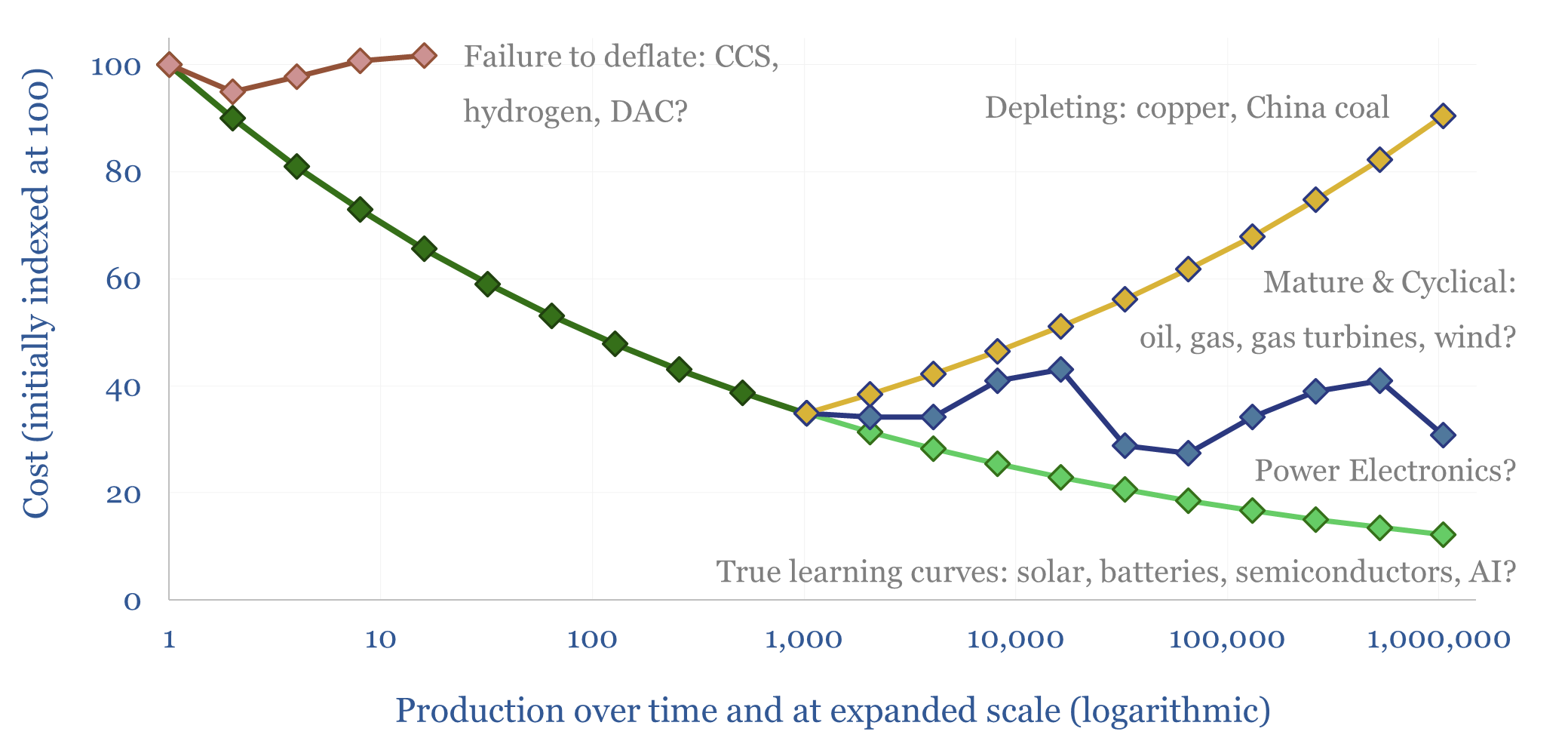

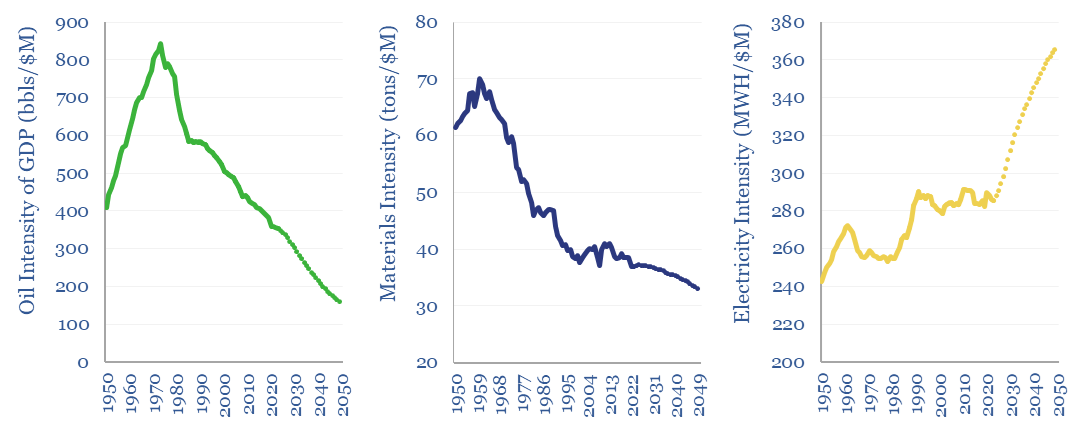

How much of the market’s current disenchantment with new energies can be attributed to persistently high costs, which failed to deflate as much as hoped? This 15-page report reviews the evidence. Cost trajectories have varied. CCS and hydrogen cost more than initially advertised. Wind costs recently re-inflated. Yet, solar, electronics and lithium ion batteries remain exceptional?

Read the Report?

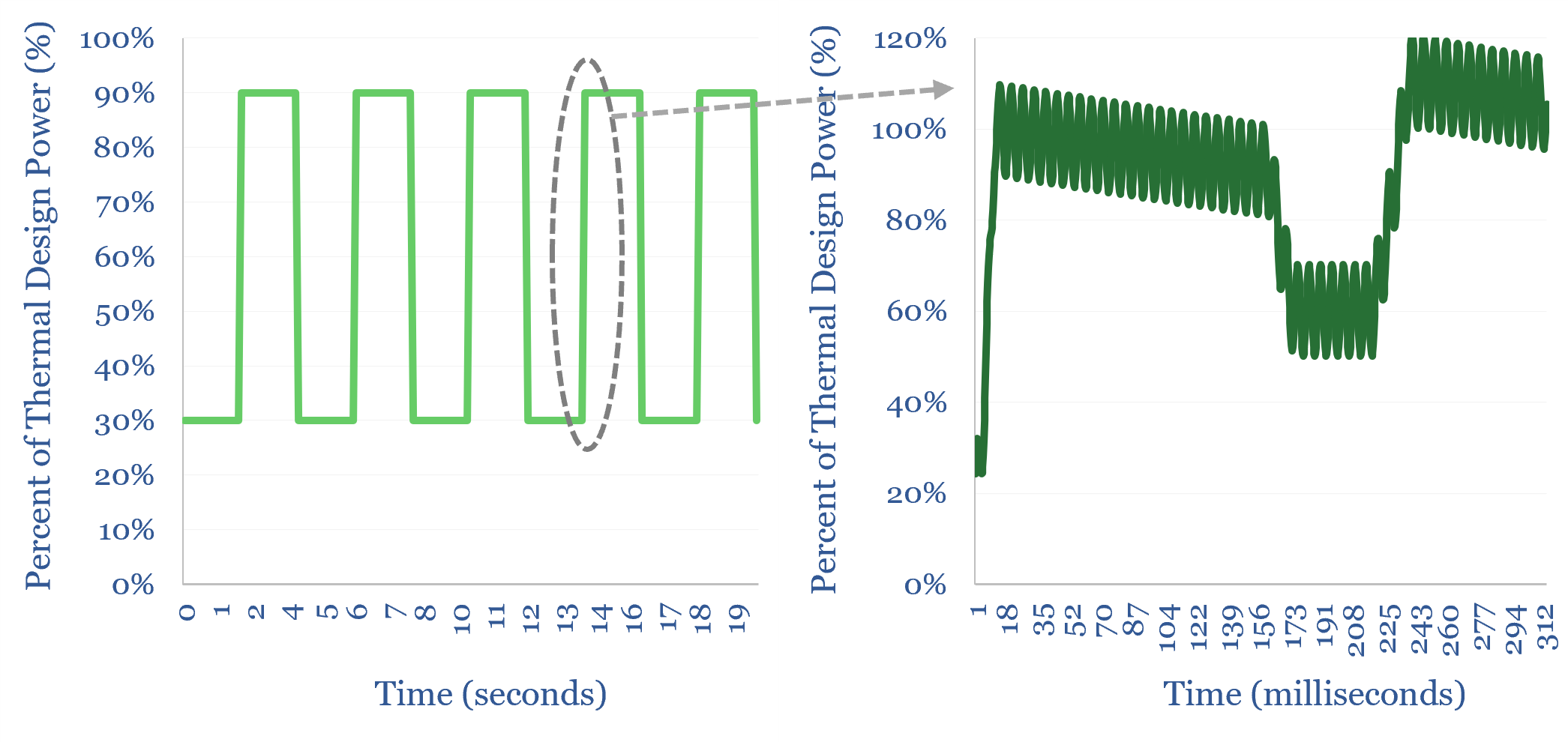

Everybody knows “AI data centers use round-the-clock power”. Yet one of the biggest power challenges for AI data data centers is precisely that they do not use round-the-clock power. They incur large load transients that cannot be handled by batteries, power grids or most generation. This 15-page report explores data center load profiles, which may require 5-10x more capacitors?

Read the Report?

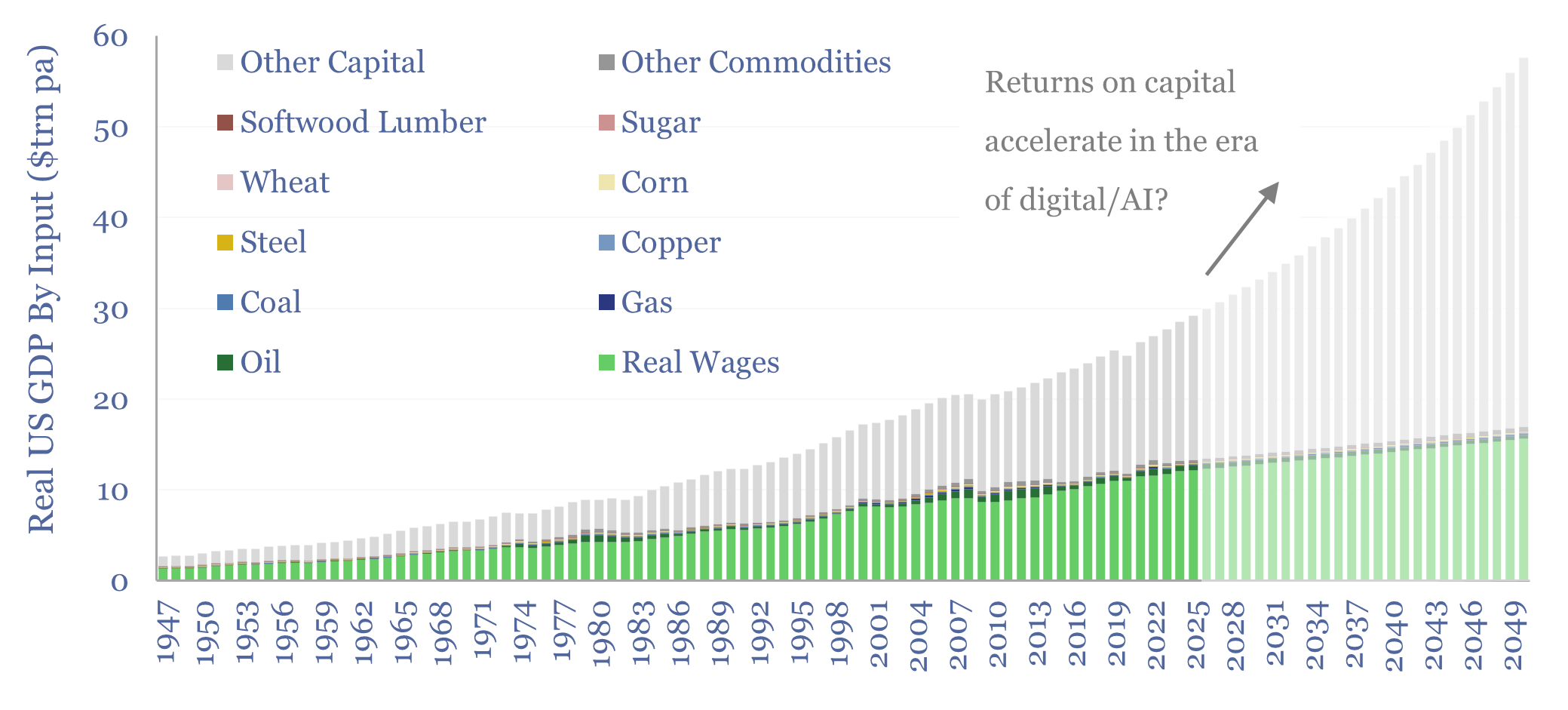

Energy transition remains among the most important and exciting topics in the world. But it is now less driven by Net Zero ambitions, and more so by digital and AI technologies. These offer world-changing possibilities; re-accelerating GDP, returns on capital, and commodities. This 13-page report captures our latest outlook on energy transition, and the opportunities therein.

Read the Report?

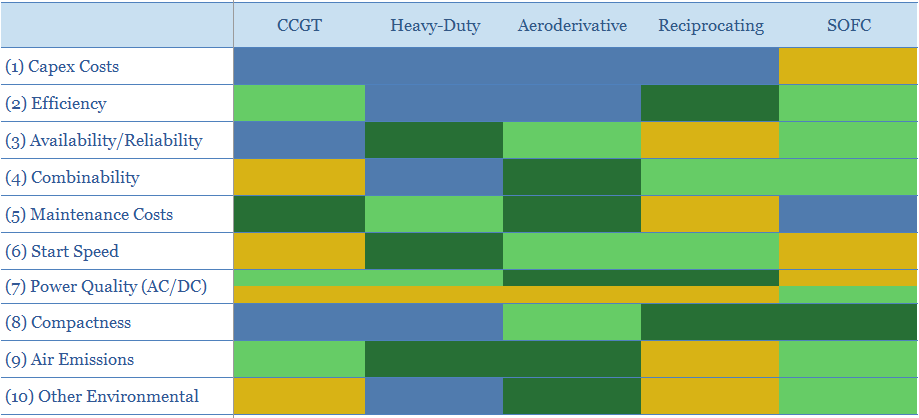

This 20-page report compares combined cycle gas turbines (CCGTs), heavy-duty gas turbines, aeroderivative gas turbines, reciprocating engines and solid oxide fuel cells (SOFCs), on ten dimensions. No one gas generation technology is best. But modular solutions may increasingly rival CCGTs, especially for energizing AI data-centers?

Read the Report?

What if AI re-shaped the power grid? This 16-page report sees potential to halve levelized T&D costs; de-bottleneck 4.5% pa of global electricity demand growth; and shift over $100bn pa of spending away from high-voltage capital goods to low-voltage smart devices and networking equipment.

Read the Report?

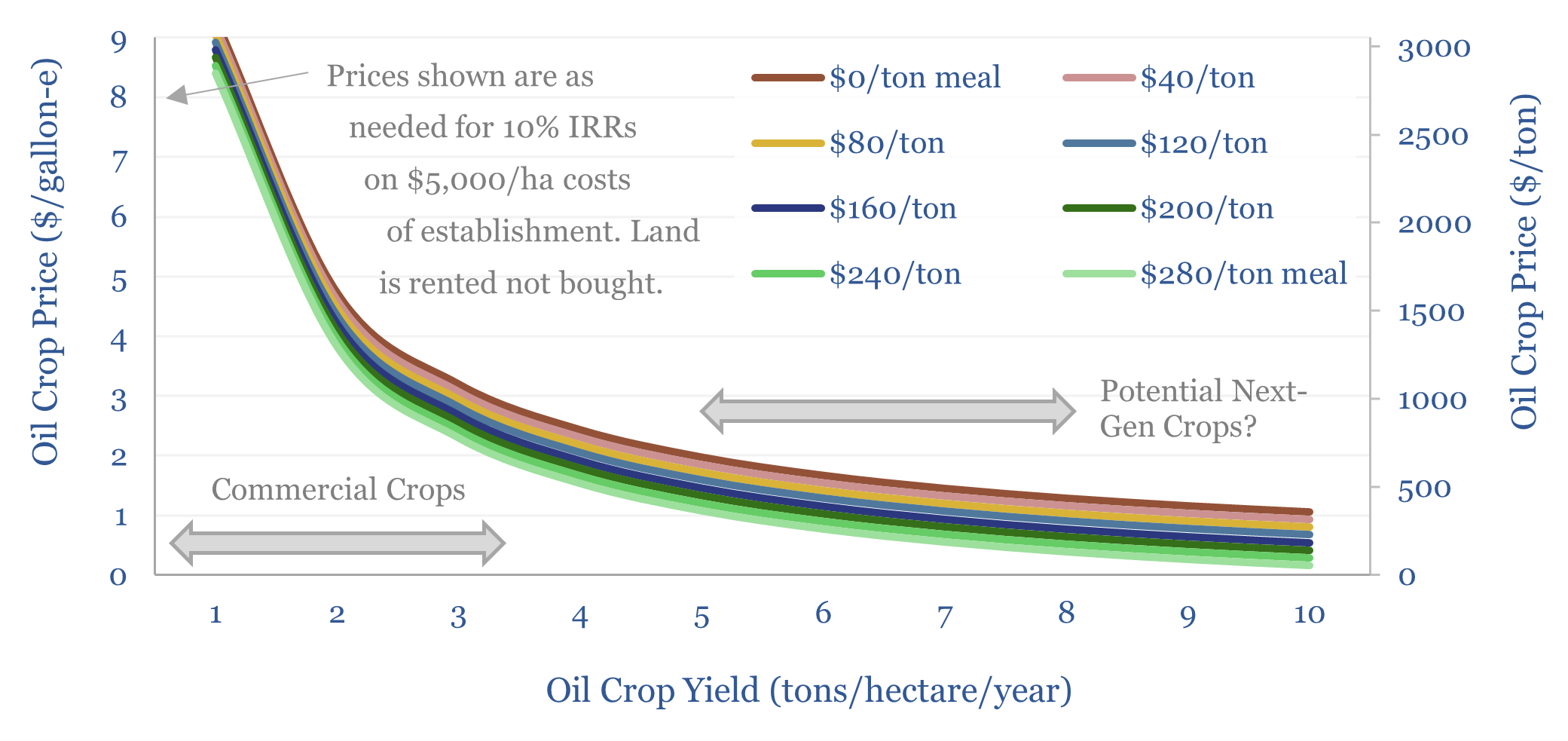

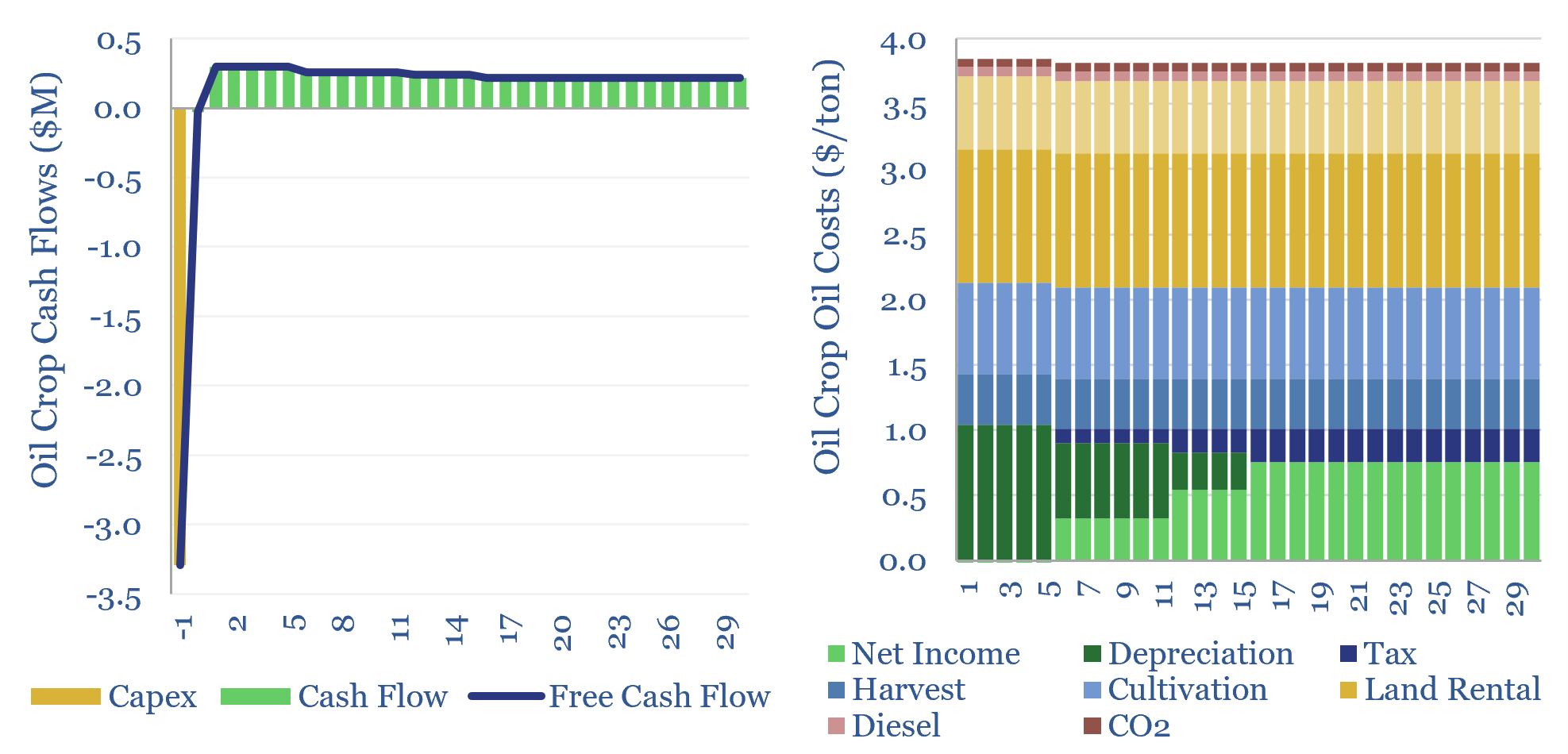

As things stand, we argue Europe will be forced to scale back its SAF targets, due to Sustainable Aviation Fuel costs and land constraints. However, our 17-page report asks what could improve the outlook. Specifically, what yields, costs and other properties would we need to see from an oil crop to get excited about unlocking cost-competitive HEFA-SAF? And could any novel crops, such as Pongamia or Carinata, take flight?

Read the Report?

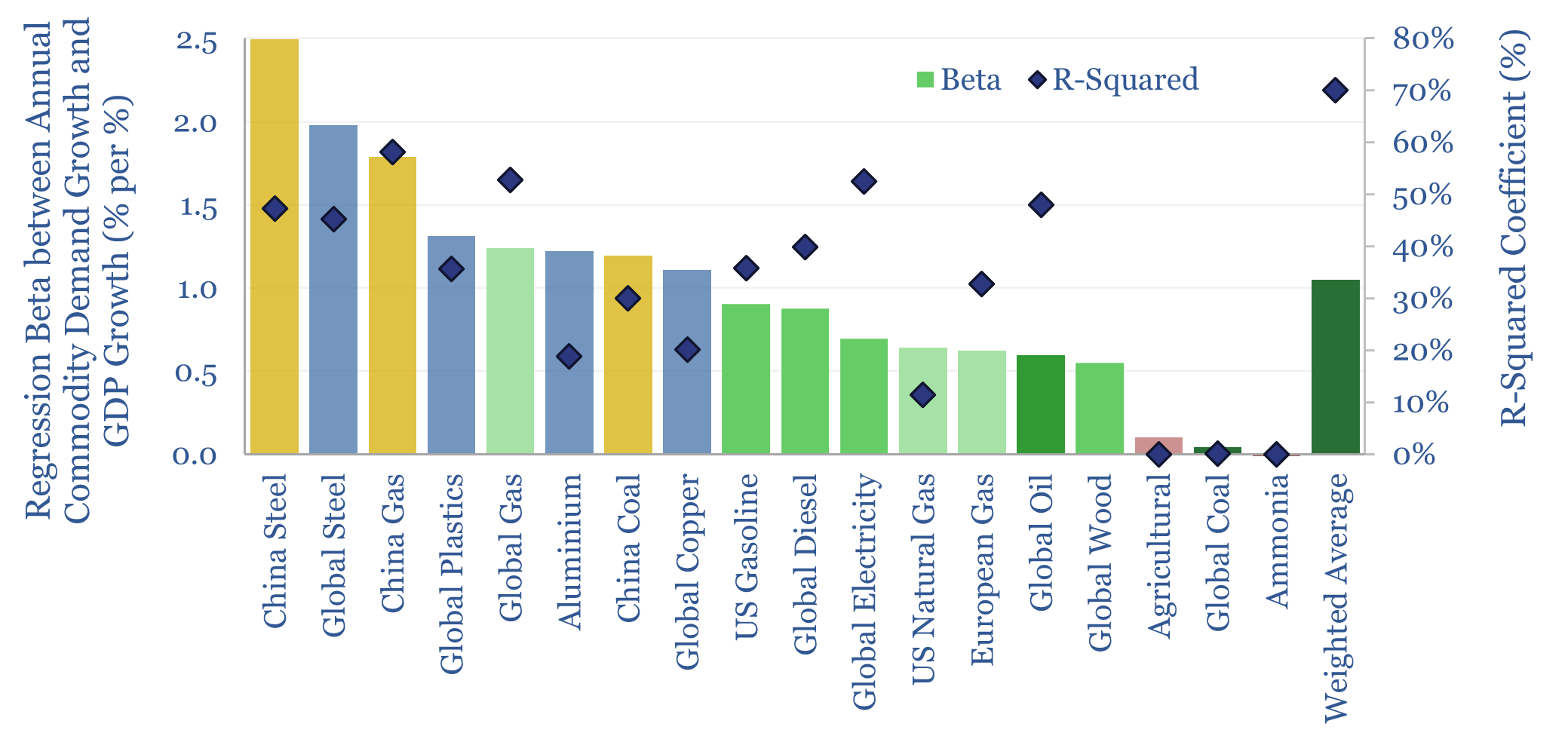

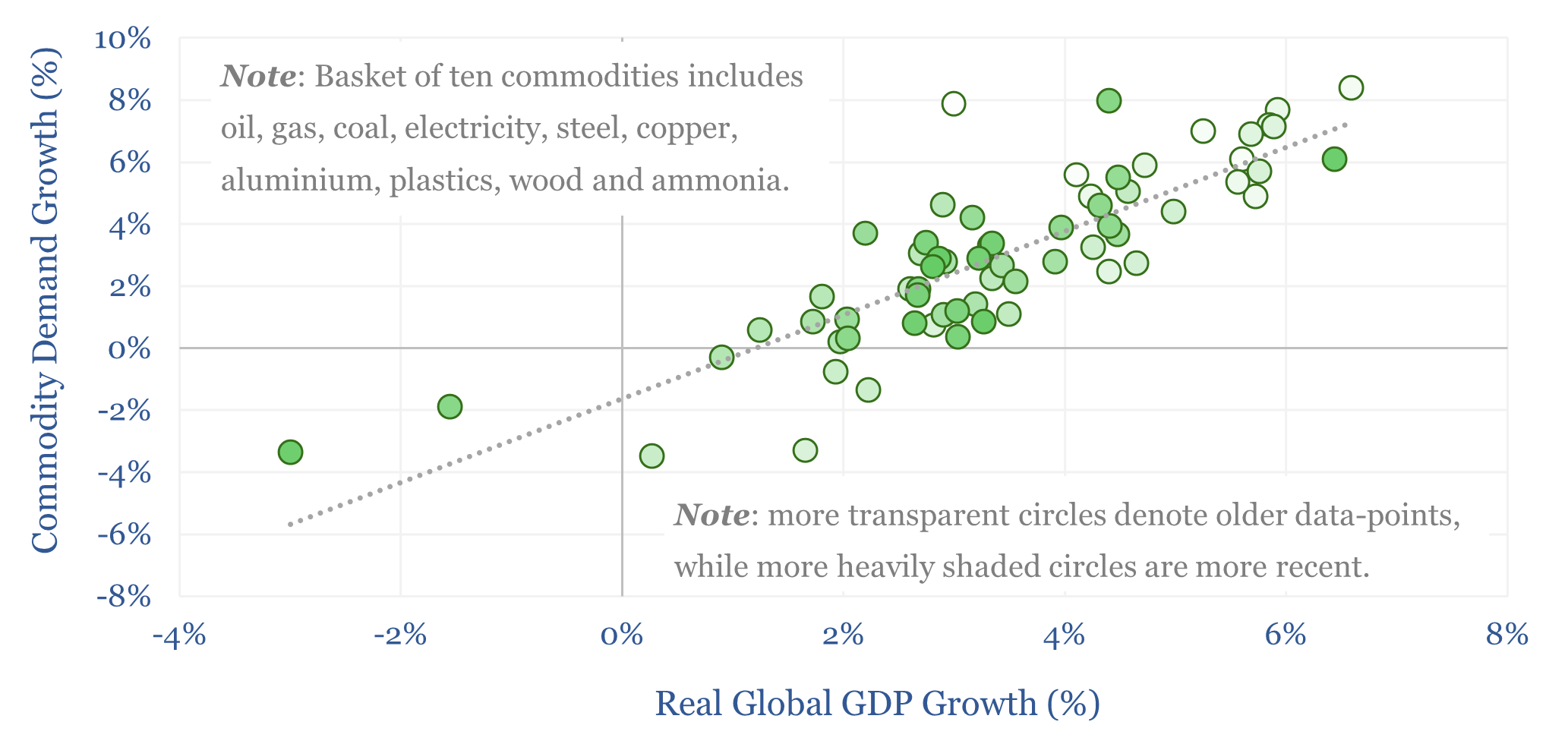

How sensitive is global commodity demand to GDP growth? This 15-page report runs regressions for 25 commodities. Slower GDP growth matters most for oil markets, which are entering a new, more competitive, era. China is also slowing. But we still see bright spots in gas, metals, materials in our 2025 commodity outlook.

Read the Report?

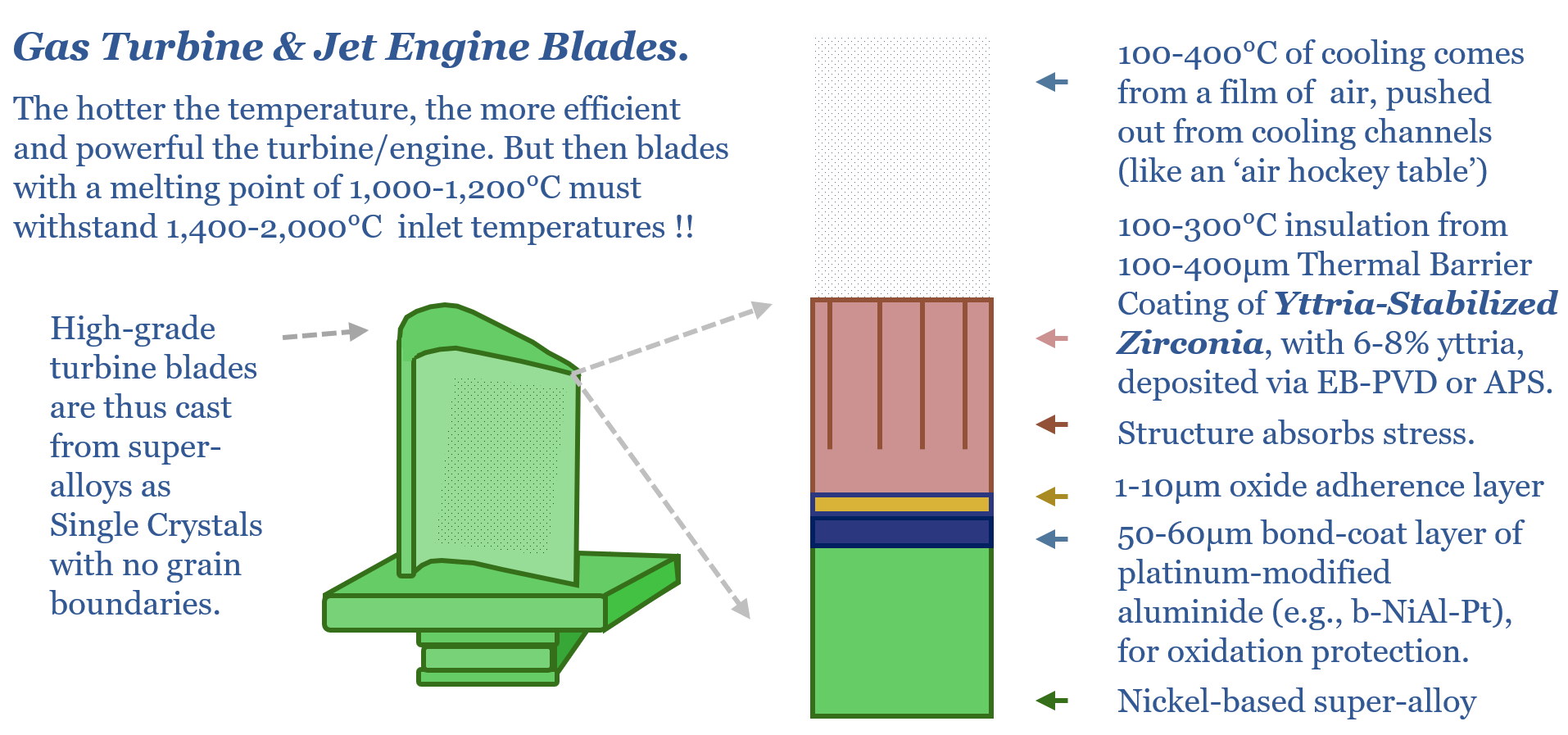

Global yttrium output is just 10-15kTpa, worth $100M pa, of which c90% is controlled by China. Yet a supply disruption for this critical metal could have ripple effects comparable to an oil shock: de-railing developed world load growth, aircraft manufacturing and the rise of AI? This 15-page report tells the story of yttria-stabilized zirconia, explores supply risks, and their implications.

Read the Report?

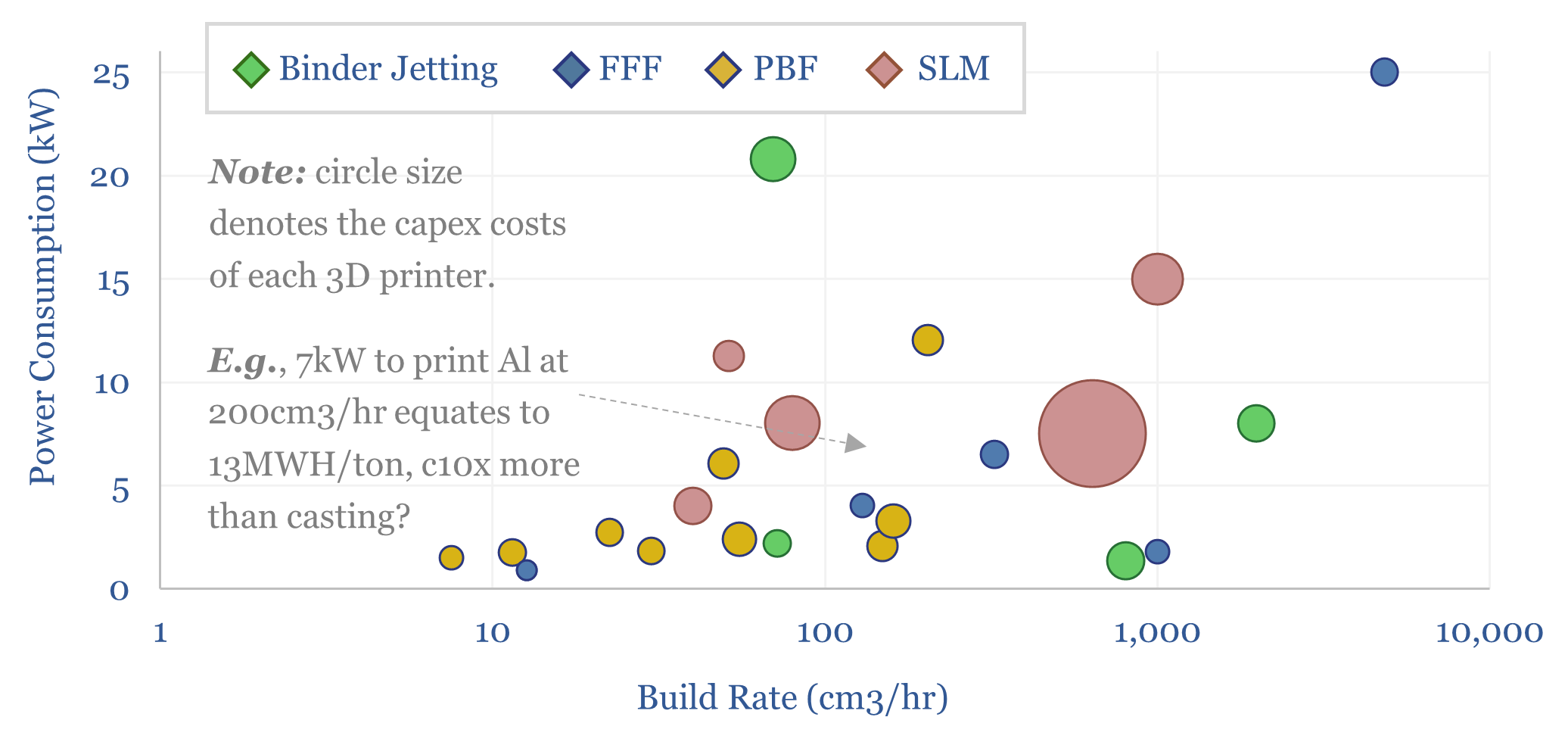

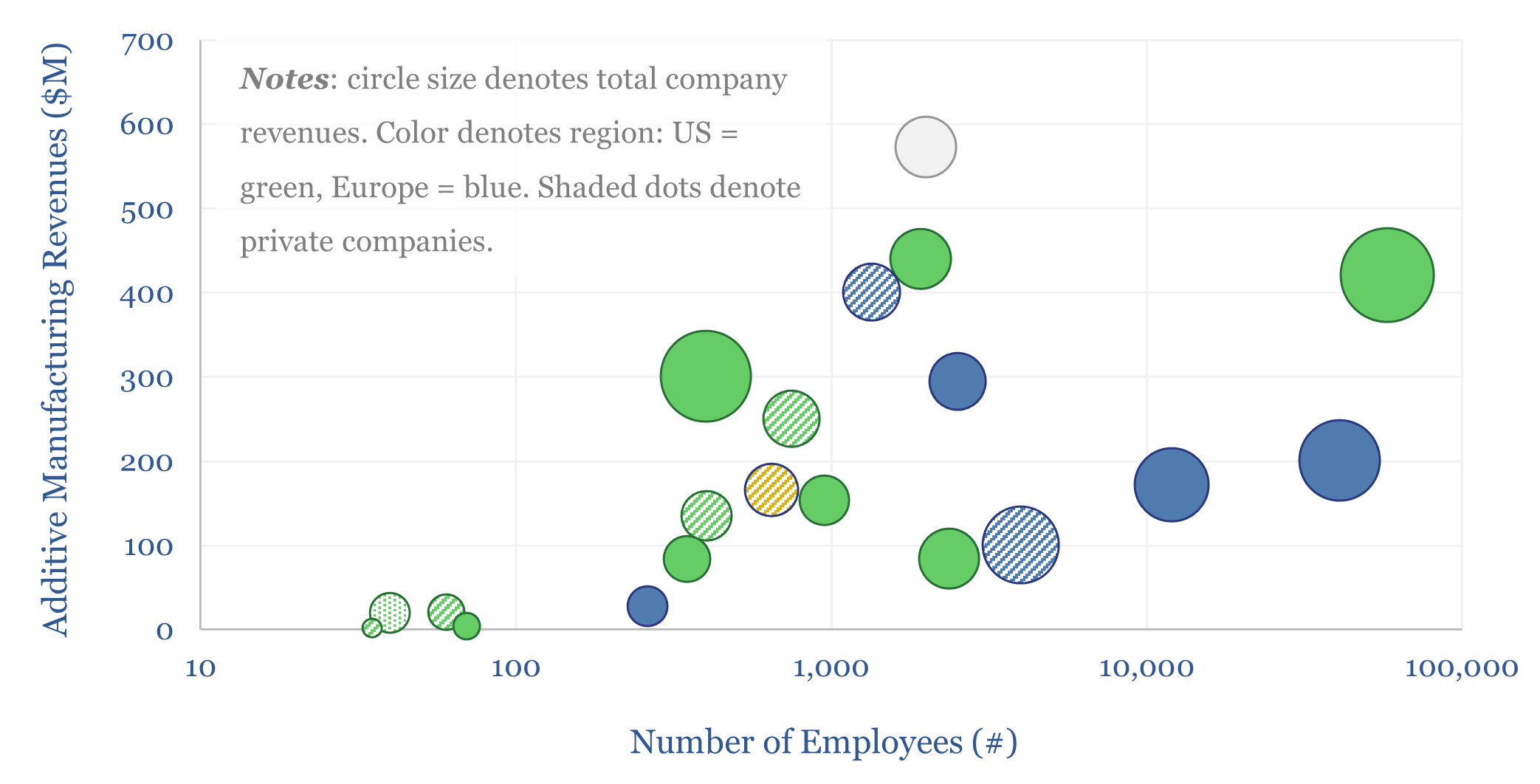

Can additive manufacturing overcome bottlenecks in gas turbine components, aerospace-related capital goods, and custom products that are unlocked by AI? This 16-page report re-evaluates the outlook for 3D printing, its economics, energy use, and company implications.

Read the Report?

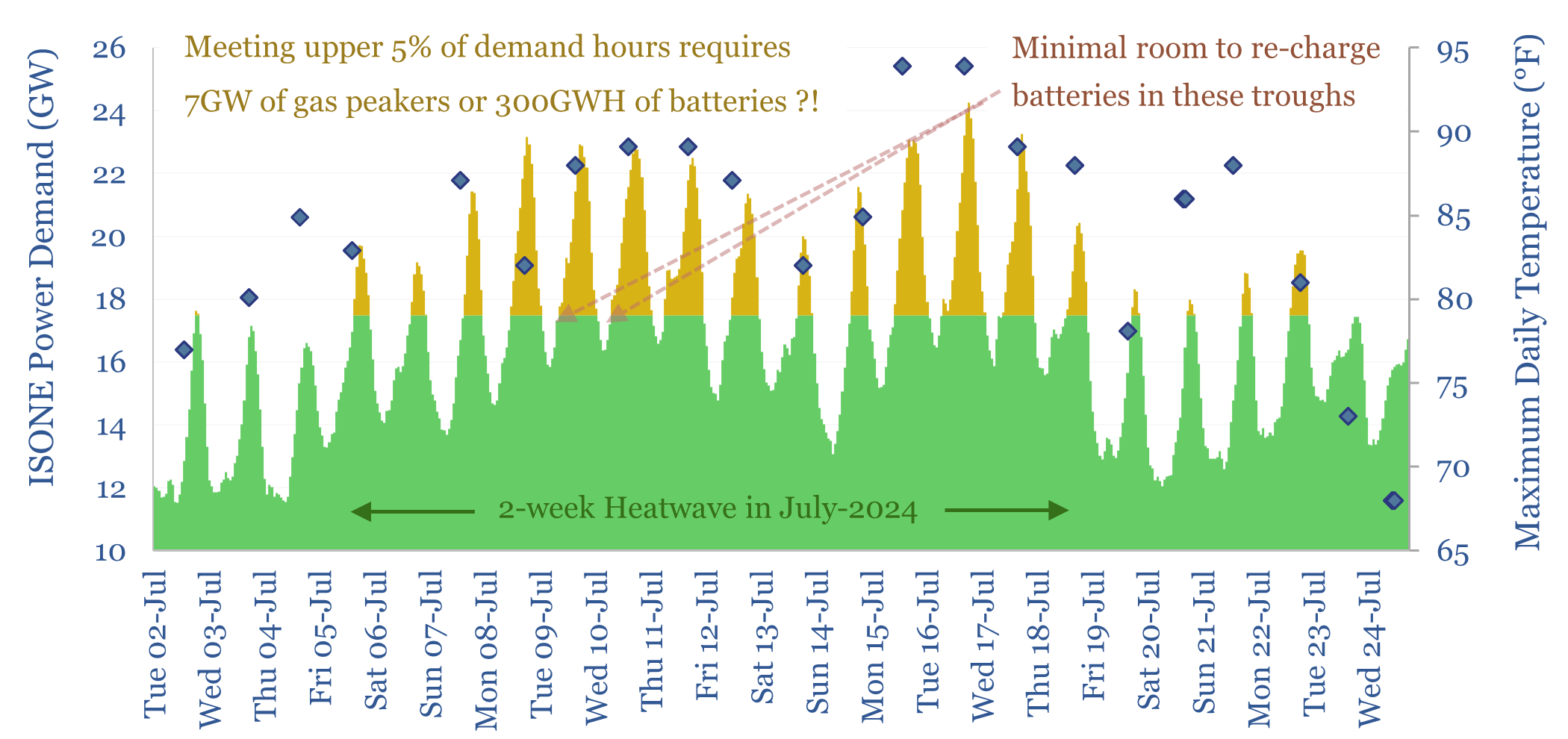

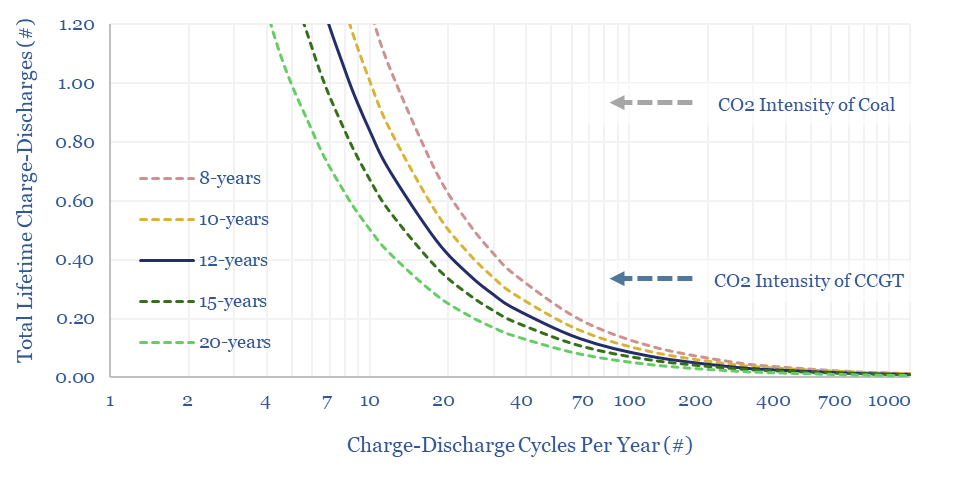

Peak loads in power grids are caused by heatwaves (in the US) and cold snaps (in Europe), which last 2-14 days. This 16-page report finds that very large batteries would be needed to ride through these episodes, costing 2-20x more than gas peakers. But the outlook differs interestingly between the US vs Europe.

Read the Report?

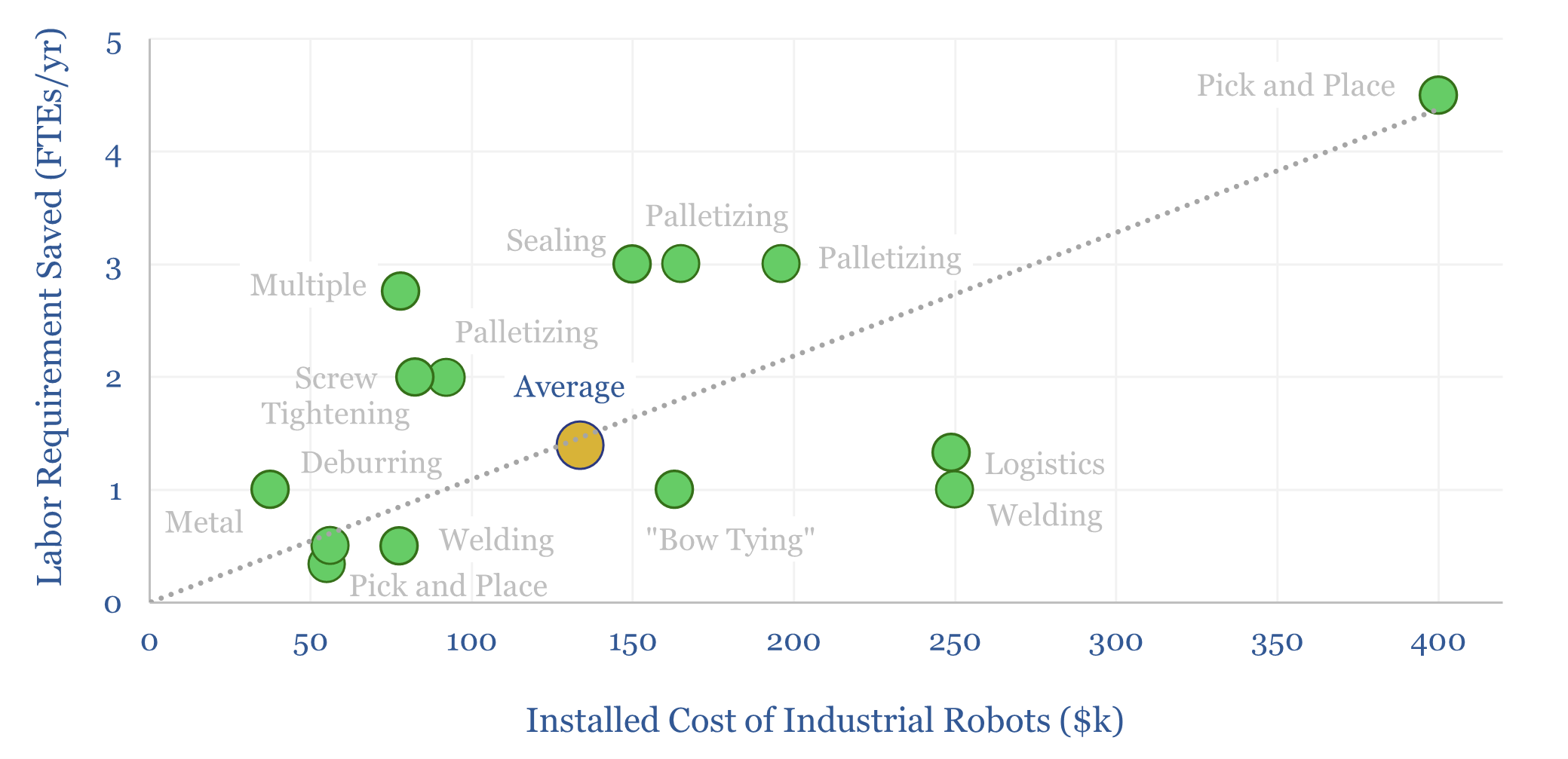

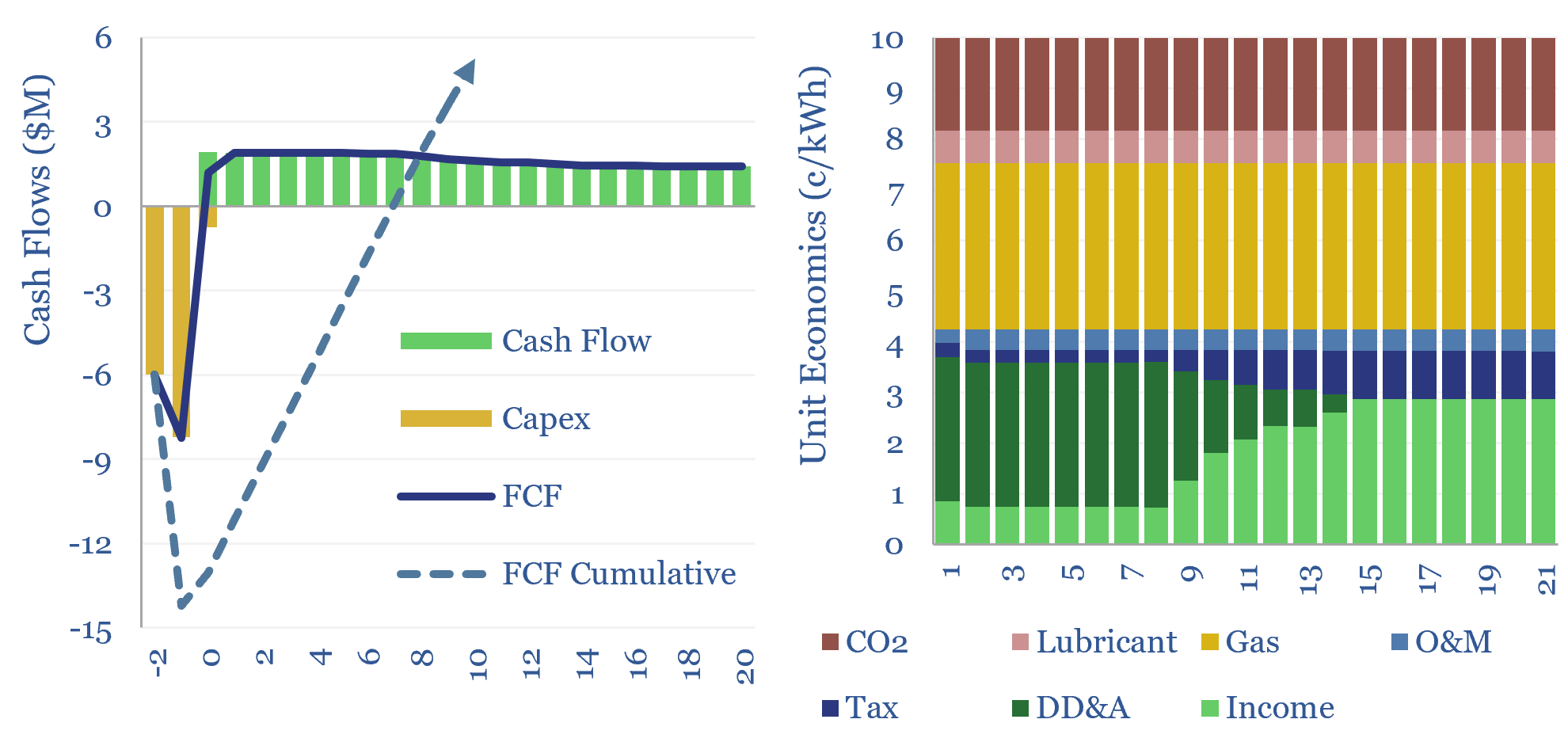

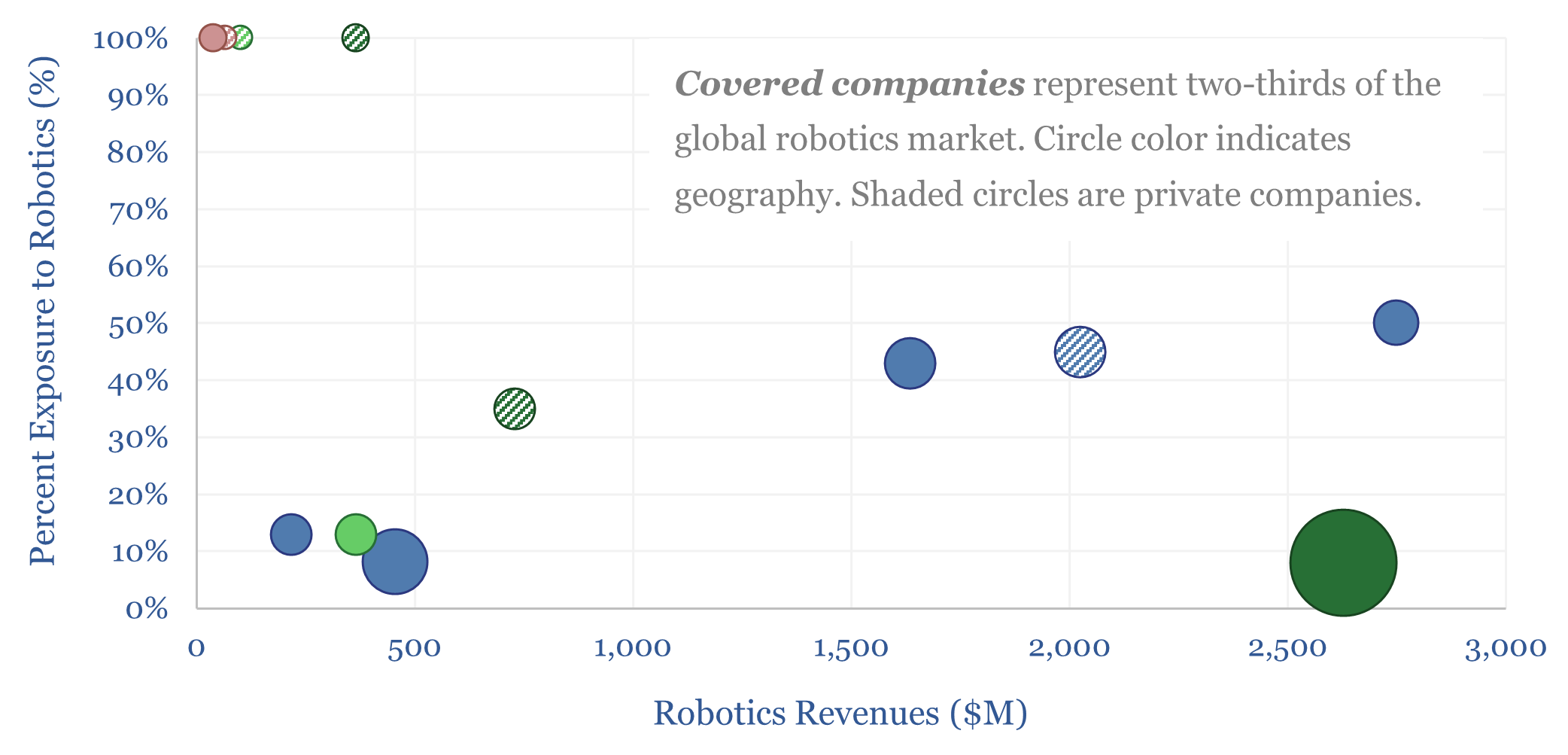

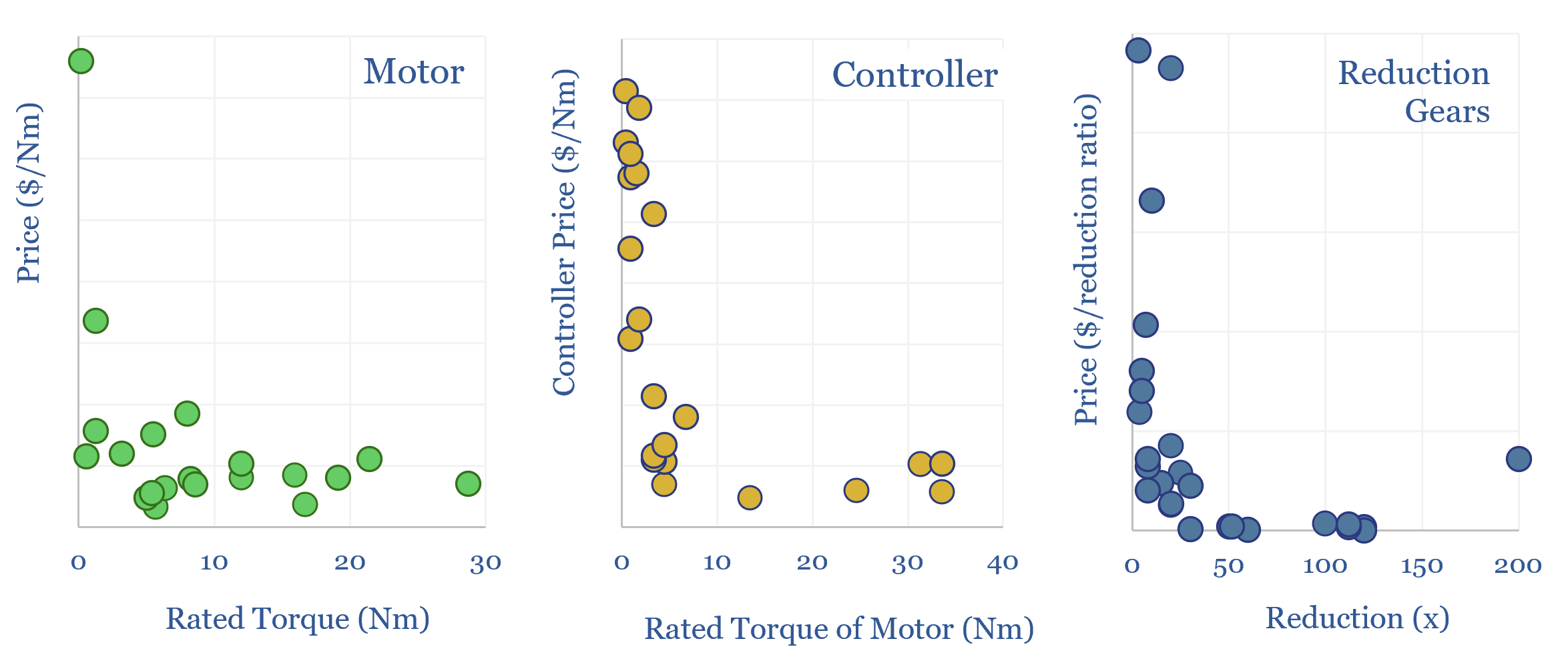

5 million industrial robots have now been deployed globally, in an $18bn pa market. But growth could inflect, with the rise of AI, and to solve labor bottlenecks, as strategic value chains are re-shored. Robotics effectively substitute labor inputs for electricity inputs. Hence today’s 18-page report compiles 25 case studies, explores the theme and who benefits?

Read the Report?

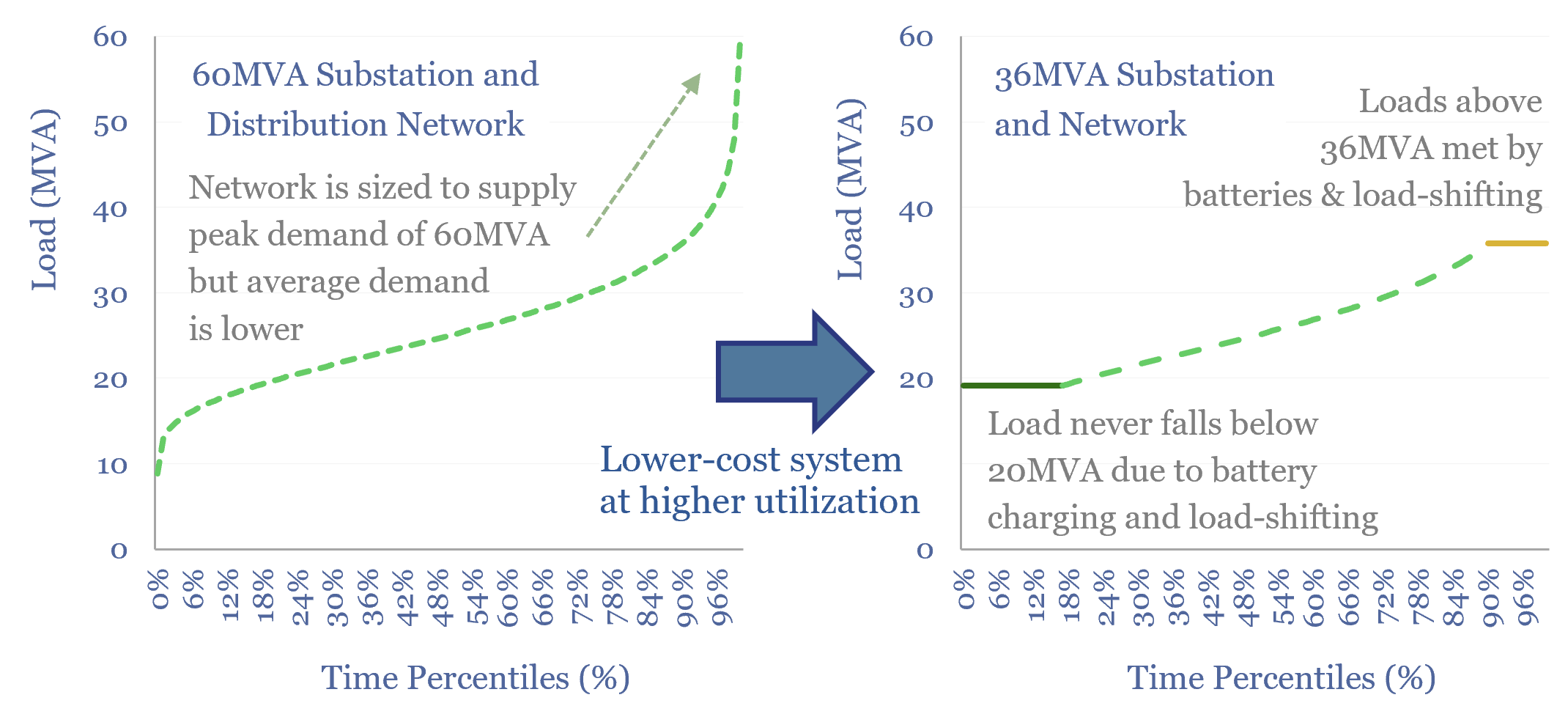

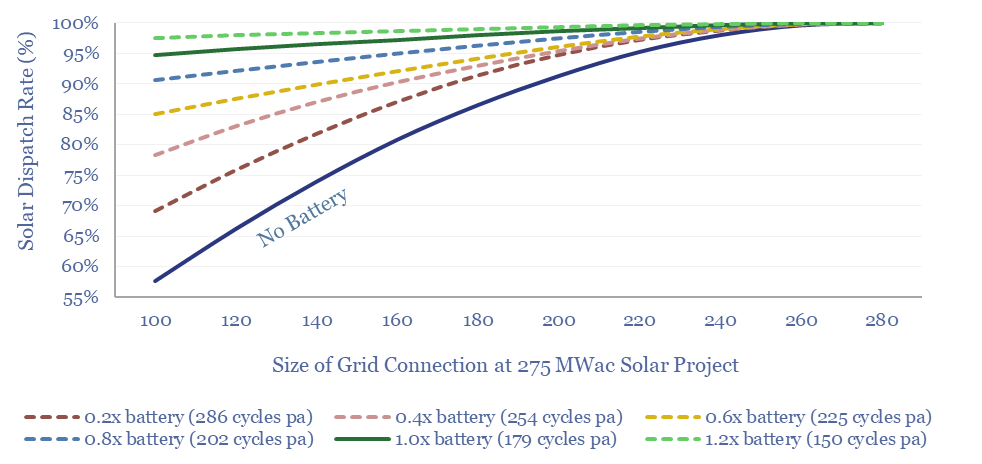

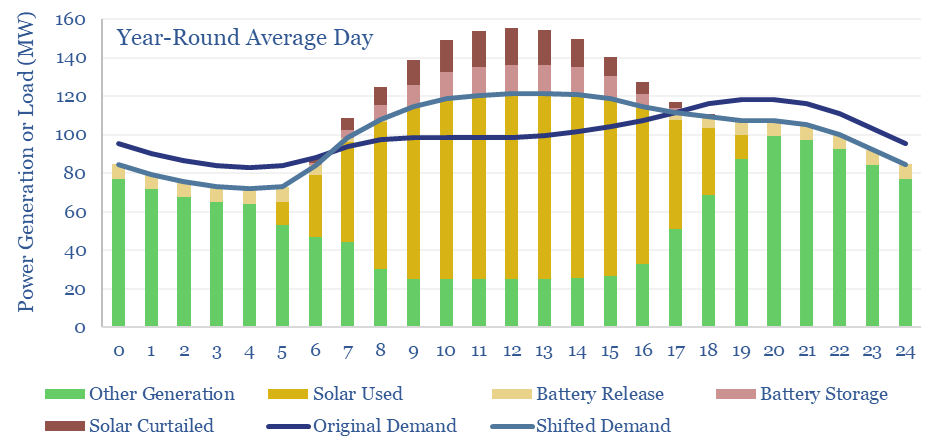

Will persistent grid bottlenecks de-rail electricity growth? This 18-page report explores using batteries and smart energy systems to reduce the need for new power lines. This option can be surprisingly economical, when back-tested on real-world load profiles. Hence we are upgrading our battery outlook.

Read the Report?

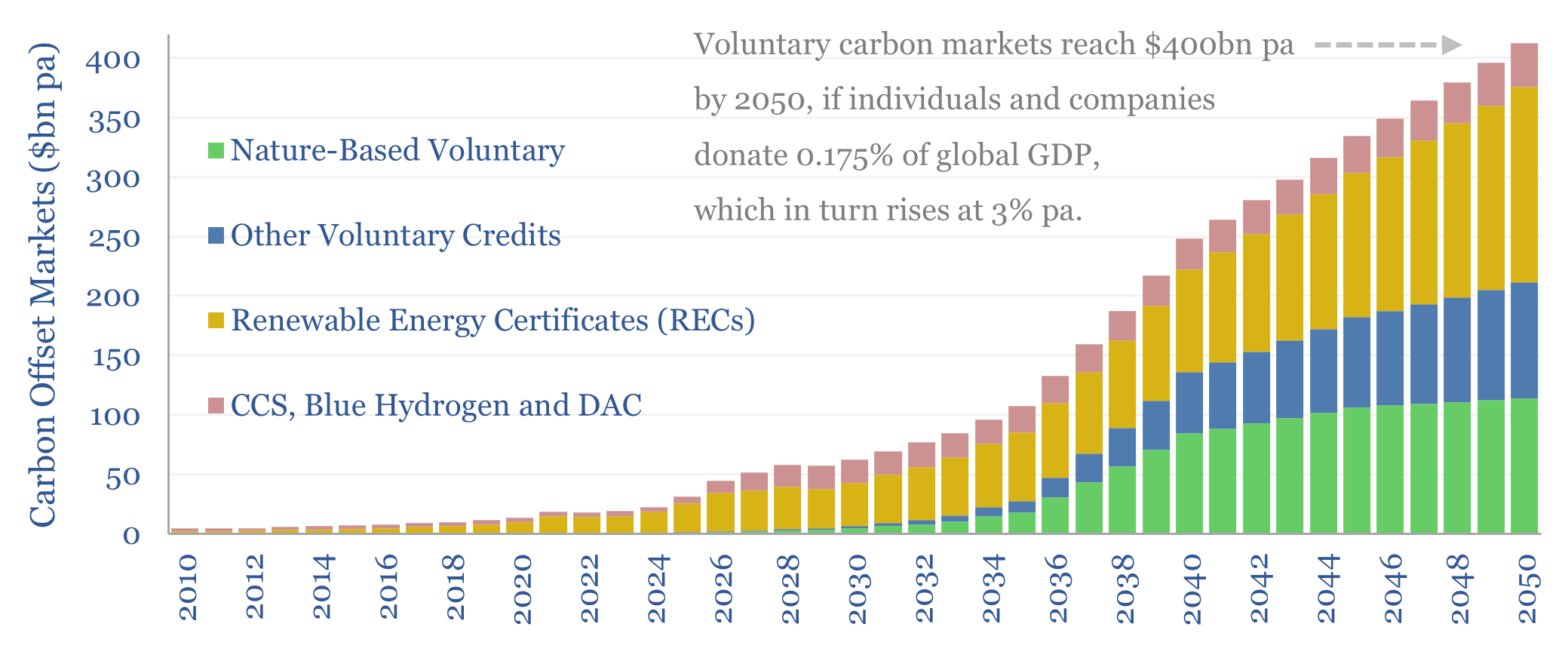

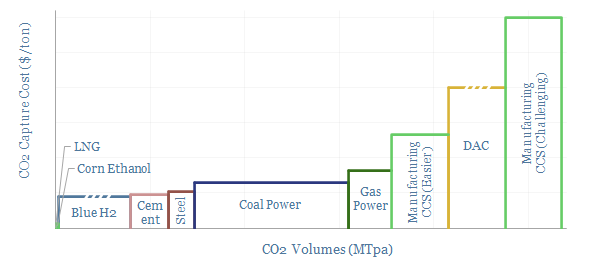

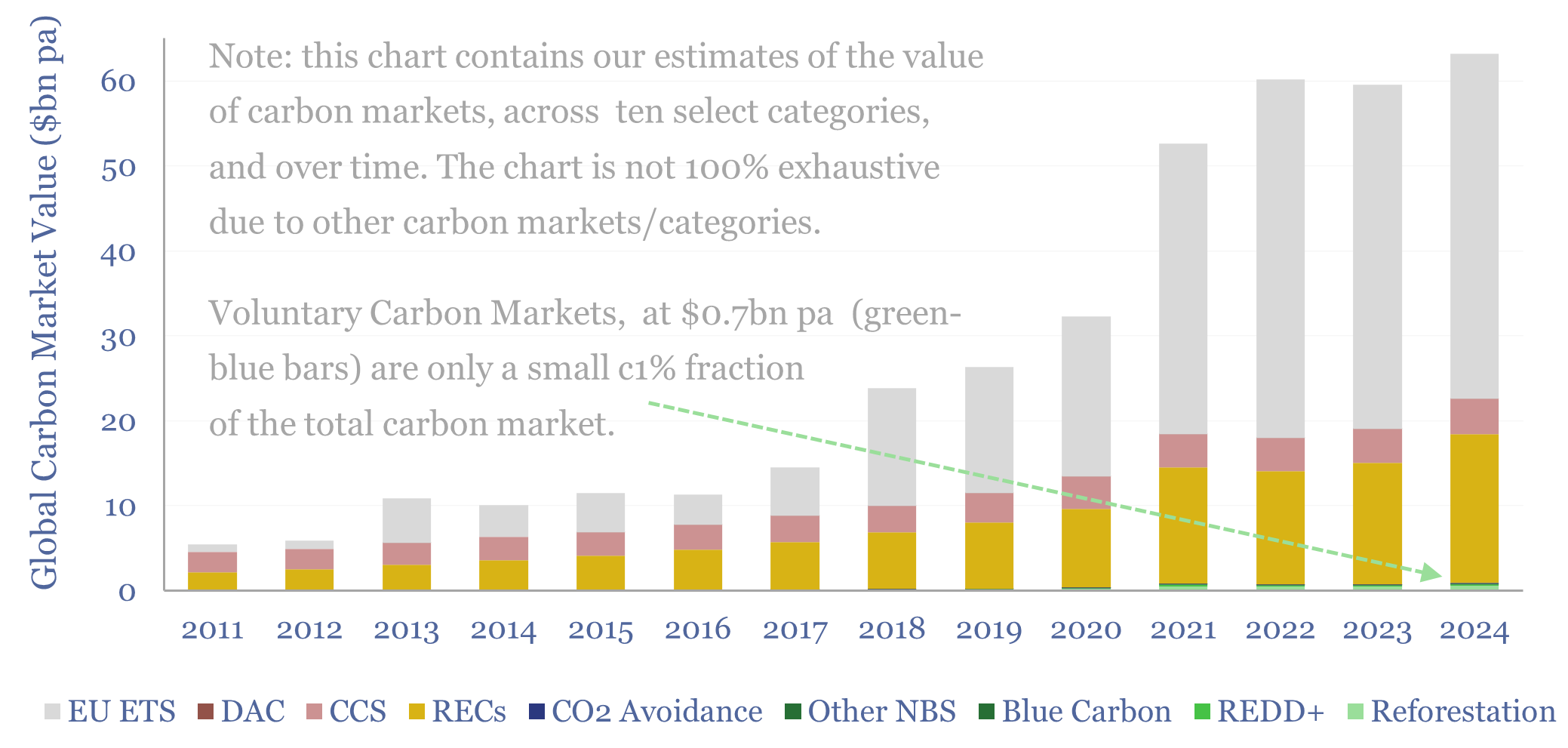

Carbon markets incentivize renewable energy, CCS, DAC, nature-based solutions and other CO2 offsets. In the past, we naïvely assumed these would grow as much as needed to reach Net Zero by 2050. This 14-page note revises our forecasts, by analogy to other forms of charitable giving. We see voluntary carbon markets reaching $400bn pa by 2050, while the EU ETS could be scaled back?

Read the Report?

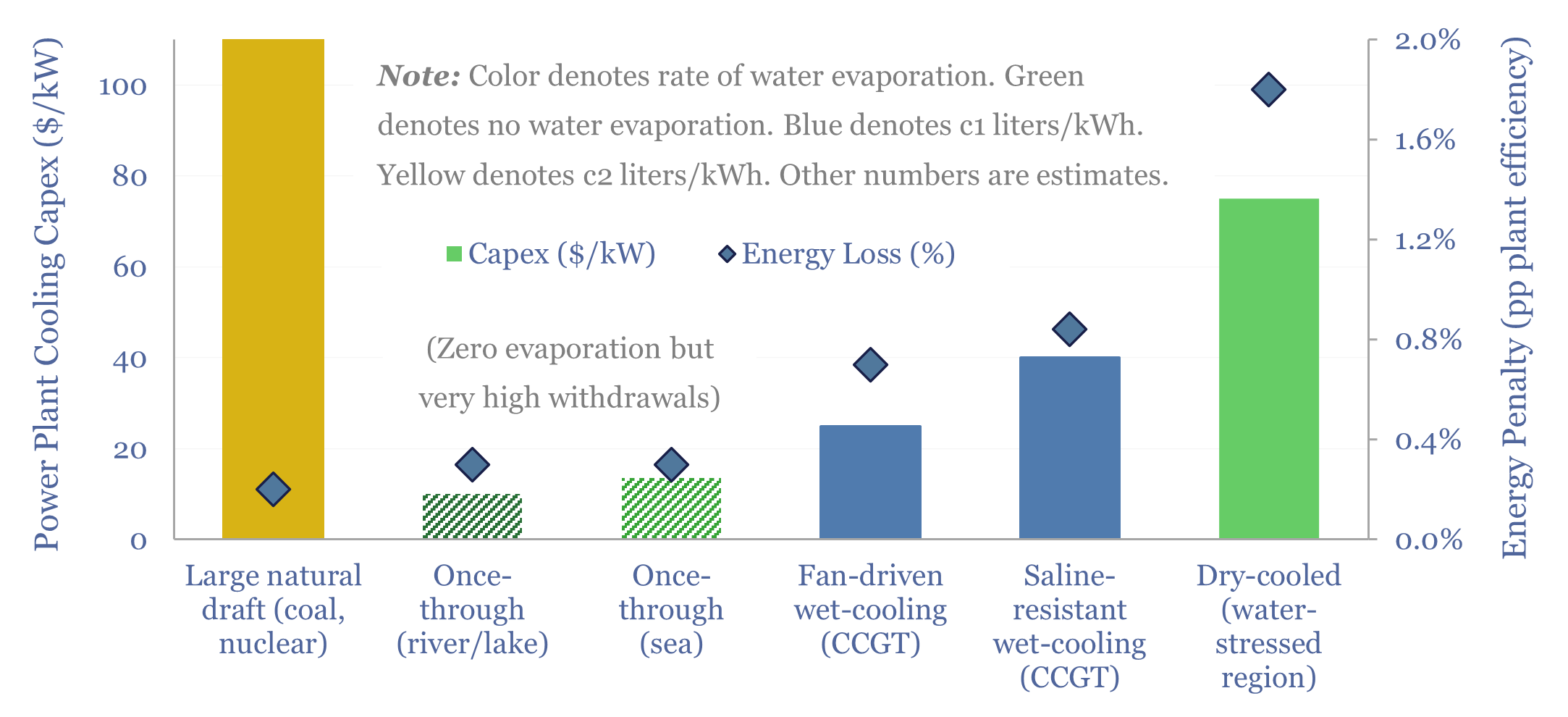

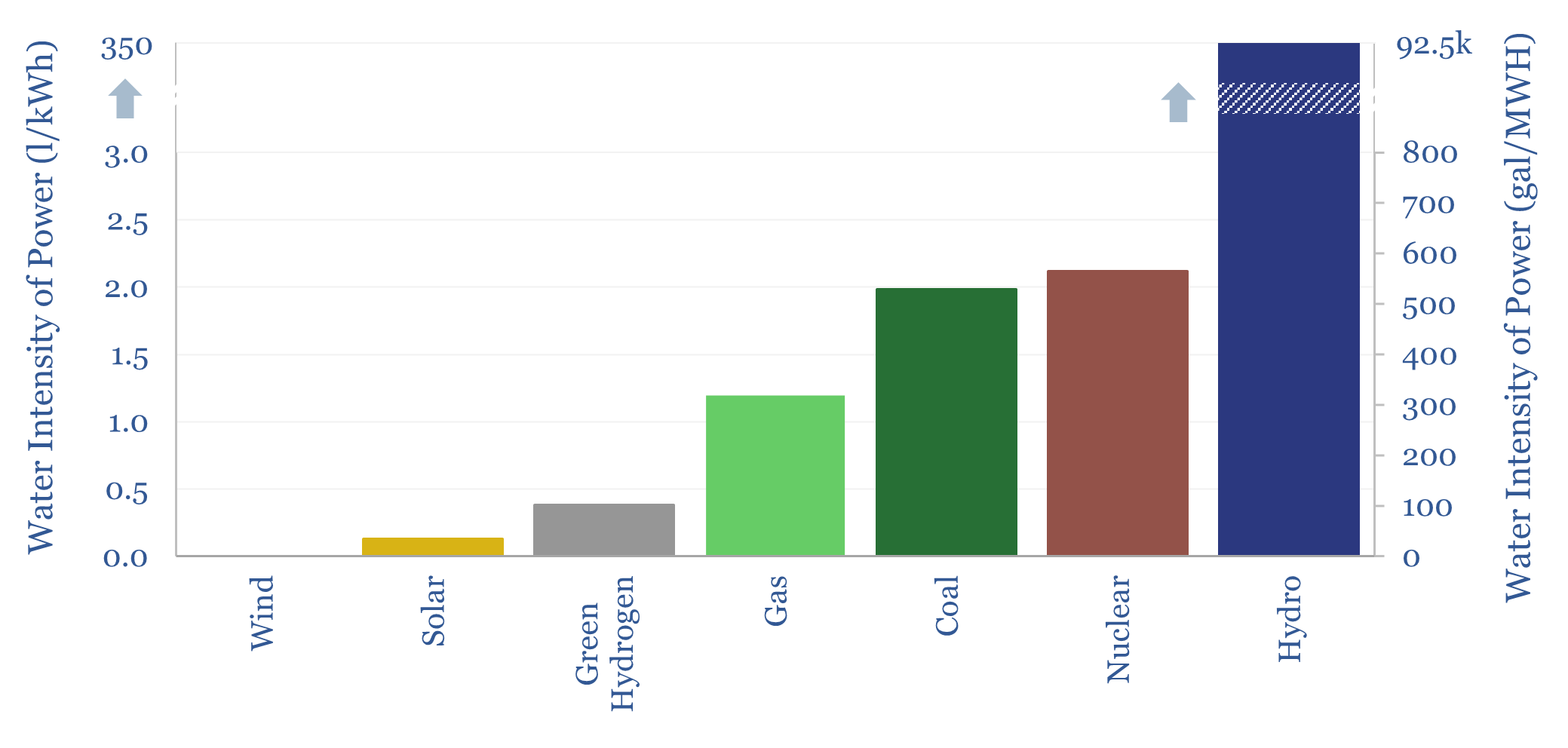

Water is needed to condense steam, downstream of the steam turbines, in nuclear, coal and CCGT power plants. But thermal power demands and fresh water scarcity are both structurally rising. Hence this 16-page report explores how the energy industry might adapt, trends in power plant cooling, and who benefits.

Read the Report?

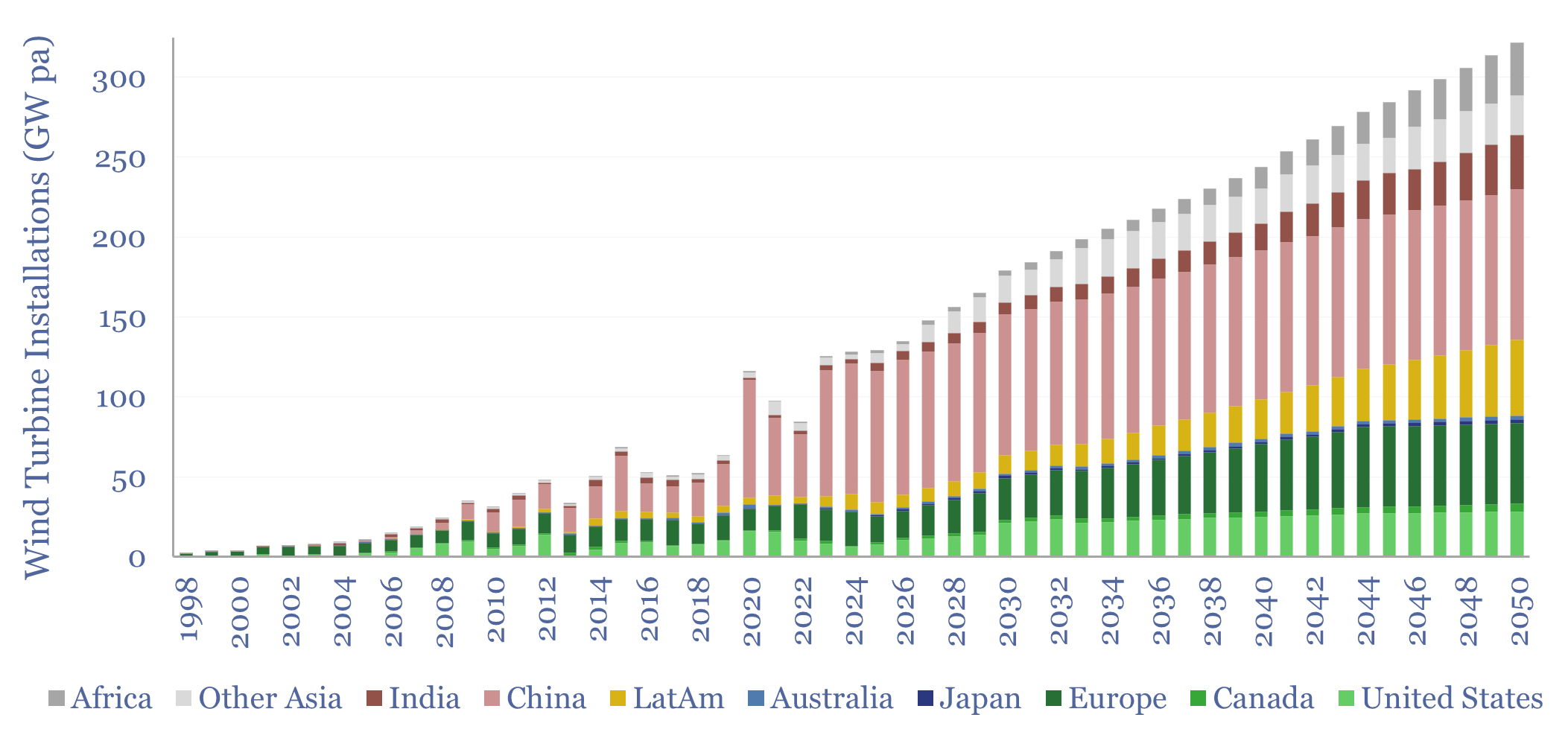

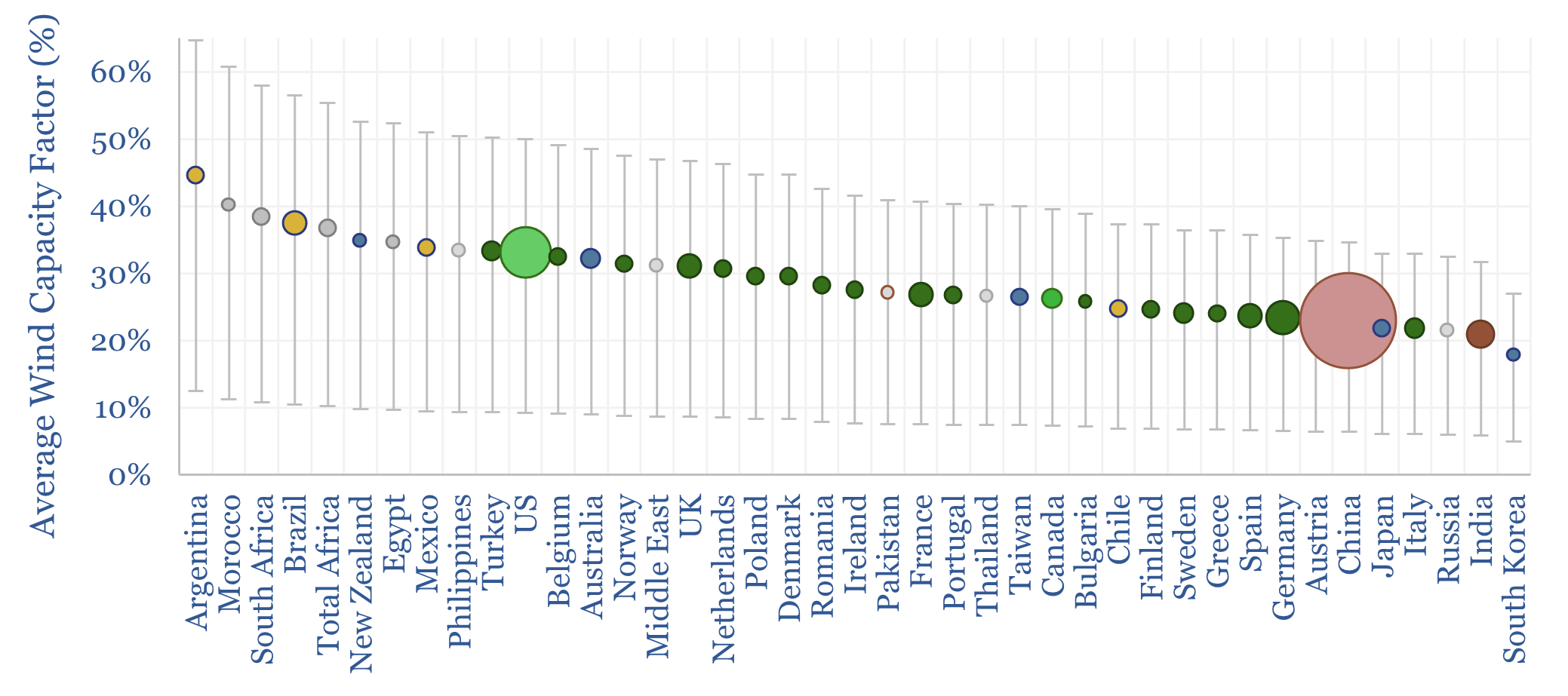

Wind economics are not good or bad in absolute terms. They depend on capacity factors, which average 26% globally, but can range from 10% to 60%. In the best locations, levelized costs are below 4c/kWh. Hence this 16-page note explores global wind capacity factors and updates our wind outlook by region throgh 2050.

Read the Report?

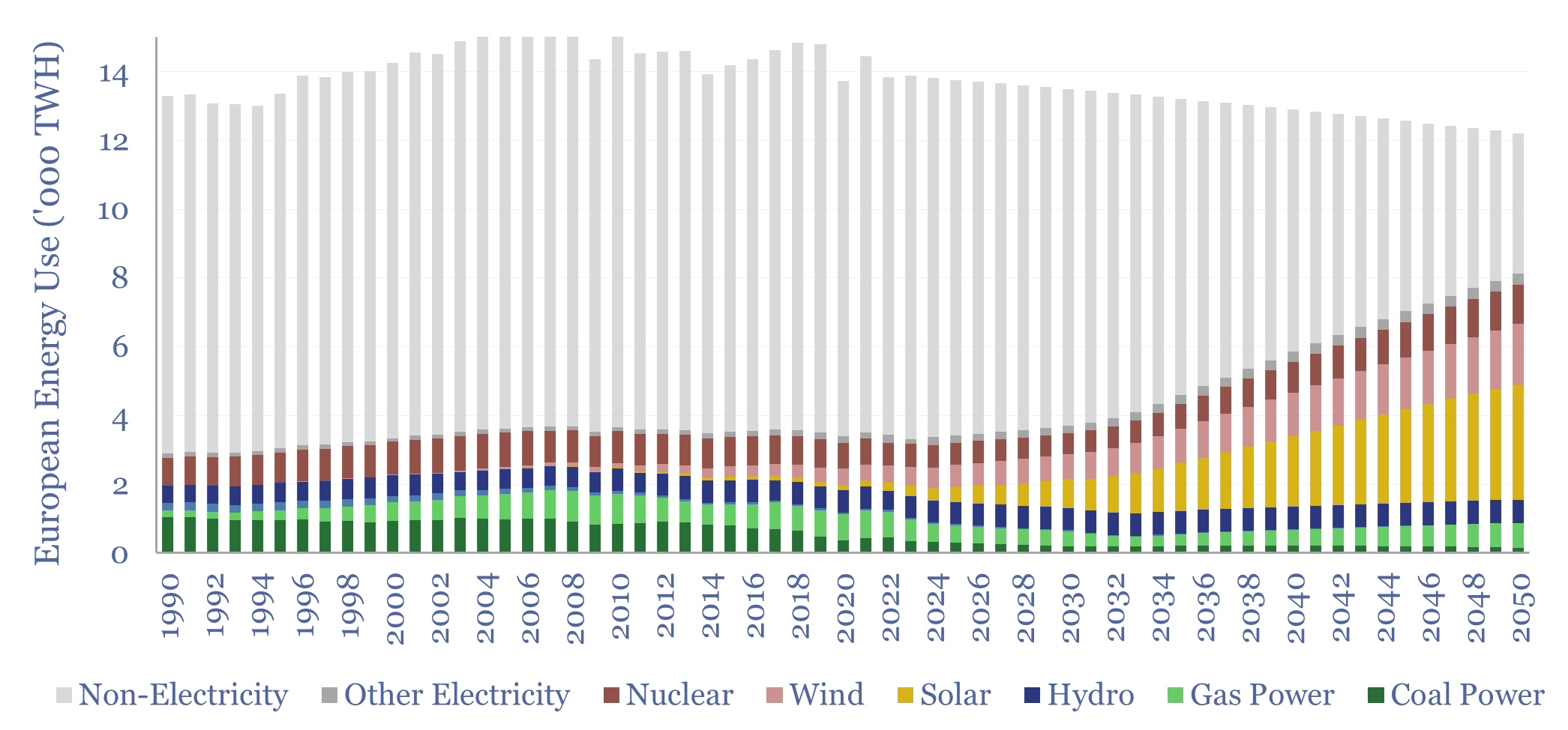

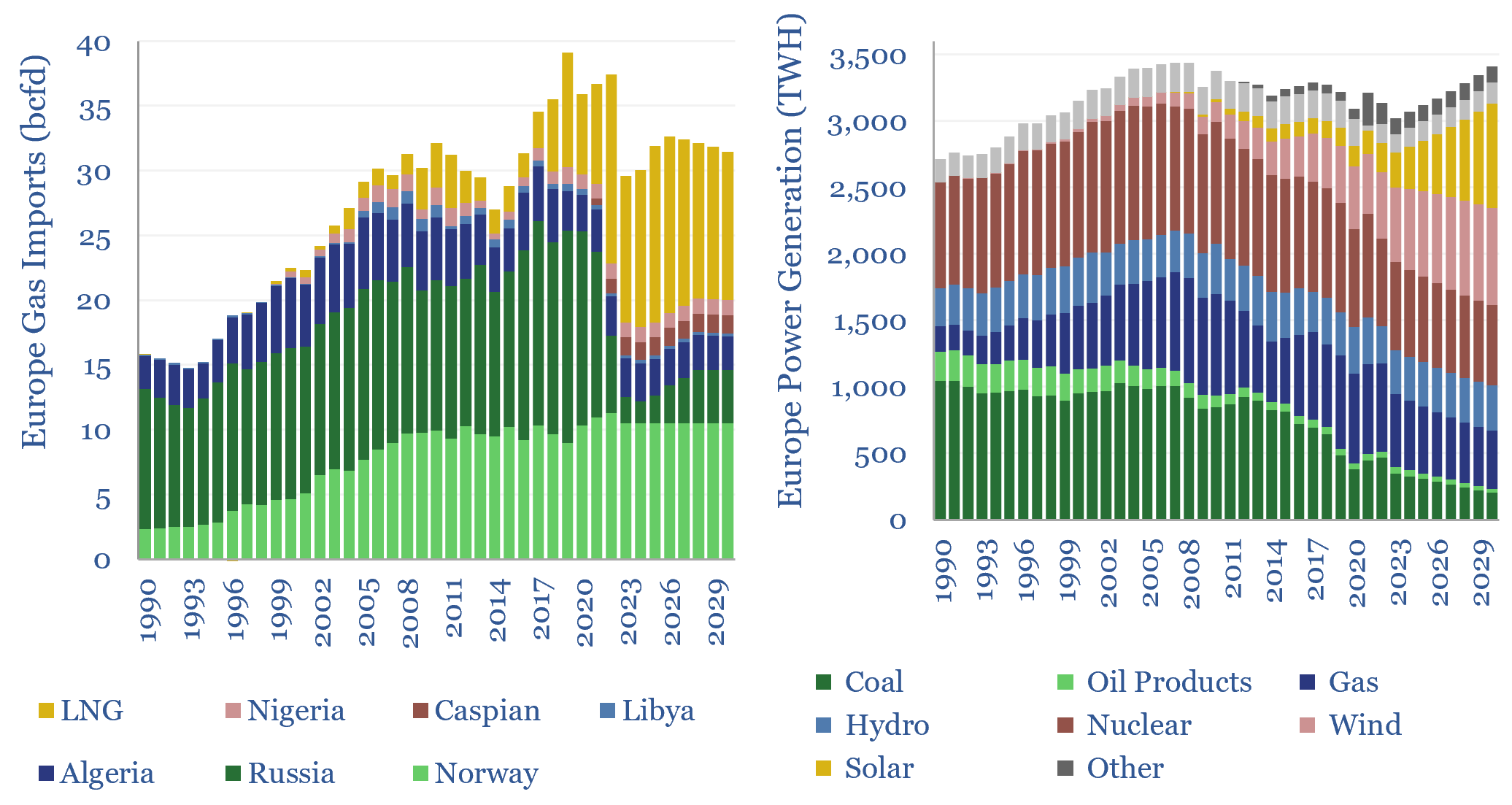

Europe’s energy ambitions are now intractable: It is just not feasible to satisfy former climate goals, new geopolitical realities, and also power future AI data centers. Hence this 18-page report evaluates Europe’s energy options; predicts how policies are going to change; and re-forecasts Europe’s gas and power balances, both to 2030 and to 2050.

Read the Report?

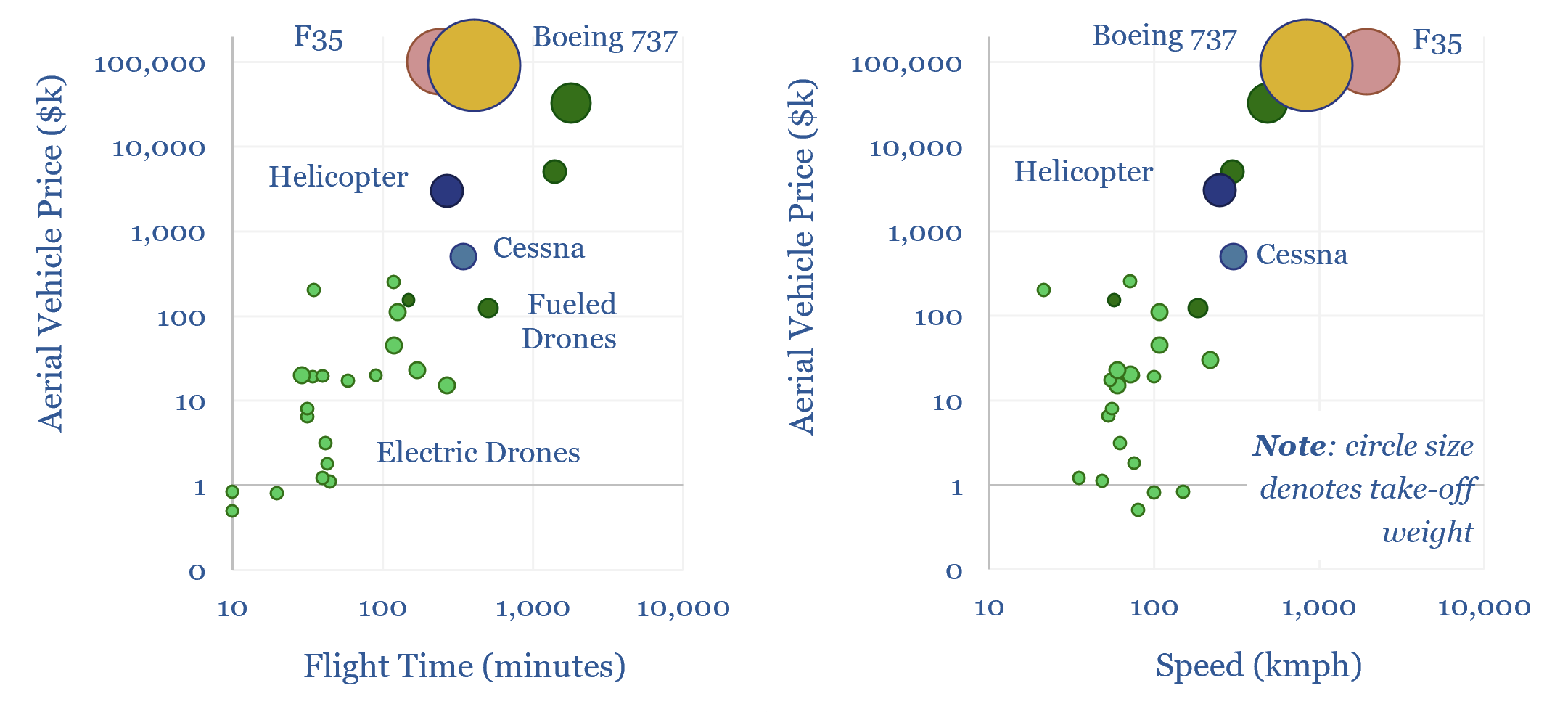

Drones cost just $1k-100k each. They may use 95-99% less energy than traditional vehicles. Their ascent is being helped by battery technology and AI. Hence this 14-page report reviews recent progress from 40 leading drone companies. What stood out most was a re-shaping of the defense industry, plus helpful deflation across power grids, renewables, agriculture, mining and last-mile delivery.

Read the Report?

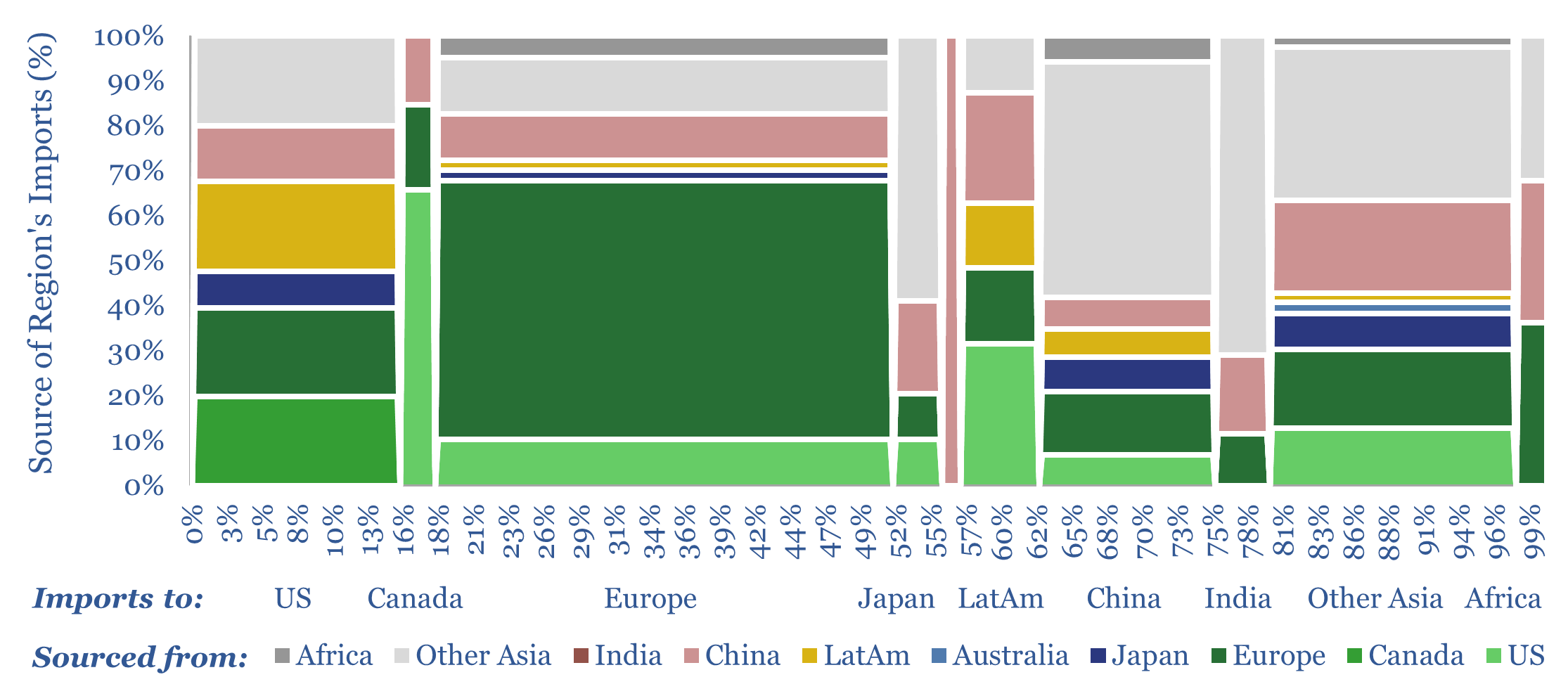

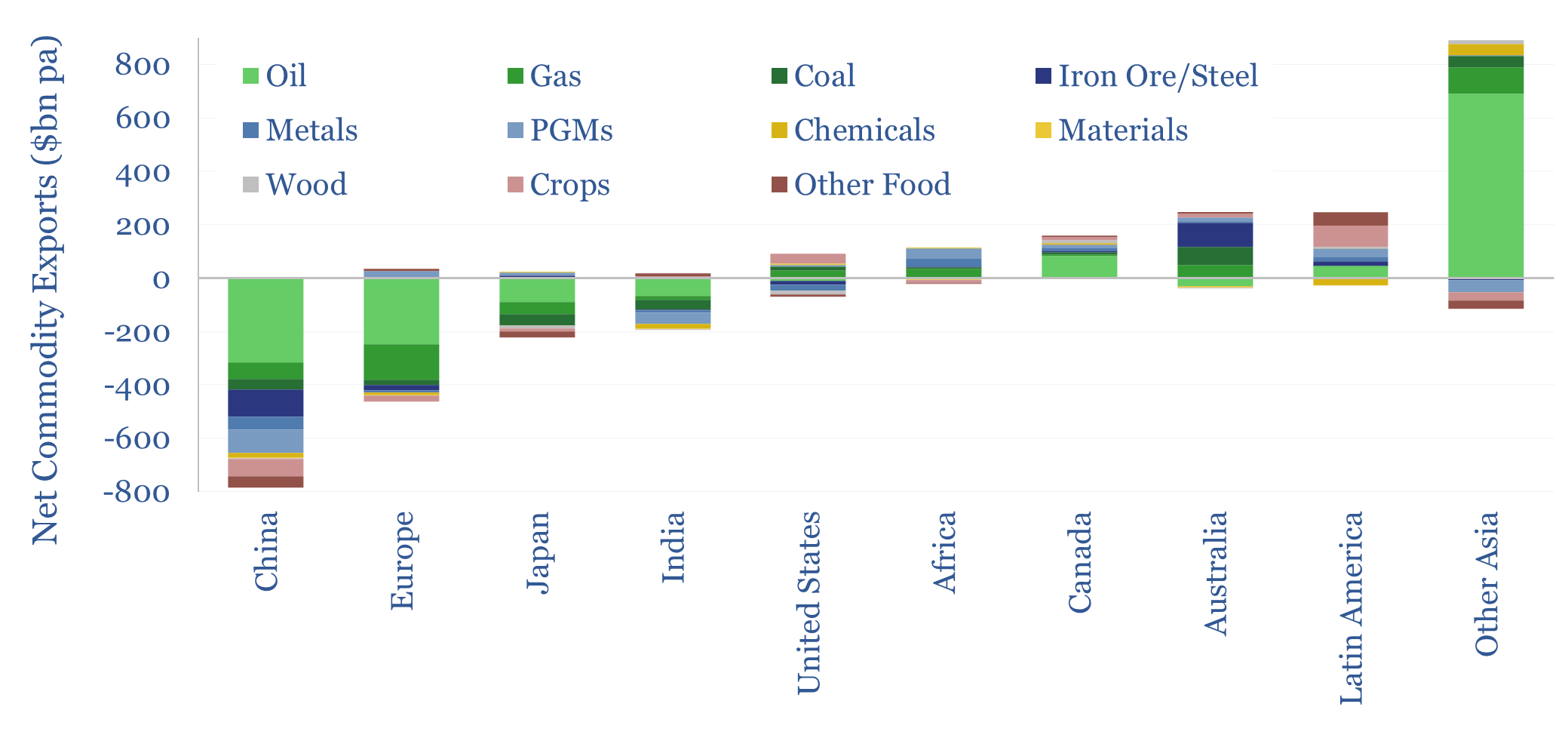

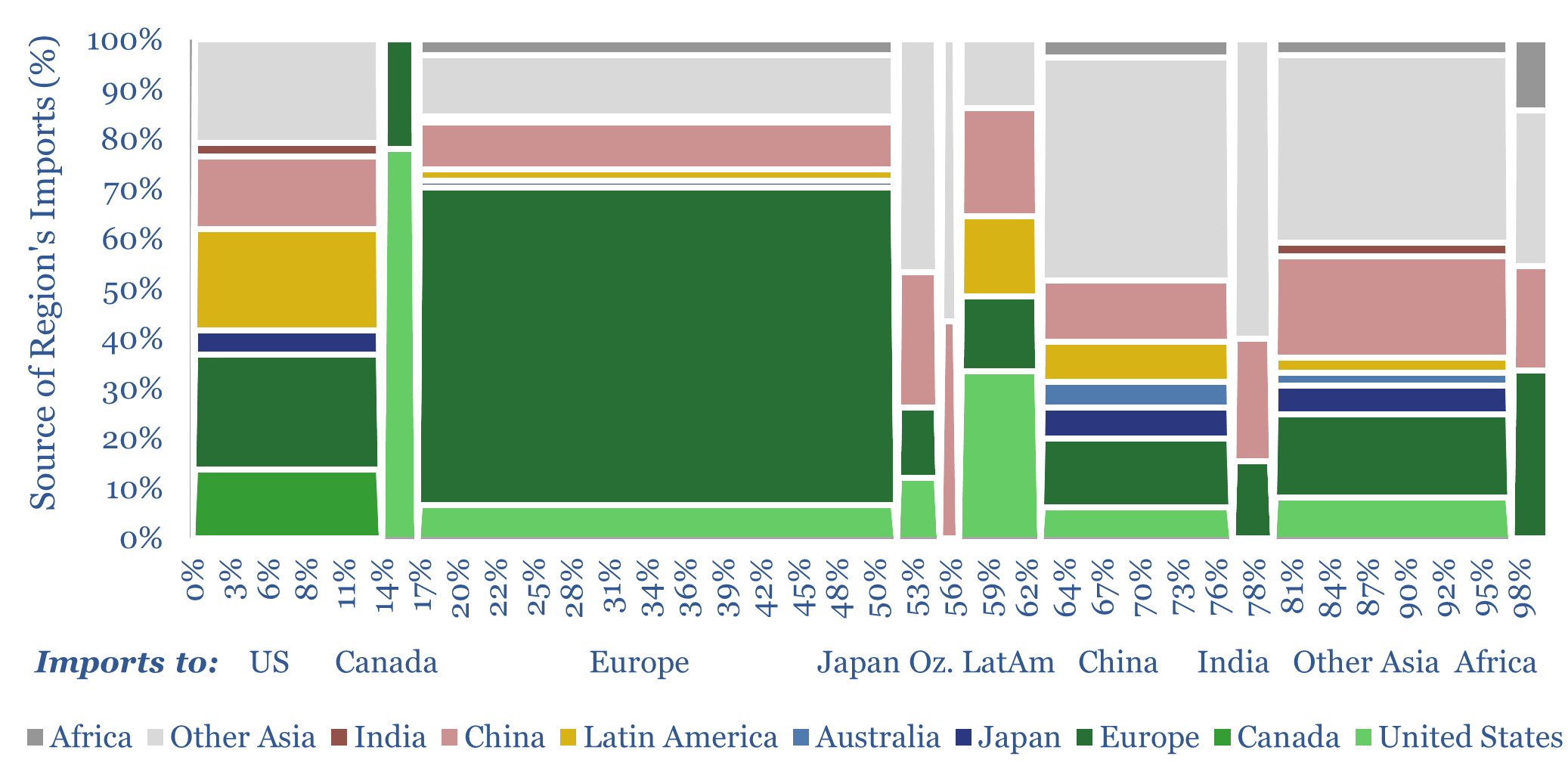

Global trade has been growing more adversarial. US foreign relations are also shifting. Hence this 16-page note maps 20 trade categories, across energy, materials and capital goods; in each case, breaking down global imports by source, and global exports by destination. Our top ten conclusions follow.

Read the Report?

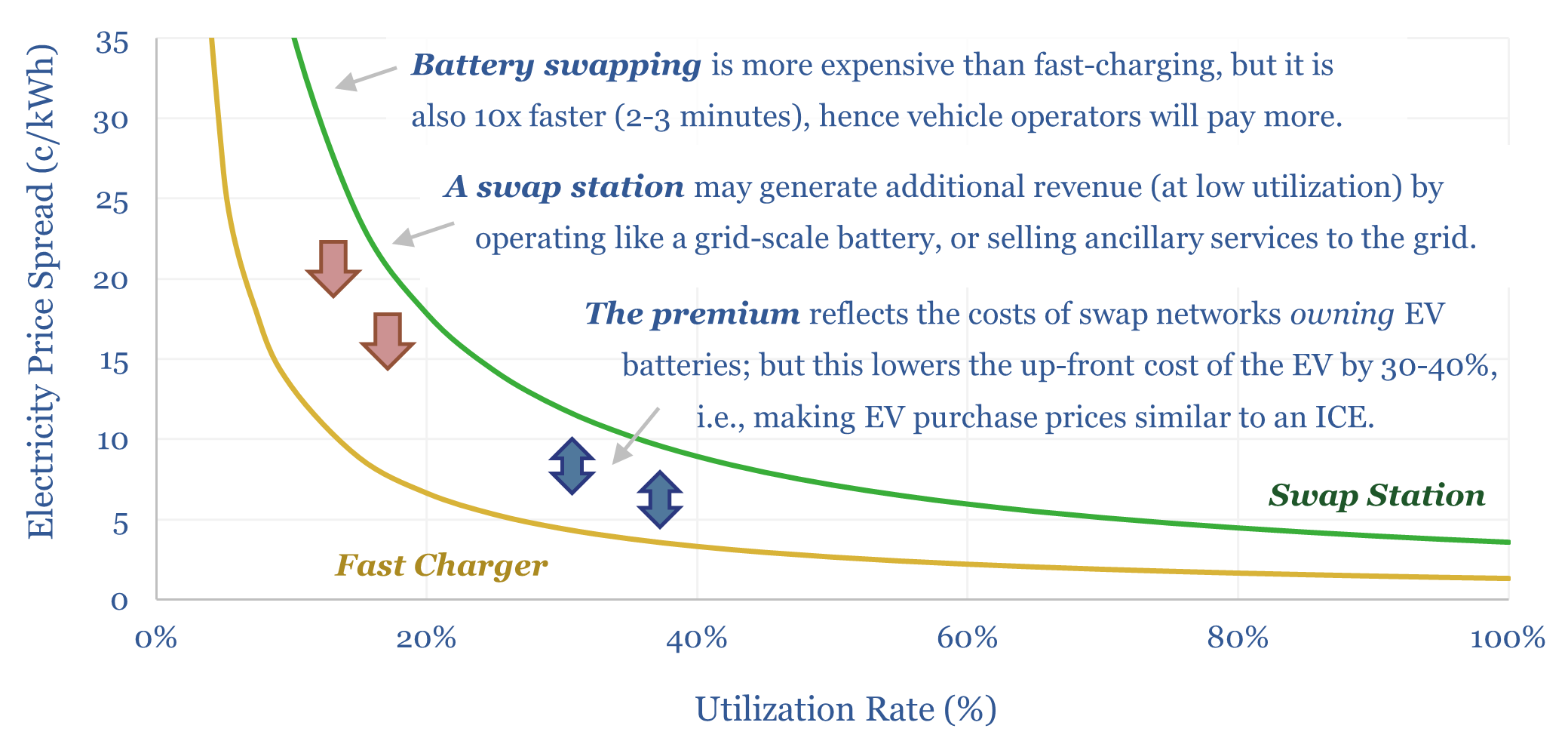

Battery swapping has seen a sudden surge of interest, especially for cars in China, some heavy vehicles, and two-wheelers throughout emerging markets. Can the theme re-accelerate EVs? This 19-page report finds many advantages, controversies over costs, and profiles leading companies.

Read the Report?

National security risks are rising in developed world energy systems, as geopolitics grow more adversarial, and cyber-attacks are at new highs. This 16-page report finds that electrification is on balance making energy systems more vulnerable, then outlines mitigation measures, and opportunities?

Read the Report?

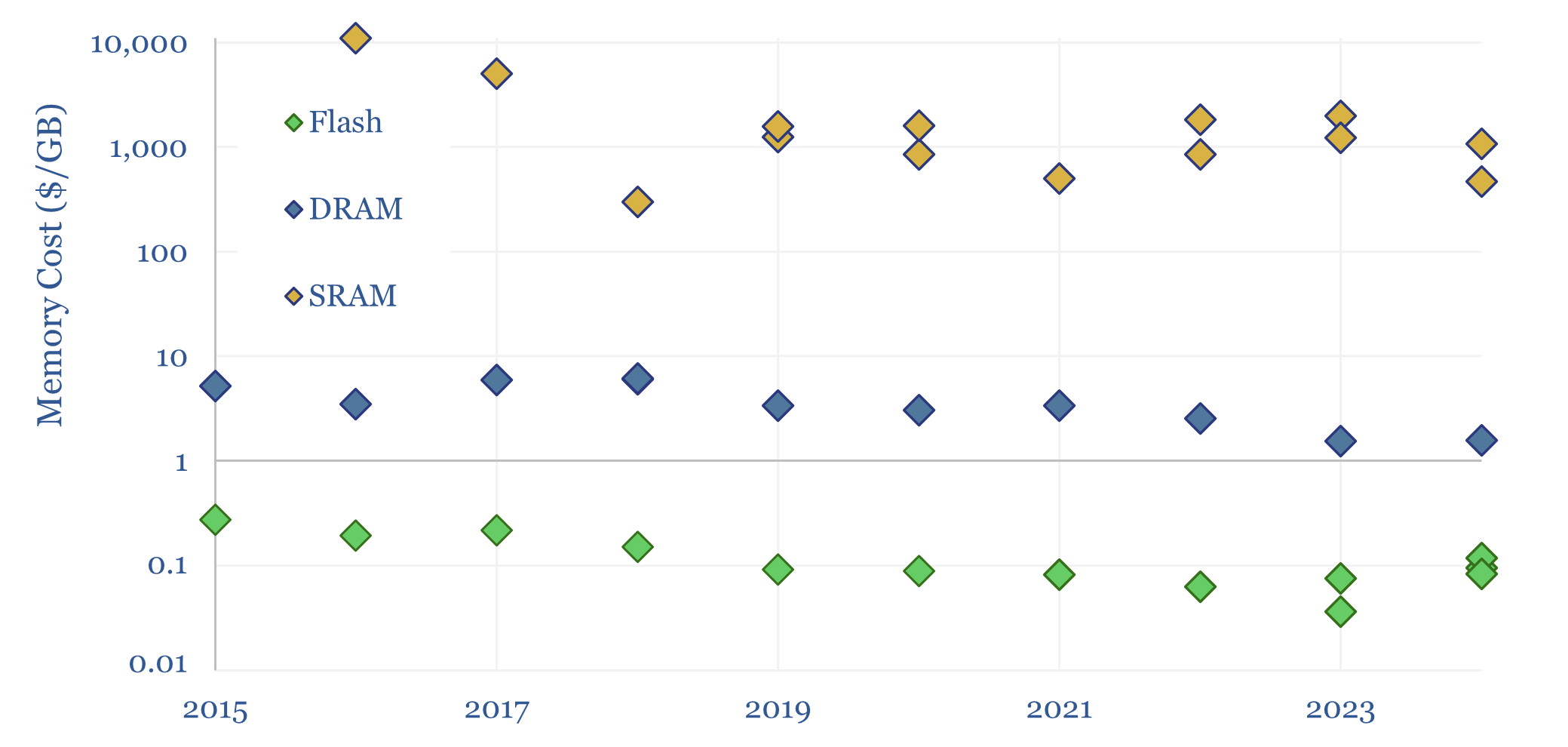

Three types of computer memory dominate modern information processing: Flash, DRAM and SRAM. This 5-page note simply covers each one, how it works, what it costs, advantages, disadvantages, market sizes and leading companies. AI likely boosts all three, but can more SRAM unlock big efficiency gains?

Read the Report?

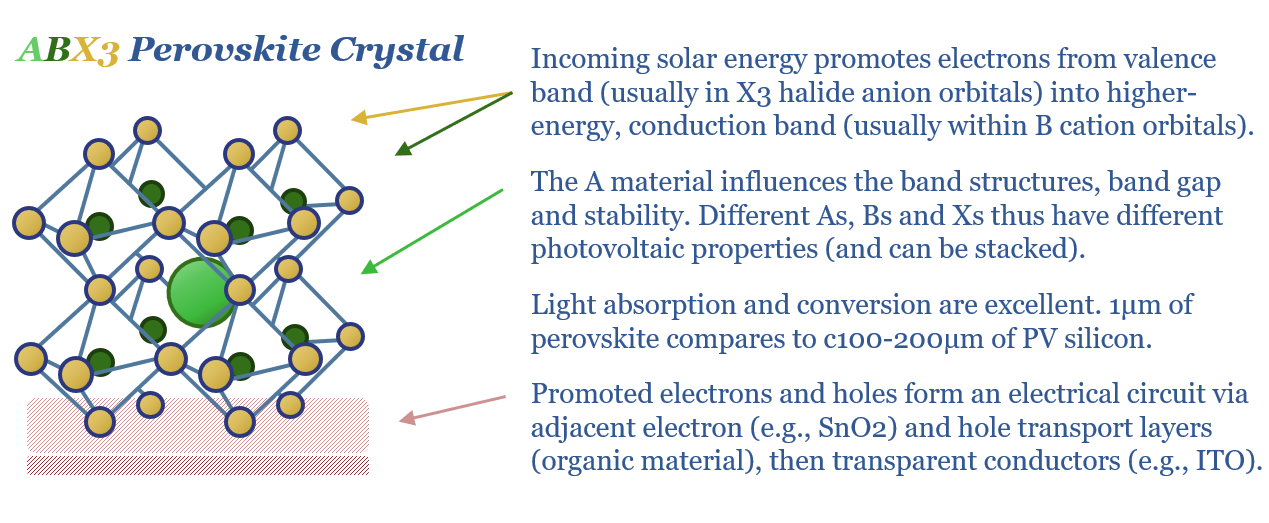

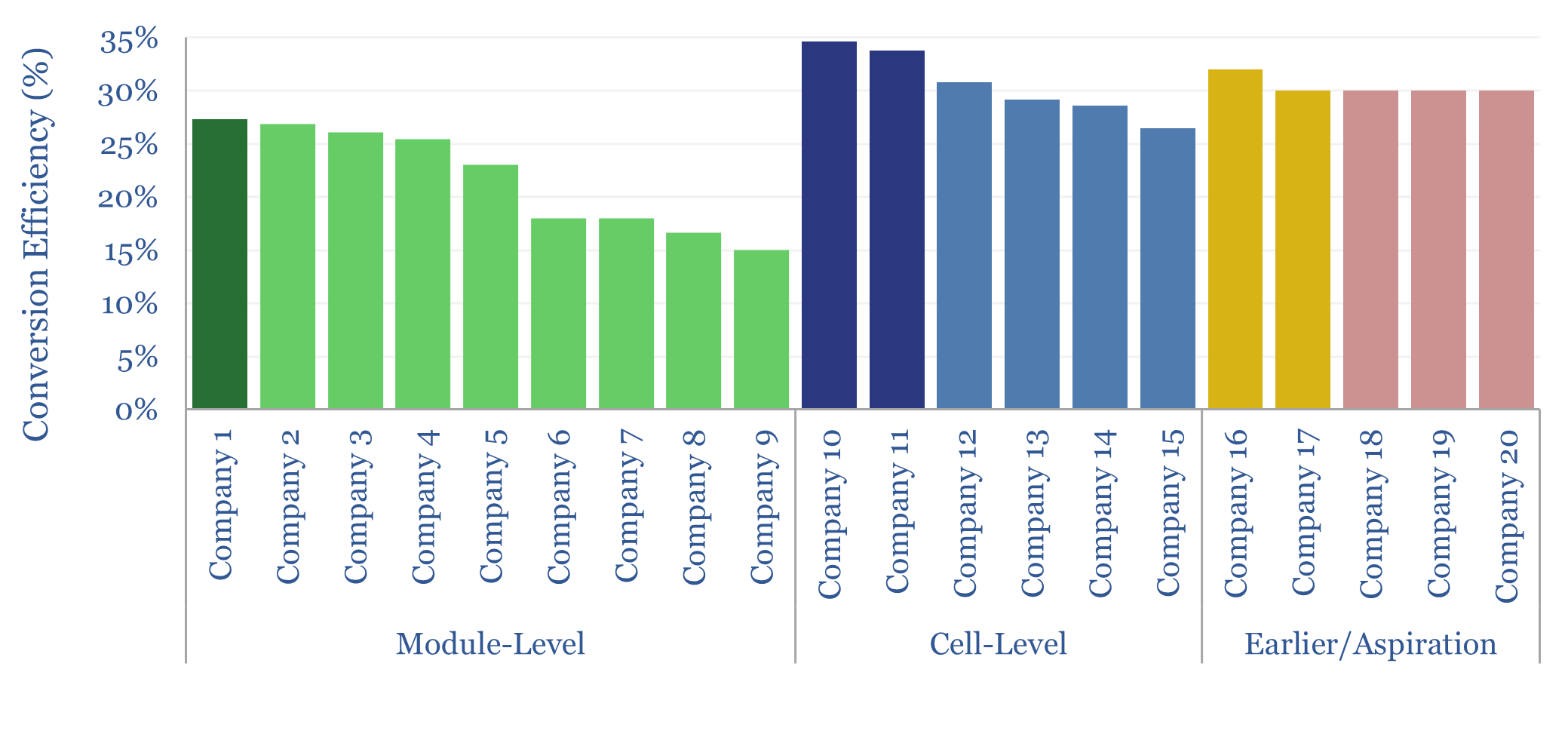

Will the next chapter of solar’s ascent come from perovskite-tandem cells, followed by perovskite-on-perovskites? This 18-page report finds more momentum than we expected. There is potential for 30% cost deflation, new solar applications (in buildings/vehicles), and a disruption of PV silicon?

Read the Report?

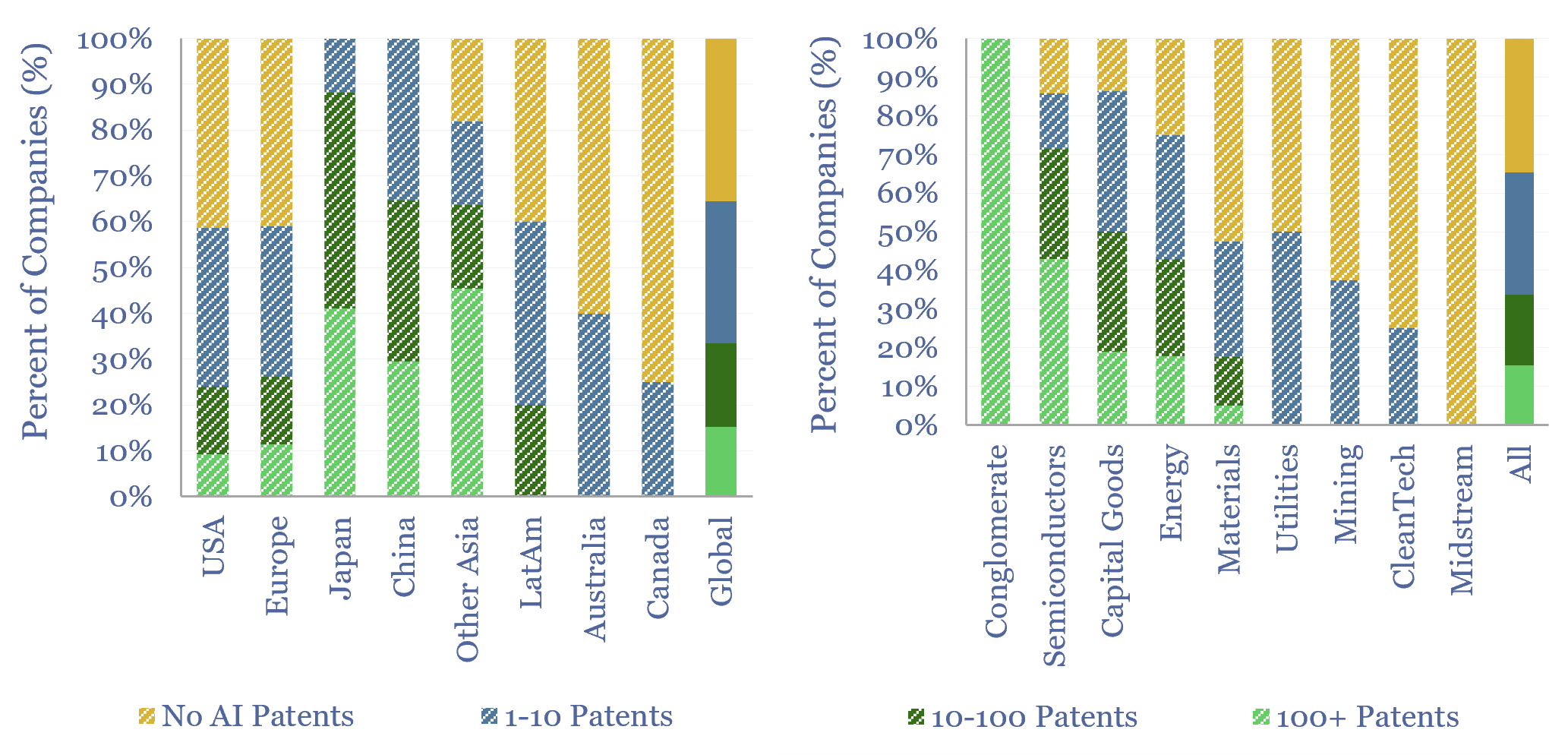

Increasingly efficient AI should unlock ever more widespread and more sophisticated uses of AI. This is shown by reviewing 40,000 patents from 200 industrial companies. This 15-page report summarizes notable companies, patent filings, and updates our 2030 forecasts for AI energy.

Read the Report?

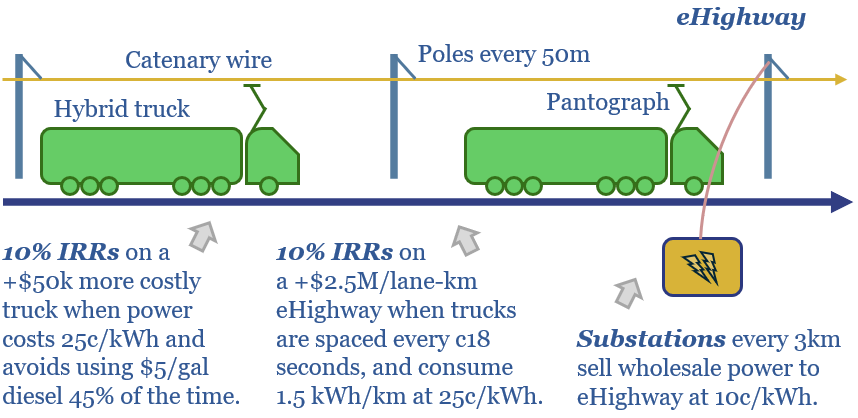

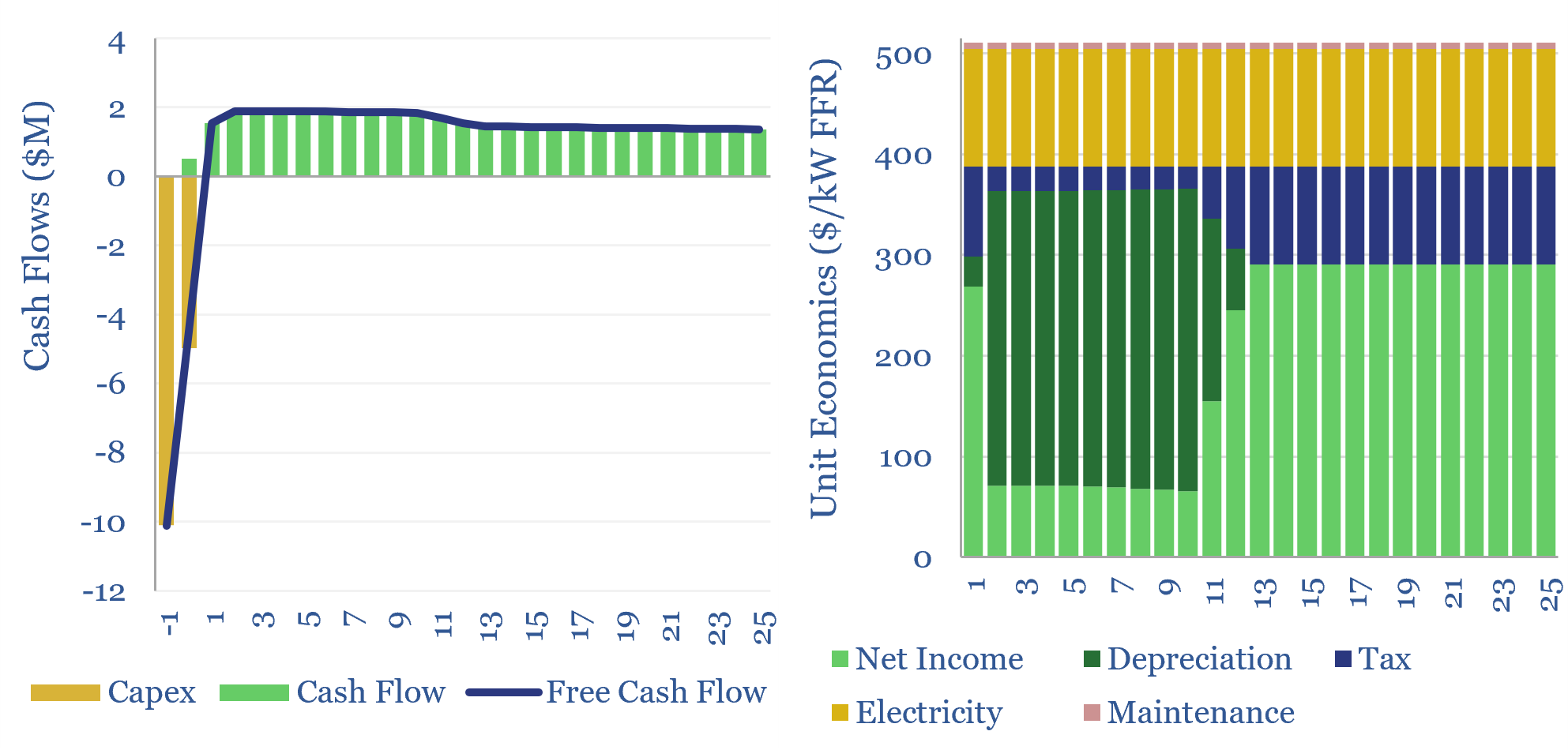

eHighways electrify heavy trucks via overhead catenary wires. They have been de-risked by half-a-dozen real-world pilots. High-utilization routes can support 10% IRRs on both road infrastructure and hybrid trucks. This 15-page report finds benefits in logistics networks and for integrating renewables?

Read the Report?

Some commentators say the 21st century will be the ‘age of the electron’. But in computing/communications, the photon has long been displacing the electron. This 17-page note gives an overview. It matters as moving data is 50-90% of data center energy use. We contrast fiber vs copper; and explore AI power, optical computing, and a boom for laser photonics?!

Read the Report?

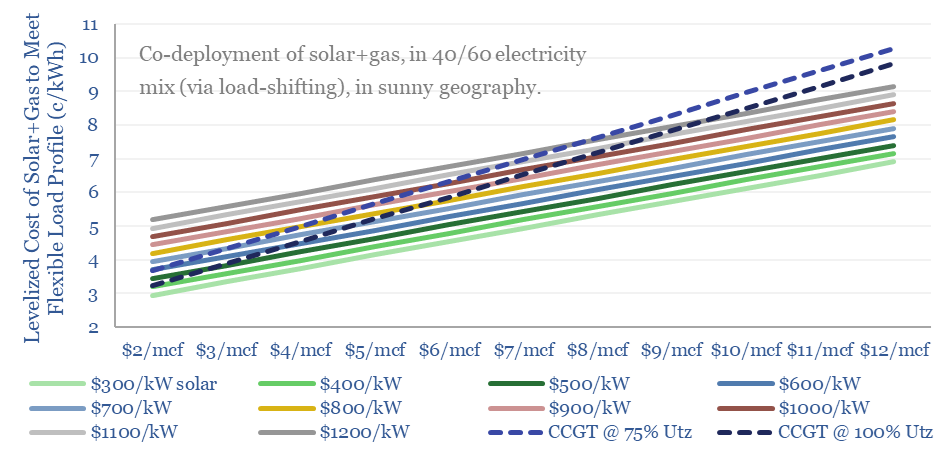

The costs to power a real-world load – e.g., a data center – with solar+gas will very often be more expensive than via a standalone gas CCGT in the US today. But not internationally? Or in the future? This 9-page note shows how solar deflation and load shifting can boost solar to >40% of future grids.

Read the Report?

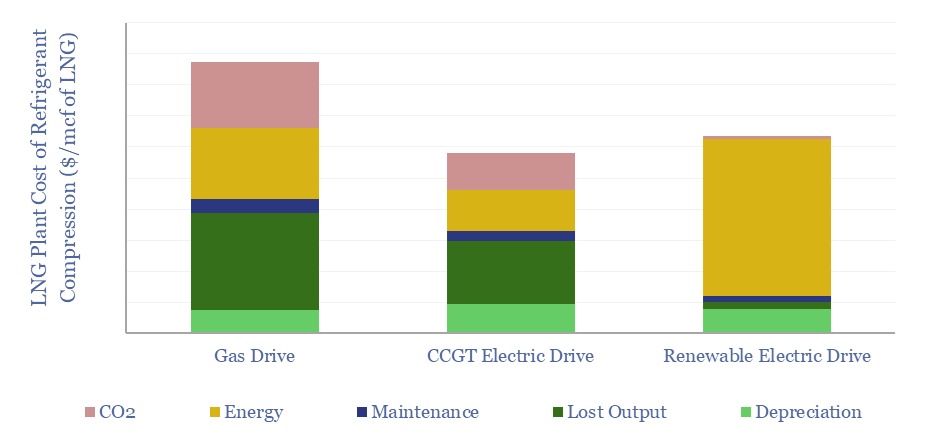

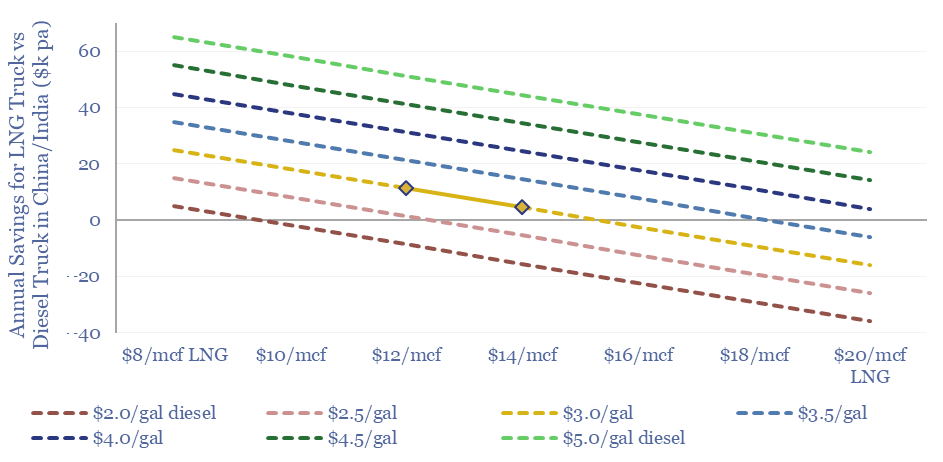

Electric motors were selected, in lieu of industry-standard gas turbines, to power the main refrigeration compressors at three of the four new LNG projects that took FID in 2024. Hence is a major change underway in the LNG industry? This 13-page report covers the costs of e-LNG, advantages and challanges, and who benfits from shifting capex.

Read the Report?

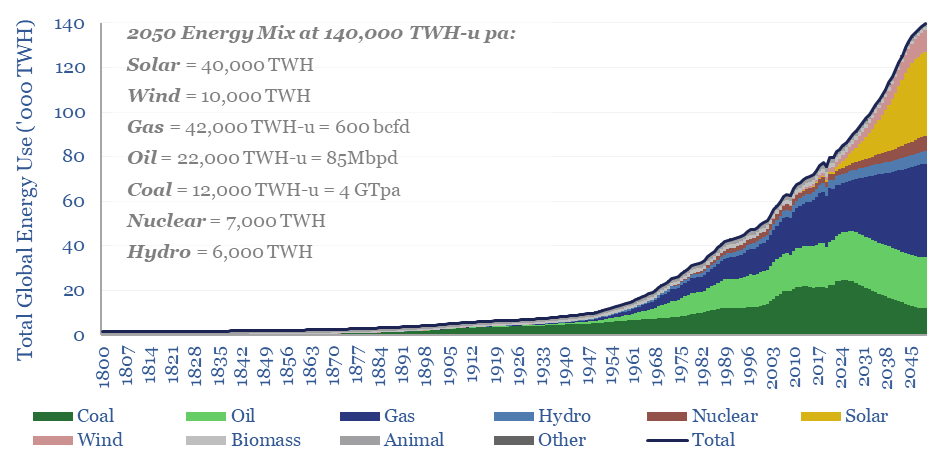

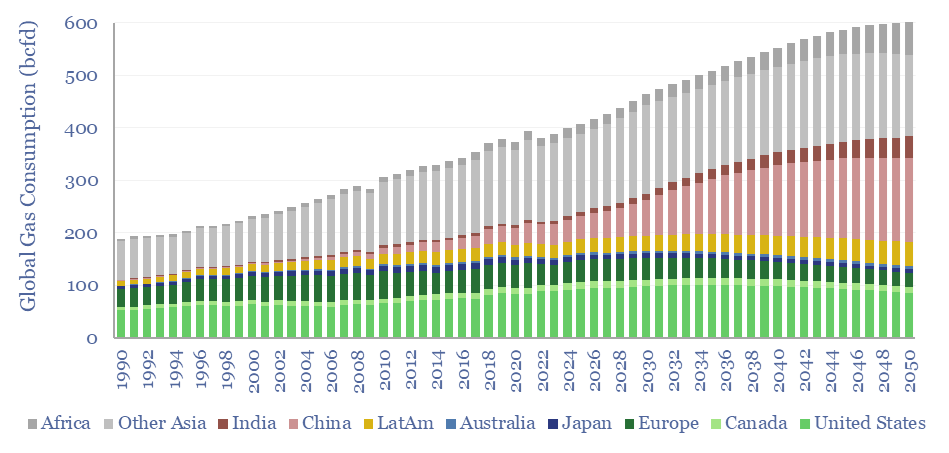

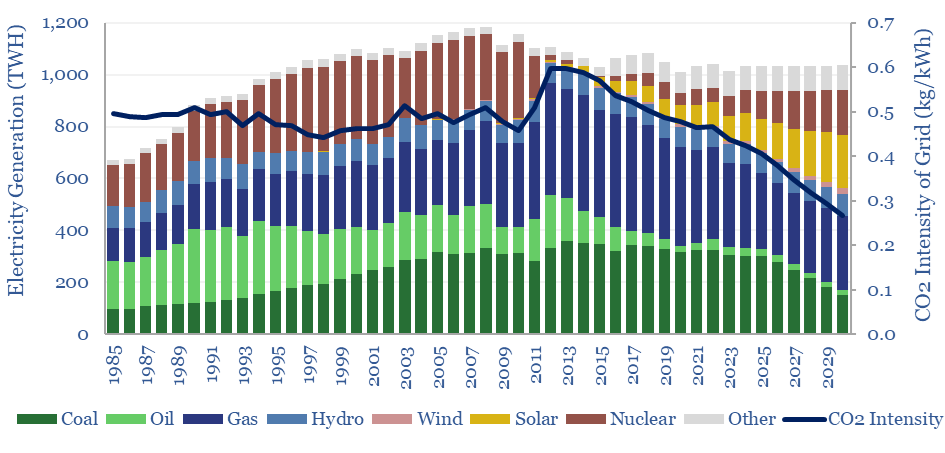

This 15-page note outlines the largest changes to our long-term energy forecasts in five years. Over this time, we have consistently underestimated both coal and solar. Both are upgraded. But we also show how coal can peak after 2030. Global gas is seen rising from 400bcfd in 2023 to 600bcfd in 2050.

Read the Report?

This 11-page report sets out our top ten predictions for 2025, across energy, industrials and climate. Sentiment is shifting. New narratives are emerging for what energy transition is. 2025-30 energy markets look well supplied. The value is in regional arbitrage, volatility, grids, AI and solar.

Read the Report?

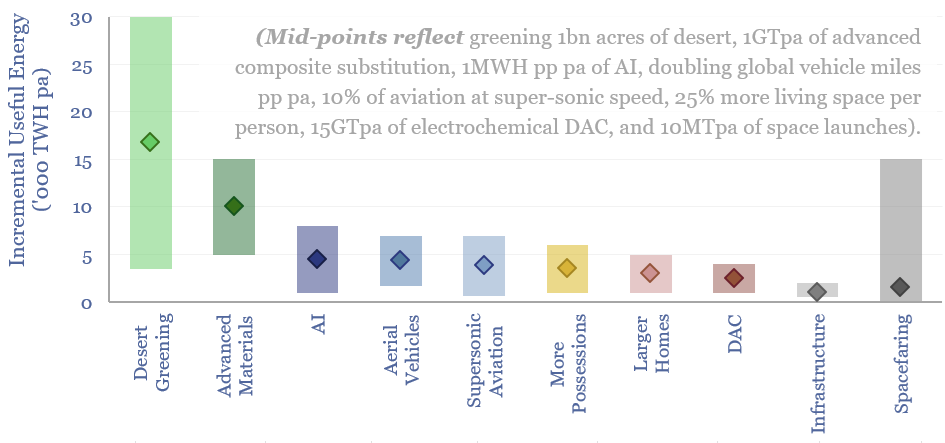

A Kardashev scale civilization uses all the energy it has available. Hence this 16-page report explores ten futuristic uses for global energy, which could absorb an additional 50,000 TWH pa by 2050 (60% upside), mainly from solar. And does this leap in human progress also allay climate concerns better than pre-existing roadmaps to net zero?

Read the Report?

Absorption chillers perform the thermodynamic alchemy of converting waste heat into coolness. Interestingly, their use with solid oxide fuel cells may have some of the lowest costs and CO2 for powering and cooling AI data-centers. This 14-page report explores the opportunity, costs and challenges.

Read the Report?

The grid-forming inverter market may soon inflect from $1bn to $15-20bn pa, to underpin most grid-scale batteries, and 20-40% of incremental solar and wind. This 11-page report finds that grid-forming inverters cost c$100/kW more than grid-following inverters, which is inflationary, but integrate more renewables, raise resiliency and efficiency?

Read the Report?

What if achieving Net Zero by 2050 and/or reaching 1.5ºC climate targets now has a 3% chance of success, for reasons that cause decision-makers to backtrack, and instead focus on climate adaptation and broader competitiveness? This 14-page report reviews the challenges. Can our Roadmap to Net Zero be salvaged?

Read the Report?

Solar trackers are worth $10bn pa. They typically raise solar revenues by 30%, earn 13% IRRs on their capex costs, and lower LCOEs by 0.4 c/kWh. But these numbers are all likely to double, as solar gains share, grids grow more volatile, and AI unlocks further optimizations? This 14-page report explores the theme and who benefits?

Read the Report?

Energy transition is a triple challenge: to meet energy needs, abate CO2 and increase competitiveness. History has now shown that ignoring the part about competitiveness gets you voted out of office?! We think raising competitiveness will be the main focus of the new administration in the US. So this 15-page report discusses overlooked angles around energy competitiveness, and updates our outlook for different themes.

Read the Report?

Groq has developed LPUs for AI inference, which are up to 10x faster and 80-90% more energy efficient than today’s GPUs. This 8-page Groq technology review assesses its patent moat, LPU costs, implications for our AI energy models, and whether Groq could ever dethrone NVIDIA’s GPUs?

Read the Report?

Gas turbines should be considered a key workhorse for a cleaner and more efficient global energy system. Installations will double to 100GW pa in 2024-30, and reach 140GW in 2030, surpassing their prior peak from 2003. This 16-page report outlines four key drivers in our outlook for gas turbines, and their implications.

Read the Report?

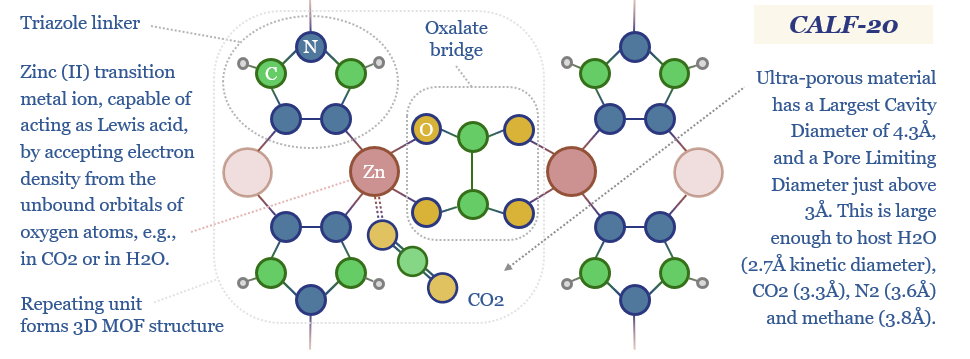

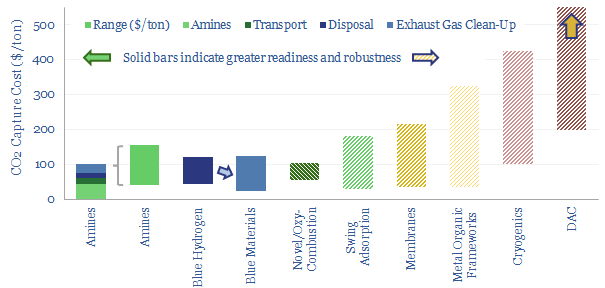

Metal Organic Frameworks (MOFs) are a game-changer for industrial separation, which consumes c10% of global energy. Activity is surging. This 18-page report reviews MOFs’ recent progress and future promise. As a case study, CALF-20 can deflate CCS costs by c50%, per Svante’s TSA process.

Read the Report?

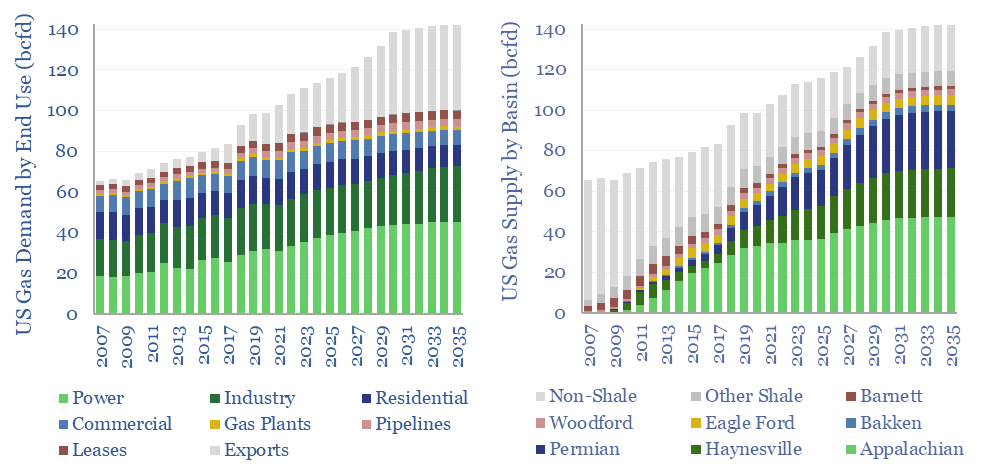

Modeling US gas supply and demand can be nightmarishly complex. Yet we have evaluated both, through 2035. This 13-page report outlines the largest drivers of demand, requires a +3% pa CAGR from the key US shale gas basins, and argues the balance of probability lies to the upside.

Read the Report?

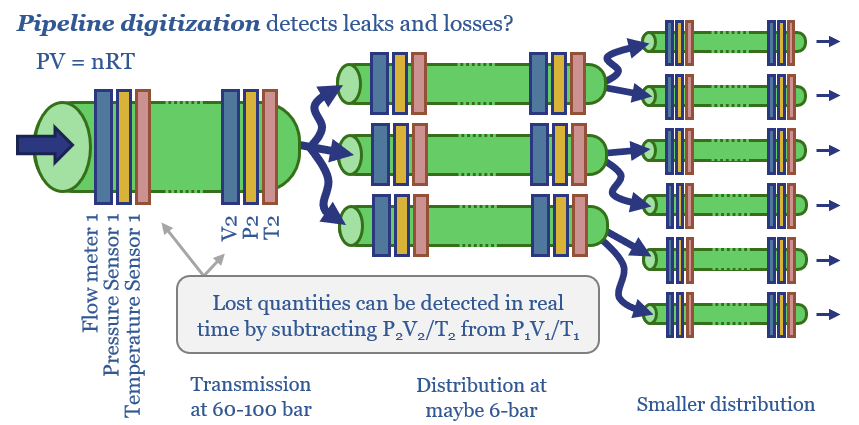

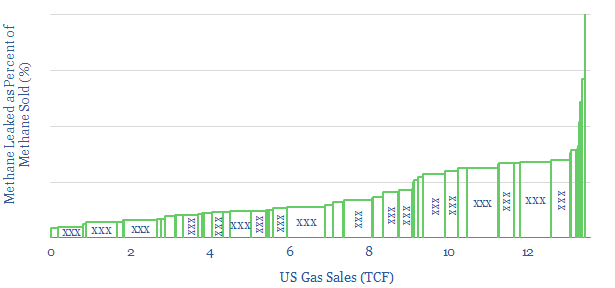

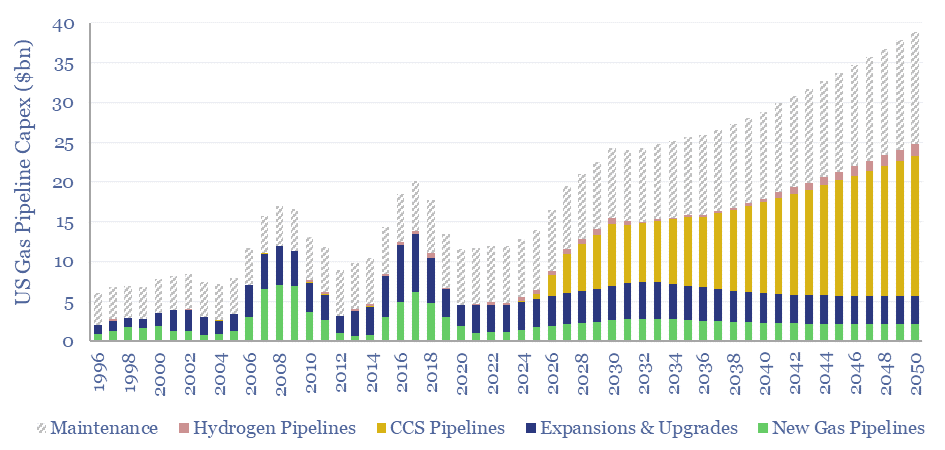

Greater digitization of gas networks looks increasingly important, as gas, biogas, hydrogen and CCS all aim to shore up their futures. This 15-page note started as a deep-dive into the true leakage rates in downstream gas; and ended up finding opportunities in sensors and pipeline monitoring.

Read the Report?

This global energy supply-demand model combines our supply outlooks for coal, oil, gas, LNG, wind and solar, nuclear and hydro, into a build-up of useful global energy balances in 2023-30. Energy markets can be well-supplied from 2025-30, barring and disruptions, but only because emerging industrial superpowers will continuing using high-carbon coal.

Download the Model?

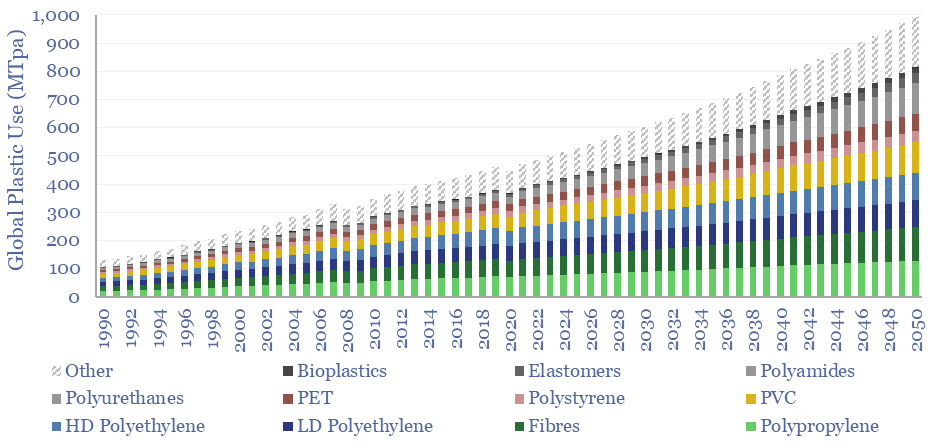

Global plastic is estimated at 470MTpa in 2022, rising to at least 800MTpa by 2050. This data-file is a breakdown of global plastic demand, by product, by region and by end use, with historical data back to 1990 and our forecasts out to 2050. Our top conclusions for plastic in the energy transition are summarized.

Download the Model?

Global gas supply-demand is predicted to rise from 400bcfd in 2023 to 600bcfd by 2050, in our outlook, while achieving net zero would require ramping gas even further to 800bcfd, as a complement to wind, solar, nuclear and other low-carbon energy. This data-file quantifies global gas demand and supply by country.

Download the Model?

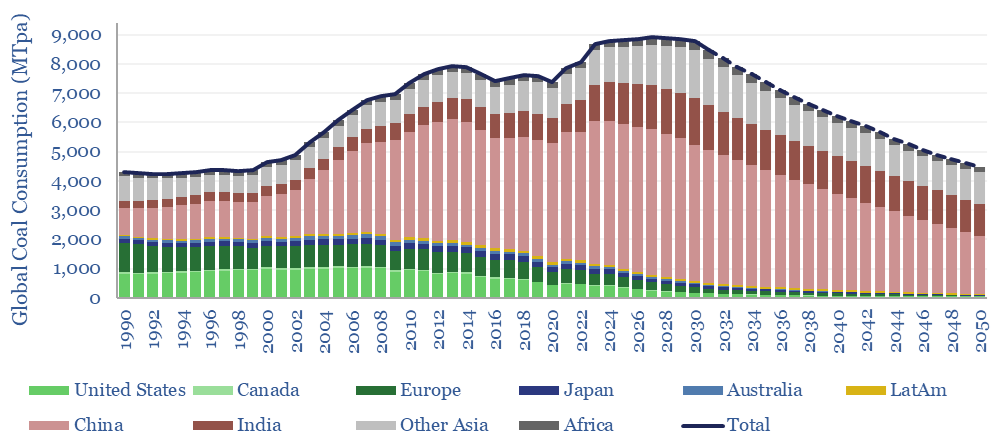

Global coal use likely hit a new all-time peak of 8.8GTpa in 2024, of which 7.6GTpa is thermal coal and 1.1GTpa is metallurgical. The largest consumers are China (5GTpa), India (1.3GTpa), other Asia (1.2GTpa), Europe (0.4GTpa) and the US (0.4GTpa). This model presents our forecasts for global coal supply-demand from 1990 to 2050.

Download the Model?

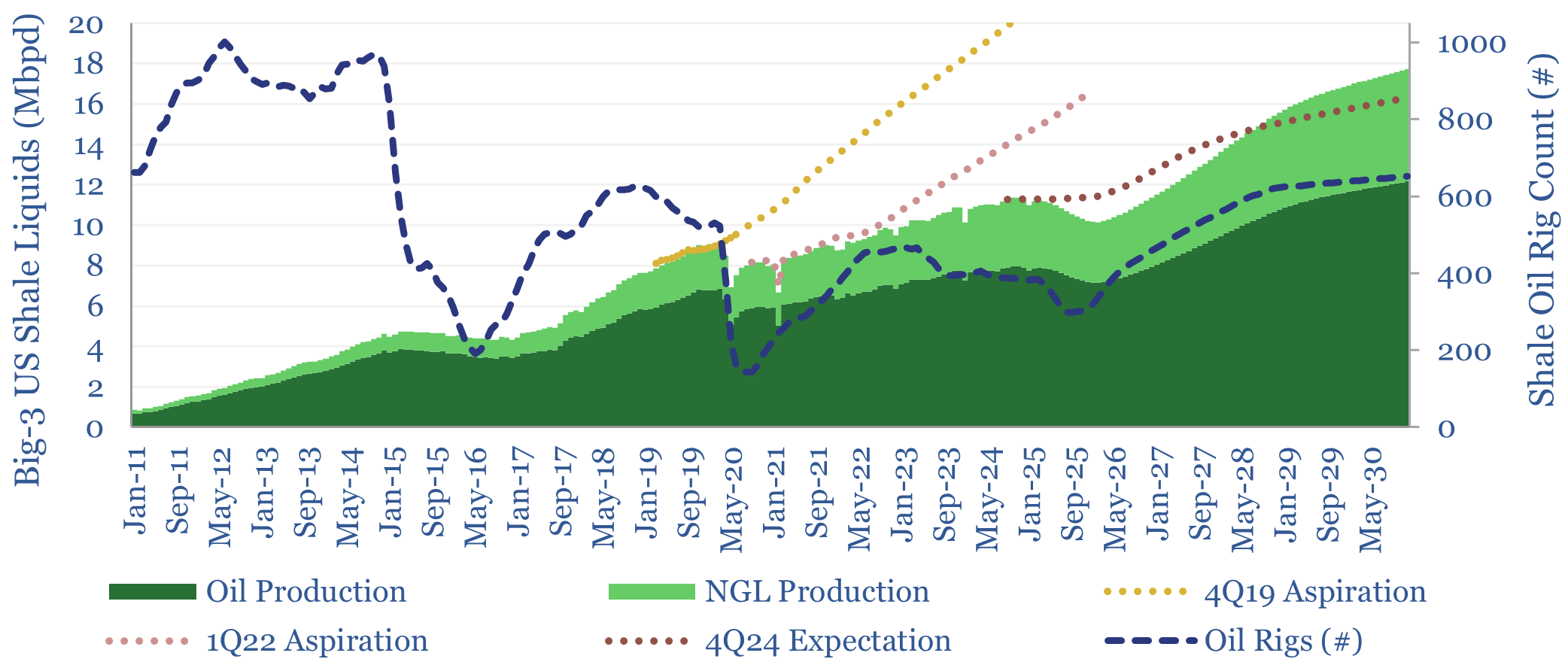

This model sets out our US shale production forecasts by basin. It covers the Permian, Bakken, Eagle Ford, Marcellus/Utica and Haynesville, as a function of the rig count, drilling productivity, completion rates, well productivity and type curves. The data-file was last updated in May-2025, revising liquids growth negative in 2025-26, which in turn tightens US gas markets?

Download the Model?

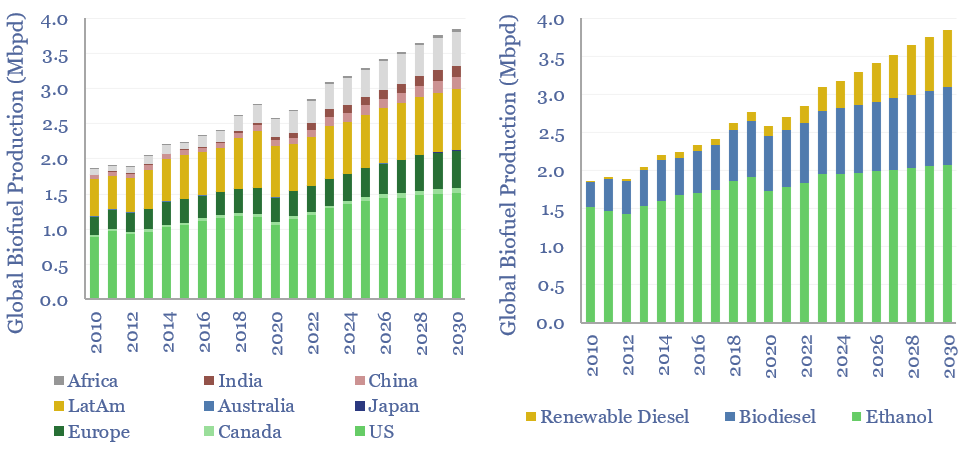

Global liquid biofuel production ran at 3.2Mbpd in 2024, of which c60% is ethanol, c30% is biodiesel and c10% is renewable diesel. 65% of global production is from the US and Brazil. Global liquid biofuel production reaches 3.8Mbpd by 2030 on our forecasts.

Download the Model?

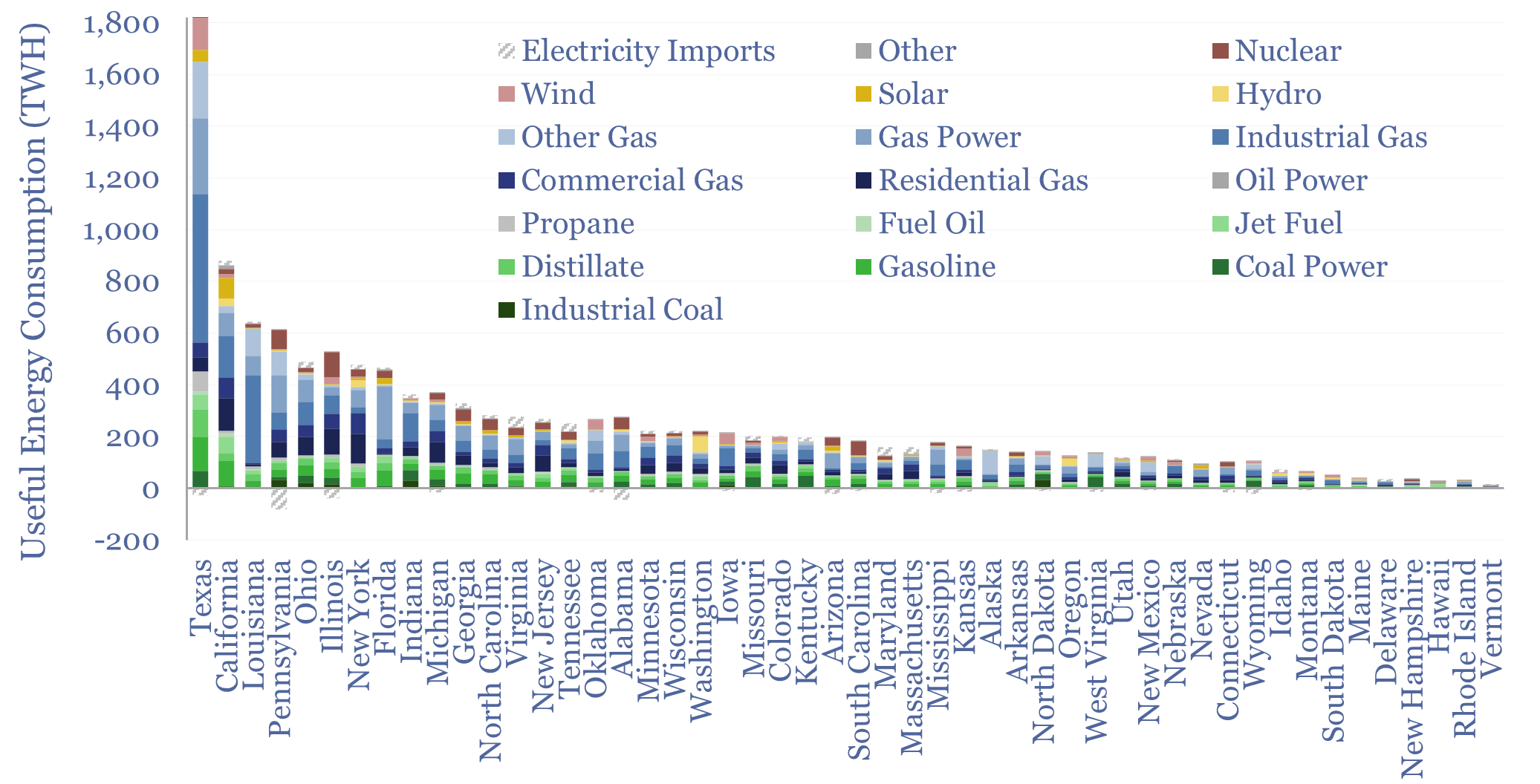

Australia’s useful energy consumption rises from 820TWH pa in 2023, by 1.2% pa 1,100 TWH pa in 2050. As a world-leader in renewables, it makes for an interesting case study. This Australia energy supply-demand model is disaggreated across 215 line items, broken down by source, by use, from 1990 to 2023, and with our forecasts to 2050.

Download the Model?

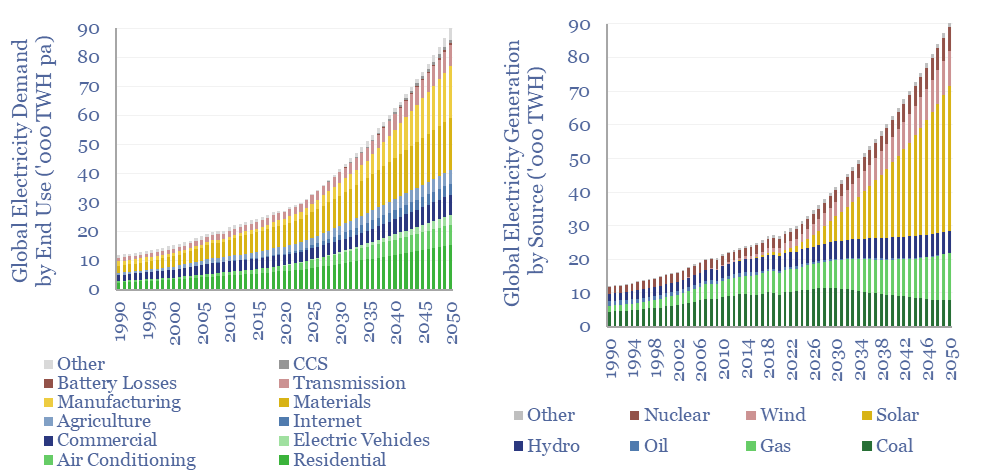

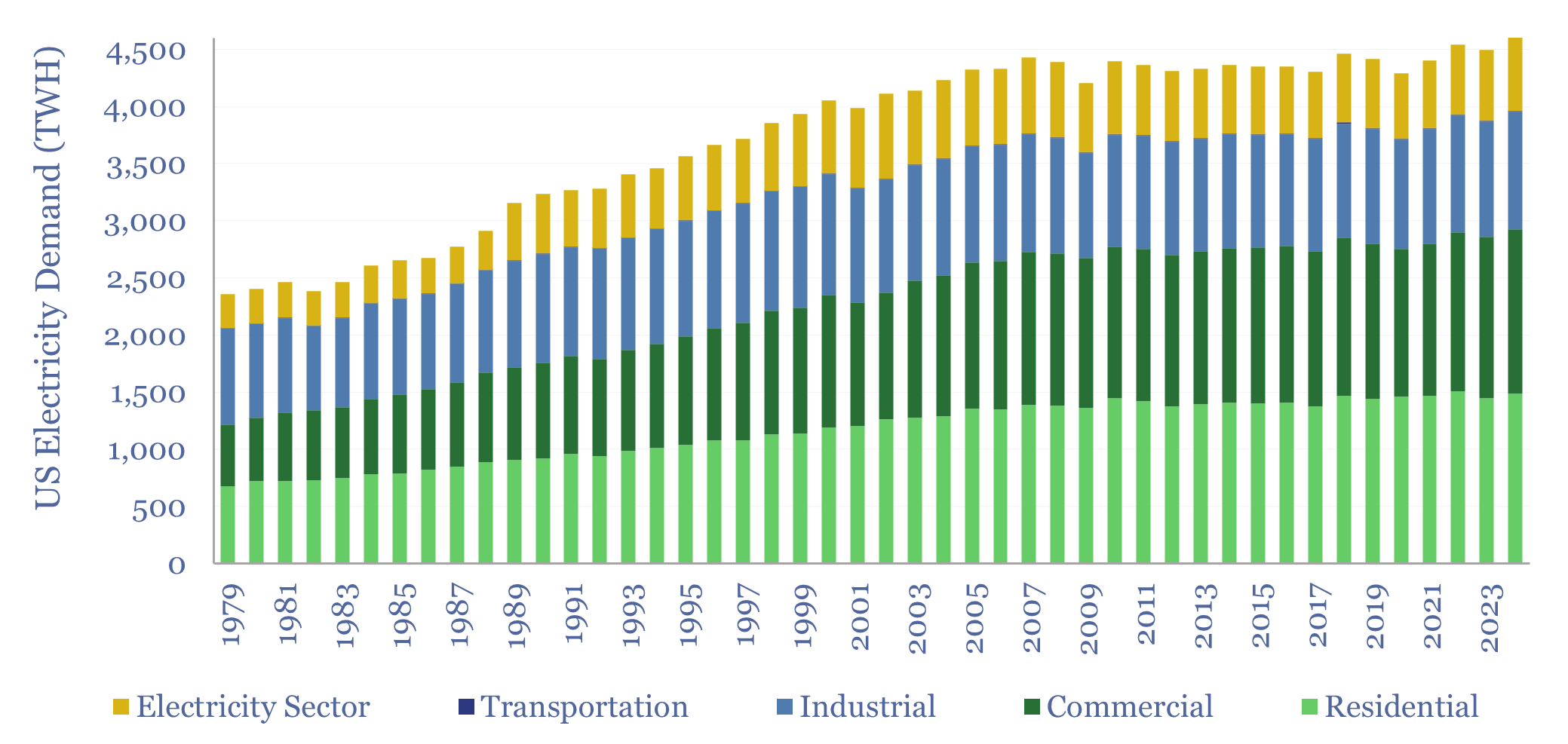

Global electricity supply-demand is disaggregated in this data-file, by source, by use, by region, from 1990 to 2050, triangulating across all of our other models in the energy transition, and culminating in over 50 fascinating charts, which can be viewed in this data-file. Global electricity demand rises 3x by 2050 in our outlook.

Download the Model?

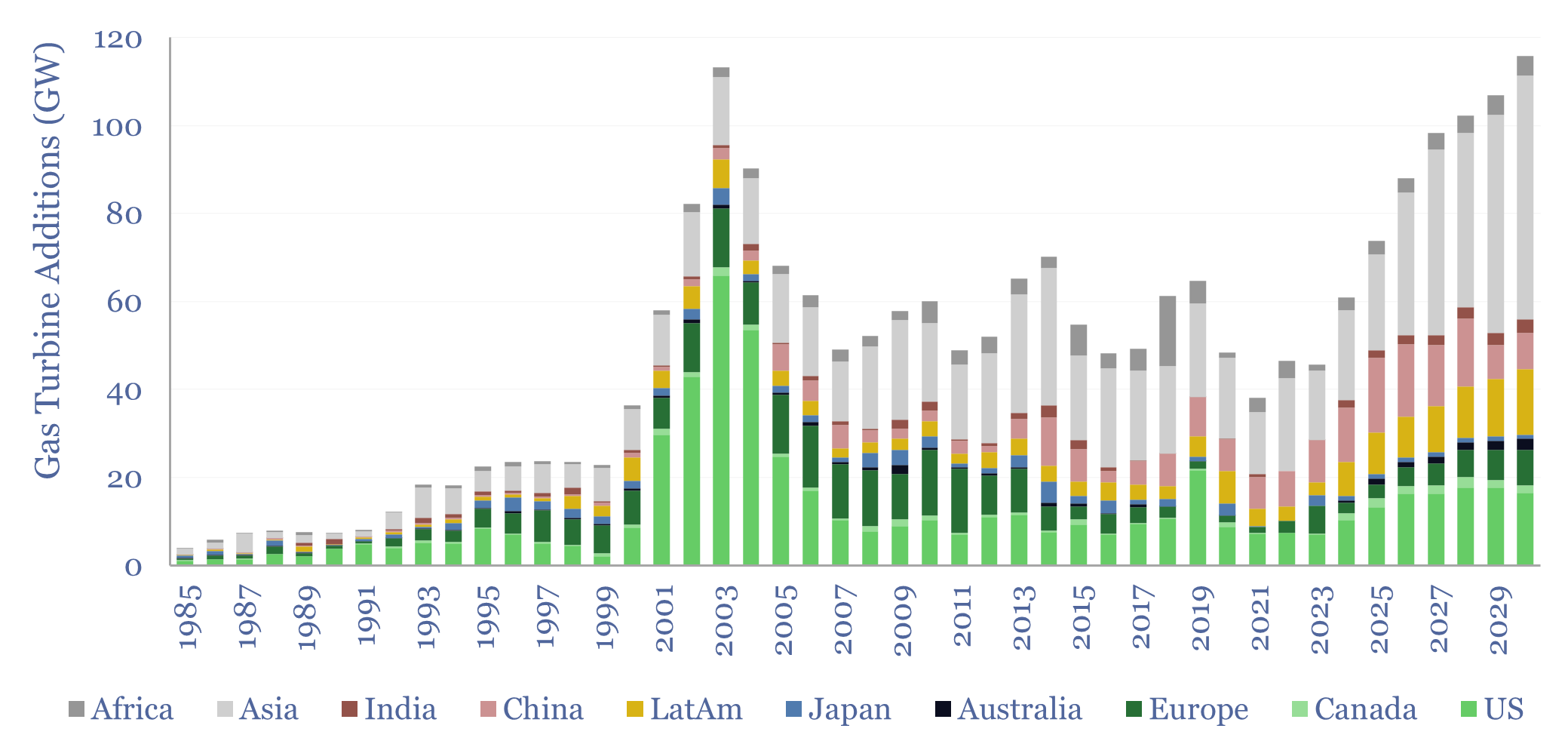

Global gas turbine additions averaged 50 GW pa over the decade from 2015-2024, of which the US was 20%, Europe was 10%, Asia was 50%, LatAm was 10% and Africa was 10%. Yet global gas turbine additions could double to 100 GW pa in 2025-30. This data-file estimates global gas turbine capacity by region and over time.

Download the Model?

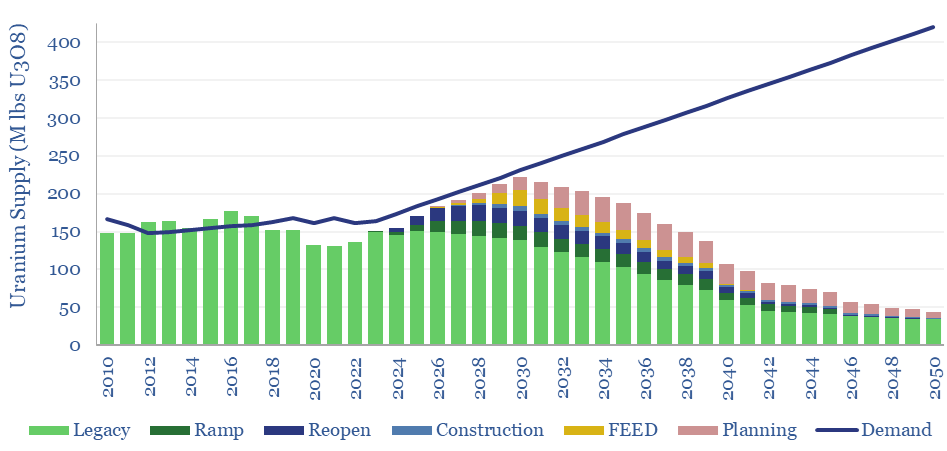

Our global uranium supply-demand model sees the market 5% under-supplied through 2030, including 7% market deficits at peak in 2025, as demand ramps from 165M lbs pa to 230M lbs pa in 2030. This is even after generous risking and no room for disruptions. What implications for broader power markets, decarbonization ambitions, and uranium prices?

Download the Model?

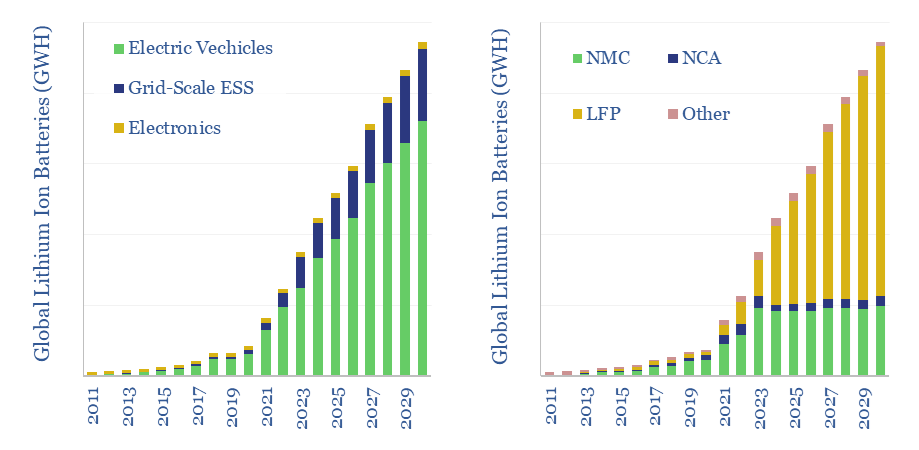

The lithium ion battery market reached 900GWH in 2023, representing 7x growth in the past half-decade since 2018, and 20x growth in the past decade since 2013. Volumes treble again by 2030. This data-file breaks down global ithium ion battery volumes by chemistry and be end use. A remarkable shift to LFP is underway, and NMC sales may even have peaked.

Download the Model?

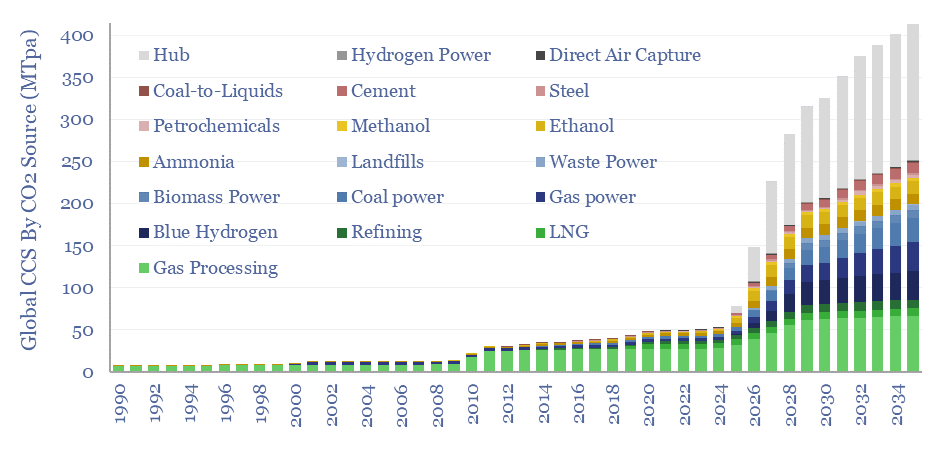

Over 400 CCS projects are tracked in our global CCS projects database. The average project is 2MTpa in size, with capex of $600/Tpa, underpinning over 400MTpa of risked global CCS by 2035, up 10x from 2019 levels. The largest CO2 sources are hubs, gas processing, blue hydrogen, gas power and coal power. The most active countries are the US, UK, Canada and Europe.

Download the Model?

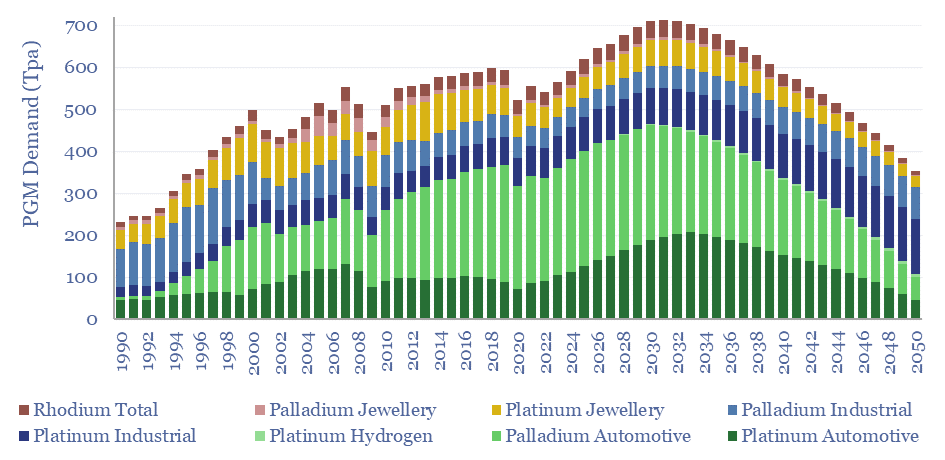

Core global PGM demand ran at 565 tons in 2023, which remains c6% lower than the all-time peak demand of 600Tpa in 2019. We model a recovery to 700 Tpa of demand for platinum, palladium and rhodium in 2030, then a long run decline to 350Tpa if EVs ultimately reach 90% of vehicle sales by 2050. Numbers can be stress-tested in this model.

Download the Model?

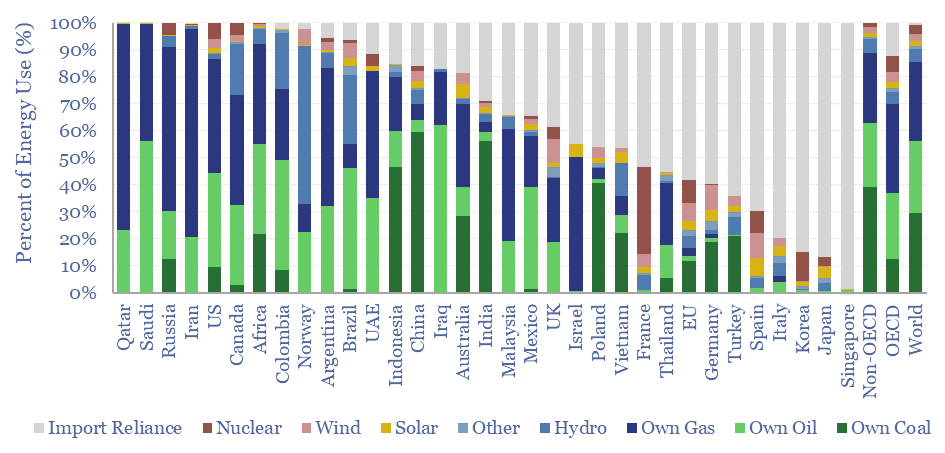

This data-file tabulates energy self-sufficiency, by country, over time, across 30 of the largest economies in the world. Among this sample, the median country generates 70% of its energy domestically, and is reliant on imports for 30% of the remainder. Energy self-sufficiency varies vastly by country.

Download the Model?

Japan’s gas and power markets are broken down by end use, traced back to 1990, and forecast forwards to 2030 in this model. Japan’s electricity demand now grows at 0.3% pa. Ramping renewables, nuclear and gas back-ups could halve Japan’s total grid CO2 intensity to below 0.25 kg/kWh by 2030.

Download the Model?

Global population and GDP are broken down in this data-file, across 10 key regions, with data back to 1960 and projections to 2050, as an input to all of our supply-demand models. Population rises at 0.7% pa from 8.0bn in 2023 to 9.7bn in 2050. Real global GDP rises at 2.5% from $105trn in 2023 to $200trn by 2050. Mega-trends are underway in demographics, manufacturing and defence.

Download the Model?

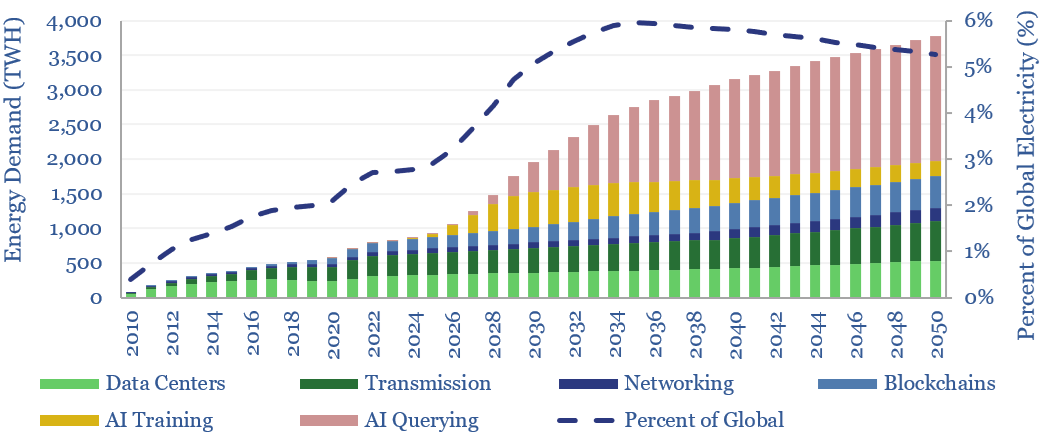

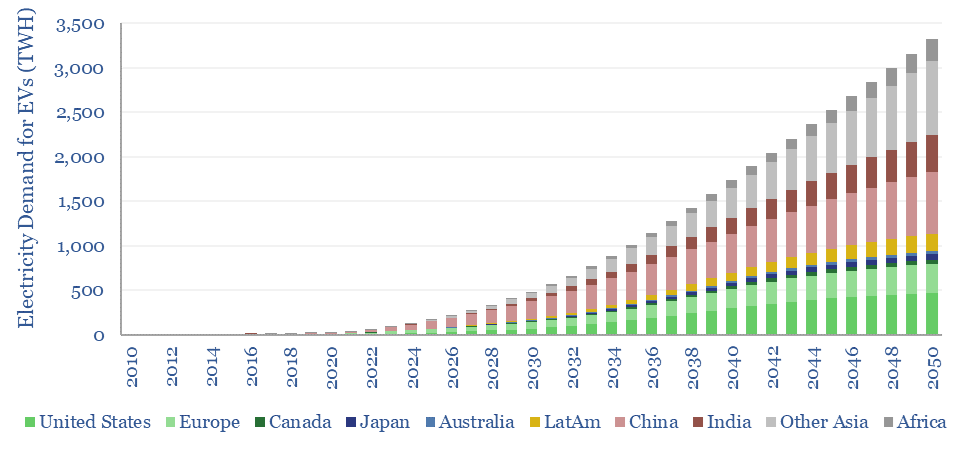

This data-file forecasts the energy consumption of the internet, rising from 800 TWH in 2022 to 2,000 TWH in 2030 and 3,750 TWH by 2050. The main driver is the energy consumption of AI, plus blockchains, rising traffic, and offset by rising efficiency. Input assumptions to the model can be flexed. Underlying data are from technical papers.

Download the Model?

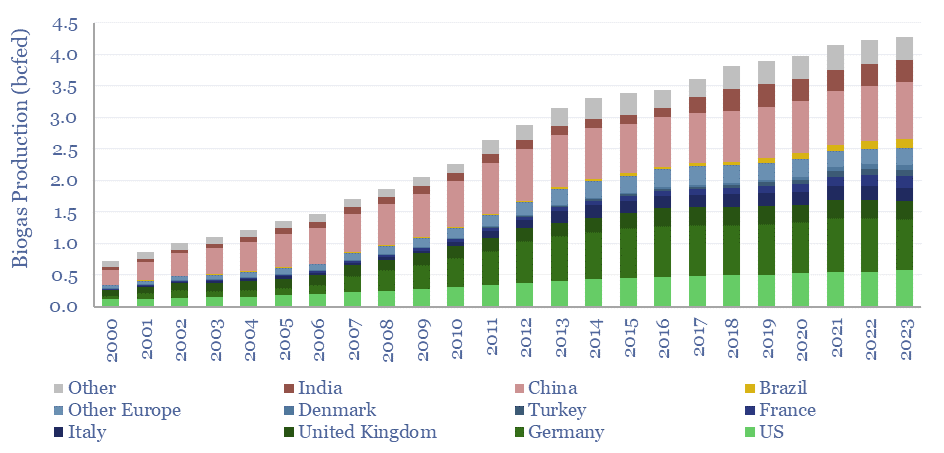

Global biogas production has risen at a 10-year CAGR of 3% to reach 4.3bcfed in 2023, equivalent to 1.1% of global gas consumption. Europe accounts for half of global biogas, helped by $4-40/mcfe subsidies. This data-file aggregates global biogas production by country, plus notes into feedstock sources, uses of biogas and biomethane.

Download the Model?

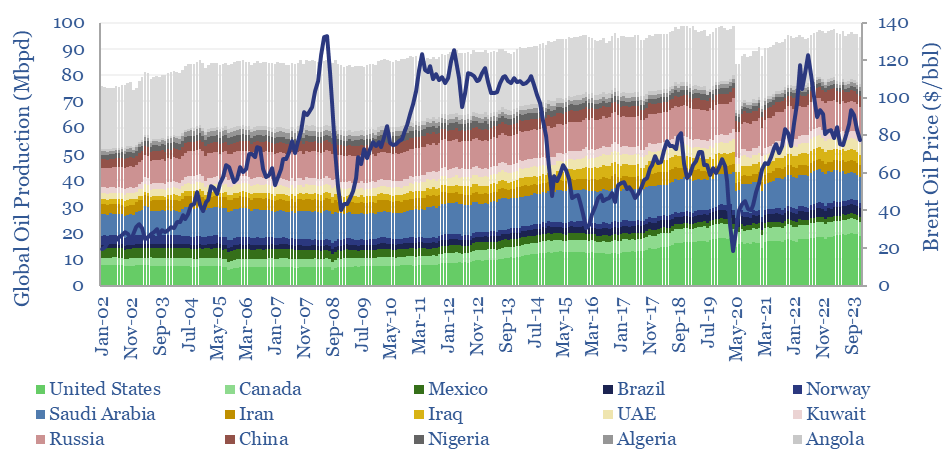

Global oil production by country by month is aggregated across 35 countries that produce 80kbpd of crude, NGLs and condensate, explaining >96% of the global oil market. Production has grown by +1Mbpd/year in the past two-decades, led by the US, Iraq, Russia, Canada. Oil market volatility is usually low, at +/- 1.5% per year, of which two-thirds is down to conscious decisions.

Download the Model?

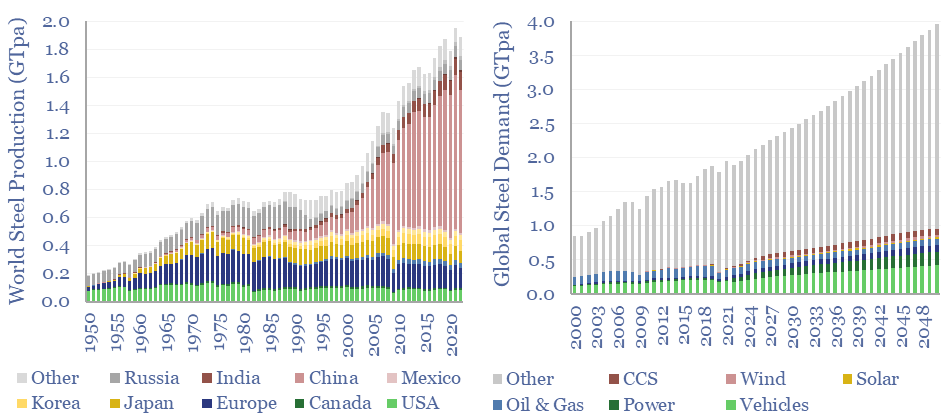

Global steel supply-demand runs at 2GTpa in 2023, having doubled since 2003. Our best estimate is that steel demand rises another 80%, to 3.6GTpa by 2050, including due to the energy transition. Global steel production by country is now dominated by China, whose output exceeds 1GTpa, which is 8x the #2 producer, India, at 125MTpa.

Download the Model?

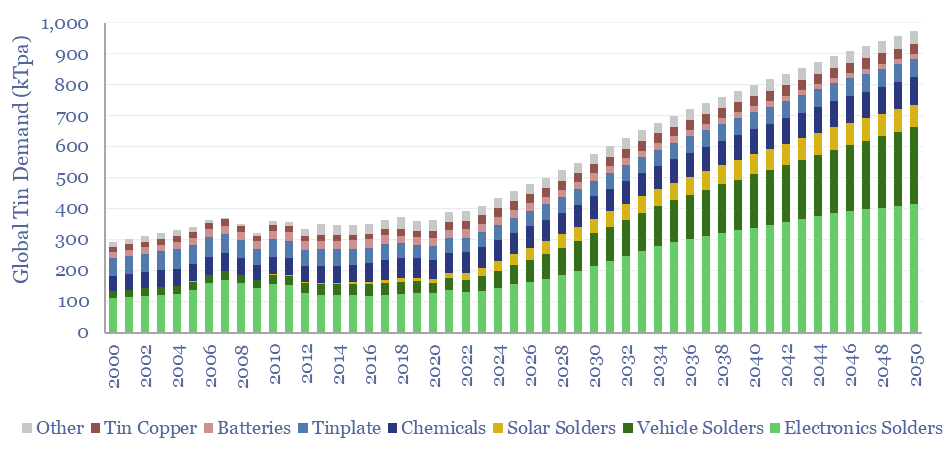

Global tin demand stands at 400kTpa in 2023 and rises by 2.5x to 1MTpa in 2050 as part of the energy transition. 50% of today’s tin market is for solder, which sees growing application in the rise of the internet, rise of EVs and rise of solar. Global tin supply and demand can be stress-tested in the model.

Download the Model?

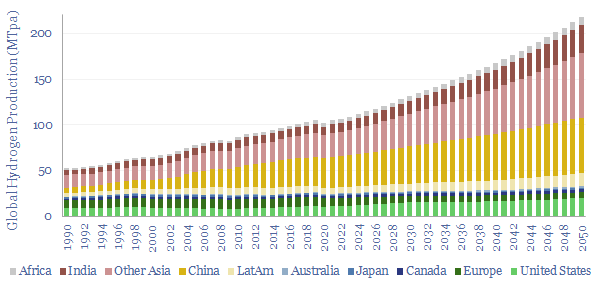

Global production of hydrogen is around 110MTpa in 2023, of which c30% is for ammonia, 25% is for refining, c20% for methanol and c25% for other metals and materials. This data-file estimates global hydrogen supply and demand, by use, by region, and over time, with projections through 2050.

Download the Model?

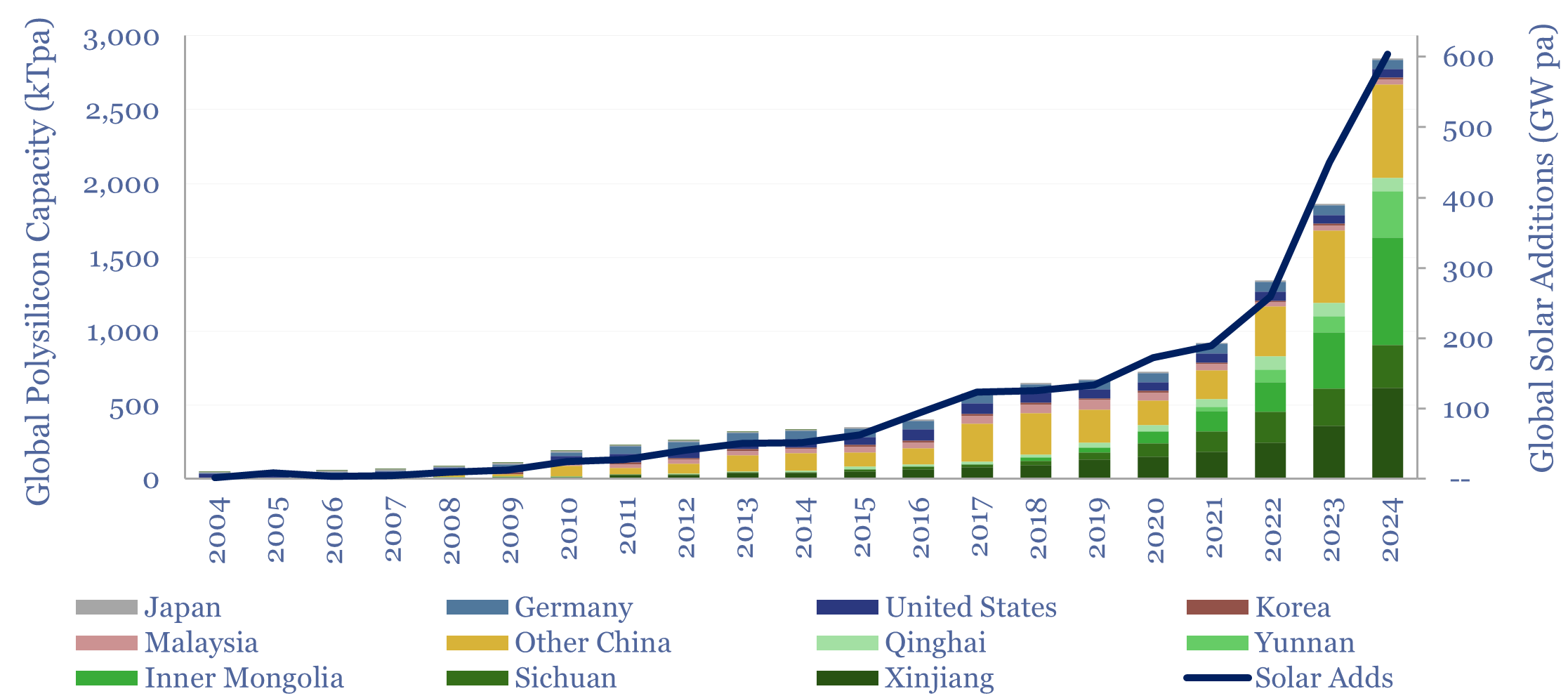

Polysilicon is a highly pure, crystalline silicon material, used predominantly for photovoltaic solar, and also for ‘chips’ in the electronics industry. Global polysilicon capacity reached 3MTpa in 2024, and global polysilicon production surpassed 1.7MTpa in 2024. China now dominates the industry, approaching 94% of all global capacity.

Download the Model?

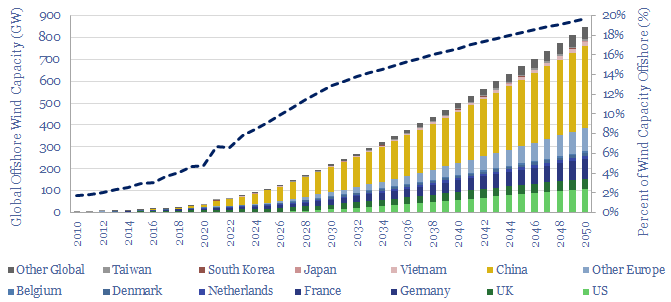

Global offshore wind capacity stood at 60GW at the end of 2022, rising at 8GW pa in the past half decade, comprising 7% of all global wind capacity, and led by China, the UK and Germany. Our forecasts see 220GW of global offshore wind capacity by 2030 and 850GW by 2050, which in turn requires a 15x expansion of this market.

Download the Model?

European gas and power markets will look better-supplied than they truly are in 2023-24. A dozen key input variables can be stress-tested in the data-file. Overall, we think Europe will need to source over 15bcfd of LNG through 2030, especially US LNG.

Download the Model?

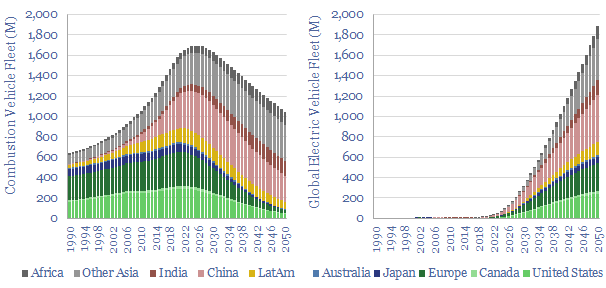

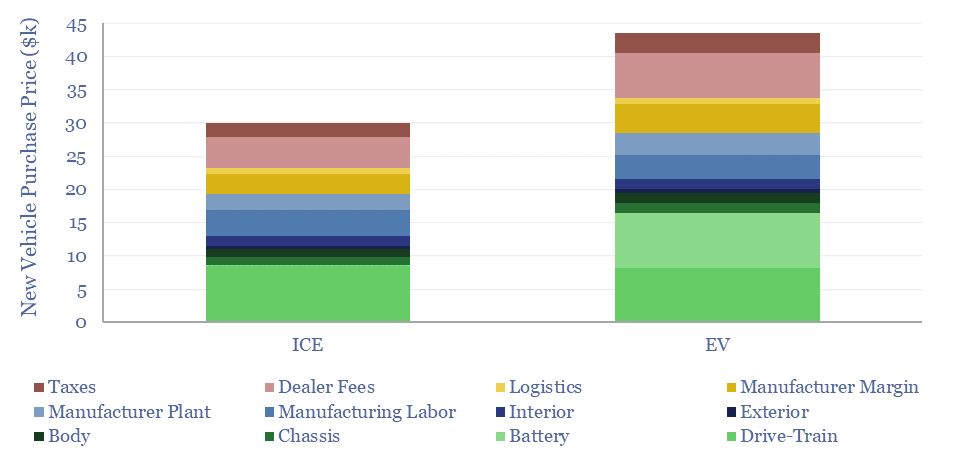

We have modeled the global light vehicle fleet, light vehicle sales by region, and the world’s shift from internal combustion engines (ICEs) towards electric vehicles (EVs) through 2050. Our base case model sees almost 200M EV sales by 2050, and a c40% decline to around 1bn combustion vehicles in the world’s fleet by 2050.

Download the Model?

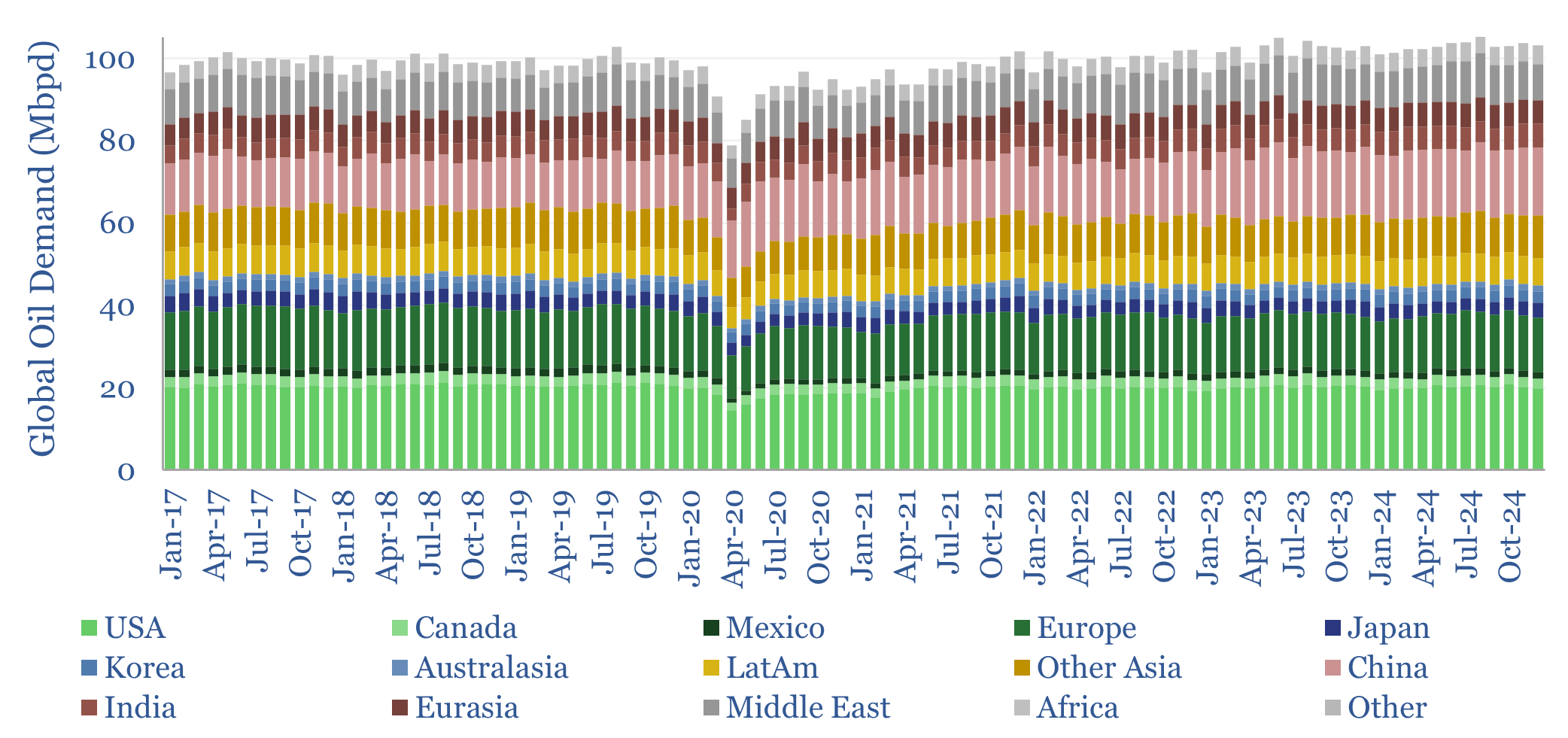

This data-file breaks down global oil demand, country-by-country, product-by-product, month-by-month, across 2017-2024. Global oil demand ran at 103 Mbpd in 2024, for +1.0 Mbpd of growth, according to our databases. For perspective, global oil demand rose at +1.2Mbpd per year in the 30-years from 1989->2019, so not much evidence, on face value, that “peak oil is nigh”.

Download the Model?

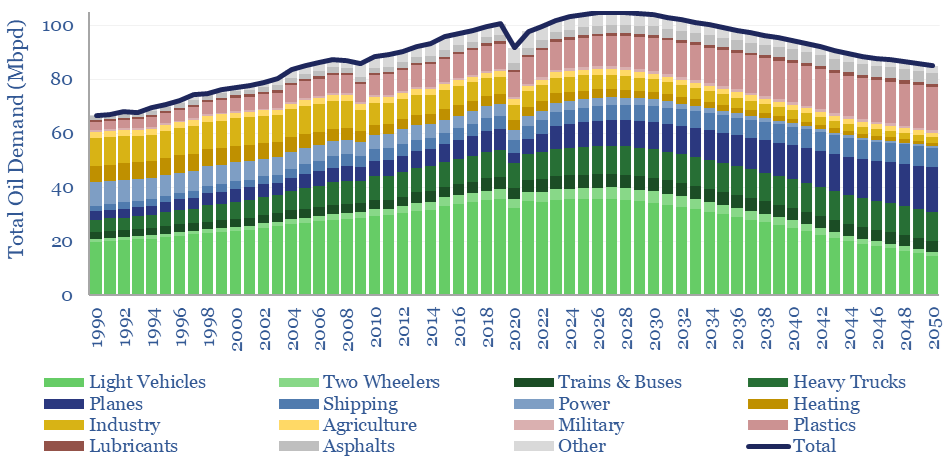

This model forecasts long-run oil demand to 2050, by end use, by year, and by region; across the US, the OECD and the non-OECD. We see demand gently rising through the 2020s, peaking at 105Mbpd in 2026-28, then gently falling to 85Mbpd by 2050 in the energy transition.

Download the Model?

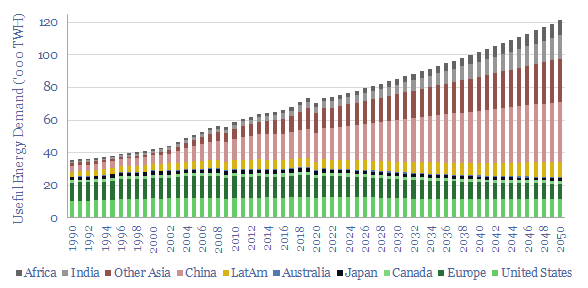

This model captures global energy demand by region through 2050, rising from 70,000 TWH in 2019-22 to 120,000 MWH in 2050. Demand rises c2% pa. Energy use per global person rises at 1% pa from 9.3 MWH pp pa to 12.6 MWH pp pa. Meeting human civilization’s energy needs is crucial to the energy transition.

Download the Model?

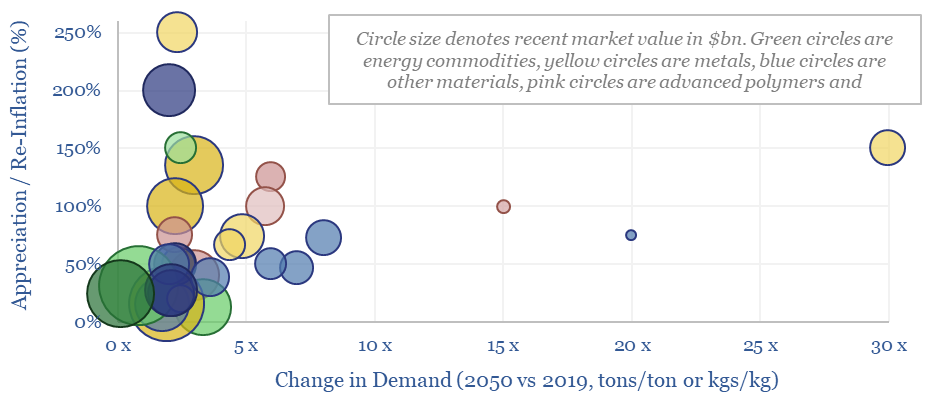

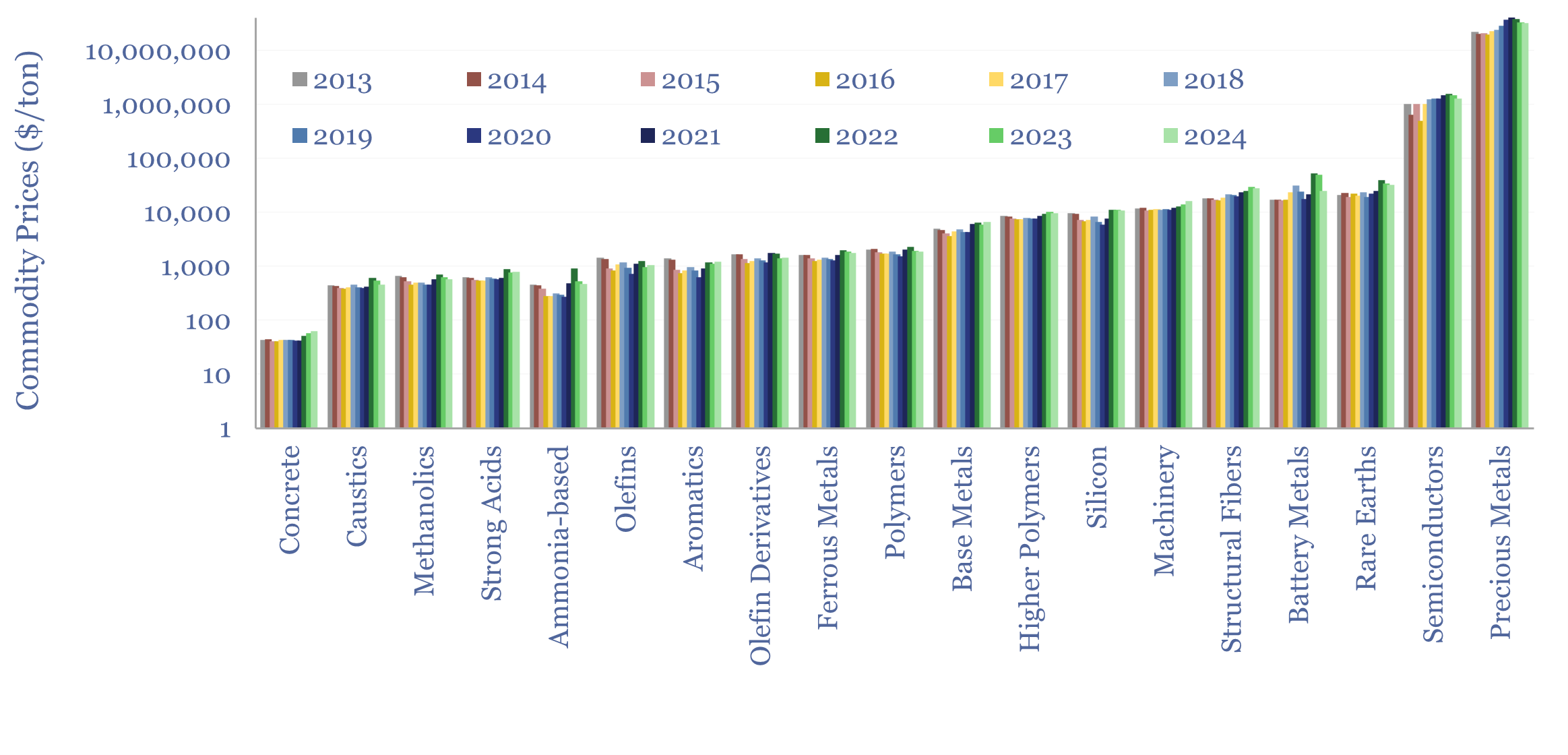

This data-file summarizes our latest thesis on ten commodities with upside in the energy transition. The average one will see demand rise by 3x and price/cost appreciate or re-inflate by 100%. The data-file contains a 6-10 line summary of our work into each commodity.

Download the Model?

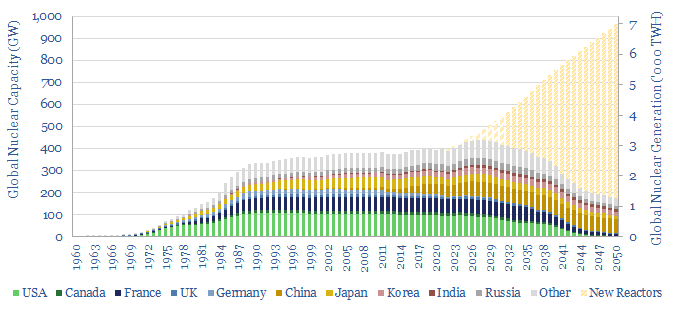

How much nuclear capacity would need to be constructed in our roadmap to net zero? This breakdown of global nuclear capacity forecasts that 30 GW of new reactors must be brought online each year through 2050, if the nuclear industry was to ramp up to 7,000 TWH of generation by 2050, which would be 6% of total global energy. There is a precedent. Delaying shutdowns helps too.

Download the Model?

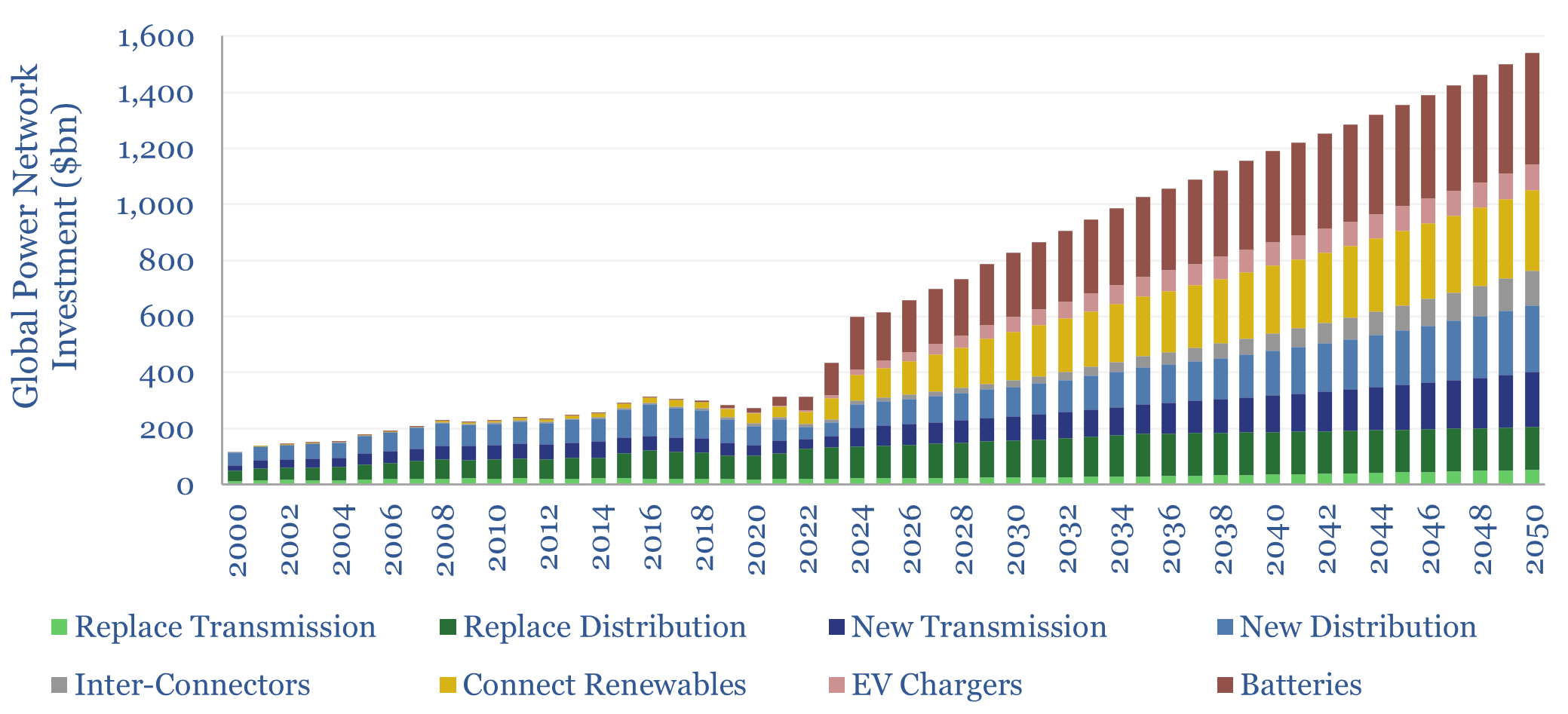

Global investment into power networks averaged $280bn per annum in 2015-20, of which two-thirds was for distribution and one-third was for transmission. Amazingly, these numbers step up to $600bn in 2030, >$1trn in the 2040s and can be as large as all primary energy investment.

Download the Model?

The US consumes 25,000 TWH of primary energy per year, which equates to 13,000 TWH of useful energy, and emits 6GTpa of CO2. This model captures our best estimates for what a pragmatic and economical decarbonization of the US will look like, reaching net zero in 2050, with forecasts for wind, solar, nuclear, hydro, oil, gas and coal consumption.

Download the Model?

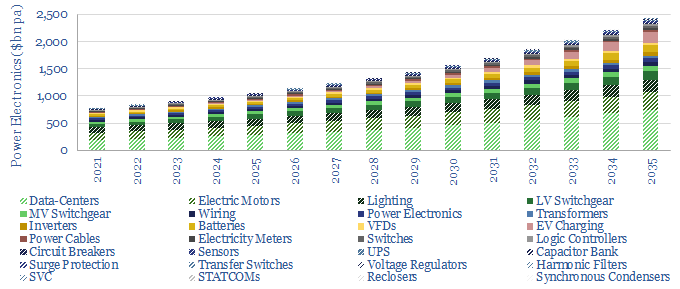

We describe c15 problems incurred by industrial and commercial power consumers. Many will require additional investment as renewables replace the large rotating generators of traditional power grids. Hence we see the market for commercial and industrial power electronics trebling from $360bn pa in 2021 to $1trn pa by 2035.

Download the Model?

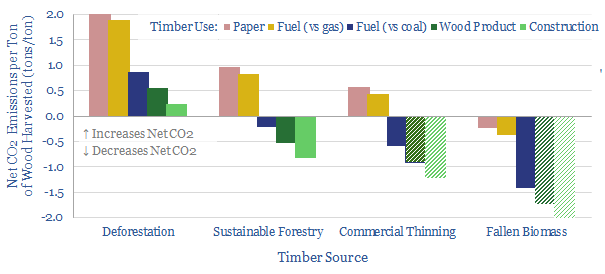

This data-file quantifies global wood production, country-by-country, back to 1960, across energy, pulp and longer-lasting materials. Overall, wood energy has declined from 11% of the world’s primary energy mix in 1960 to c4% today, but it remains stubbornly high in less-developed countries, amplifying deforestation.

Download the Model?

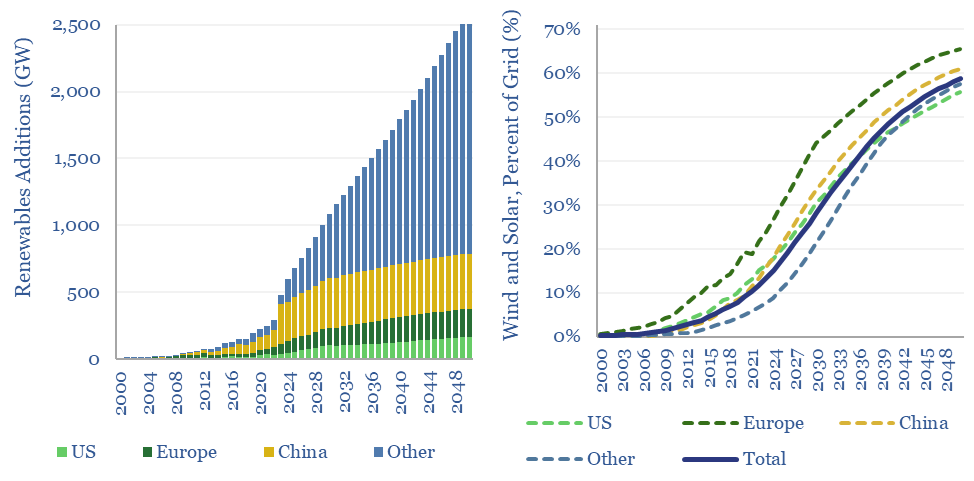

Global wind and solar capacity additions reached 600GW pa (AC-basis) in 2024, which is 2x higher than in 2021 and 10x higher than in 2011. The pace of gross wind and solar capacity additions can rise by a further 5x by 2050, bringing wind and solar to 60% of a greatly expanded global power grid by 2050. Most of the upside is in solar.

Download the Model?

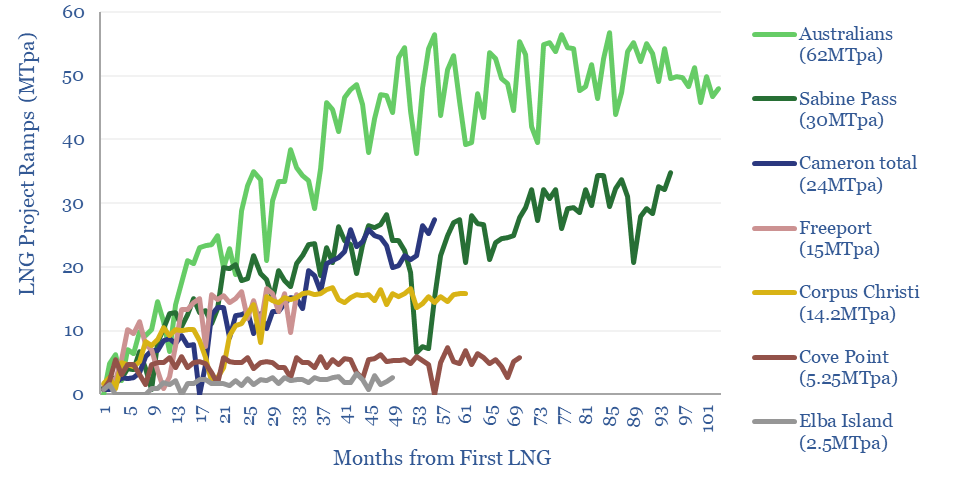

Global LNG output ran at 406MTpa in 2024. This model estimates global LNG production by facility across 150 LNG facilities. Our latest forecasts are that global LNG demand will rise at a 6% CAGR, to reach 710MTpa by 2035, for an absolute growth rate of +30MTpa per year, but there is a supply-crunch in 2024-26, then a construction boom?

Download the Model?

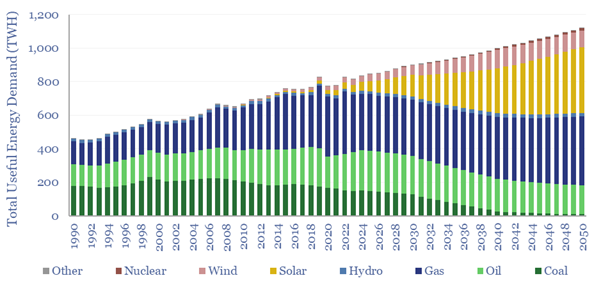

This data-file is a global energy market model for the energy transition. It contains long-term energy supply-demand forecasts by energy source; based on a dozen core input assumptions. Total useful energy consumed by human civilization rises from 80,000 TWH pa to 140,000 TWH pa by 2050. The mix is 30% gas, 30% solar, 15% oil, 8% coal, 7% wind, 5% nuclear, 4% hydro. Numbers can be stress-tested in the data-file.

Download the Model?

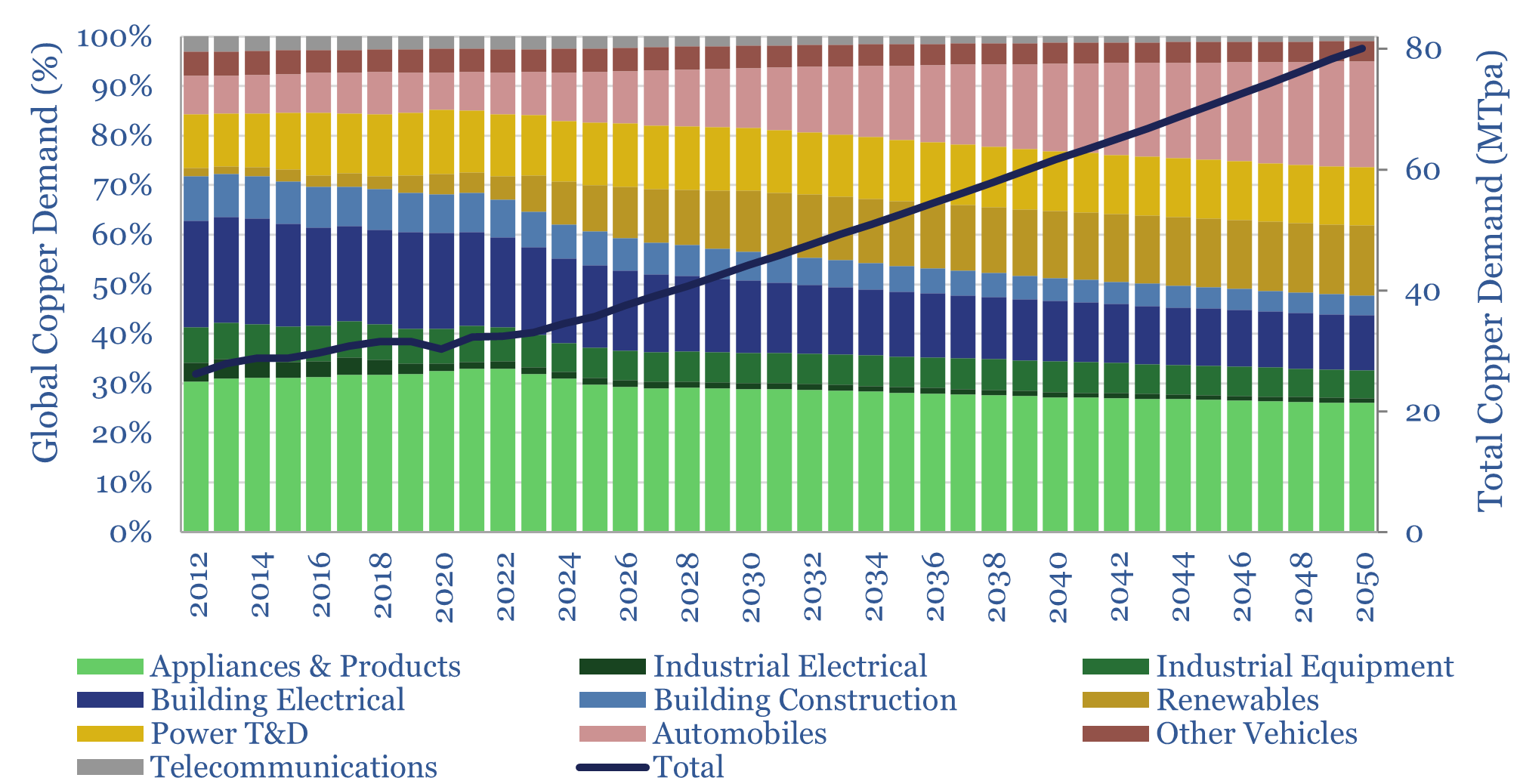

This data-file estimates global copper demand as part of the energy transition, rising from 33MTpa in 2023 to 44MTpa in 2030 and 80MTpa by 2050. Key demand drivers are solar, EVs, greater AC adoption and possibly drones and robotics. You can stress test half-a-dozen key input variables in the model.

Download the Model?

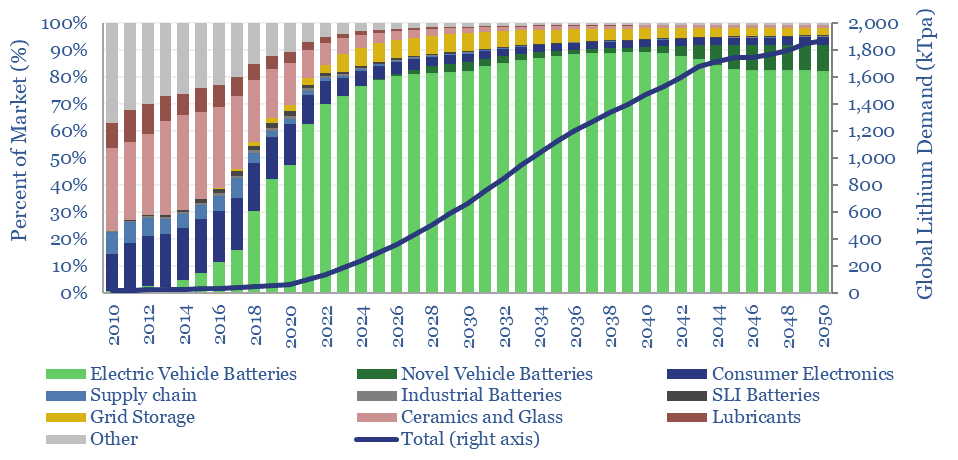

This data-file estimates global demand for lithium as part of the energy transition. The market has already trebled from 23kTpa in 2010 to 65kTpa in 2020, while we see the ascent continuing to 500kTpa in 2030 and almost 2MTpa in 2050. 90% is driven by transport. Global reserves suffice to cover the demand.

Download the Model?

This data-file provides an overview of energy economics, across 175 different economic models constructed by Thunder Said Energy, in order to put numbers in context. This helps to compare marginal costs, capex costs, energy intensity, interest rate sensitivity, and other key parameters that matter in the energy transition.

Download the Model?

The economics costs of reciprocating gas engines are captured in this data-file. As a rule of thumb, a 5MW recip that costs $1,500/kW, runs with 60% utilization, and 40% efficiency, requires a 8-10c/kWh power price (or levelized cost) to generate a 10% IRR, depending on the CO2 price. Capex costs are derived from prior case studies in a backup tab.

Download the Model?

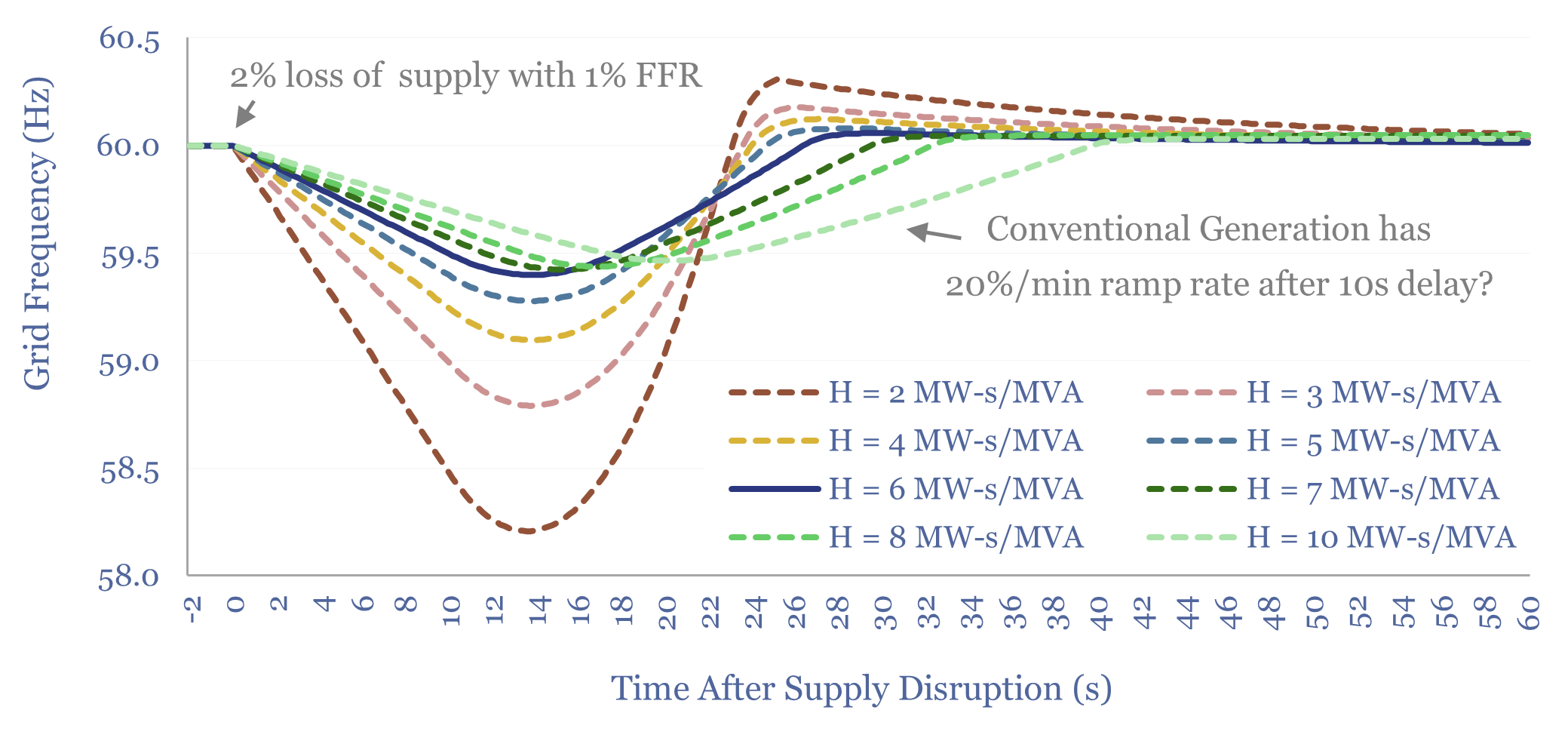

The economics of flywheels can be stress-tested in this data-file, requiring a $500/kW fee for fast-frequency response, to generate a 10% IRR on c$10,000/kWh of capex costs, on a typical flywheel plant with around 15-minutes of energy storage. The rise of renewables and AI increasingly requires adding inertia to power grids. Flywheels may be one solution.

Download the Model?

This economic model captures the production costs of helium, which is cryogenically extracted from low concentrations in natural gas. $200/mcf helium prices can support 10% IRRs on a resource with 2% helium content. $400-1,000/mcf spot prices can unlock 50-100% IRRs and trigger a capex boom. Economics can be stress-tested in this data-file.

Download the Model?

The costs of oil crops, a crucial input for bio-diesel and SAF, will usually range from $900-1,200/ton, in order to generate acceptable 6-15% IRRs for producers. This translates into $3-4/gallon in feedstock costs. These oil crops also likely embed over 2 kg/gallon of CO2 intensity. The economics of oil crops can be stress-tested in this data-file, especially for palm oil, rapeseed oil (aka canola oil) and novel biofuel crops.

Download the Model?

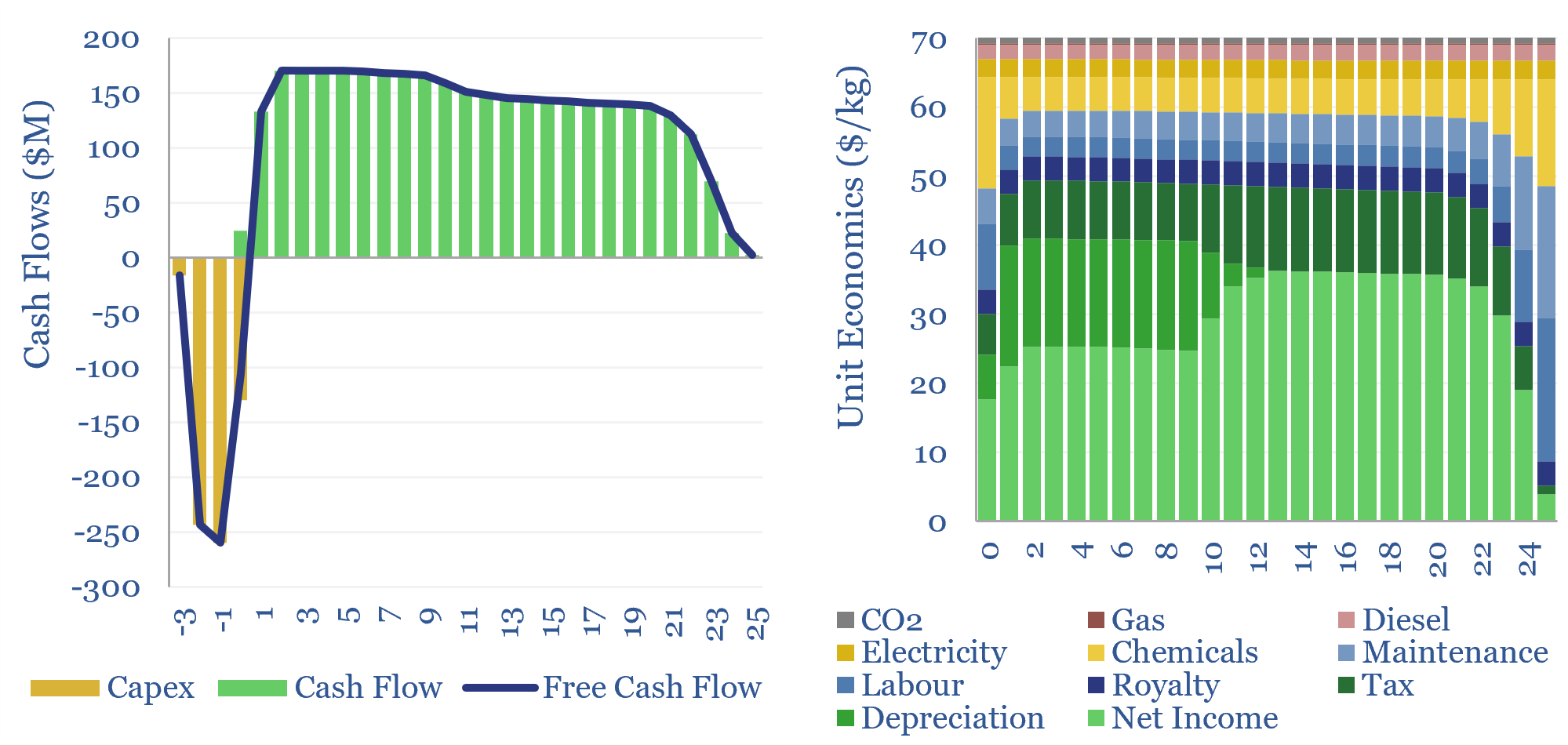

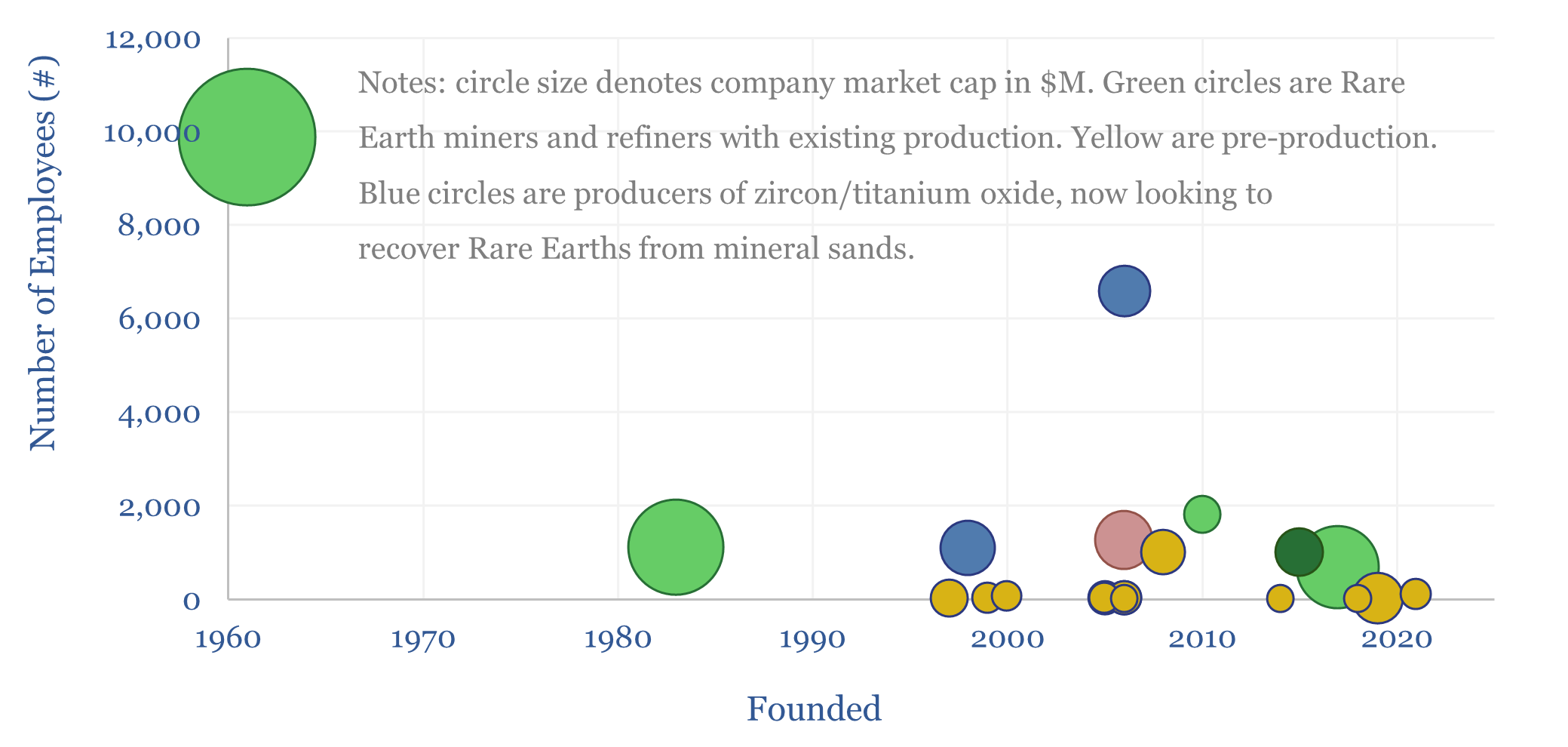

The costs of Rare Earth mining and refining are captured in this model, requiring a $70/kg blended product price, to generate a 20% IRR on $150,000/Tpa of capex. Primary energy intensity exceeds 100 MWH/ton and CO2 intensity exceeds 20 tons/ton. Economics are particularly sensitive to ore grade, recovery rates and chemical costs.

Download the Model?

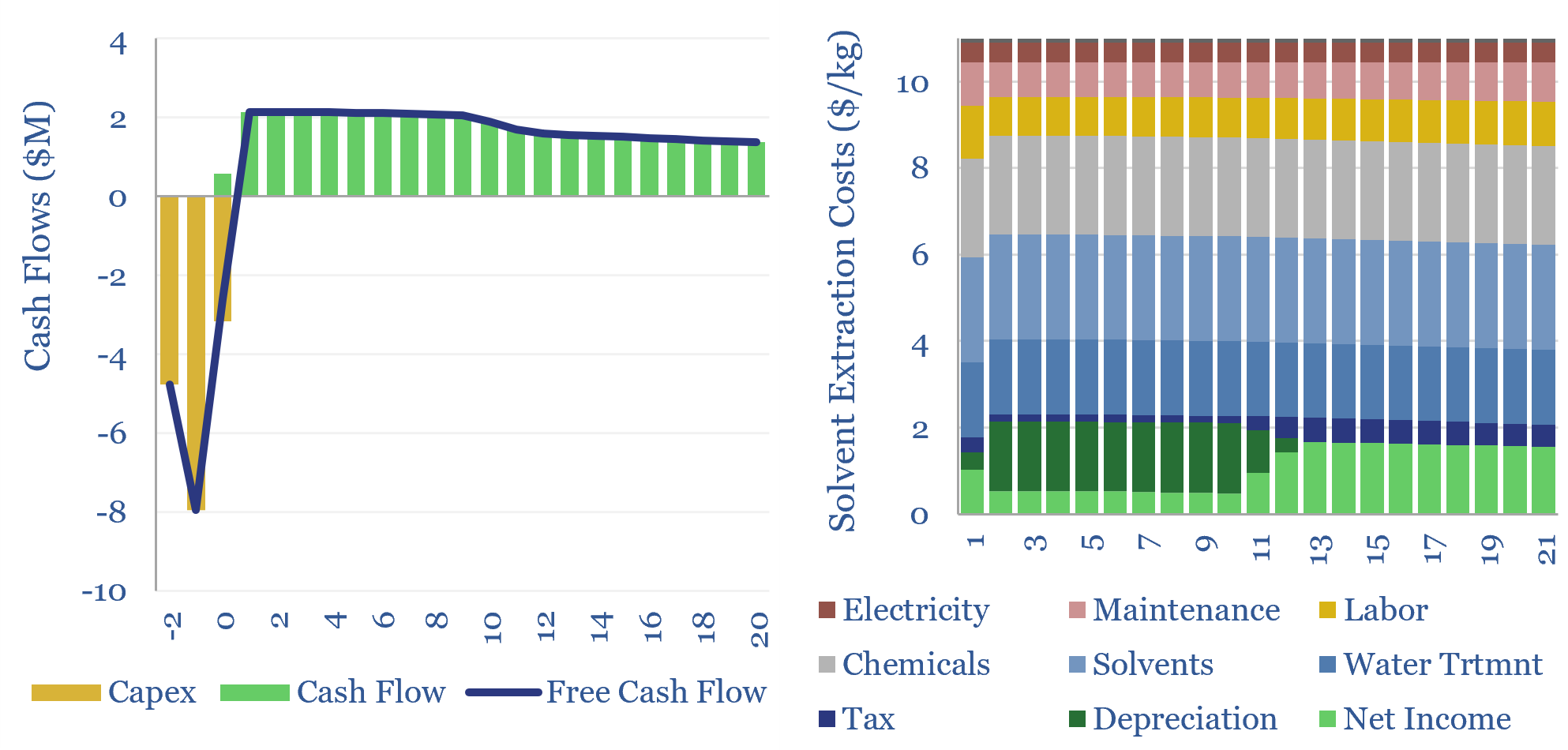

How are Rare Earths separated and concentrated? The process uses solvent extraction in mixer-settlers. It will typically cost over $10/kg, and possibly in the hundreds of dollars per kg. Solvent extraction costs are highly variable and can be stress-tested in this data-file.

Download the Model?

Investment casting is fast and scalable, especially when producing hundreds-thousands of metal parts. $5/kg unlocks a 10% IRR on a 70% utilized metal-casting plant with $2,000/Tpa of capex, producing a typical 10kg aluminium product. This data-file captures the costs of investment-cast products, which can be stress-tested. 115MTpa of metals are cast every year, of which […]

Download the Model?

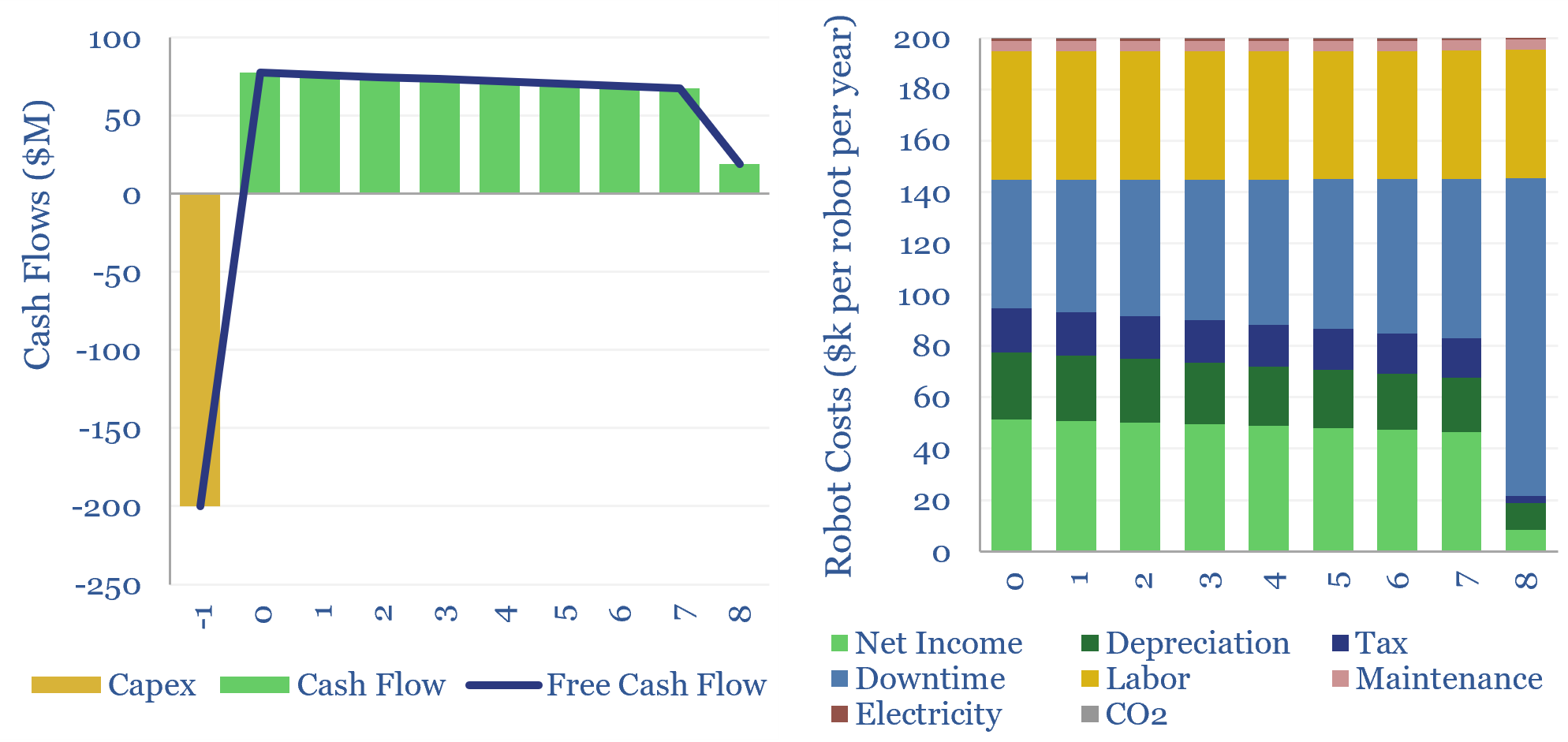

There are 5M industrial robots deployed globally. A typical example costs $130k to install, does incur costs to run, but displaces 1.3 FTE jobs, saves 50% total costs, and thus achieves a payback of 1.5-years and a project-level IRR of 65%. This data-file captures the economics of deploying industrial robots.

Download the Model?

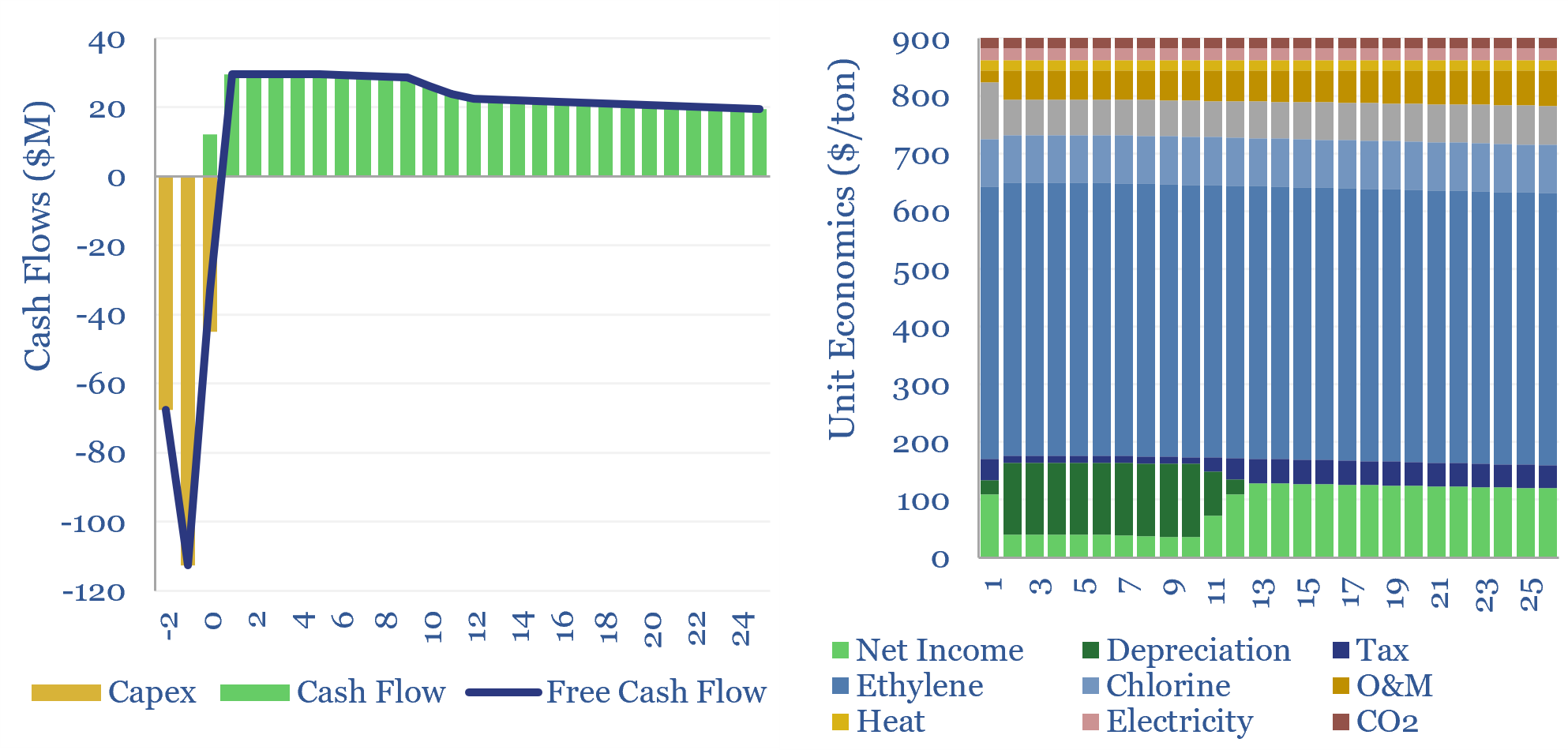

This data-file estimates the cost of PVC production and the cost of VCM production, from first principles, based on capex, input materials, heat, electricity, labor and other opex. As a rule of thumb, 10% IRRs require c$900/ton PVC and c$750/ton VCM, and PVC will embed around 2 tons of CO2 per ton of PVC. Numbers […]

Download the Model?

Conveyors are often the most economical way to move bulk materials over long distances, e.g., from a mine to a processing plant, with an economic cost of $0.1/ton-km, in order to generate a 10% IRR on capex, opex and other costs. These costs are c30% lower than for heavy trucks, opex is at least 60% lower, and CO2 intensity is also about 60% lower. Conveyor costs are calculated in this data-file.

Download the Model?

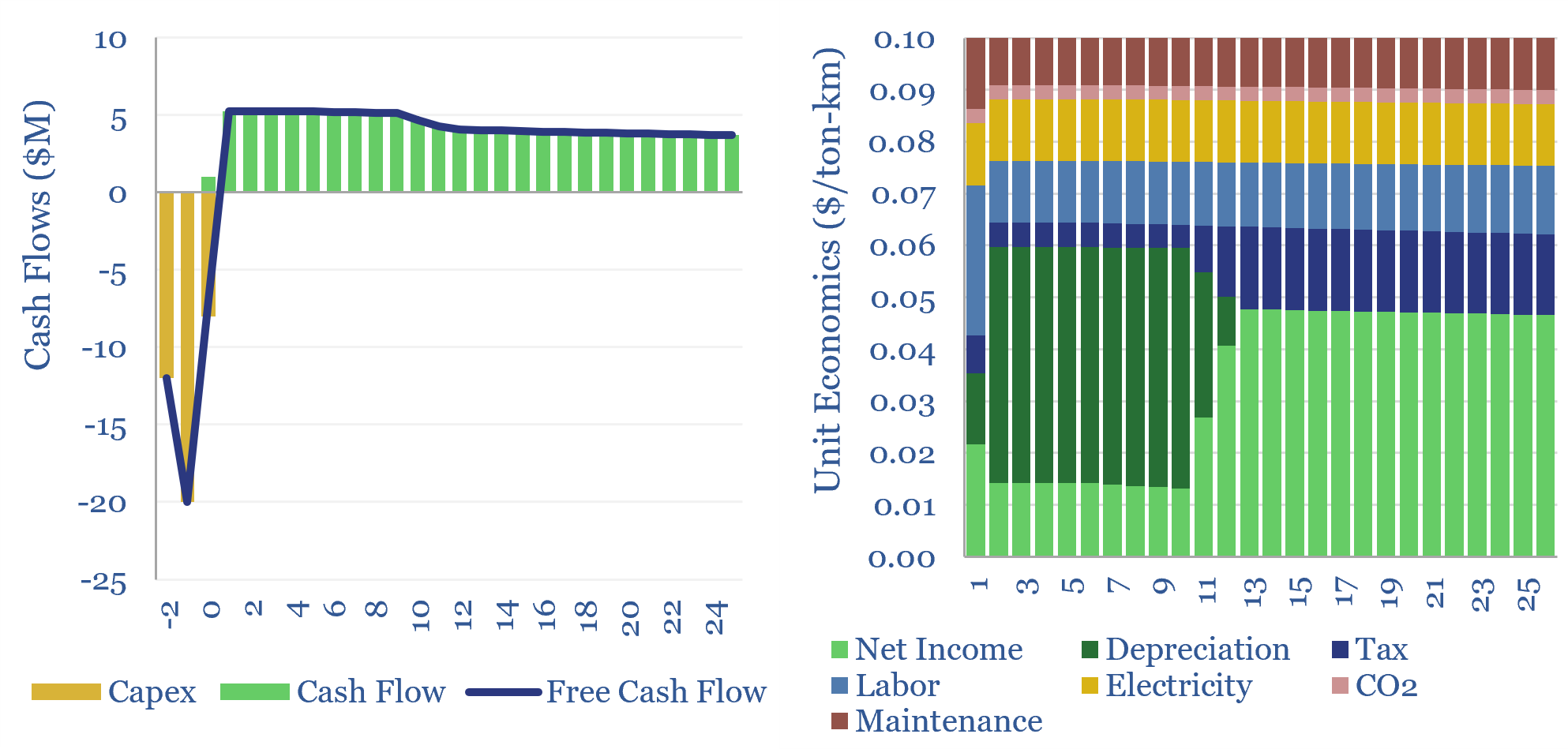

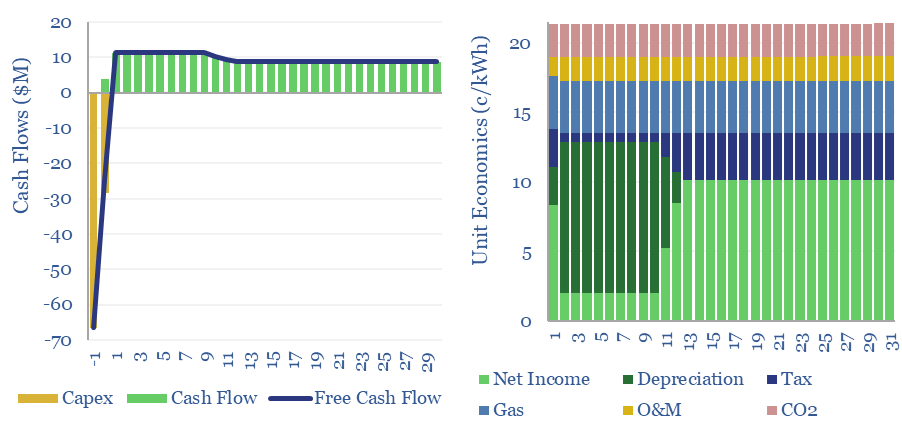

A typical waste-to-energy plant, without subsidies, must charge 16c/kWh to generate a 10% IRR off of c$7,000/kW in capex costs, plus another 14c/kwh-equivalent of revenues from avoided landfilling and metals recovery. This economic model covers waste-to-energy levelized costs of electricity.

Download the Model?

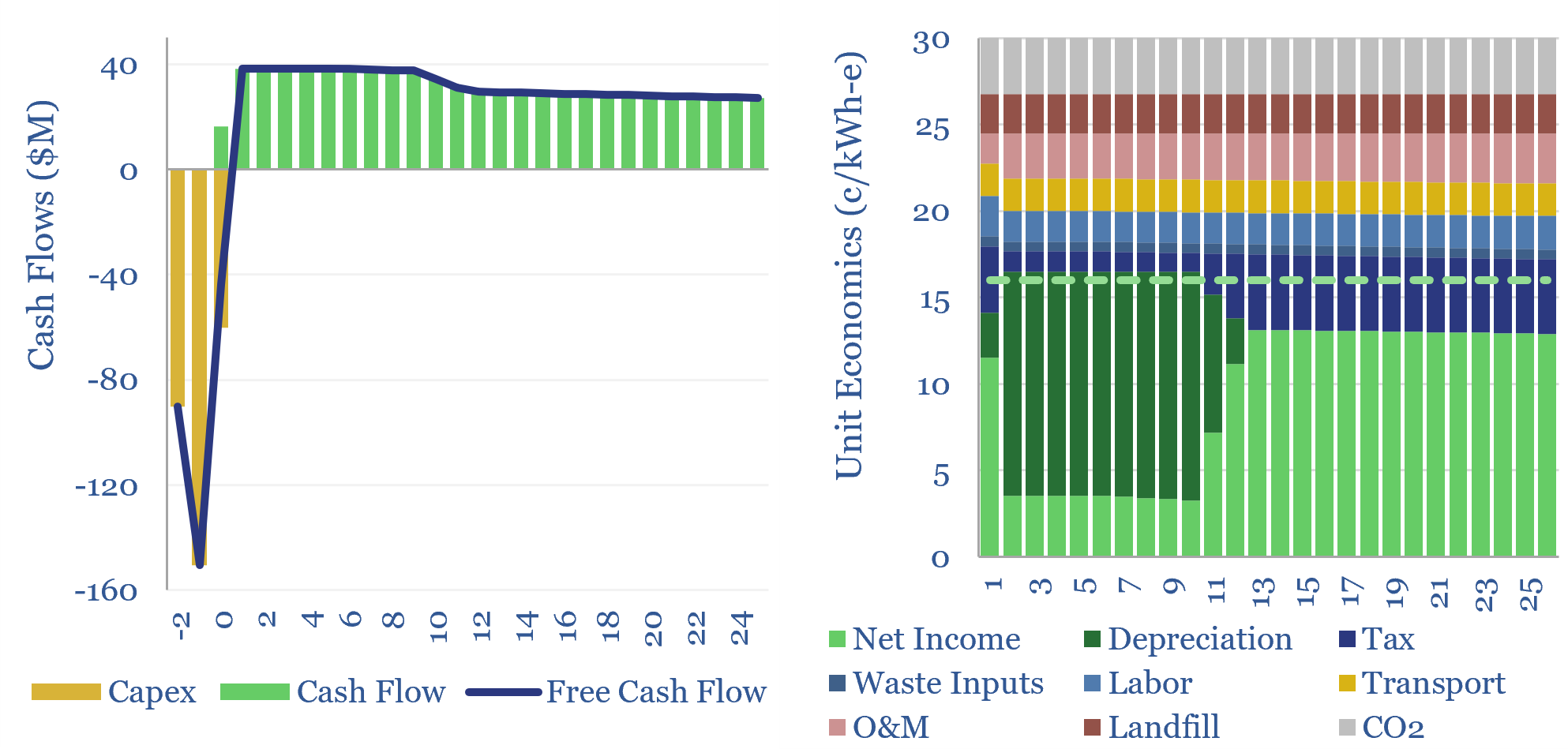

eHighways present an opportunity to electrify heavy trucking, by conveying medium voltage power via overhead steel catenary lines, through a pantograph, to an electric or hybrid-electric truck. This data-file captures the economics of eHighways, covering capex costs, returns and sensitivities, both for road operators and truck operators. The CO2 intensity of trucking can be reduced […]

Download the Model?

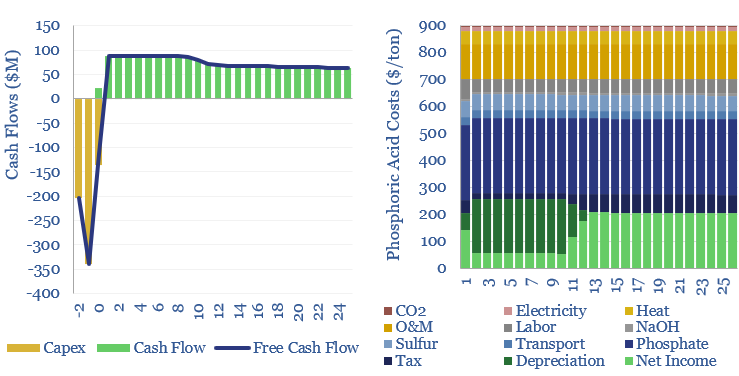

Phosphoric acid production costs are $500-900/ton, for a 10% IRR on a new facility, with $1,000-2,000/Tpa of capex. This is using the ‘wet process’, where phosphate ores are reacted with sulfuric acid. CO2 intensity is 0.6 tons/ton. However, the numbers depend on product purity. There is also a 10x higher carbon, yet potentially lower-cost process, using coke in China. These variations are captured in our model.

Download the Model?

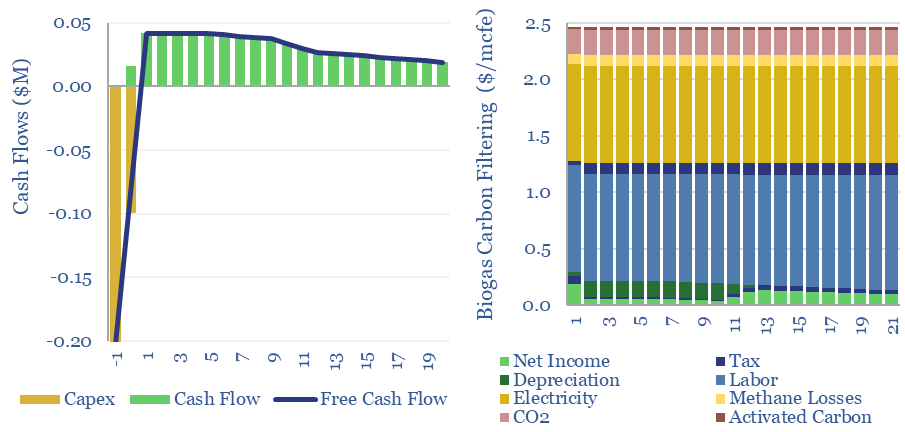

Costs of biogas upgrading into biomethane are estimated at $7/mcf off of capex cost of $400/ton, in this data-file. The largest contributor to total costs is carbon filtering, to remove siloxanes, VOCs and H2S, which we have modelled from first principles, at $2/mcfe. Underlying data into biogas compositions and impurities are also tabulated for reference.

Download the Model?

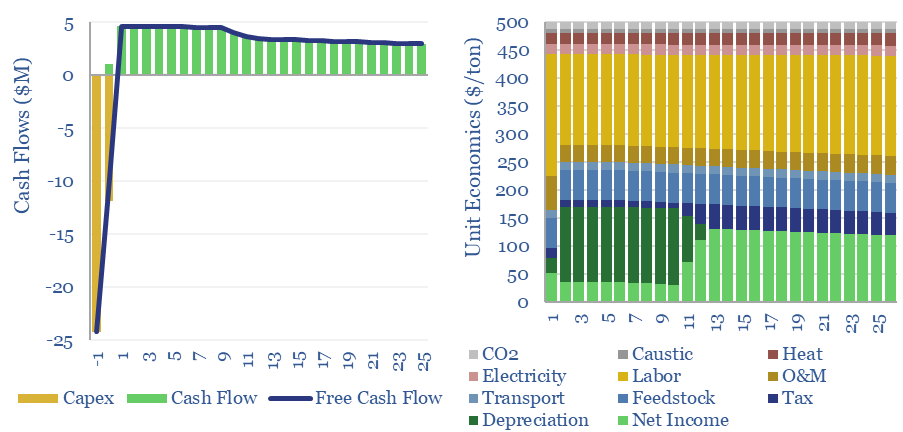

Plastic recycling requires a $500/ton product price, to earn a 10% IRR off of c$1,000/Tpa of up-front capex, at a mechanical recycling facility with 0.3 tons/ton of CO2 intensity (up to 80-90% below virgin plastics, more than we expected). This data-file captures the economics and the costs of plastic recycling, especially for the mechanical recycling of PET.

Download the Model?

Natural hydrogen could be recovered from the Earth’s subsurface, with costs ranging from $0.3-10/kg, and CO2 intensities of 0.2-5.0 kg/kg. This data-file models the economic costs of gold hydrogen, and its sub-variants such as white hydrogen and orange hydrogen.

Download the Model?

Gas peaker plants run at low utilizations of 2-20%, during times of peak demand in power grids. A typical peaker costing $950/kW and running at 10% utilization has a levelized cost of electricity around 20c/kWh, to generate a 10% IRR with 0.5 kg/kWh of CO2 intensity. This data-file shows the economic sensitivities to volatility and utilization.

Download the Model?

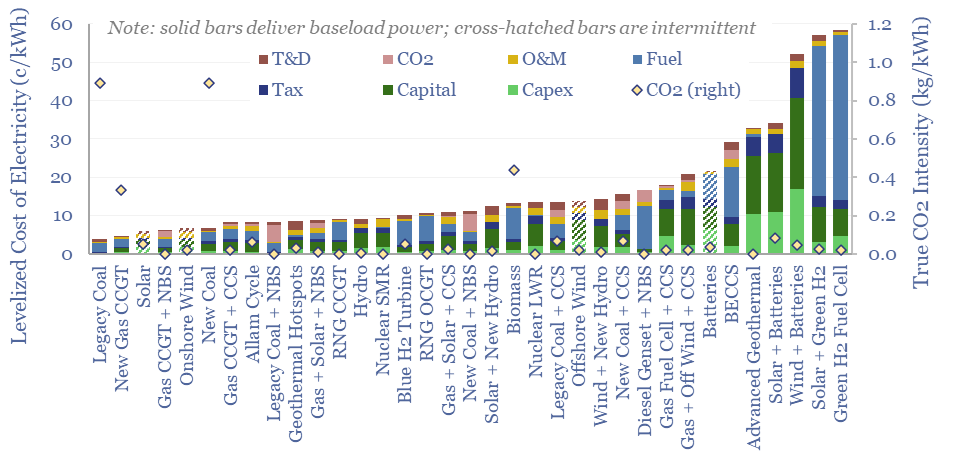

This data-file summarizes the levelized cost of electricity, across 35 different generation sources, covering 20 different data-fields for each source. Costs of generating electricity can vary from 2-200 c/kWh. The is more variability within categories than between them. Numbers can readily be stress-tested in the data-file.

Download the Model?

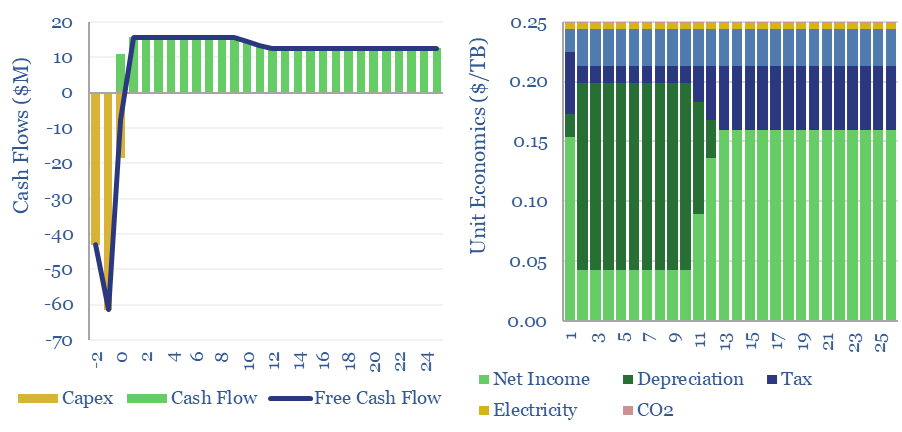

The costs of fiber optic data transmission run at $0.25/TB per 1,000km in order to earn a 10% IRR on constructing a link with $120 per meter capex costs. Capex is 85% of the total cost. This data fiber breaks down the costs of fiber optic data transmission from first principles, across capex, utilization, electricity and maintenance.

Download the Model?

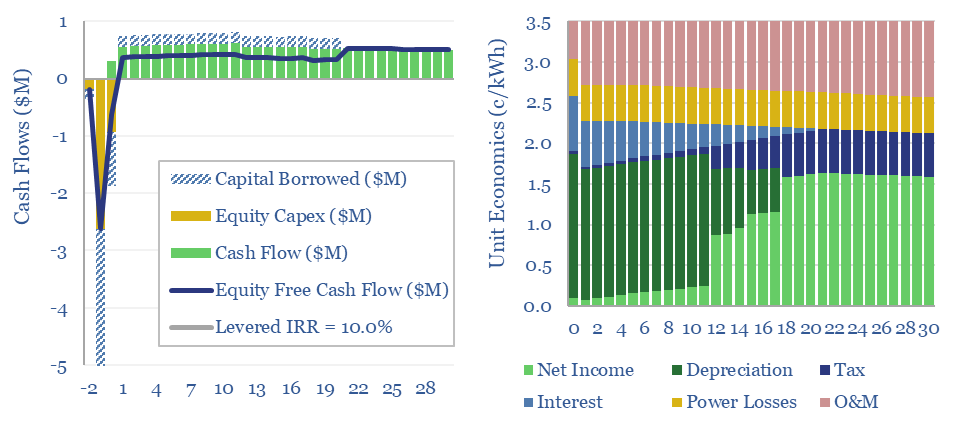

Power distribution costs to residential, commercial and industrial consumers are estimated at 3.5 c/kWh in this model, to generate a 10% levered return, in a 5km x 10MW distribution line, at 17kV, rated up to 400A, with a capex cost of $150/kW-km, a 5% line loss and 40% annualized utilization. All of these inputs can be stress-tested in the data-file.

Download the Model?

This data-file captures the costs of AC power transmission, requiring a 1.5c/kWh spread to earn a 10% levered IRR on a new 100km and 1,000MW transmission line, with capex costs of $1.5/kW-km. These numbers are supported by backup tabs, tabulating the costs of recent projects and a full granular breakdown for the capex costs of transmission lines.

Download the Model?

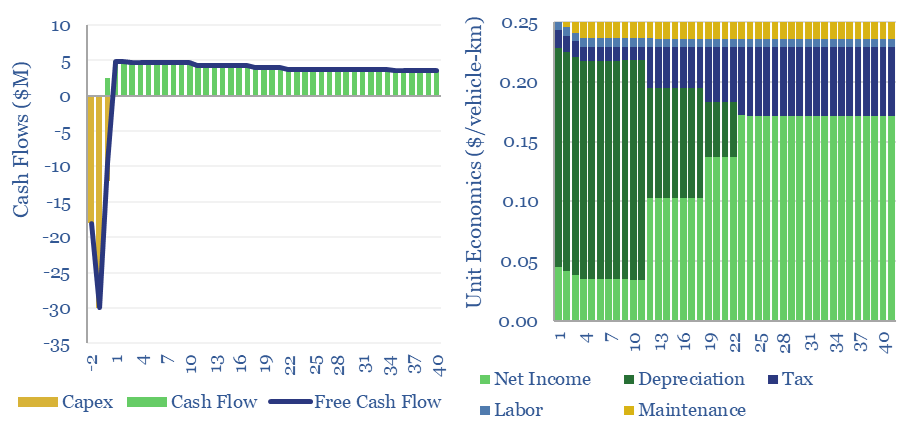

A typical road costs $3M/lane-km to construct, with an effective cost of $0.25 per vehicle-km subsequently travelled. The range varies with utilization and road complexity. Around 10% of the costs are materials, mainly aggregates, while the remainder of the capex is spent on construction and engineering.

Download the Model?

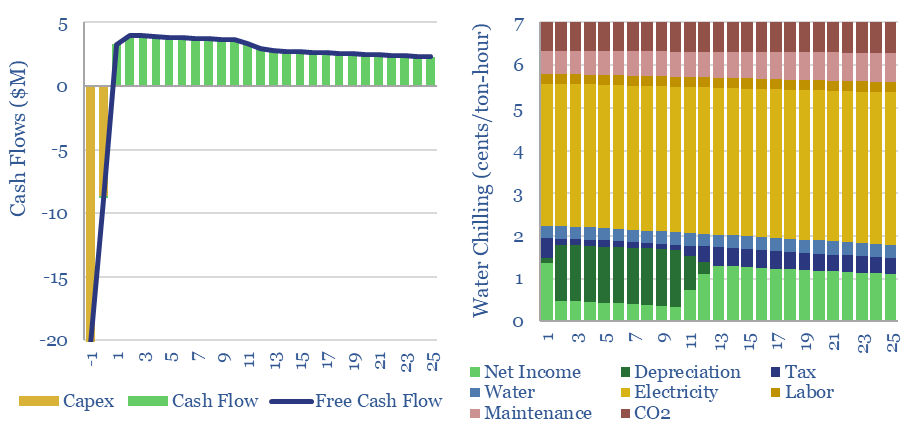

This data-file captures the costs of industrial cooling, especially liquid cooling using commercial HVAC equipment, across heat-exchangers, cooling tower evaporators and chillers. Our base case is that removing 100MW-th of heat has capex costs of $1,000/ton, equivalent to c$300/kW-th, expending 0.12 kWh-e of electricity per kWh-th, with a total cost of 7 c/ton-hour.

Download the Model?

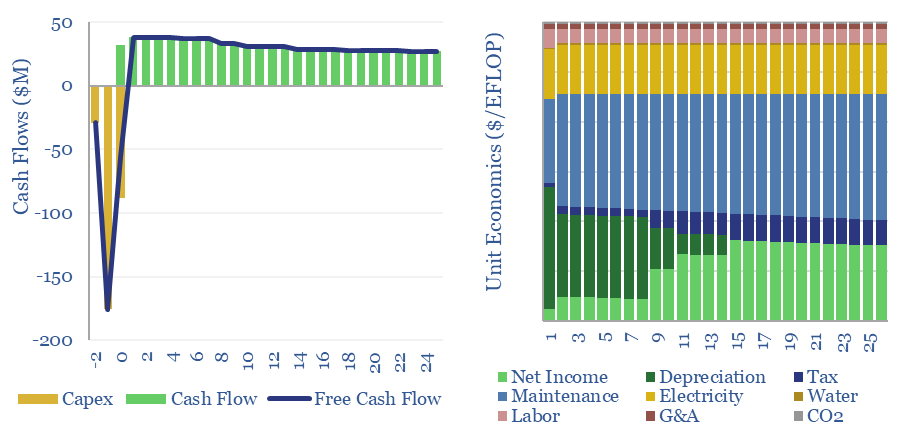

The capex costs of data-centers are typically $10M/MW, with opex costs dominated by maintenance (c40%), electricity (c15-25%), labor, water, G&A and other. A 30MW data-center must generate $100M of revenues for a 10% IRR, while an AI data-center in 2024 may need to charge $5/EFLOP of compute.

Download the Model?

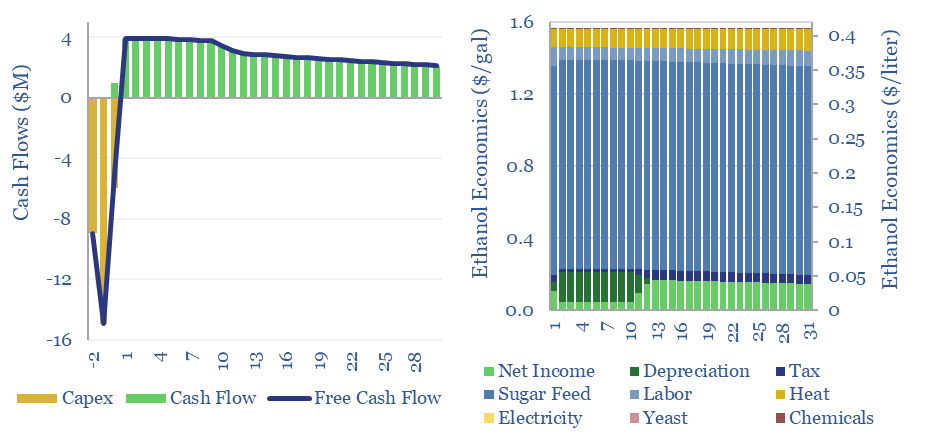

This data-file captures the economics of ethanol production, as a biofuel derived from sugar. A 10% IRR requires $1-4/gallon ethanol, equivalent to $0.25-1/liter, or $60-250/boe. Economics are most sensitive to input sugar prices. Net CO2 intensity is at least 50% lower than hydrocarbons.

Download the Model?

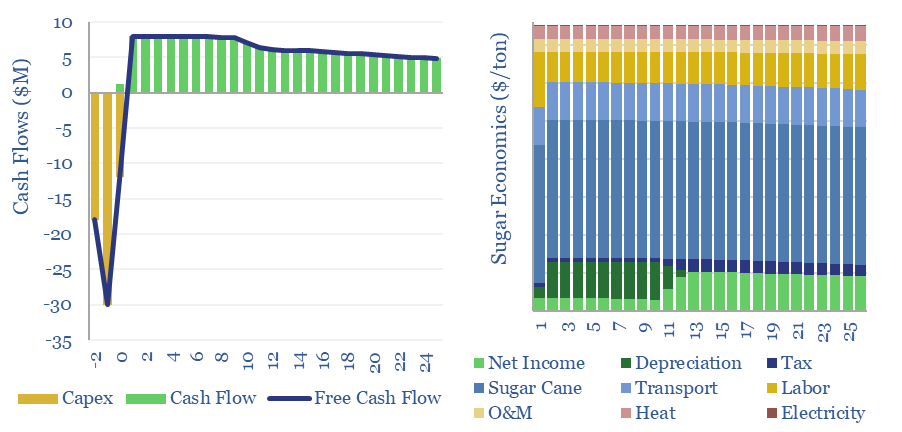

The costs of sugar production are estimated at $260/ton for a 10% IRR at a world-scale sugar refinery, in a major sugar-producing region. Higher returns are achievable at recent world sugar prices, and by valorizing waste streams such as molasses for ethanol and bagasse for cogenerated electricity.

Download the Model?

Woody biomass can be converted into clean hydrogen via gasification. If the resultant CO2 is sequestered, each ton of hydrogen may be associated with -20 tons of CO2 disposal. The economies of hydrogen from biomass gasification require $11/kg-e revenues for a 10% IRR on capex of $3,000/Tpa of biomass, or lower, with CO2 disposal incentives.

Download the Model?

Our base case estimates for Compressed Air Energy Storage costs require a 26c/kWh storage spread to generate a 10% IRR at a $1,350/kW CAES facility, with 63% round-trip efficiency, charging and discharging 365 days per year. Our numbers are based on top-down project data and bottom up calculations, both for CAES capex (in $/kW) and CAES efficiency (in %) and can be stress-tested in the model. What opportunities?

Download the Model?

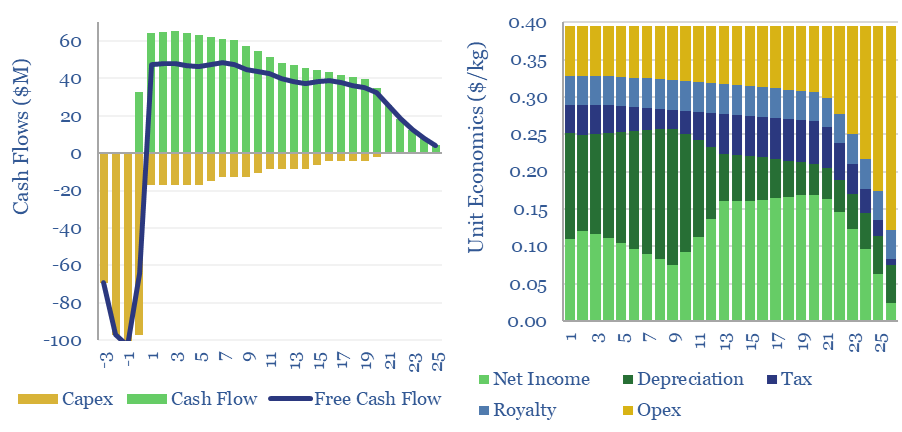

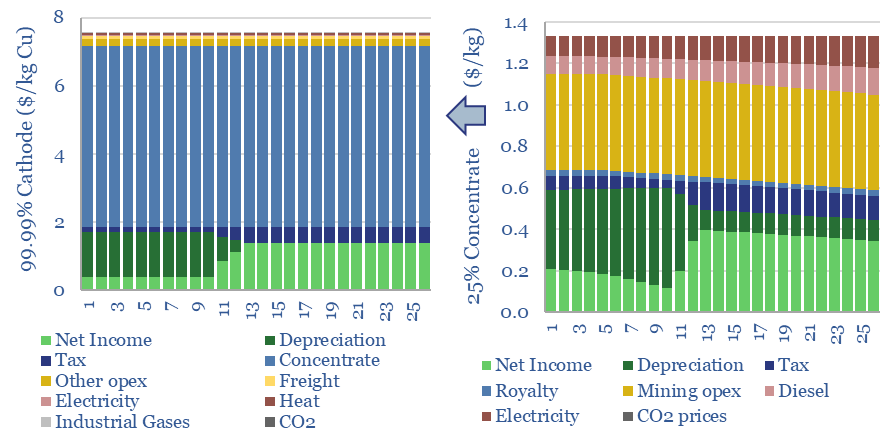

The economic cost of copper production is build up from first princples in this model, from mine, to concentrator, to smelter to 99.99% pure copper cathodes. Our base case is $7.5/kg copper cathode, with 4 tons/ton CO2 intensity, after starting from an 0.57% ore grade. Numbers vary sharply and can be stress-tested in the data-file.

Download the Model?

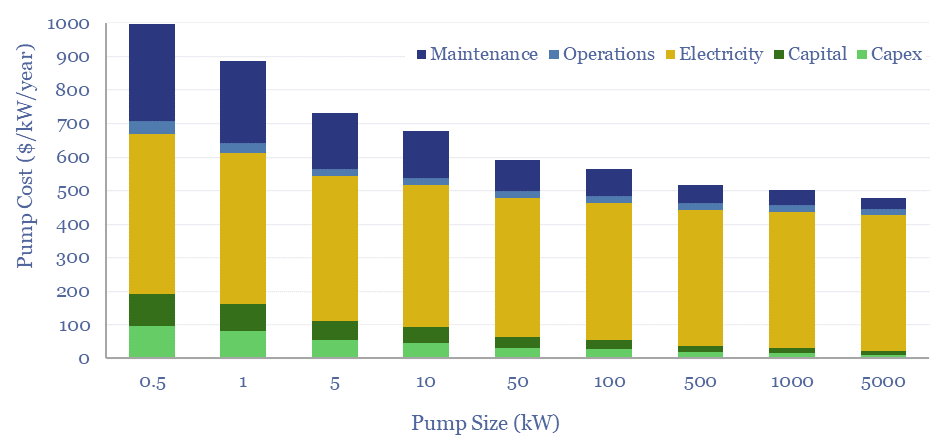

Total pump costs can be ballparked at $600/kW/year of power, of which 70% is electricity, 20% operations and maintenance, 10% capex/capital costs. But the numbers vary. Hence this data-file breaks down the capex costs of pumps, other pump costs, pump energy consumption and the efficiency of pumps from first principles.

Download the Model?

This data-file captures the costs of thermal energy storage, buying renewable electricity, heating up a storage media, then releasing the heat for industrial, commercial or residential use. Our base case requires 13.5 c/kWh-th for a 10% IRR, however 5-10 c/kWh-th heat could be achieved with lower capex costs.

Download the Model?

Hot potassium carbonate is a post-combustion CCS technology that bypasses the degradation issues of amines, and can help to decarbonize power, BECCS and cement plants. We think costs are around $100/ton and energy penalties are 30-50%. Potassium carbonate CCS can be stress-tested in this data-file, across 50 inputs.

Download the Model?

Redox flow battery costs are built up in this data-file, especially for Vanadium redox flow. In our base case, a 6-hour battery that charges and discharges daily needs a storage spread of 20c/kWh to earn a 10% IRR on $3,000/kW of up-front capex. Longer-duration redox flow batteries start to out-compete lithium ion batteries for grid-scale storage.

Download the Model?

Gas dehydration costs might run to $0.02/mcf, with an energy penalty of 0.03%, to remove around 90% of the water from a wellhead gas stream using a TEG absorption unit, and satisfy downstream requirements for 4-7lb/mmcf maximum water content. This data-file captures the economics of gas dehydration, to earn a 10% IRR off $25,000/mmcfd capex.

Download the Model?

Fans and blowers comprise a $7bn pa market, moving low-pressure gases through industrial and commercial facilities. Typical costs might run at $0.025/ton of air flow to earn a return on $200/kW equipment costs and 0.3kWh/ton of energy consumption. 3,000 tons of air flow may be required per ton of CO2 in a direct air capture plant.

Download the Model?

Gas fractionation separates out methane from NGLs such as ethane, propane and butane. A full separation uses up almost 1% of the input gas energy and 4% of the NGL energy. The costs of gas fractionation require a gas processing spread of $0.7/mcf for a 10% IRR off $2/mcf input gas, or in turn, an average NGL sales price of $350/ton. Costs of gas fractionation vary and can be stress tested in this model.

Download the Model?

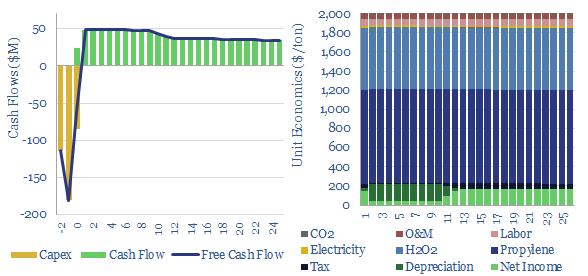

Hydrogen peroxide production costs run at $1,000/Tpa, to generate a 10% IRR at a greenfield production facility, with c$2,000/Tpa capex costs. Today’s market is 5MTpa, worth c$5bn pa. CO2 intensity runs to 3 kg of CO2 per kg of H2O2. But lower-carbon hydrogen could be transformational for clean chemicals?

Download the Model?

This model estimates the levelized cost of offshore wind at 13c/kWh, to generate a 7% IRR off of capex costs of $4,000/kW and a utilization factor of 40-45%. Each $400/kW on capex adds 1c/kWh and each 1% on WACC adds 1.3 c/kWh to offshore wind levelized costs.

Download the Model?

Propylene oxide production costs average $2,000/ton ($2/kg) in order to derive a 10% IRR at a newbuild chemicals plant with $1,500/Tpa in capex. 80% of the costs are propylene and hydrogen peroxide inputs. 60-70% of this $25bn pa market is processed into polyurethanes. CO2 intensity is 2 tons of CO2 per ton of PO today, but there are pathways to absorb CO2 by reaction with PO and possibly even create carbon negative polymers.

Download the Model?

This database contains a record of every company that has ever been mentioned across Thunder Said Energy’s energy technology research, as a useful reference for TSE’s clients. The database summarizes 3,000 mentions of 1,700 energy transition companies, broader energy producing and consuming companies, their size, focus and a summary of our key conclusions, plus links to further research.

Download the Screen?

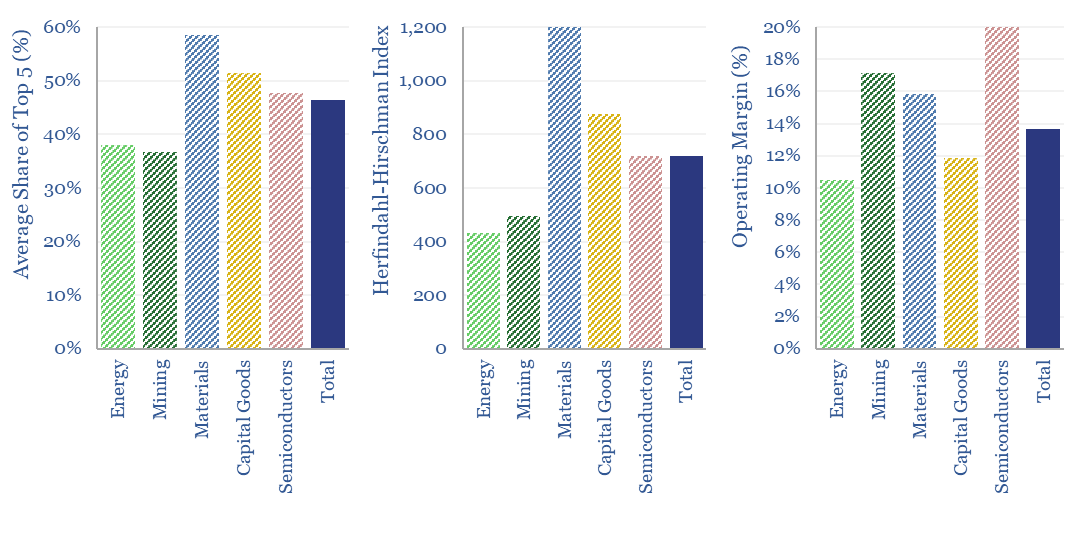

What is the market concentration by industry in energy, mining, materials, semiconductors, capital goods and other sectors that matter in the energy transition? The top five firms tend to control 45% of their respective markets, yielding a ‘Herfindahl Hirschman Index’ (HHI) of 700.

Download the Screen?

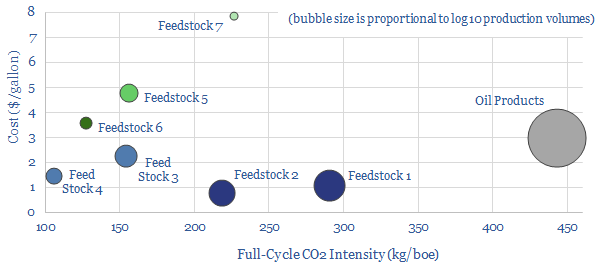

Biofuels are currently displacing 3.5Mboed of oil and gas. But they are not carbon-free, and their weighted average CO2 emissions are only c50% lower. This data-file breaks down the biofuels market across seven key feedstocks, to help identify which opportunities can scale for the lowest costs and CO2, versus others that require further technical progress.

Download the Screen?

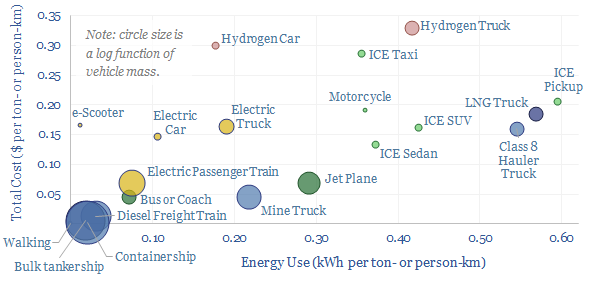

Vehicles transport people and freight around the world, explaining 70% of global oil demand, 30% of global energy use, 20% of global CO2e emissions. This overview summarizes all of our research into vehicles, and key conclusions for the energy transition.

Download the Screen?

Carbon capture and storage (CCS) prevents CO2 from entering the atmosphere. Options include the amine process, blue hydrogen, novel combustion technologies and cutting edge sorbents and membranes. Total CCS costs range from $80-130/ton, while blue value chains seem to be accelerating rapidly in the US. This article summarizes the top conclusions from our carbon capture and storage research.

Download the Screen?

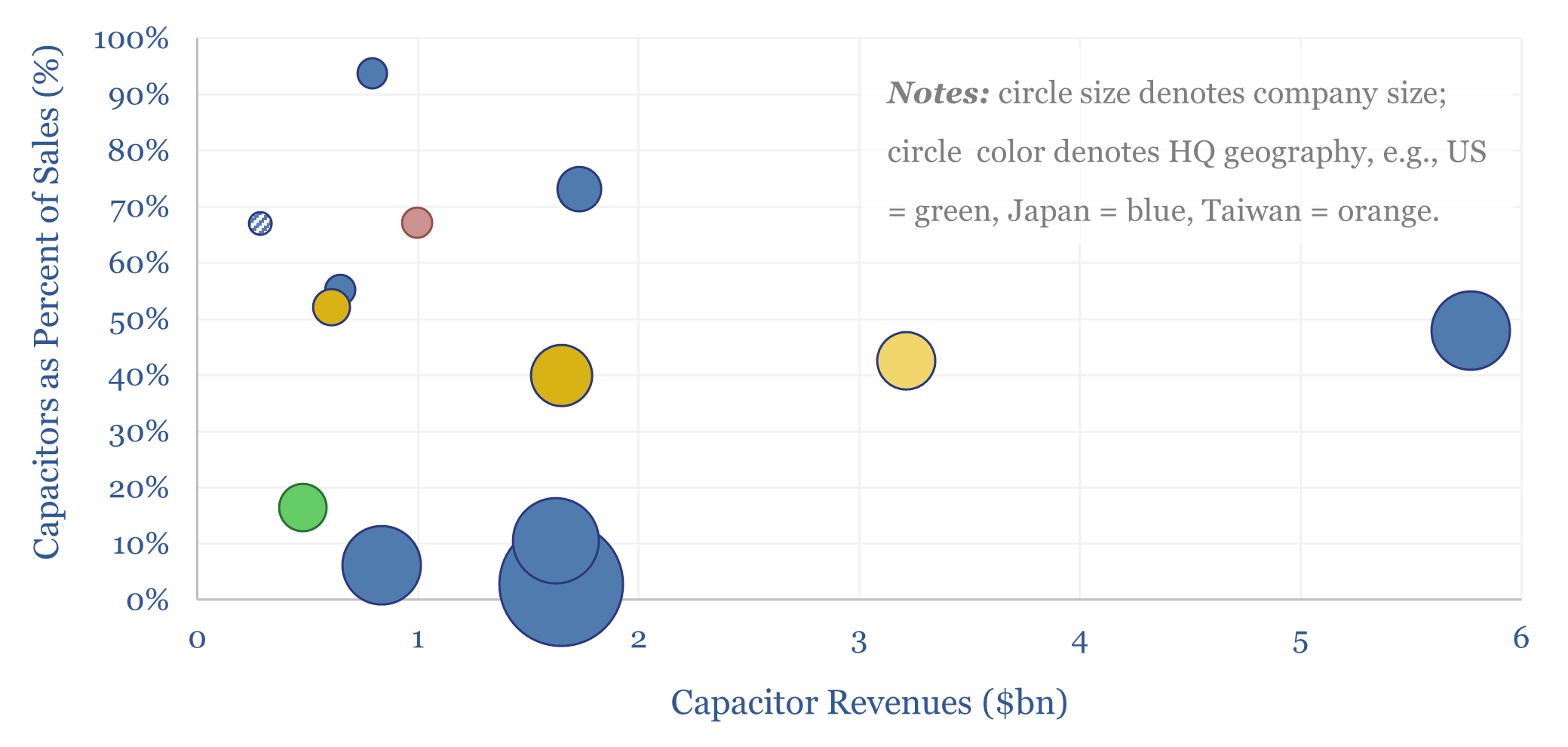

This data-file profiles a dozen leading companies in capacitors, which control two-thirds of the $30bn pa global market. Many companies also produce other passive electronic components, sensors and MOSFETs. Hence will the rise of AI, especially transient-heavy data-centers, pull on demand?

Download the Screen?

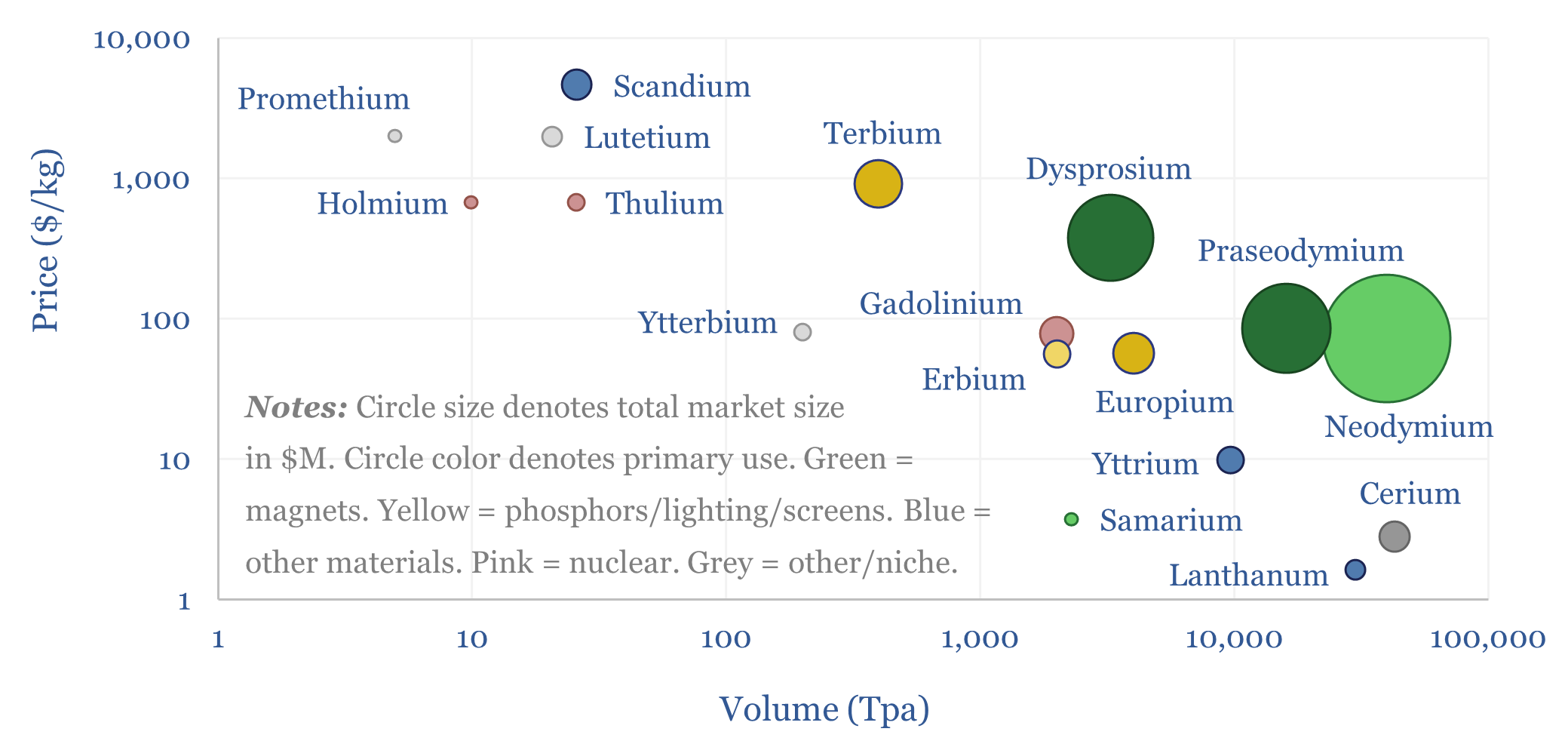

The global Rare Earth market is 390kTpa of mined Rare Earth Oxide equivalents, which is processed to yield 150kTpa of sellable Rare Earth materials, with a value of $7bn pa. But “price” is not “value”. This data-file breaks down the global Rare Earth market, by metal, by price (in $/kg), by volume (in Tpa), and summarizes the key uses of each Rare Earth metal.

Download the Screen?

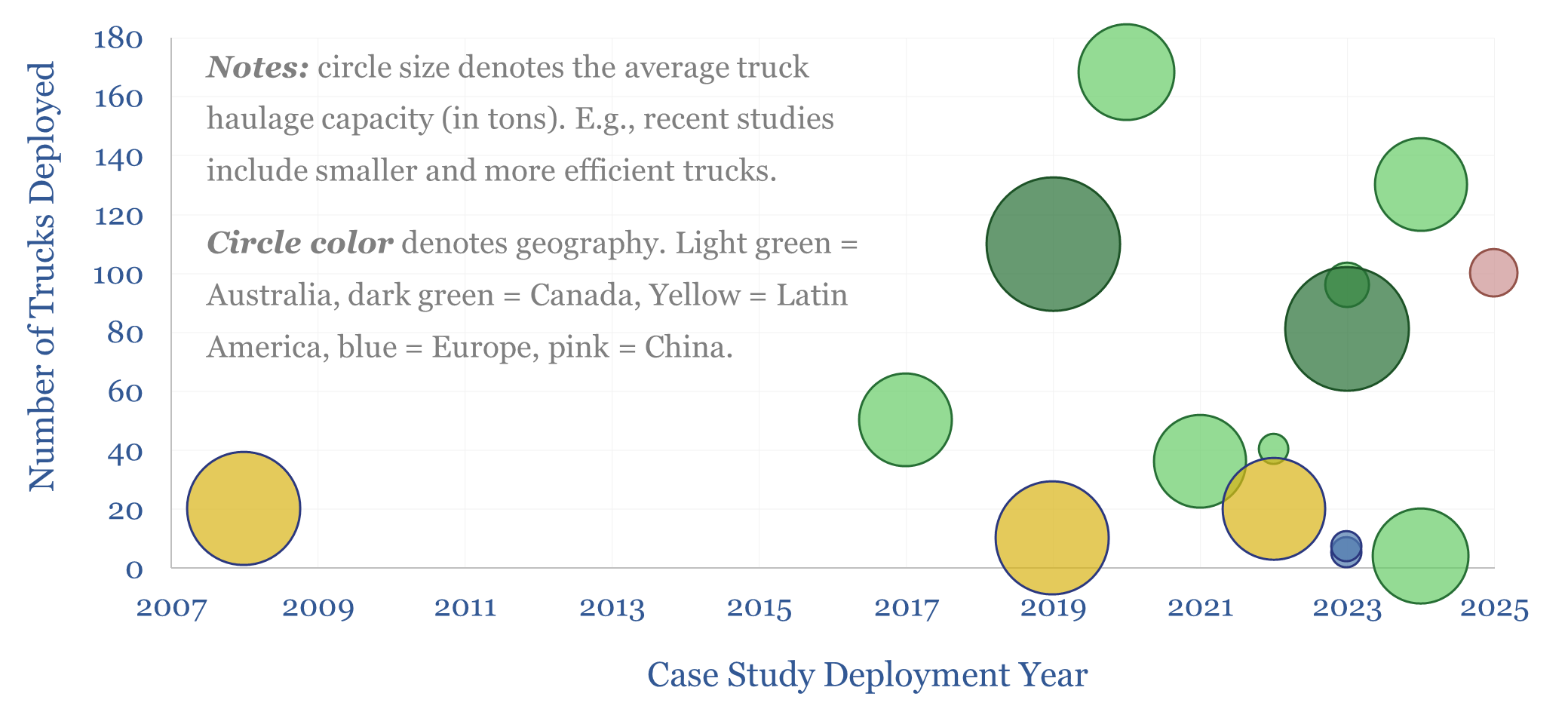

Autonomous mining trucks have been gaining share since 2010, and now number almost 2,000 in total, across dozens of mines globally. So this data-file presents some case studies of autonomous mining trucks, and provides yet another example of digital progress. The work also shows leading companies in autonomous mining trucks, among adopters and mining equipment companies.

Download the Screen?

This screen of Rare Earth miners and refiners captures 20 Rare Earth companies, their flagship projects, and economic parameters such as capex, ore grades, end products and NPVs. A vibrant landscape is evolving, especially for NdPr and DyTb, although the market is still risking pre-produdction projects heavily.

Download the Screen?

Our smart meter data-file cpatures 1.1bn global smart meter installations by region and over time. Smart meters automate the submission of consumption data to the grid, while opening the door to real-time monitoring and load disaggregation, which can reduce total demand by 9% and peak demand by 13%. Opportunities are growing alongside AI. Leading companies are profiled.

Download the Screen?

Additive manufacturing companies are screened in this data-file, across 20 technology leaders. We have also tabulated 25 case studies, where AM reduces weight by 40%, cost by 50%, and lead-time by 60%. The industry remains highly competitive. But could it be turning a corner? Especially for metal components in capital goods and aerospace?

Download the Screen?

This data-file profiles a dozen leading industrial robotics companies. The top five producers account for 60% of the global market, led by companies in Japan and Europe. Although China now comprises half of all industrial robot deployments, and thus Chinese companies are entering the robotics space.

Download the Screen?

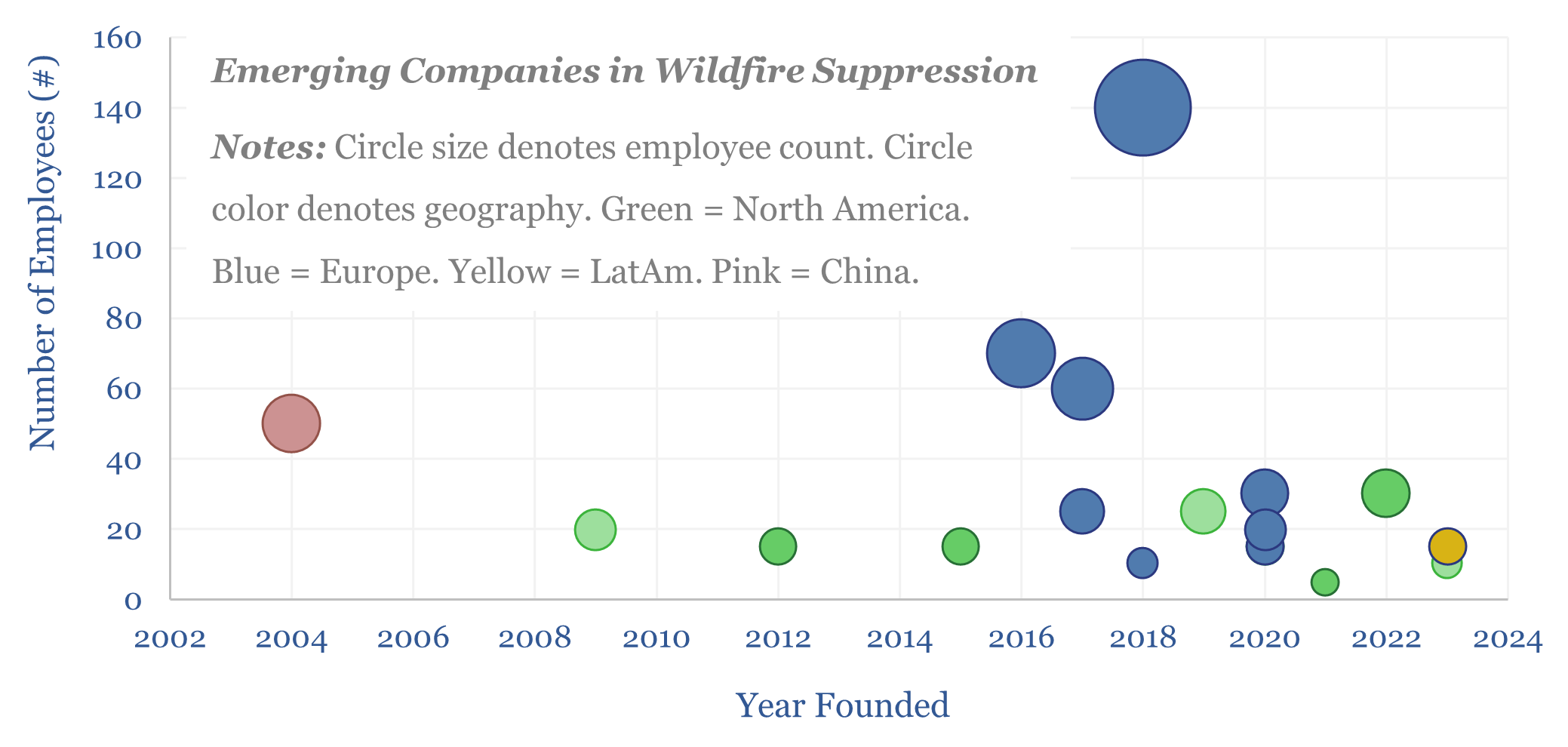

1-2bn acres of land burns globally each year, which could increase by over 35% due to climate change. Hence this data-file screens emerging companies in wildfire suppression, which are focused on preventing, detecting and containing wildfires. The most commonly used methods are drones and AI. Thus adapting to climate change requires more energy not less?

Download the Screen?

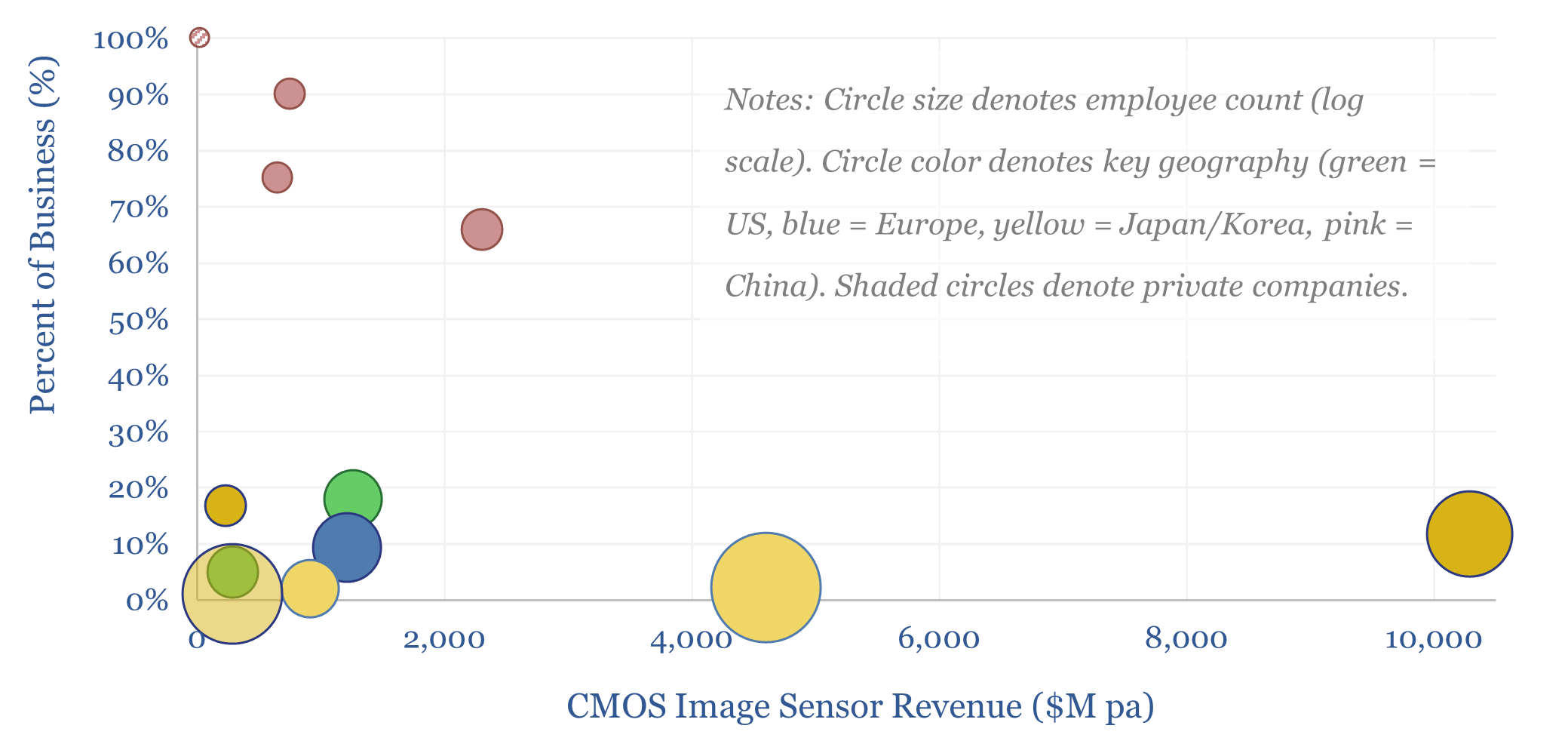

This screen captures a dozen leading companies in CMOS image sensors, which underpin modern digital imagery, from cell-phone cameras to vehicle applications to industrial robots with “machine vision”. It is a concentrated landscape, with incumbents in Japan, Korea, the US and Europe, and fast-growing Chinese competitors. What upside here amidst the rise of AI?

Download the Screen?

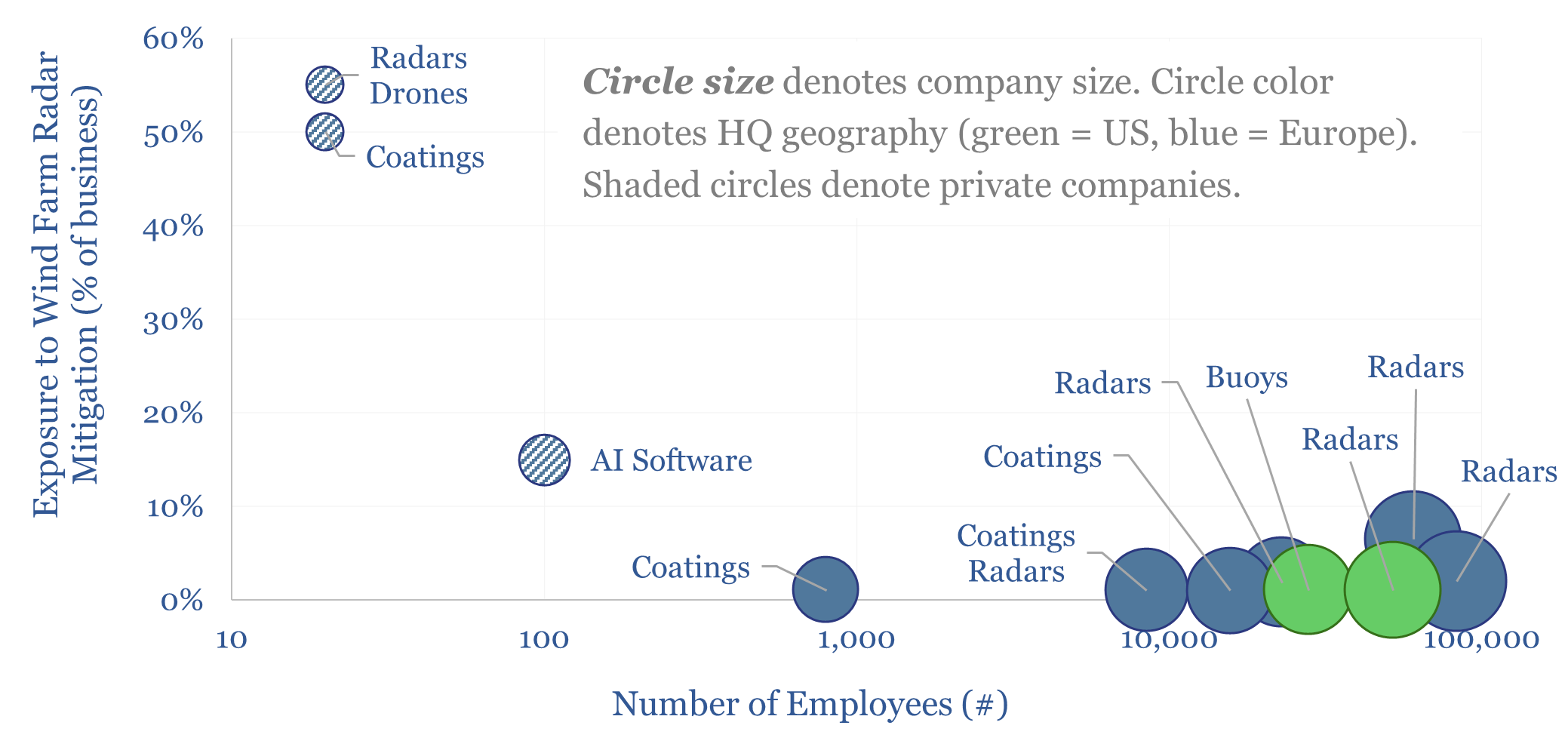

Wind turbines create clutter and blind spots on radar systems, interfering with air traffic control, ocean monitoring and risks to national security and defence. These themes increasingly matter. Hence this data-file screens a dozen companies mitigating the radar interference of wind turbines, from large listed providers of next-gen radar systems, to start-ups developing nano-scale stealth coatings for wind turbine blades.

Download the Screen?

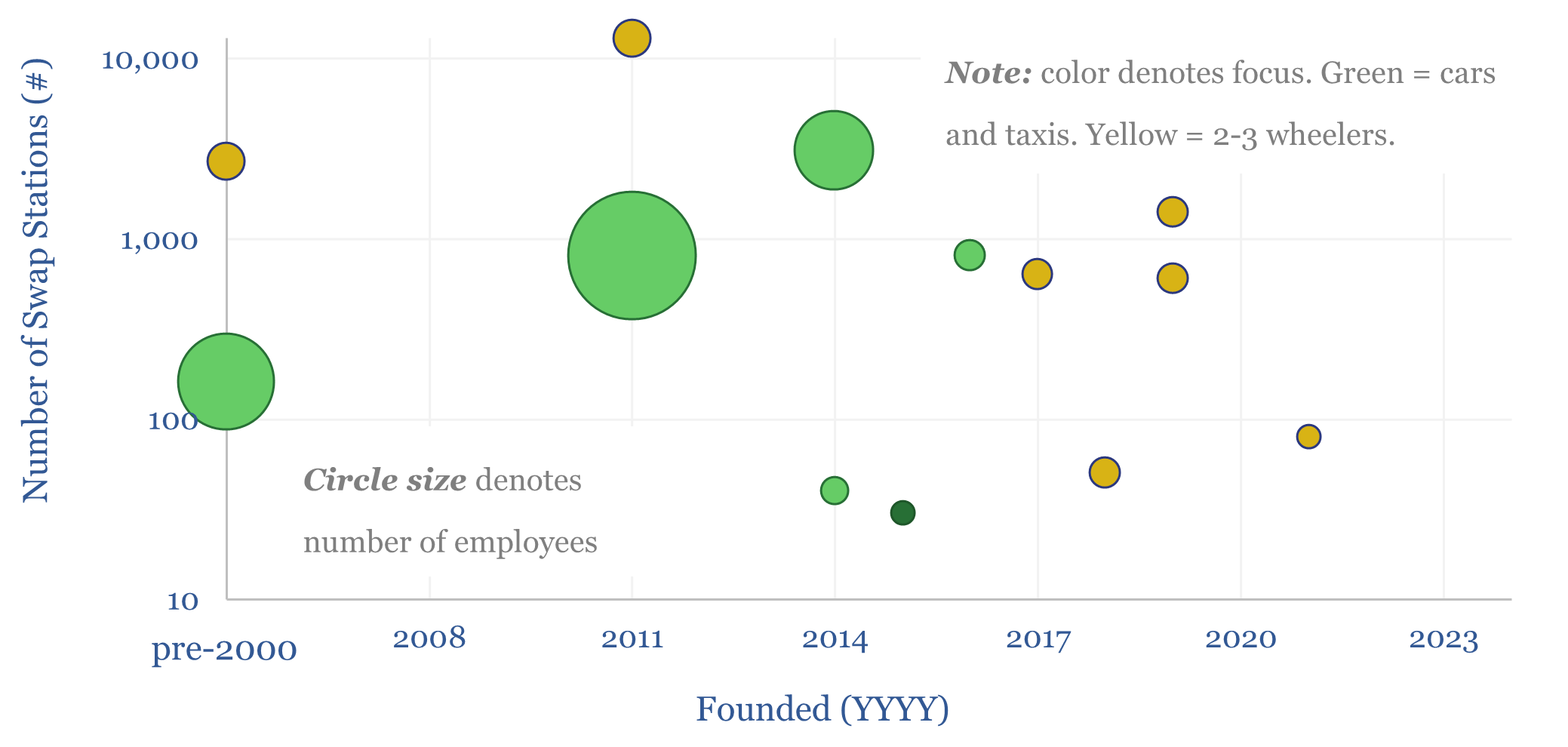

Leading companies in battery swapping are covered in this data-file, with the dozen largest companies operating around 25,000 stations by the end of 2024 (80% for 2-3 wheelers, 20% for cars or larger vehicles). Rapid expansion is guided. CATL says swap stations could meet the needs of one-third of electric vehicles by 2030. This data-file compares the companies and their offerings.

Download the Screen?

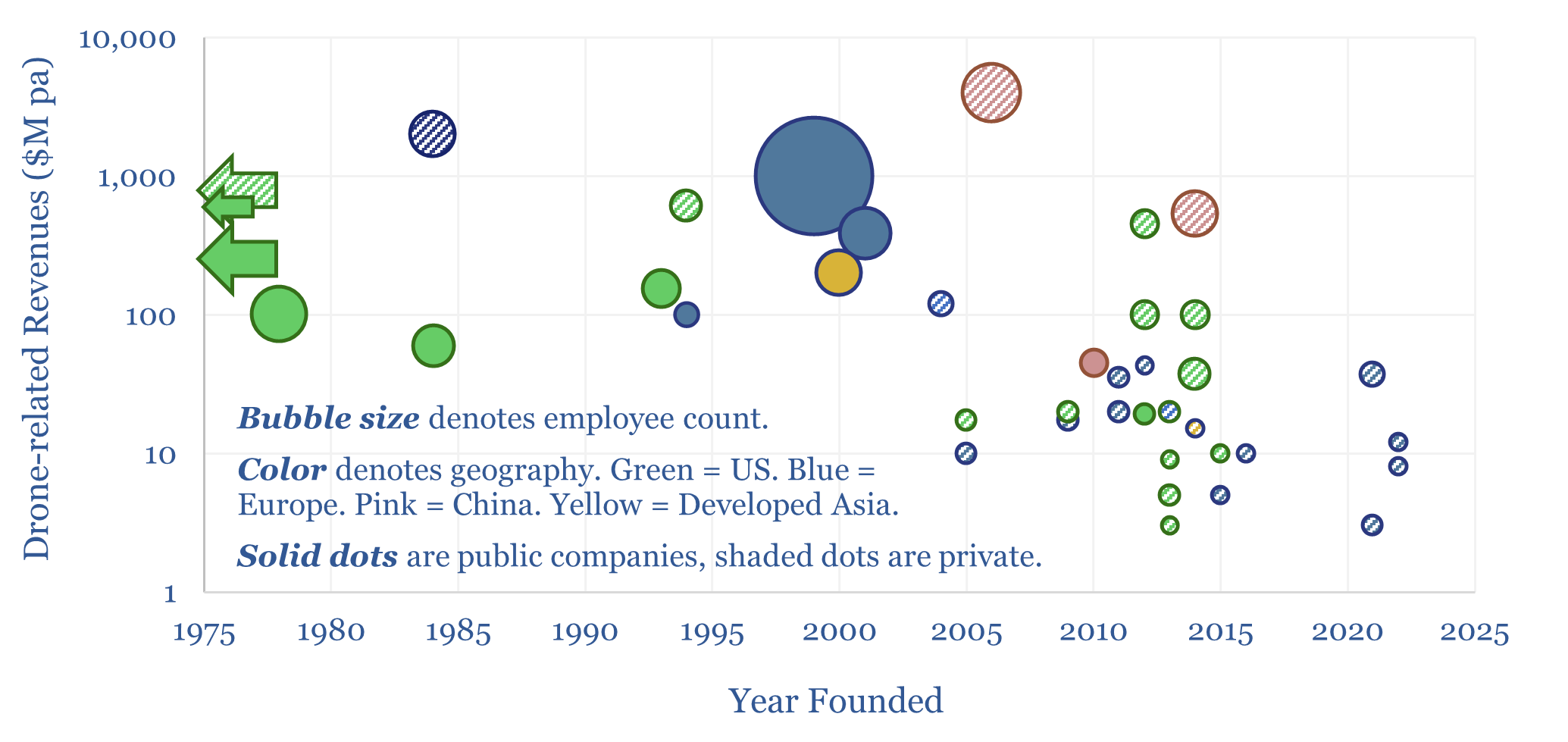

This data-file is a screen of 40 leading drone companies, which either manufacturing drones for consumer, commercial and defense purposes; offer drone inspection services; or offer drone delivery services. It is a vibrant landscape, with over half of the companies founded after 2010, worth c$40bn pa, and creating c$120bn pa of economic benefits.

Download the Screen?

US nuclear generation of 800 TWH pa has come from 94 reactors, at 65 nuclear plants, owned by c50 companies, with 102 GW of current capacity. This data-file breaks down the industry by plant and by owner/operator, and assesses the restart potential of shuttered nuclear plants.

Download the Screen?

This data-file is a screen of 20 perovskite solar companies, which are producing perovskite or perovskite-tandem modules at MW-GW scale, testing perovskite cells at lab scale with a view to future manufacturing, or early- or venture-stage companies that are developing new perovskite solar technologies. Perovskites are a class of materials with the structure ABX3, exceptionally […]

Download the Screen?

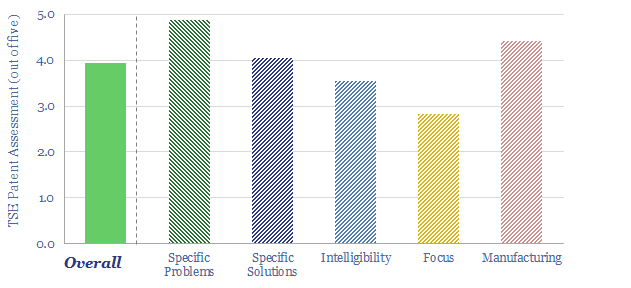

This data-file tabulates industrial companies deploying AI, based on their patent filings. 200 leading industrial companies have filed 40,000 AI/ML-related patents in 2022-24, with 65% now developing their own AIs in house. Examples are summarized. We will continue adding to and expanding this data-file over time.

Download the Screen?

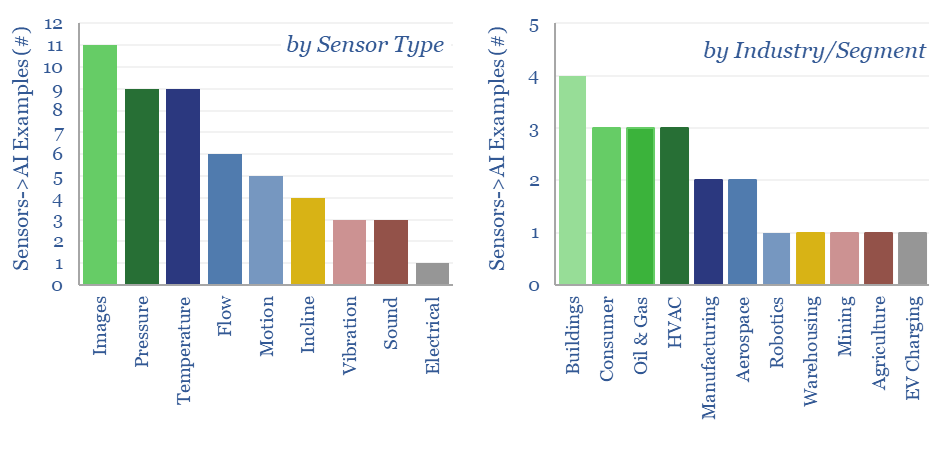

The global sensor market is worth $230bn pa and likely accelerates due to the rise of AI. This data file has compiled 15-20 examples of AI systems integrating sensor data, as patented by industrial companies in 2024, to estimate what types of sensors, will be used in which contexts, and whether AI demand will surprise to the upside?

Download the Screen?

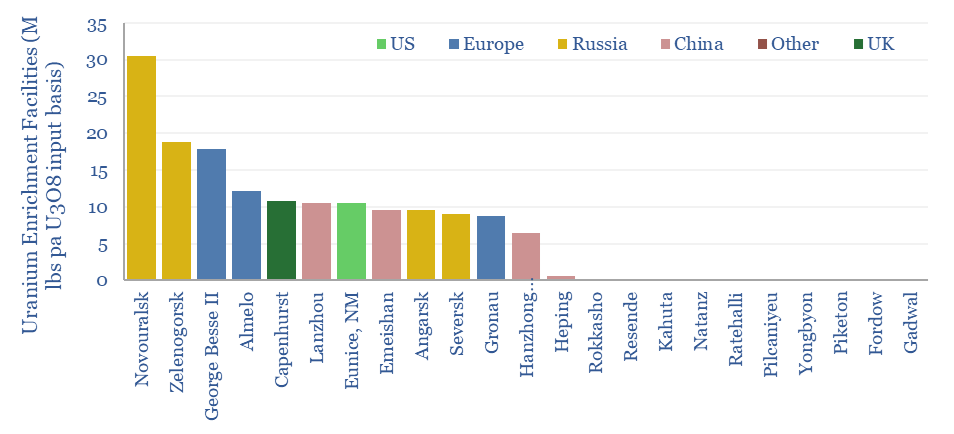

Global uranium enrichment by country, by company and by facility are estimated in this data-file, covering the 155M lbs pa uranium market. The data-file includes a build-up of enrichment facilities (ranked by SWU capacity), notes on each enrichment company and an attempt to map the world’s uranium production to where it is enriched and ultimately consumed.

Download the Screen?

This data-file summarizes the leading companies in solar trackers, their pricing (in $/kW), operating margins (in %), company sizes, sales mixes and recent news flow. Five companies supply 70% of the market, which is worth $10bn pa, and increasingly gaining in importance?

Download the Screen?

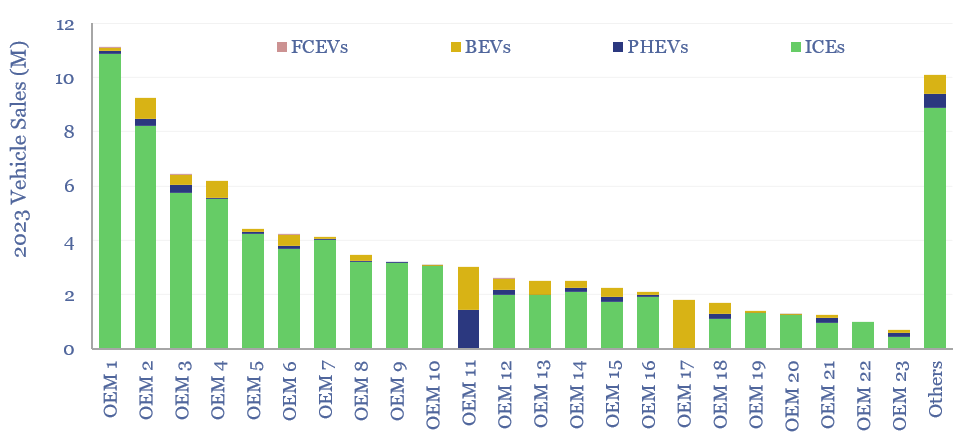

Global vehicle sales by manufacturer are broken down in this screen. 20 companies produce 85% of the world’s vehicles, led by Toyota, VW, Stellantis, GM and Ford. The data-file contains key numbers and notes on each company, including each company’s sales of BEVs, PHEVs, general EV strategy, and how it has been evolving in 2024.

Download the Screen?

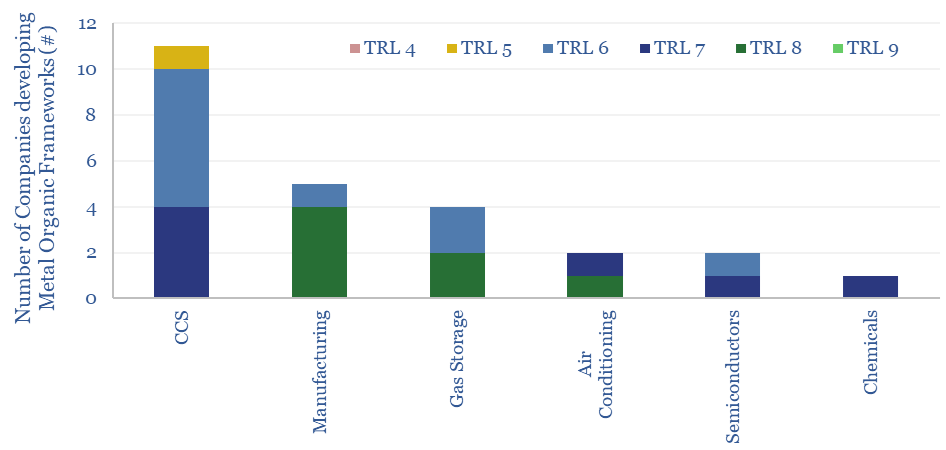

Metal organic frameworks (MOFs) are an exciting class of materials, which could reduce the energy penalties of CO2-separation by c80%, and reduce the cost of carbon capture to $20-40. This data-file screens companies developing metal organic frameworks, where activity has been accelerating rapidly, especially for CCS applications.

Download the Screen?

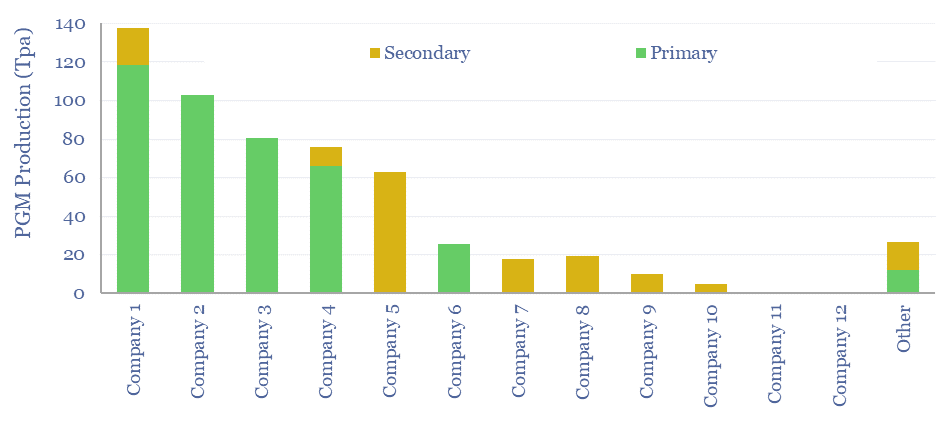

This data-file is a screen of leading PGM producers and recyclers. Eight companies control 90% of global production. Most are mid-caps. Four have primary listings in South Africa. Three are listed in Europe and the UK. Ore grades average 4 grams/ton, and recovery requires 60GWH/ton of energy, emitting 40kT/ton of CO2. But do recent company disclosures suggest that the gloom over PGMs is lifting?

Download the Screen?

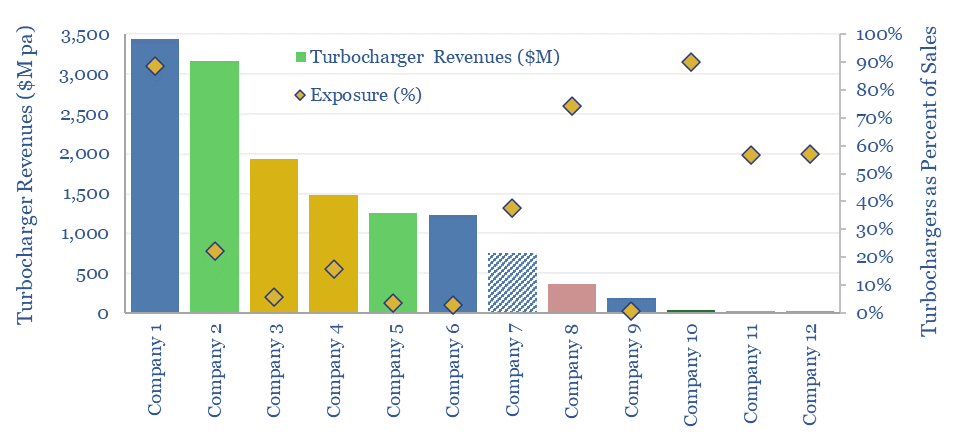

Six leading companies in turbochargers control two-thirds of the $15-20bn pa global turbochargers market. 55% of ICE vehicles now have turbochargers, which can improve fuel economy my as much as 10%, by enabling smaller and better utilized engines to achieve higher peak power ratings. What opportunities ahead, to adapt for vehicle electrification, or even if EV sales accelerate less than expected in 2025-30?

Download the Screen?

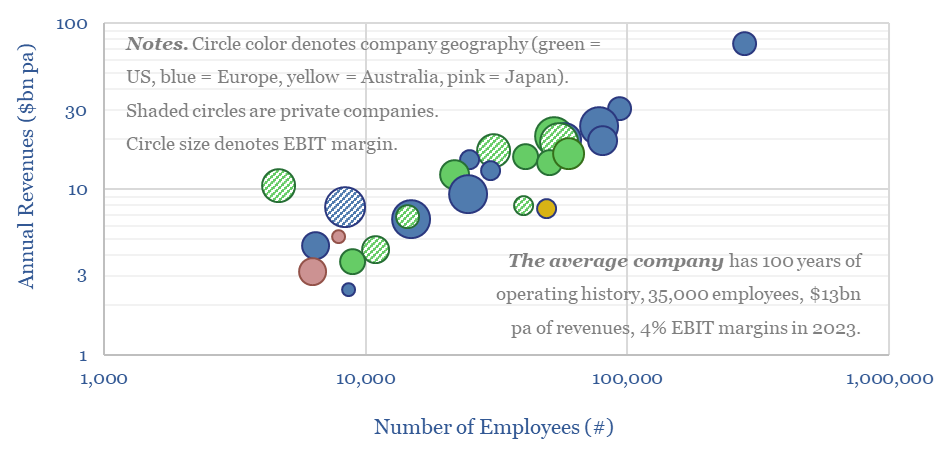

40% of total installed project costs tend to accrue to construction companies, as screened in this data-file. The average of 25 large engineering and construction companies has 100 years of operating history, 35,000 employees, generated $13bn pa of revenues in 2023, and at a c4% EBIT margins.

Download the Screen?

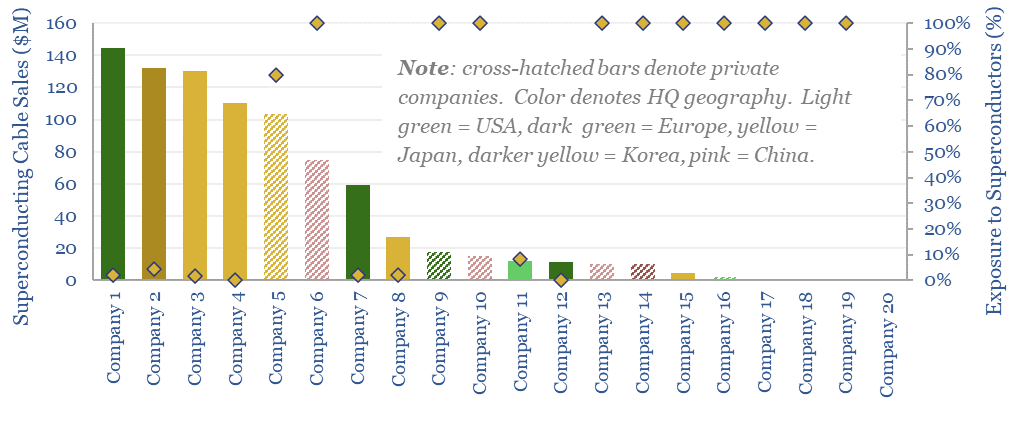

This superconductor screen summarizes all of our work into superconductors, screening past projects, active companies, superconductor materials and the properties of commercial HTS tapes. Five listed companies in Europe, Japan and the US are particularly important for superconducting cable projects to relieve grid bottlenecks?

Download the Screen?

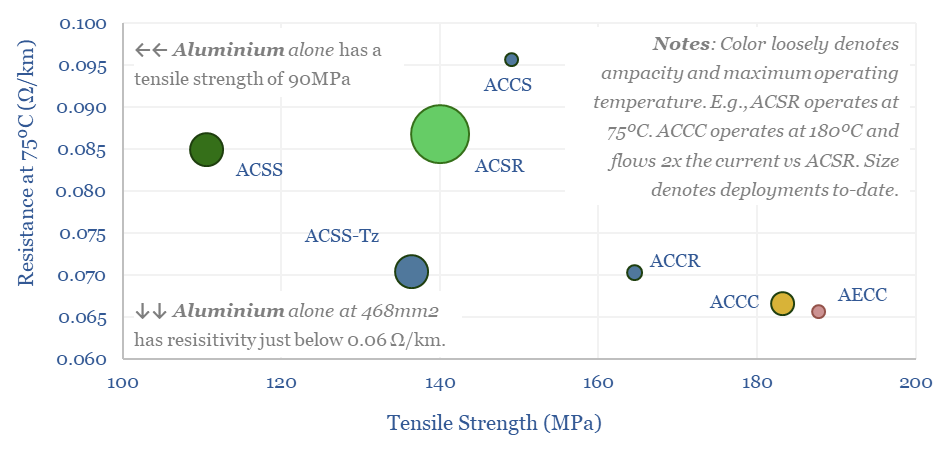

Advanced conductors have 2x higher amperage capacities and temperature limits than standard Aluminium Conductor Steel Reinforced (ACSR) used in AC transmission lines. This data-file screens Advanced conductors versus ACSR on dimensions such as tensile strength, performance and costs, and also screens leading companies.

Download the Screen?

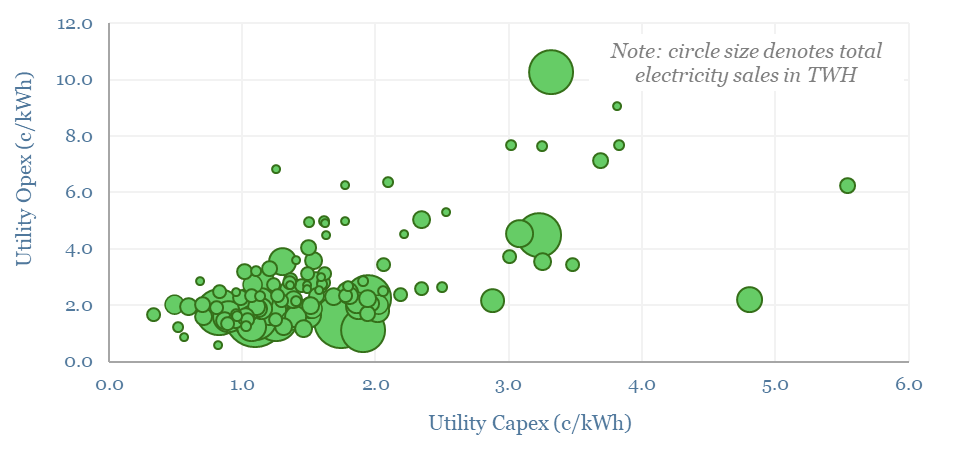

This data-file evaluates transmission and distribution costs, averaging 7c/kWh in 2024, based on granular disclosures for 200 regulated US electric utilities, which sell 65% of the US’s total electricity to 110M residential and commercial customers. Costs have doubled since 2005. Which utilities have rising rate bases and efficiently low opex?

Download the Screen?

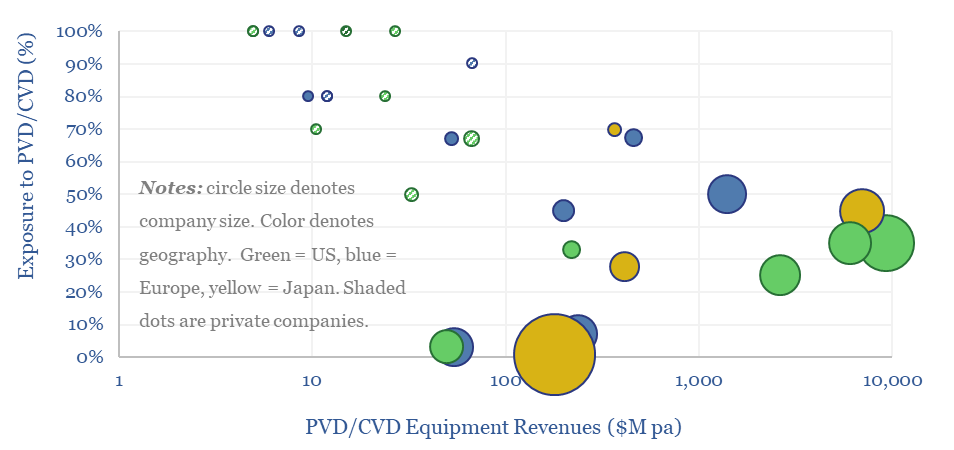

This data-file is a screen of leading companies in vapor deposition, manufacturing the key equipment for making PV silicon, solar, AI chips and LED lighting solutions. The market for vapor deposition equipment is worth $50bn pa and growing at 8% per year. Who stands out?

Download the Screen?

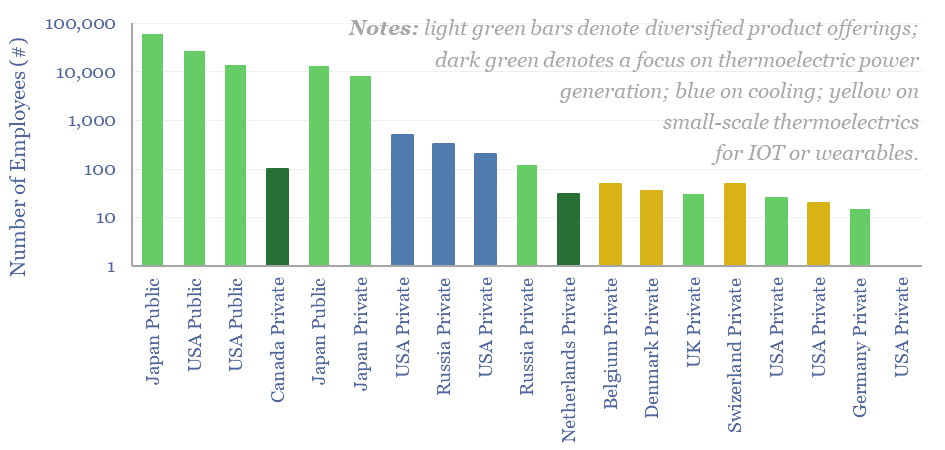

Thermoelectric devices convert heat directly into electricity, or conversely provide localized cooling/heating by absorbing electricity. This data-file screens leading companies in thermoelectrics, their product specifications, applications and underlying calculations for thermoelectric efficiency.

Download the Screen?

50 companies make conductive silver pastes to form the electrical contacts in solar modules. This data-file tabulates the compositions of silver pastes based on patents, averaging 85% silver, 4% glass frit and 11% organic chemicals. Ten companies stood out, including a Korean small-cap specialist.

Download the Screen?

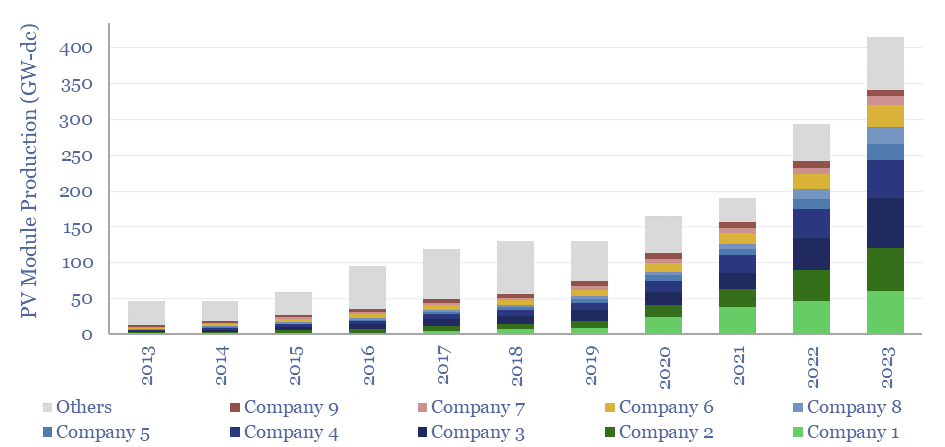

The world produced over 400GW of solar modules in 2023, which is up 10x from a decade ago. This data-file breaks down solar module production by company and over time, comparing the companies by solar module selling prices ($/kW), margins (%), efficiency (%), transparency, and technology development.

Download the Screen?

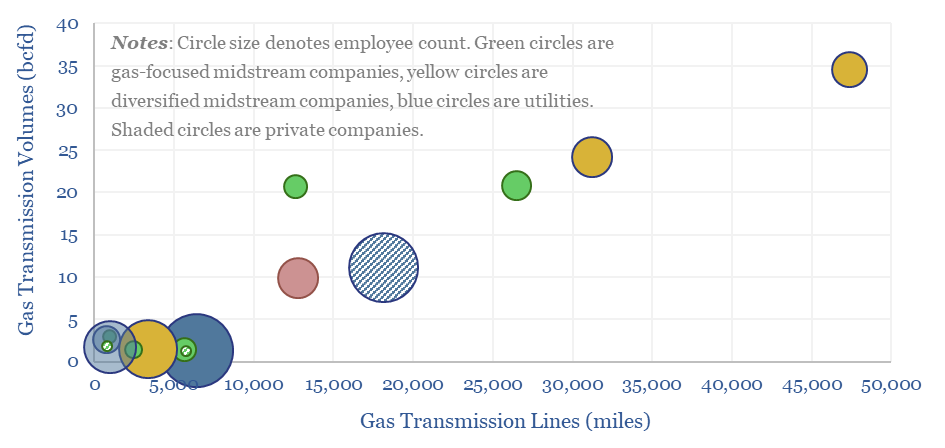

This data-file aggregates granular data into US gas transmission, by company and by pipeline, for 40 major US gas pipelines which transport 45TCF of gas per annum across 185,000 miles; and for 3,200 compressors at 640 related compressor stations.

Download the Screen?

This data-file tracks some of the leading solar inverter companies and inverter costs, efficiency and power electronic properties. As China now supplies 85% of all global inverters, at 30-50% lower $/W pricing than Western companies, a key question explored in the data-file is around price versus quality.

Download the Screen?

This data-file screens 20 leading companies in harmonic filters, tabulating their size, geography, ownership details, patent filings and a description of their offering. Active harmonic filters reduce total harmonic distortion below 5%, with 97% efficiency, within 5 ms. Half a dozen companies stood out in our screen, including one large, listed Western capital goods company.

Download the Screen?

This data-file is a screen of thermal energy storage companies, developing systems that can absorb excess renewable electricity, heat up a storage medium, and then re-release the heat later, for example as high-grade steam or electricity. The space is fast-evolving and competitive, with 17 leading companies progressing different solutions.

Download the Screen?

Polysilicon is a highly pure, crystalline silicon material, used predominantly for photovoltaic solar, and also for ‘chips’ in the electronics industry. Global polysilicon capacity reached 3MTpa in 2024, and global polysilicon production surpassed 1.7MTpa in 2024. China now dominates the industry, approaching 94% of all global capacity.

Download the Screen?

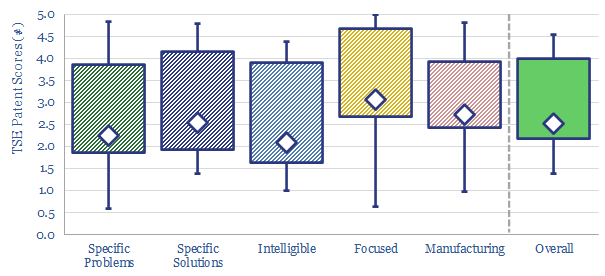

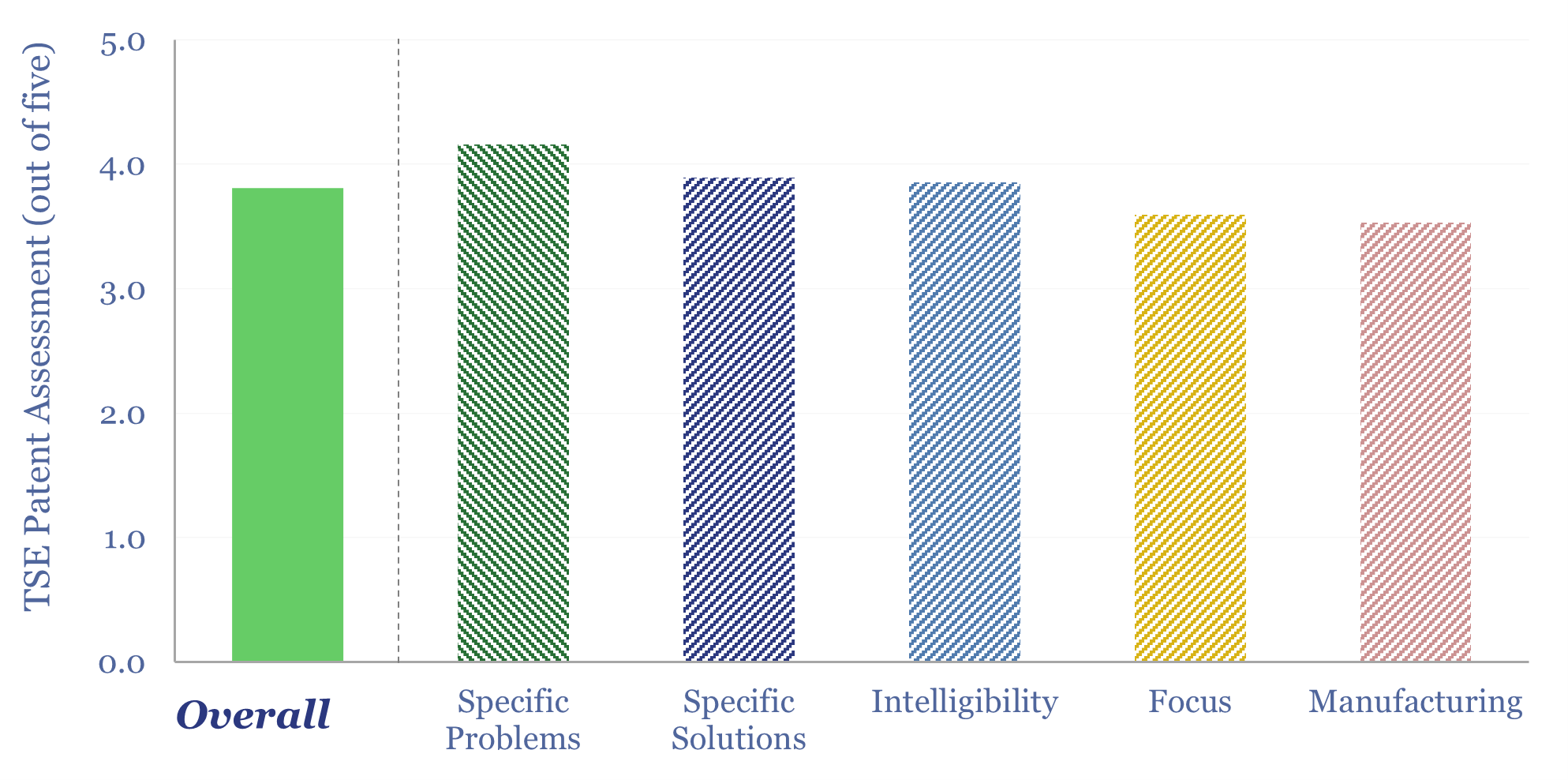

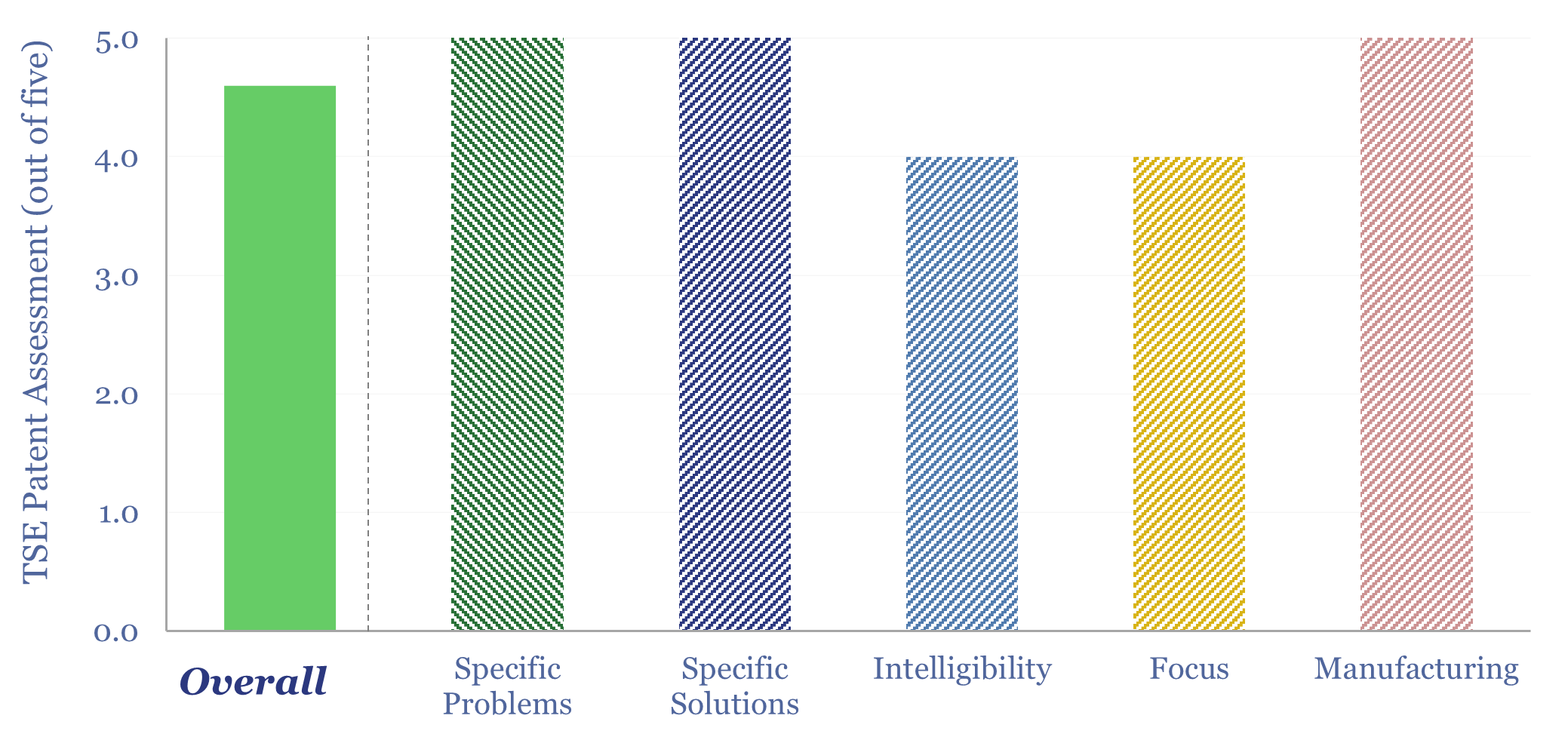

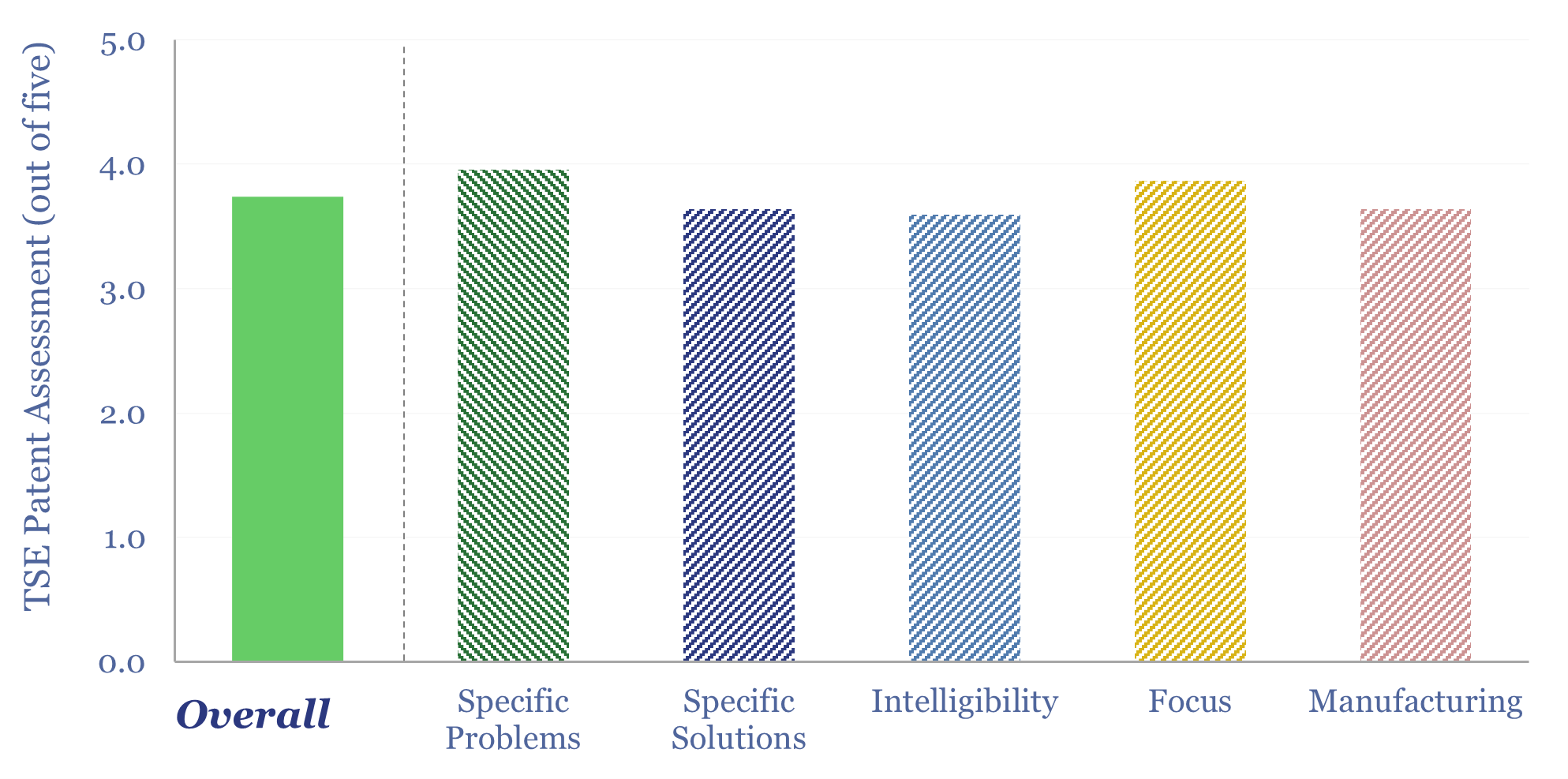

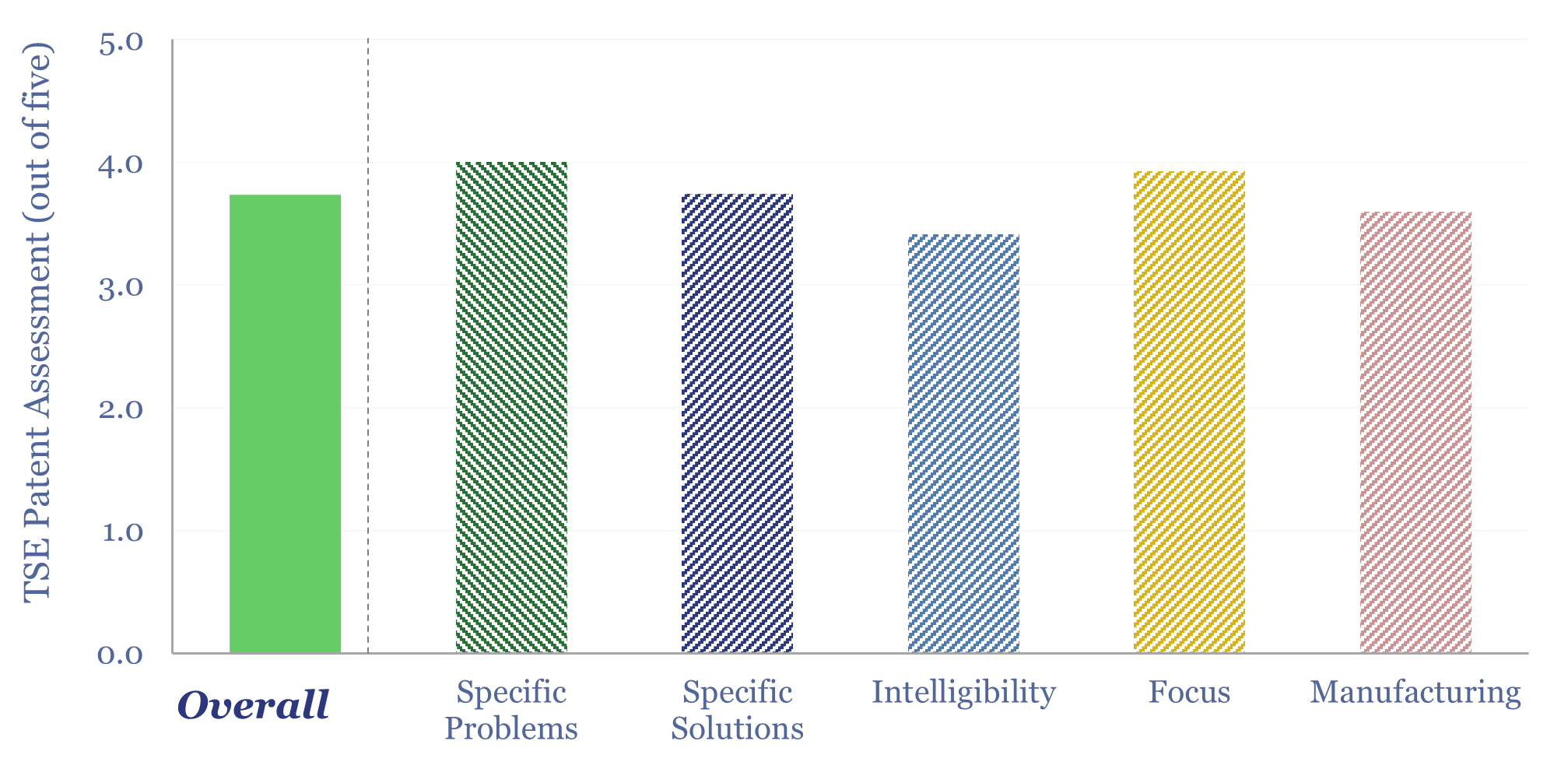

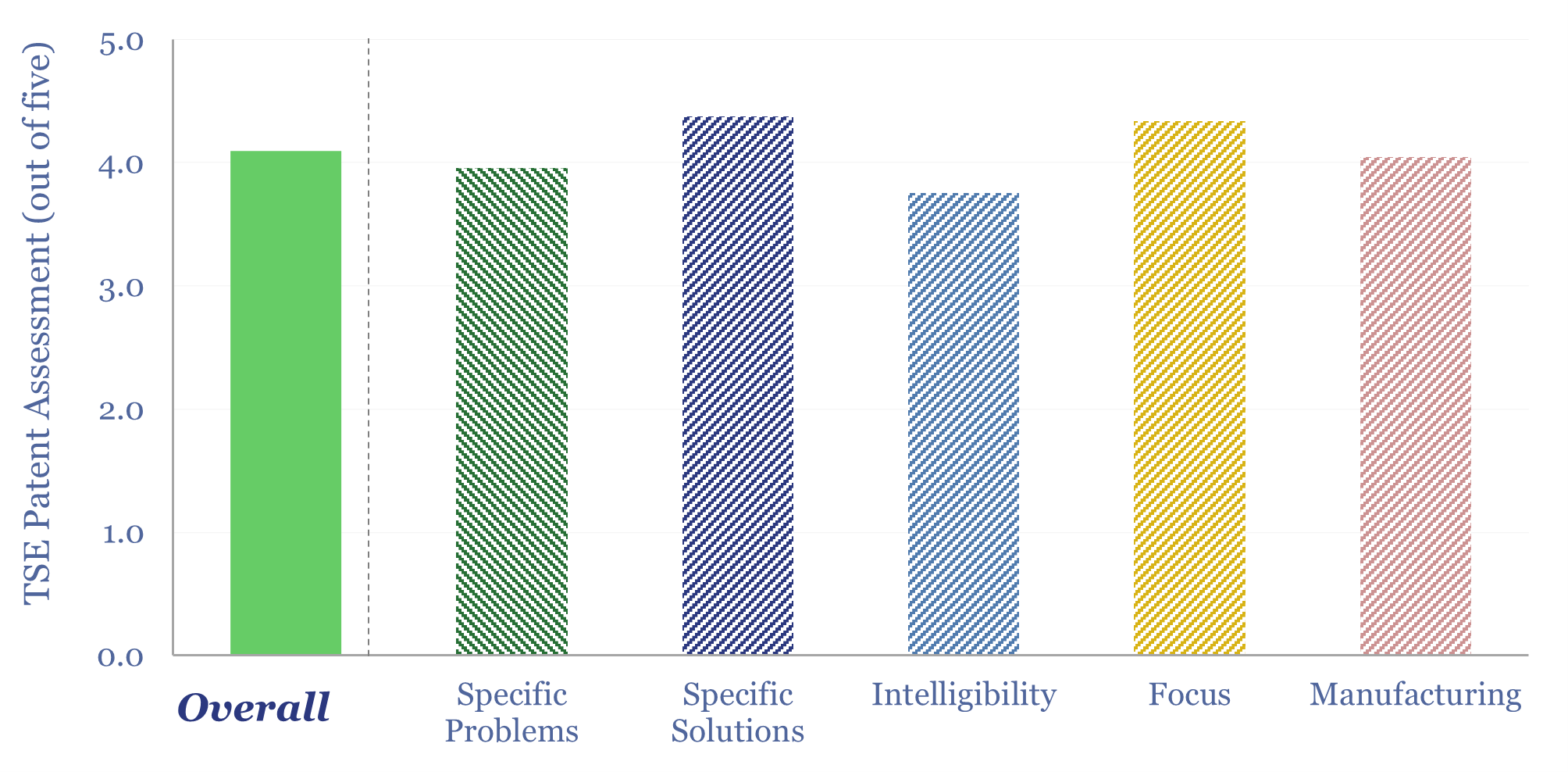

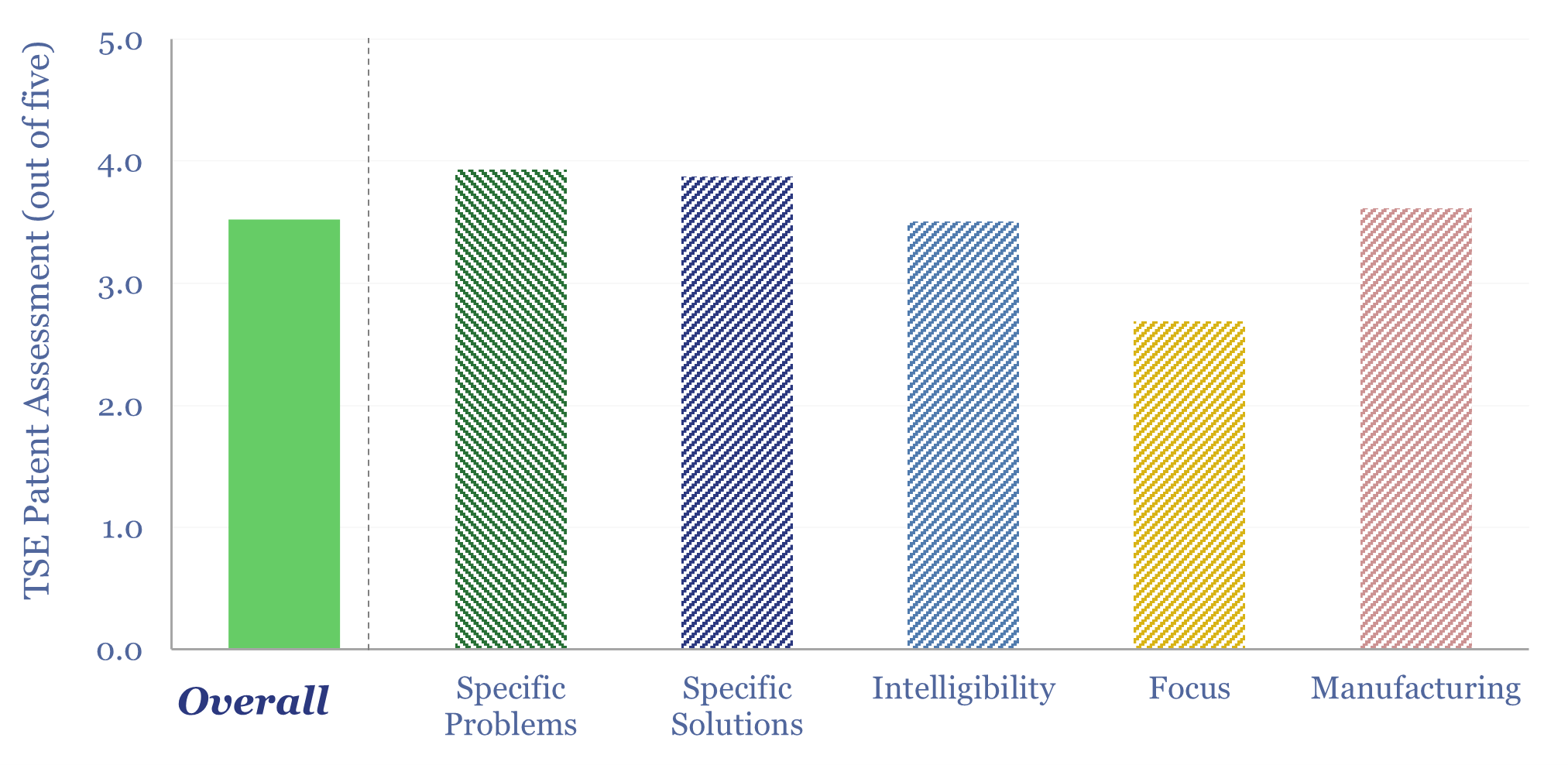

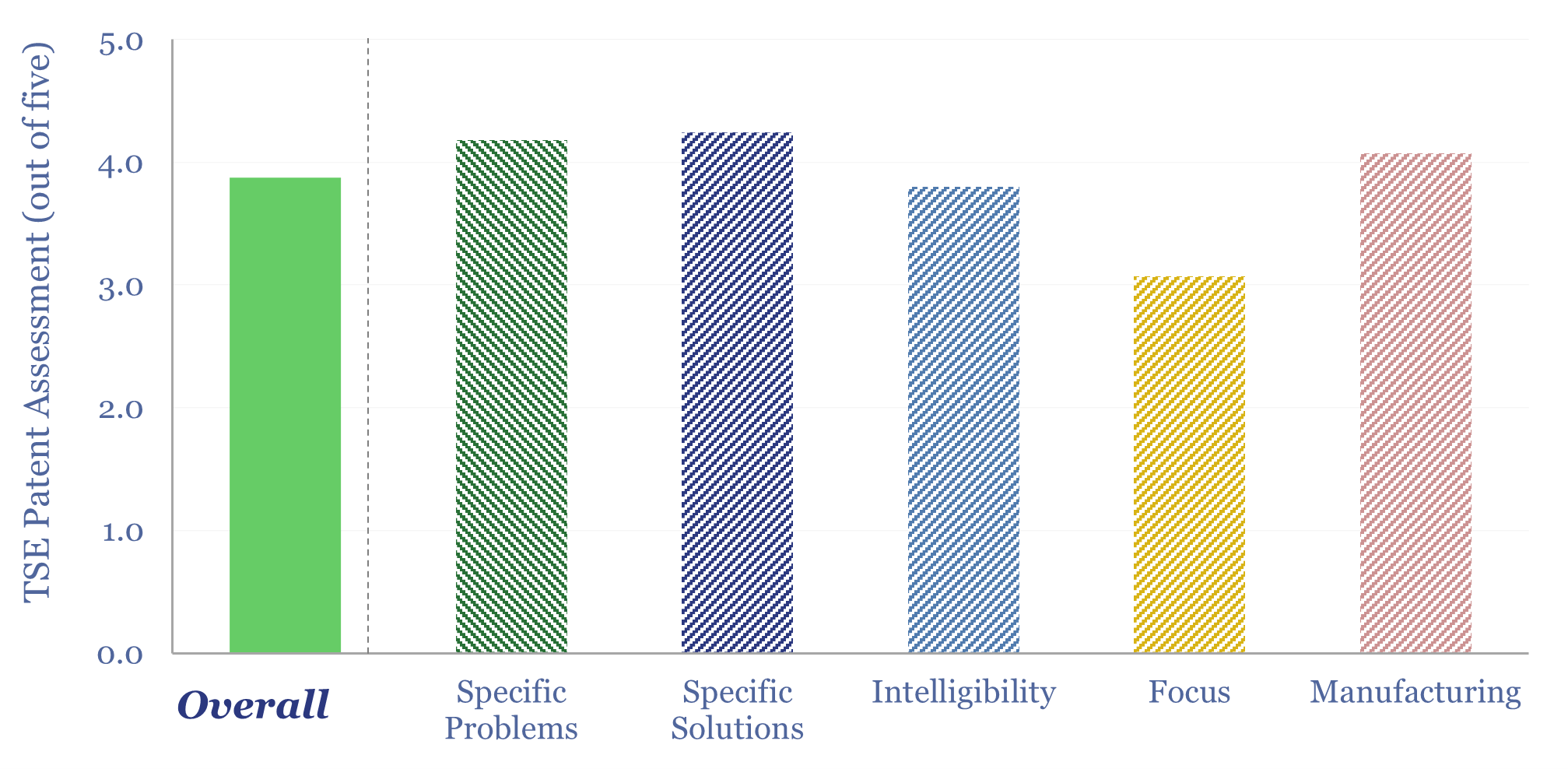

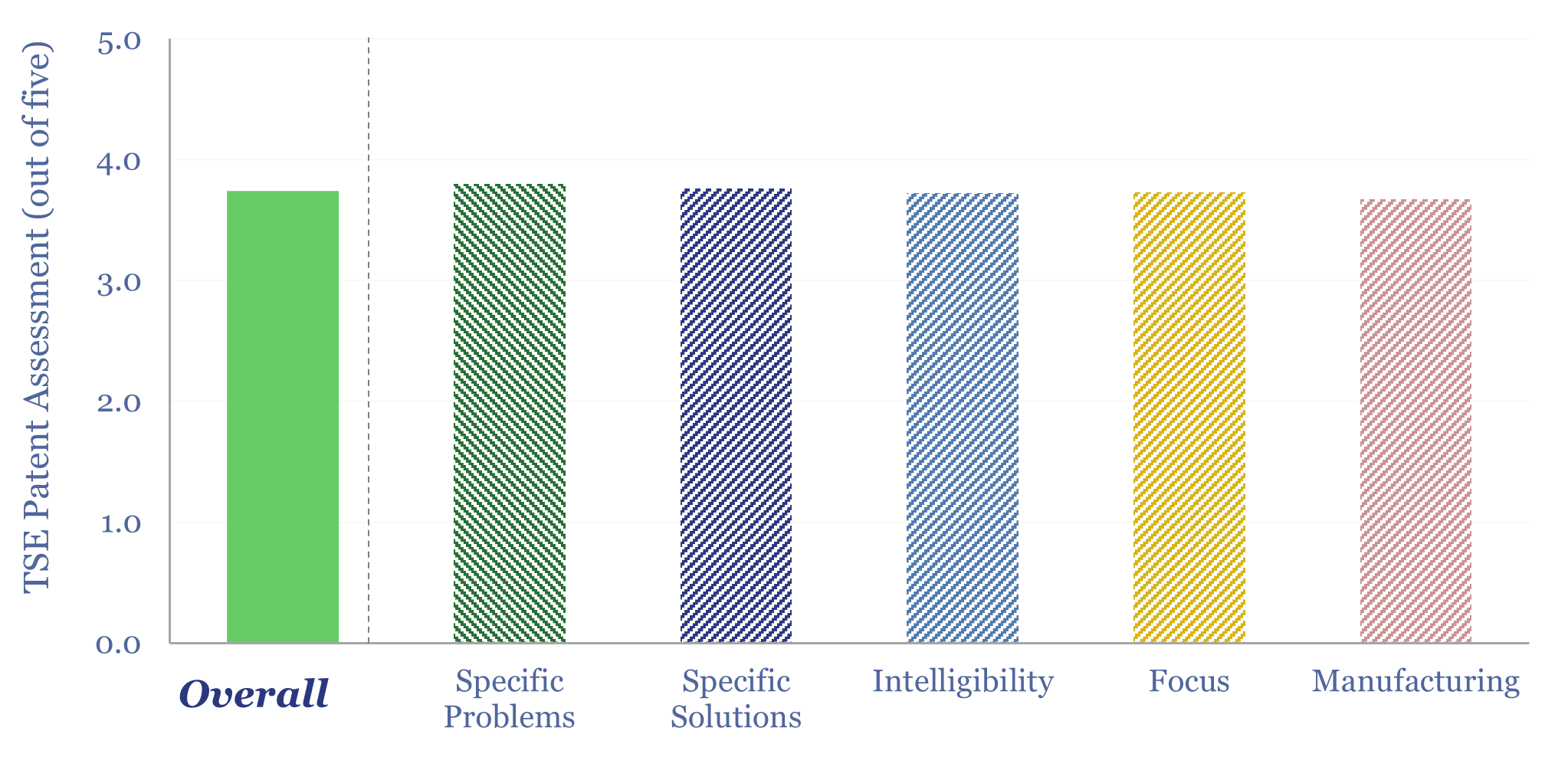

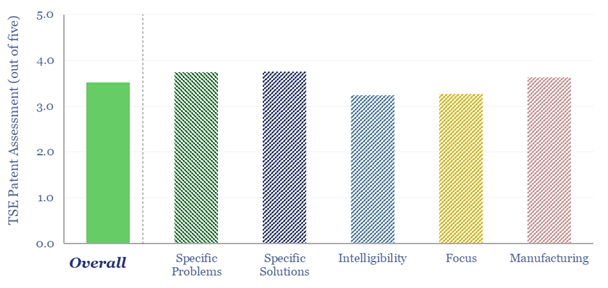

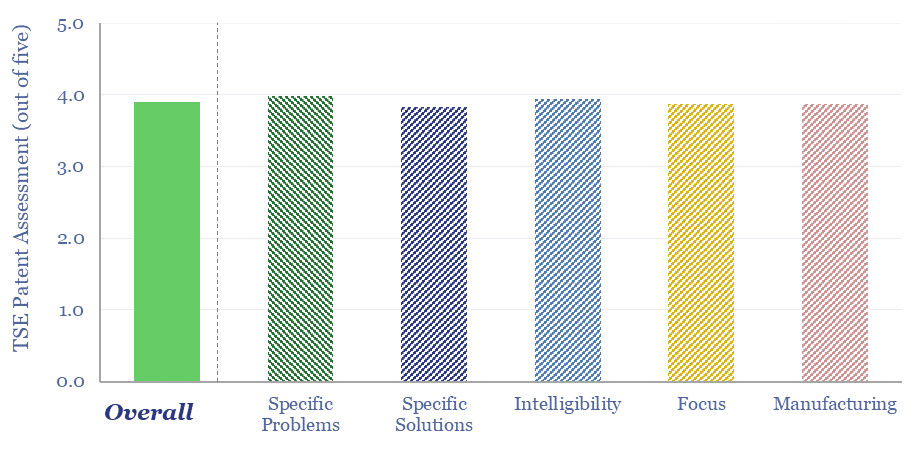

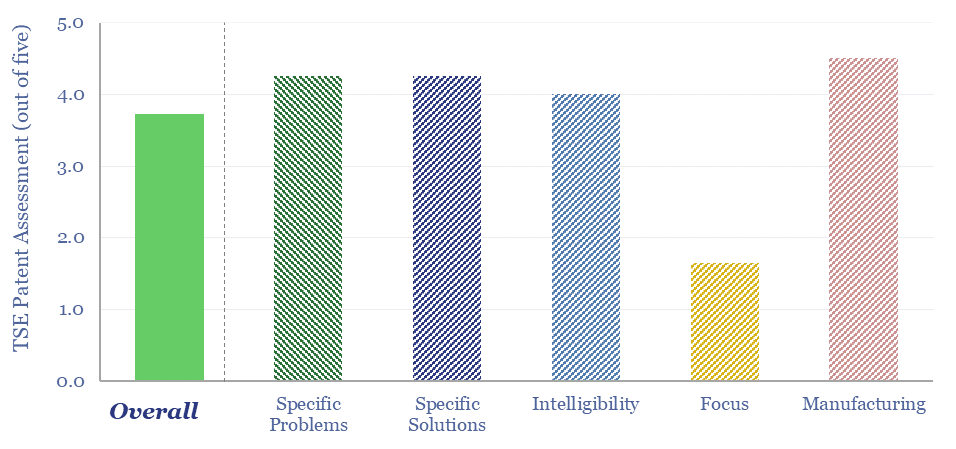

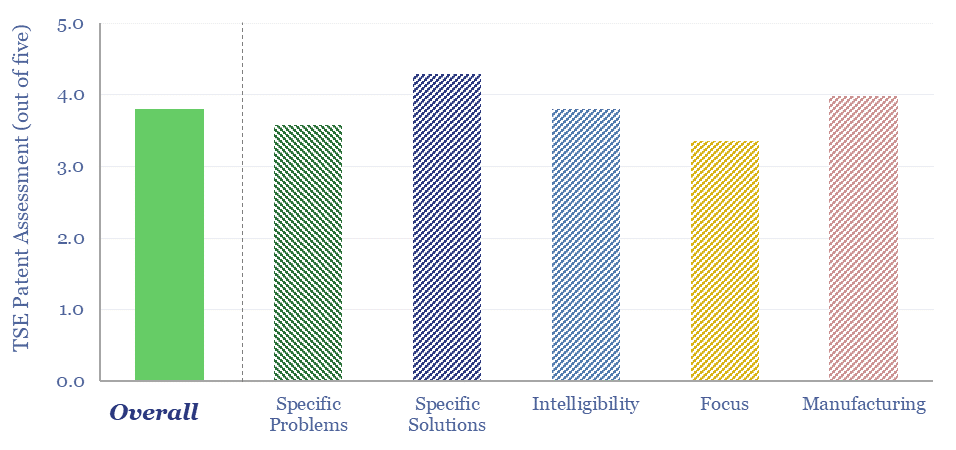

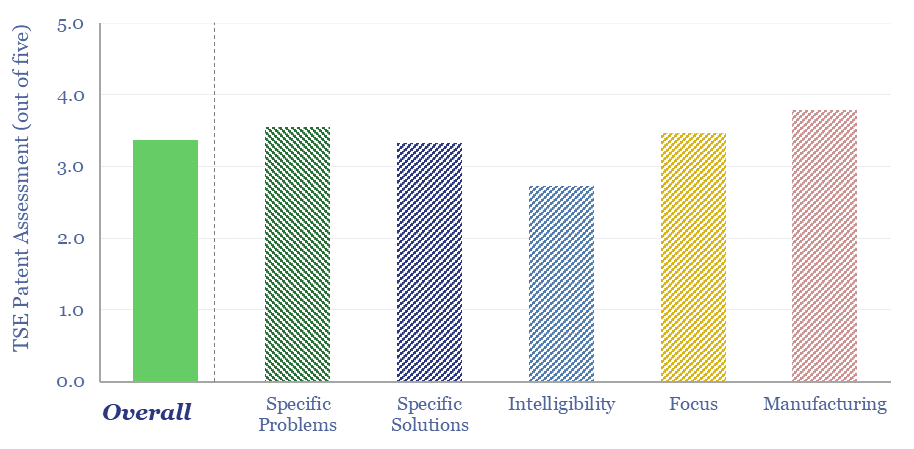

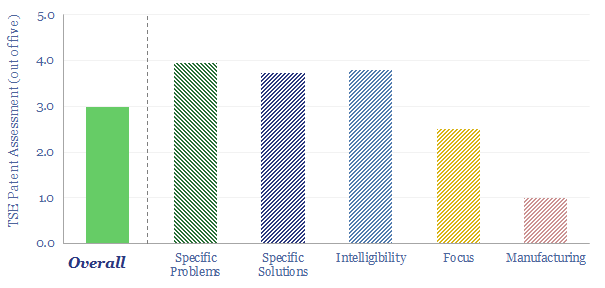

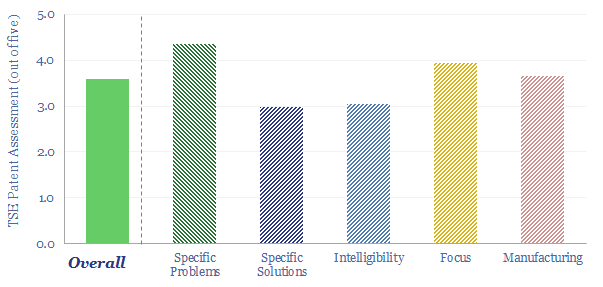

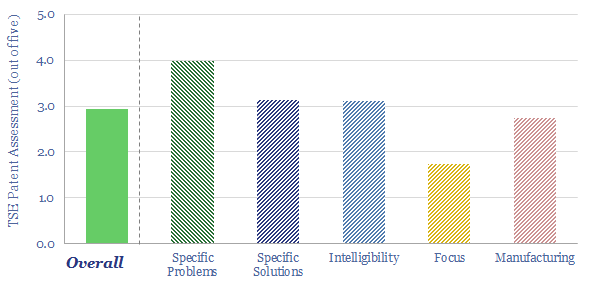

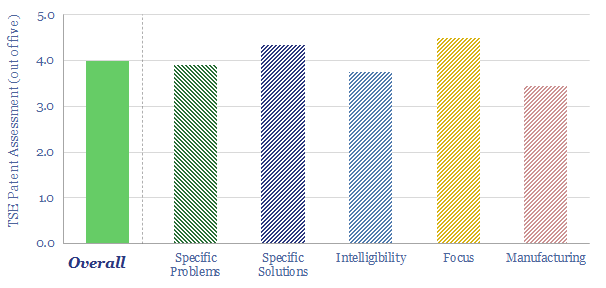

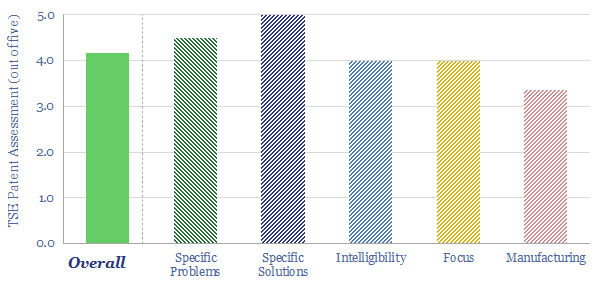

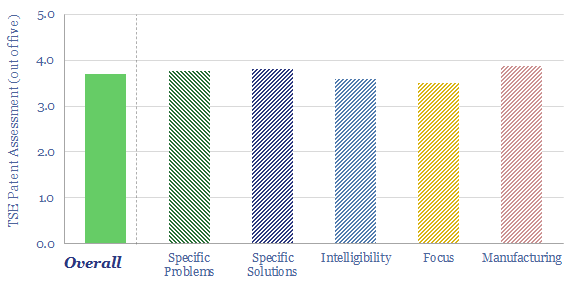

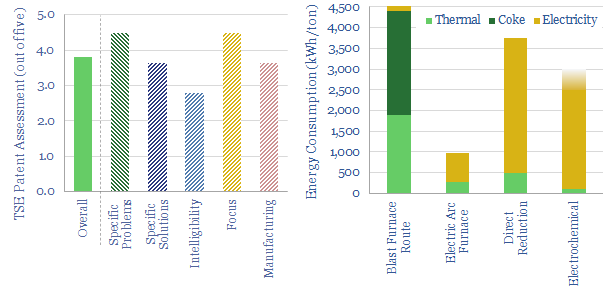

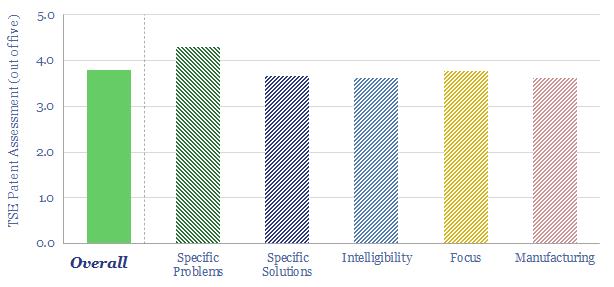

This data-file aggregates all of our patent assessments into a single reference file, so different companies’ scores can be compared and contrasted. Our average score is 3.5 out of 5.0. Skew is to the downside. Intelligibility is the biggest challenge. Scores correlate with TRL and revenues.

Download the Patent Screen?

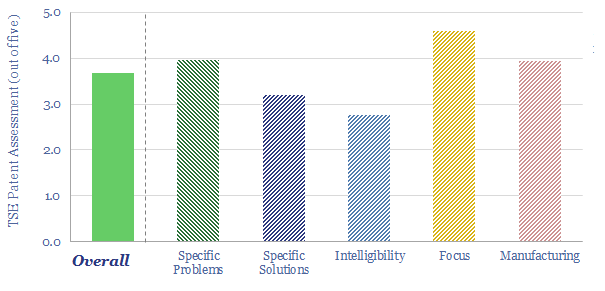

Gecko Robotics is a leader in AI+Robotics (AIR), which can save tens of millions of dollars per year, when autonomous asset inspections are used to eliminate down-time and optimize maintenance operations. The company has already reached $1.25bn of valuation. The value hinges on the marriage of specialized hardware with an AI platform. This holds lessons for the future of robotics and across the industrial world?

Download the Patent Screen?

Rare Earth recycling may recover Rare Earths at 50% lower costs and with over 90% less energy and CO2 than primary production, as long as the recycling process is simple, and only requires a small quantity of readily available commodity chemicals. This is exemplified by patents from REEcycle, which can recover over 90% of the Rare Earths in scrap magnets with over 99% purity.

Download the Patent Screen?

VoltaGrid has become the largest provider of mobile, natural gas reciprocating engines in the US, reaching GW-scale in 2025, in order to rapidly energize data centers, e-frac operations in shale, and other micro-grids in mining and industry amidst power grid bottlenecks. This data-file reviewed VoltaGrid’s mobile micro-grid technology and patents.

Download the Patent Screen?

Itron is a US-leader in smart energy meters and smart energy networks. Once you have these smart meters widely deployed across the electricity network, you can start to do really interesting things. This data-file gathers concrete examples of Itron’s smart energy network technology, based on reviewing 15 patents.

Download the Patent Screen?

Cognex machine vision technology is used to ID products, inspect products, guide robotics and gauge sizes. This data-file reviews 20 case studies, with payback periods typically below 1-year. Increasing capabilities of AI are already extending use cases for these systems. We conclude this trend will continue, and also unlock more demand for industrial robots.

Download the Patent Screen?

Water is used in heat exchangers, in data-center cooling and power plant cooling. These are interesting areas, which have featured in our research. But what opportunities to raise performance and lower water use? Ecolab water management technology monitors the composition of industrial water and then optimizes additives against scaling, fouling and corrosion. Recent patents will support the rise of AI.

Download the Patent Screen?

Exail Technologies is listed in Paris and focuses on navigational and maritime robotics. It has a range of maritime drones, with applications from mine-sweeping to assisting with offshore wind, offshore oil and gas and civil infrastructure projects in coastal waters. A key to these drones is incorporating Exail’s Inertial Navigation Systems. We have reviewed the technology.

Download the Patent Screen?

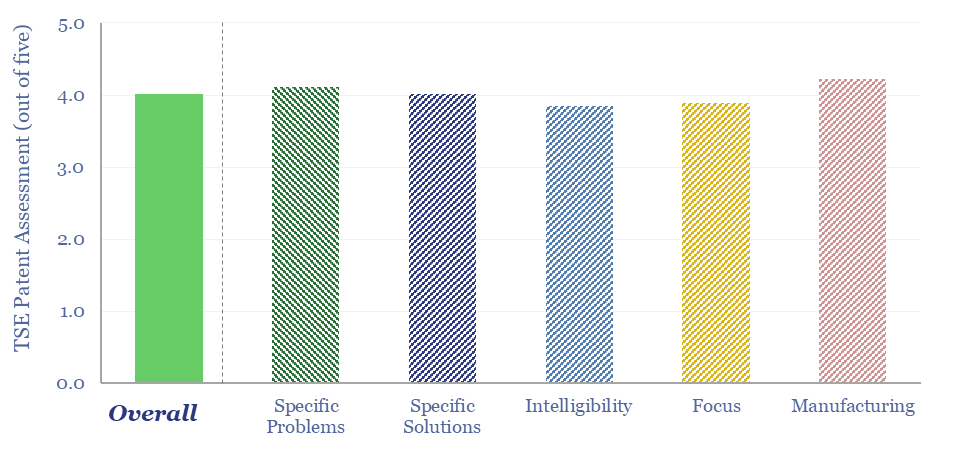

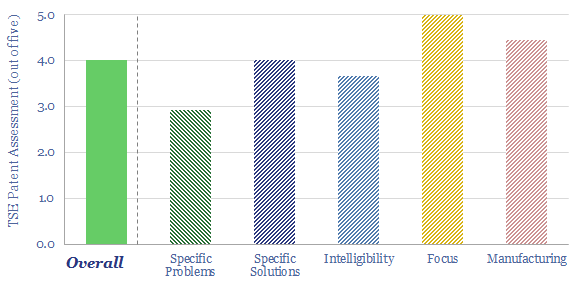

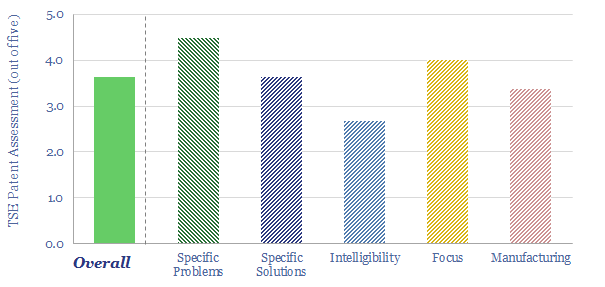

Doosan Enerbility is a power plant manufacturer, headquartered in Korea, specializing in nuclear plant construction, gas plant construction, offshore wind, civil engineering and parts manuacturing. In this patent review, we assessed Doosan Enerbility gas turbine technology. We can de-risk its claims for a 43%-efficient simple-cycle turbine, 60%+ efficient CCGT, and 1,600ºC turbine inlet temperatures.

Download the Patent Screen?

Microwave Chemical is a small-cap company, developing microwave-based heating solutions, across over a dozen use cases, from acrylic recyling, to producing food/cosmetic compounds, to carbon fiber (particularly interesting!). We reviewed a dozen of the company’s patents in this data-file, which is a Microwave Chemical technology review and finds a moat in efficient microwave heating.

Download the Patent Screen?

This data-file explores Leilac low-carbon cement technology, which separates the calcination stage, within an indirectly heated reactor, so that 98% pure CO2 can be gathered and sequestered, with requiring post-combustion CCS (amines). Patents from parent company, Calix, lock up the technology, with clear and intelligible details, although this also shows where the challenges are.

Download the Patent Screen?

This Smart Wires technology review finds that Static Synchronous Series Compensators (SmartValve) and dynamic line rating software (SUMO) can increase throughput along existing transmission lines by 20-100%+. The patents confer a visible moat around SmartValve and focus on improving electrical performance reducing deployment costs.

Download the Patent Screen?

Shanghai Electric gas turbine technology is contrasted against the Western gas turbine leaders in this data-file, based on reviewing 20 patents from 2021-24. Shanghai Electric is clearly trying to compete in this space, and the patent review uncovered interesting details into turbine temperatures, efficiencies, reliability, AI+sensing and manufacturing costs.

Download the Patent Screen?

Howmet is an engineered metals company, and the world’s #1 supplier of blades and vanes for jet engines and gas turbines. It has claimed an edge in direct-casting cooling channels (rather than drilling them) and bond coats that improve the adherence of Thermal Barrier Coatings. Our Howmet gas turbine technology review found support for these claims, via reviewing a dozen patents.

Download the Patent Screen?

Kraken Technologies is an operating system, harnessing big data across the power value chain, from asset optimization, to grid balancing, to utility customer services. We reviewed ten patents, which all harness big data, of which 65% optimize aspects of the grid, and 40% are using AI. This supports the deployment of distributed energy, renewables and EVs.

Download the Patent Screen?

Groq has developed LPUs for AI inference, which are up to 10x faster and 80-90% more energy efficient than today’s GPUs. This 8-page Groq technology review assesses its patent moat, LPU costs, implications for our AI energy models, and whether Groq could ever dethrone NVIDIA’s GPUs?

Download the Patent Screen?

Bi-Directional Bipolar Junction Transistors are an emerging category of semiconductor-based switching device, that can achieve lower on-state voltage drops than MOSFETs and softer, faster switching than IGBTs, to improve efficiency and lower component count in bi-directional power converters. This data-file screens B-TRAN patents from Ideal Power.

Download the Patent Screen?

Can we de-risk Air Products’s ammonia cracking technology in our roadmaps to net zero, which is crucial to recovering green hydrogen in regions that import green ammonia from projects such as Saudi Arabia’s NEOM. We find strong IP in Air Products’s patents. However, we still see 15-35% energy penalties and $2-3/kg of costs in ammonia cracking.

Download the Patent Screen?

This patent screen reviews Eastman’s molecular recycling technology. Specifically, Eastman is spending over $2bn, to construct 3 plants, with 380kTpa of capacity, to break down hard-to-recycle polyesters back into component monomers, with 20-80% lower CO2 intensity than virgin product. We find evidence for 30-years of fine-tuning, and can bridge to 10% IRRs if buyers pay sufficient premia for the recycled outputs.

Download the Patent Screen?

Prysmian E3X technology is a ceramic coating that can be added onto new and pre-existing power transmission cables, improving their thermal emissivity,so they heat up 30% less, have 25% lower resistive losses, and/or can carry 25% increased currents. This data-file locates the patents underpinning E3X technology, identifies the materials used, and finds a strong moat.

Download the Patent Screen?

Cemvita is a private biotech company, based in Houston, founded in 2017. It has isolated and/or engineered more than 150 microbial strains, aiming to valorize waste, convert CO2 to useful feedstocks, mine scarce metals (e.g., direct lithium extraction) and “brew” a variant of gold hydrogen from depleted hydrocarbon reservoirs. This data-file is our Cemvita Factory technology review, based on exploring its patents.

Download the Patent Screen?

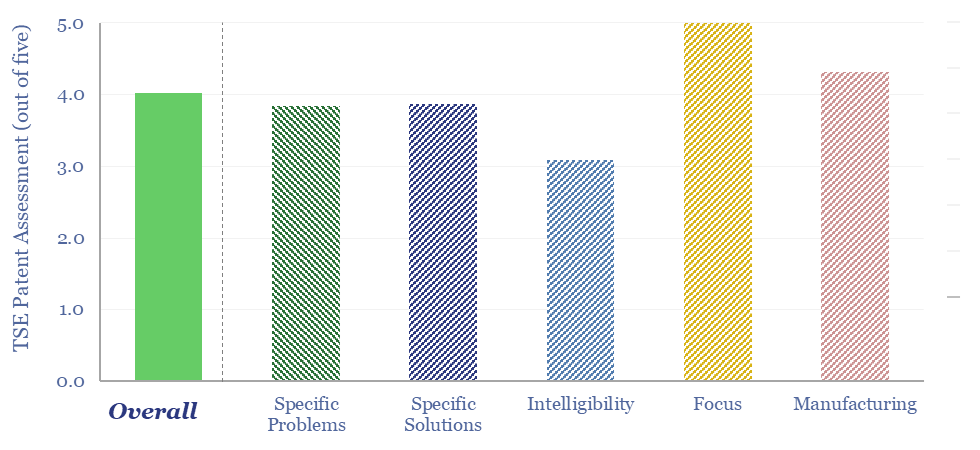

Oklo is a next-generation nuclear company, based in California, recently going public via SPAC at a $850M valuation, backed by Sam Altman, of Y-Combinator and OpenAI fame. Oklo’s fast reactor technology absorbs high energy neutrons in liquid metal and targets ultimate costs of 4c/kWh. What details can we infer from assessing Oklo’s patents, and can we de-risk the technology in our roadmap to net zero?

Download the Patent Screen?

Cummins is a power technology company, listed in the US, specializing in diesel engines, underlying components, exhaust gas after-treatment, diesel power generation and pivoting towards hydrogen. We reviewed 80 patents from 2023-24. What outlook for Cummins technology and verticals in the energy transition?

Download the Patent Screen?

Is Babcock and Wilcox’s BrightLoop technology a game-changer for producing low-carbon hydrogen from solid fuels, while also releasing a pure stream of CO2 for CCS? Conclusions and deep-dive details are covered in this data-file, allowing us to guess at BrightLoop’s energy efficiency and a moat around Babcock’s reactor designs?

Download the Patent Screen?

This data-file is our LONGi technology review, based on recent patent filings. The work helps us to de-risk increasingly efficient solar modules, a growing focus on perovskite-tandem cells, and low-cost solar modules, with simple manufacturing techniques that may ultimately displace bottlenecked silver from electrical contacts. Key conclusions in the data-file.

Download the Patent Screen?

Origen Carbon Solutions is developing a novel DAC technology, producing CaO sorbent via the oxy-fuelled calcining of limestone with no net CO2 emissions. It is similar to the NET Power cycle, but adapted for a limestone kiln. The concept is very interesting. Our base case costs are $200-300/ton of CO2. This data-file contains our Origen DAC technology review.

Download the Patent Screen?

Solar encapsulants are 300-500μm thick films, protecting solar cells from moisture, dirt and degradation; electrically insulating them at 4 x 10^15 Ωcm resistivity; and yet allowing 90% light transmittance. The industry is moving away from commoditized EVA towards specialized blends of co-polymers and additives. Is there a growing moat around Mitsui Chemicals’ solar encapsulants?

Download the Patent Screen?

This data-file reviews Verdox DAC technology, optimizing polyanthraquinones and polynaphthoquinones, then depositing them on porous carbon nano-tube scaffolds. These quinones are shown to selectively adsorb CO2 when a voltage is applied, then desorb them when a reverse voltage is applied, unlocking 70% lower energy penalties than incumbent DAC?

Download the Patent Screen?

Solvay is a chemicals company with growing exposure to battery materials, especially the PVDF binders that hold together active materials in the electrodes. But also increasingly in electrolyte solvents, salts and additives. Interestingly, our patent review finds optimizations of this overall system can improve the longevity and energy density of batteries, which may also lead to consolidation across the battery supply chain?

Download the Patent Screen?

Pressure exchangers transfer energy from a high-pressure fluid stream to a low-pressure fluid stream, and can save up to 60% input energy. Energy Recovery Inc is a leading provider of pressure exchangers, especially for the desalination industry, and increasingly for refrigeration, air conditioners, heat pump and industrial applications. Our technology review finds a moat.

Download the Patent Screen?

Our Plug Power technology review is drawn from the company’s recent patent filings, which offer some of the most detailed disclosures we have ever seen into the manufacturing of PEM electrolysers and fuel cells, underlying catalyst materials, membranes and their manufacturing. One patent seems like a breakthrough. Other patents candidly presented challenges.

Download the Patent Screen?

MIRALON is an advanced material, being commercialized by Huntsman, purifying carbon nanotubes from the pyrolysis of methane and also yielding turquoise hydrogen. This data-file reviews MIRALON technology, patents, and a strong moat. Our model sees 15% IRRs if Huntsman reaches a medium-term cost target of $10/kg MIRALON and $1/kg H2.

Download the Patent Screen?

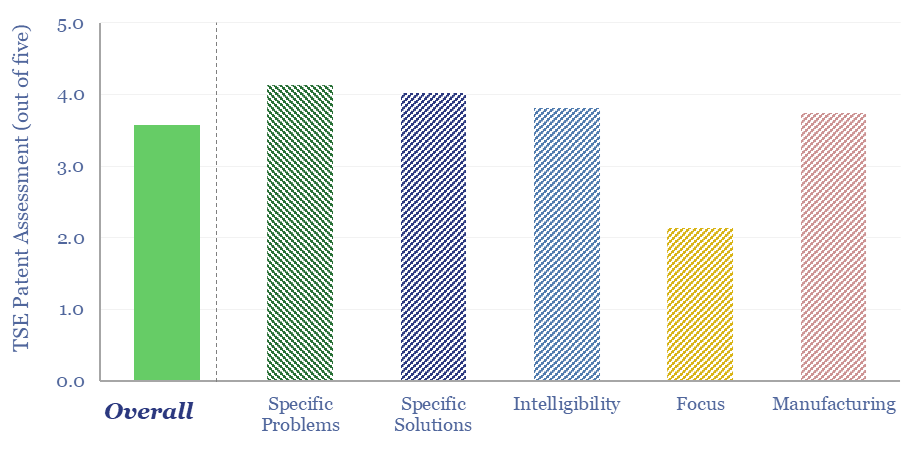

This data-file reviews Bloom Energy’s solid oxide fuel cell technology. What surprised us most was a candid overview of degradation pathways of solid oxide fuel cells, a focus on improving the longevity of fuel cells, albeit this sometimes seems to be via heavy uses of Rare Earth metals, and increasing complexity. The patents do suggest a moat around Bloom Energy fuel cell technology.

Download the Patent Screen?

Newlight is converting (bio-)methane and air into polyhydroxybutyrate (PHB), a type of polyhydroxyalkanoate (PHA), a biodegradable bioplastic which it markets as AirCarbon. The product is ‘carbon negative’, biodegradable, strong, ‘never soggy’, dishwasher safe. Our AirCarbon technology review found some good underlying innovations, but was unable to de-risk cost and capex aspirations.

Download the Patent Screen?

Montana Technologies is developing AirJoule, an HVAC technology that uses metal organic frameworks, to lower the energy costs of air conditioning by 50-75%. The company is going public via SPAC and targeting first revenues in 2024. Our AirJoule technology review finds strong rationale, technical details and challenges.

Download the Patent Screen?

Alterra Energy has steadily been refining its plastic recycling technology since 2017. The company recently signed license agreements with Neste and Freepoint. The technology is a continuous reactor, with seven discrete stages, using scavengers to remove contaminants, and patented hardware to minimize fouling and devolatilize chars.

Download the Patent Screen?

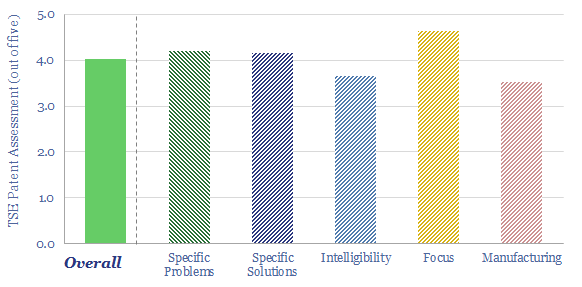

Advantage is a Montney gas producer, which recently sourced a $300M investment from Brookfield to scale up its Entropy23 amine blend for natural-gas CCS. Entropy has captured 90-93% of the CO2 at the first pilot plant at Glacier, Alberta, with 2.4 GJ/ton reboiler duty, 40% below MEA. This 7-page report confirms a moat around the technology and raises three challenges.

Download the Patent Screen?

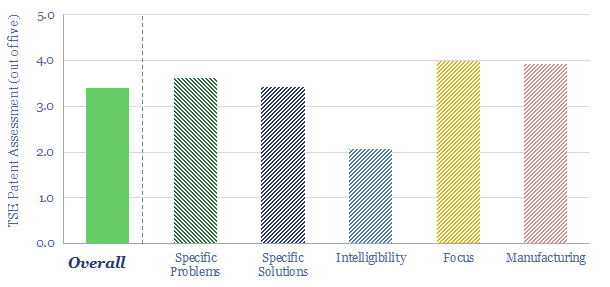

Topsoe autothermal reforming technology aims to maximize the uptime and reliability of blue hydrogen production, despite ultra-high combustion temperatures from the partial oxidation reaction, while achieving high energy efficiency, 90-97% CO2 capture and

Download the Patent Screen?

Electra is developing an electrochemical refining process, to convert iron ore into high purity iron, and ultimately into steel, using only renewable electricity. It has raised c$100M, gained high-profile backers, and is working towards a test plant. This 9-page note reviews an exceptionally detailed patent, finds clear innovations, but also some remaining risks and cost question marks.

Download the Patent Screen?

Aker Carbon Capture is a public company, listed in Norway, with c120 permanent employees. It has developed novel solvents for post-combustion carbon capture, modular CCS plants (JustCatch, at 40-100kTpa, and BigCatch at >400kTpa). The company aims to secure contracts for 10MTpa of CCS by 2025. This technology review looks for a moat in the patents.

Download the Patent Screen?

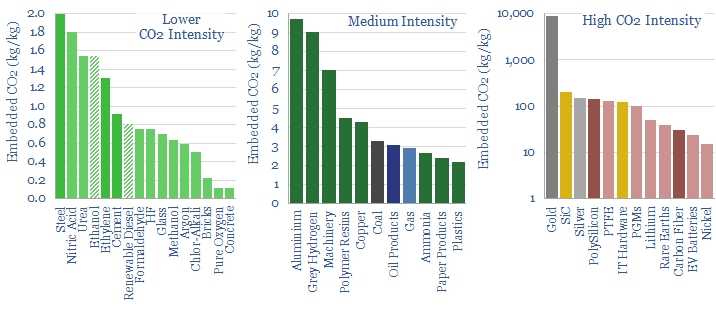

This data-file tabulates the energy intensity and CO2 intensity of materials, in tons/ton of CO2, kWh/ton of electricity and kWh/ton of total energy use per ton of material. The build-ups are based on 160 economic models that we have constructed to date, and simply intended as a helpful summary reference. Our key conclusions on CO2 intensity of materials are below.

Download the Data?

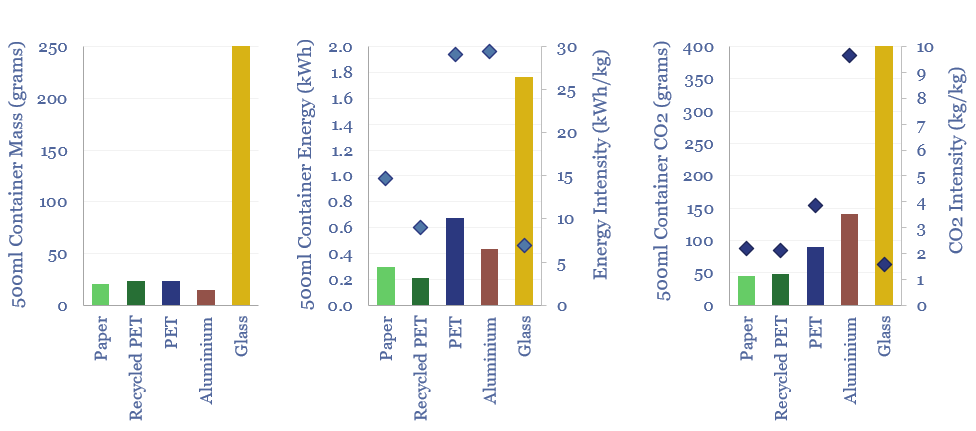

The energy intensity of plastic products and the CO2 intensity of plastics are built up from first principles in this data-file. Virgin plastic typically embeds 3-4 kg/kg of CO2e. But compared against glass, PET bottles embed 60% less energy and 80% less CO2. Compared against virgin PET, recycled PET embeds 70% less energy and 45% less CO2. Aluminium packaging is also highly efficient.

Download the Data?

This data-file aggregates granular data into US gas transmission, by company and by pipeline, for 40 major US gas pipelines which transport 45TCF of gas per annum across 185,000 miles; and for 3,200 compressors at 640 related compressor stations.

Download the Data?

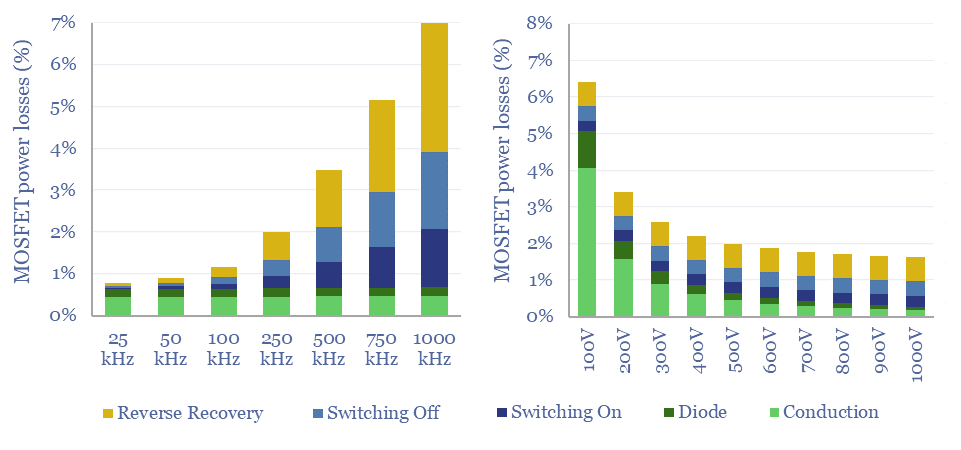

MOSFETs are fast-acting digital switches, used to transform electricity, across new energies and digital devices. MOSFET power losses are built up from first principles in this data-file, averaging 2% per MOSFET, with a range of 1-10% depending on voltage, switching, on resistance, operating temperature and reverse recovery charge.

Download the Data?

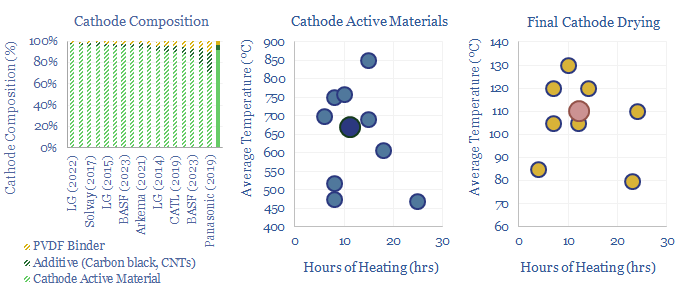

Lithium ion batteries famously have cathodes containing lithium, nickel, manganese, cobalt, aluminium and/or iron phosphate. But how are these cathode active materials manufactured? This data-file gathers specific details from technical papers and patents by leading companies such as BASF, LG, CATL, Panasonic, Solvay and Arkema.

Download the Data?

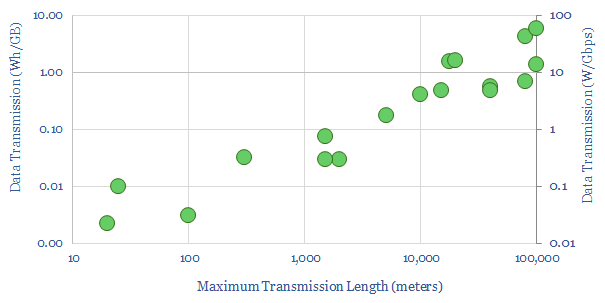

What is the energy intensity of fiber optic cables? Our best estimate is that moving each GB of internet traffic through the fixed network requires 40Wh/GB of energy, across 20 hops, spanning 800km and requiring an average of 0.05 Wh/GB/km. Generally, long-distance transmission is 1-2 orders of magnitude more energy efficient than short-distance.

Download the Data?

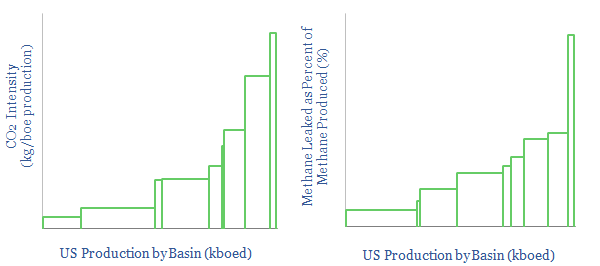

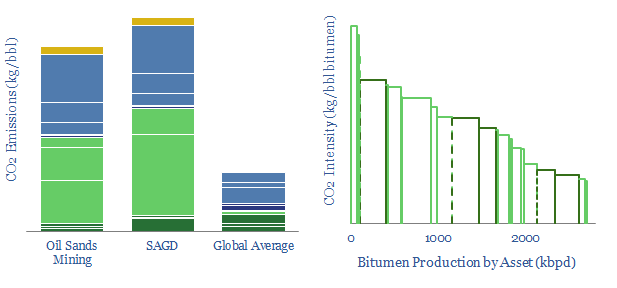

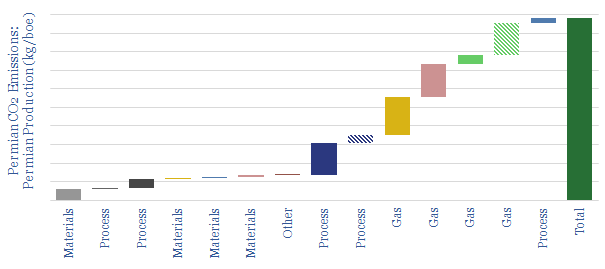

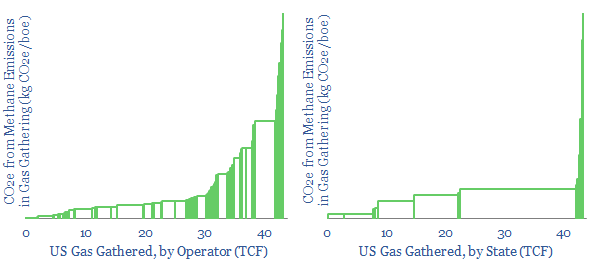

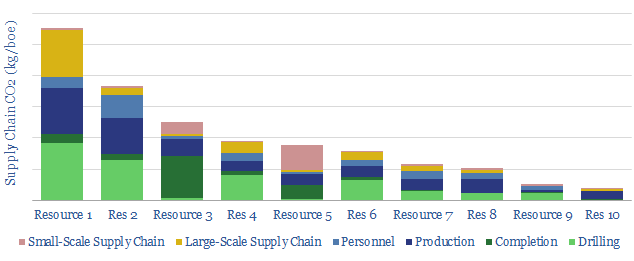

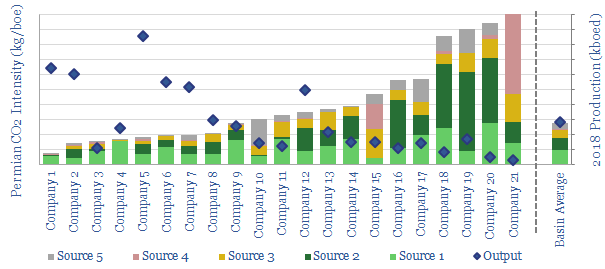

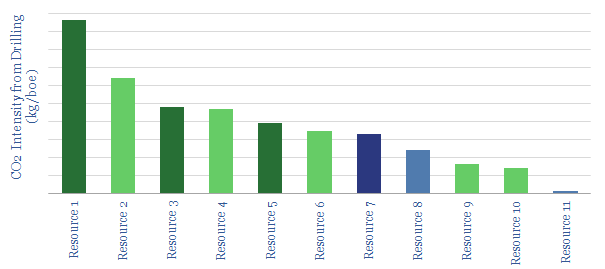

The CO2 intensity of oil and gas production is tabulated for 425 distinct company positions across 12 distinct US onshore basins in this data-file. Using the data, we can aggregate the total upstream CO2 intensity in (kg/boe), methane leakage rates (%) and flaring intensity (in mcf/boe), by company, by basin and across the US Lower 48.

Download the Data?

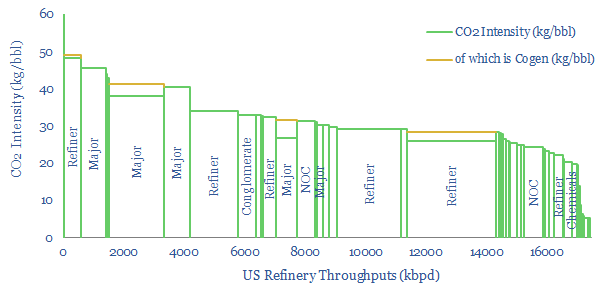

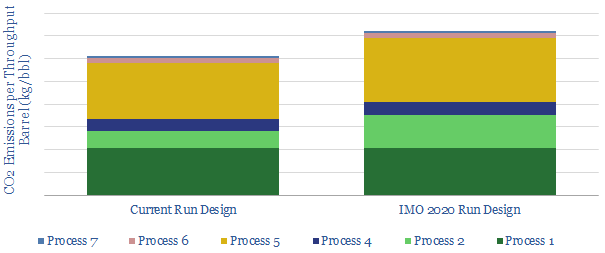

This US refinery database covers 125 US refining facilities, with an average capacity of 150kbpd, and an average CO2 intensity of 33 kg/bbl. Upper quartile performers emitted less than 20 kg/bbl, while lower quartile performers emitted over 40 kg/bbl. The goal of this refinery database is to disaggregate US refining CO2 intensity by company and by facility.

Download the Data?

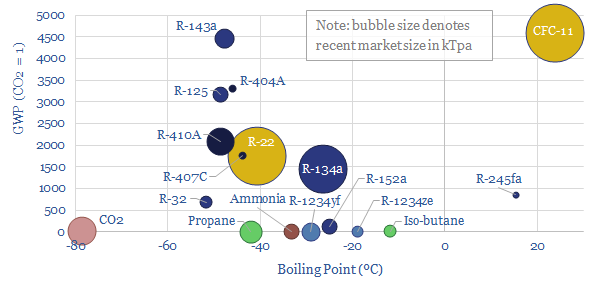

This data-file is a breakdown of c1MTpa of refrigerants used in the recent past for cooling, across refrigerators, air conditioners, in vehicles, industrial chillers, and increasingly, heat pumps. The market is shifting rapidly towards lower-carbon products, including HFOs, propane, iso-butane and even CO2 itself. We still see fluorinated chemicals markets tightening.

Download the Data?

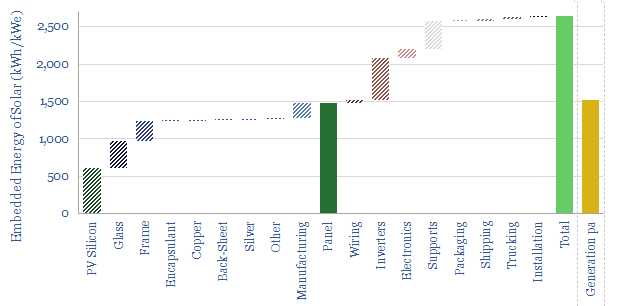

What is the energy payback and embedded energy of solar? We have aggregated the consumption of 10 different materials (in kg/kW) and around 10 other energy-consuming line-items (in kWh/kW). Our base case estimate is 2.5 MWH/kWe of solar and an energy payback of 1.5-years. Numbers and sensitivities can be stress-tested in the data-file.

Download the Data?

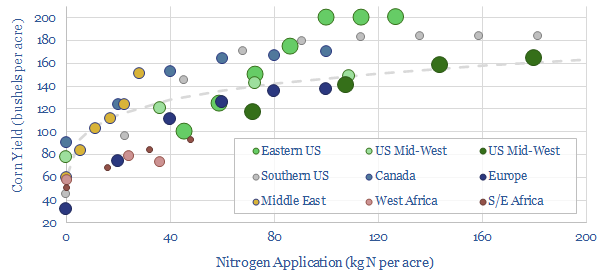

How much does fertilizer increase crop yields? Aggregating all of the global data, a good rule of thumb is that up to 200kg of nitrogen can be applied per acre, increasing corn crop yields from 60 bushels per acre (with no fertilizer) to 160 bushels per acre (at 200 kg/acre). But the relationship is logarithmic, with diminishing returns.

Download the Data?

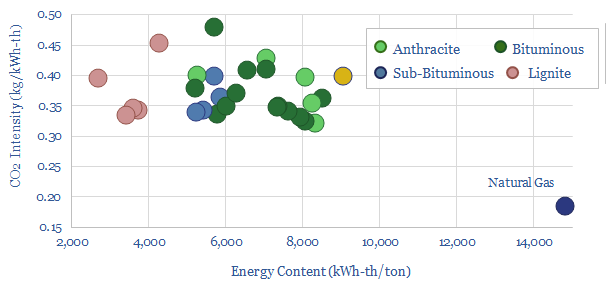

The CO2 intensity of coal is estimated at 0.37kg/kWh of thermal energy, at a typical coal grade comprising 63% carbon and 6,250 kWh/ton of energy content. This is the average across 25 samples in our data-file, while moisture, ash and sulphur are also appraised. Coal is 2x more CO2 intensive than natural gas.

Download the Data?

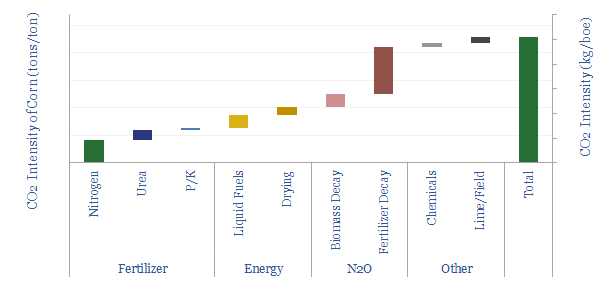

The CO2 intensity of producing corn averages 0.23 tons/ton, or 75kg/boe. 50% is from N2O emissions, a powerful greenhouse gas, from the breakdown of nitrogen fertilizer. Producing 1 kWh of food energy requires 9 kWh of fossil energy.

Download the Data?

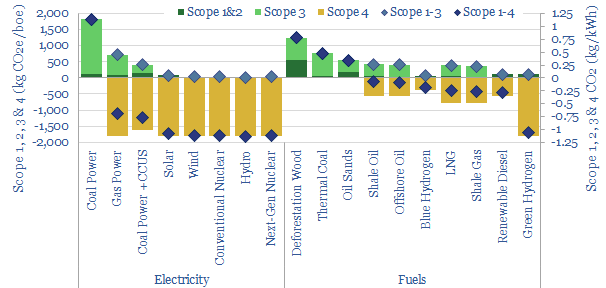

Scope 4 CO2 emissions capture the CO2 that is avoided by use of a product. Many energy investments with positive Scope 1-3 emissions have deeply negative Scope 1-4 emissions. Numbers are quantified and may offer a more constructive approach to decarbonization investments.

Download the Data?

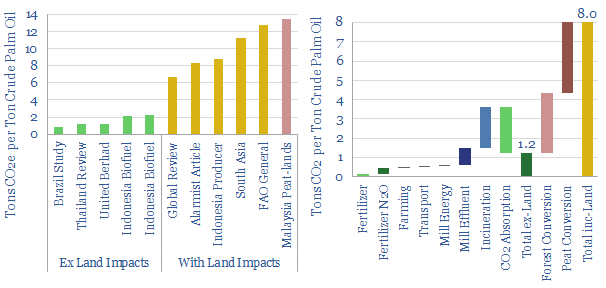

Global palm oil production runs at 80MTpa, for food, HPC and bio-fuels. Carbon intensity is 1.2 tons CO2e per ton of crude palm oil, excluding land use impacts, and 8.0 tons/ton on a global basis including land use impacts. This means once a bio-fuel has more than c35% palm oil in its feedstock, it is likely to be higher carbon than conventional diesel.

Download the Data?